Highlights of the Week

- Markets opened the week unsettled by reports that President Trump plans to nominate Kevin Warsh as the next Fed Chair, reviving concerns over balance-sheet discipline and Federal Reserve credibility.

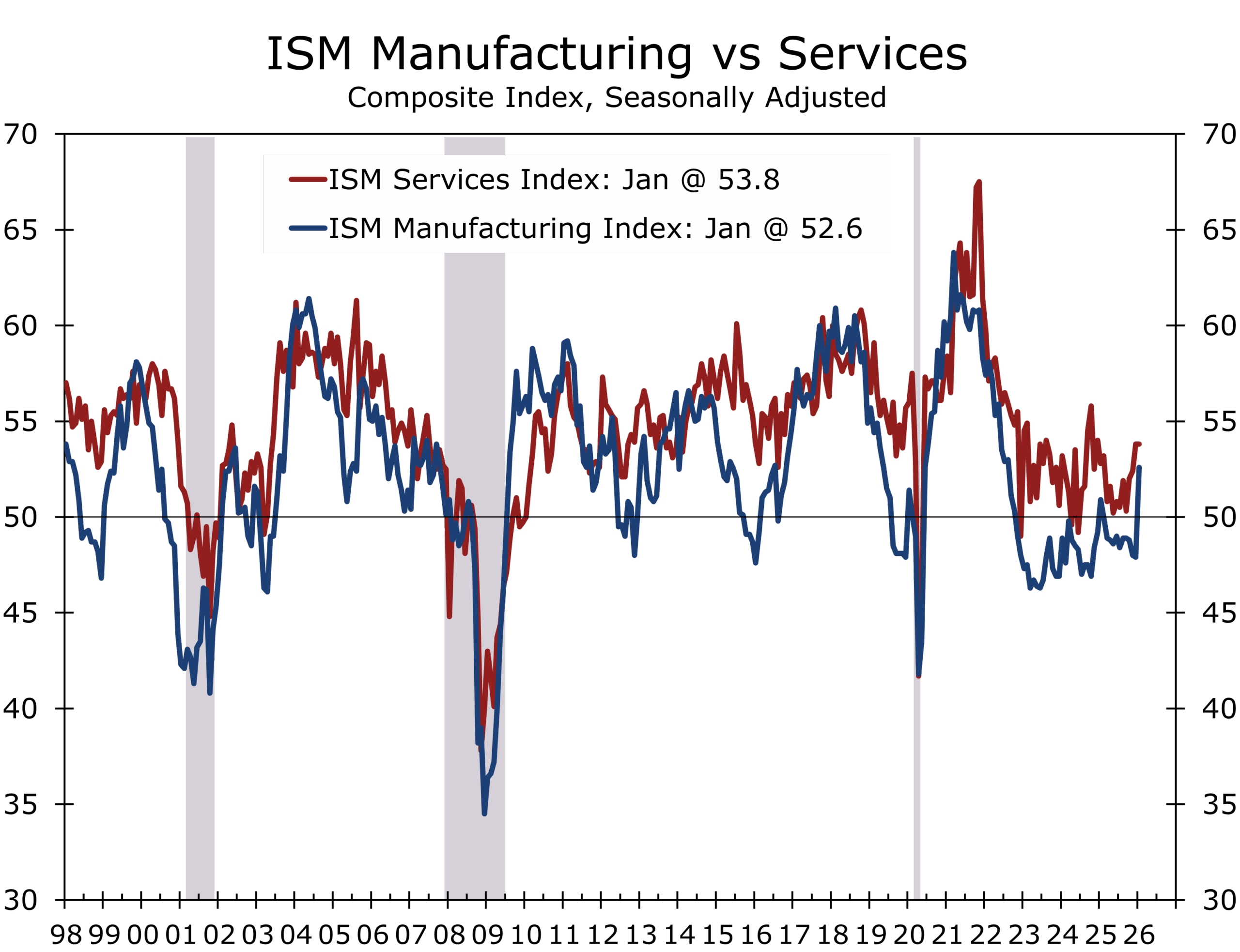

- The ISM Manufacturing Index delivered its strongest reading in three years, possibly signaling tentative improvement after a prolonged industrial slump.

- Labor market data point to cooling through slower hiring and low turnover, not a surge in layoffs.

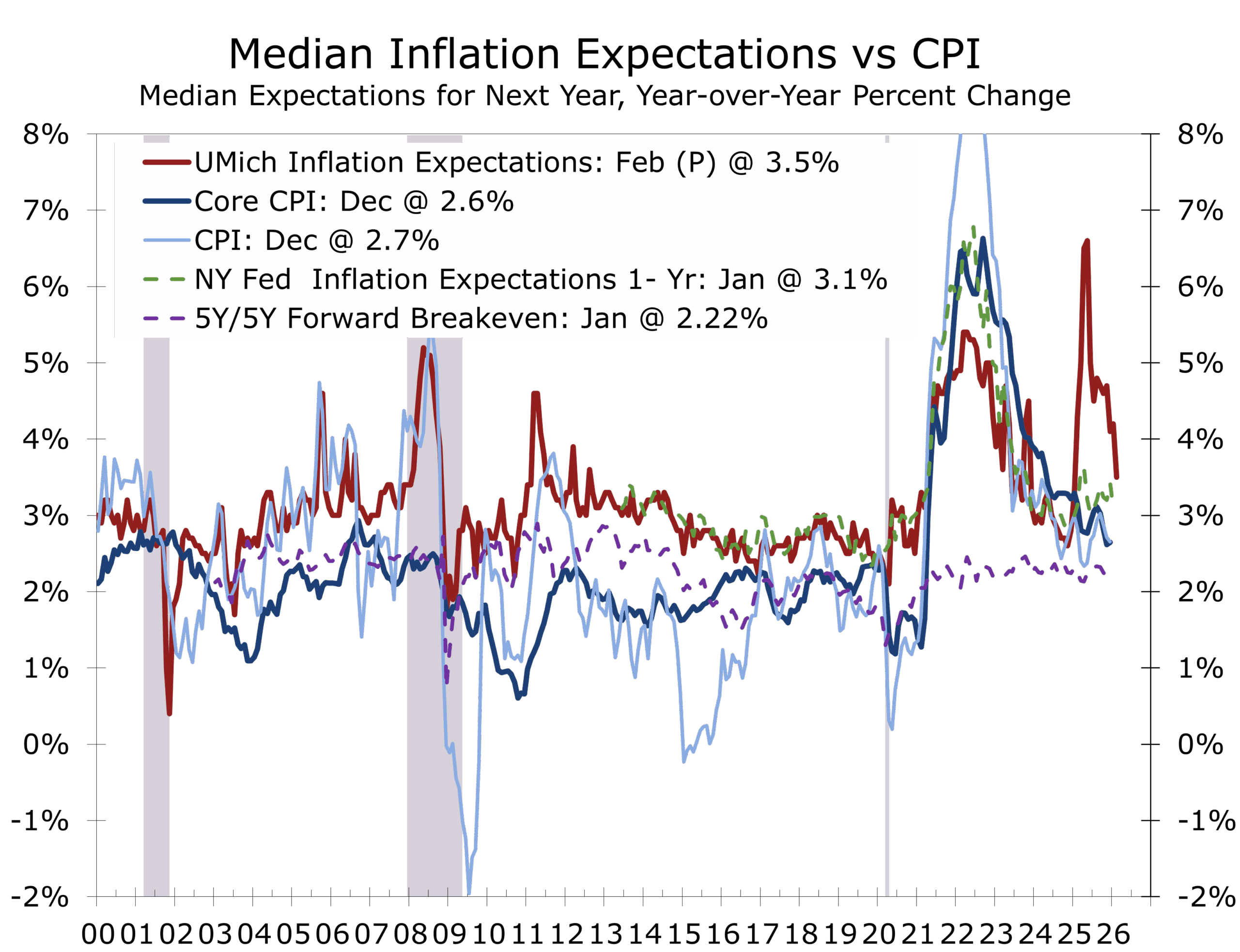

- Consumer inflation expectations continued to ease across multiple surveys.

- Despite early volatility, the Dow Jones Industrial Average reached an all-time high, underscoring late-cycle resilience and selective risk appetite.

Markets Test the Reins

The week began on uneasy footing after reports that President Trump is considering appointing Kevin Warsh as the next Chair of the Federal Reserve. Markets were quick to dust off old priors. Warsh’s reputation as a balance-sheet hawk revived deeper concerns about whether the Fed is prepared to reassert credibility after more than a decade of extraordinary accommodation. For years, balance-sheet expansion acted as a persistent tailwind for asset prices, compressing credit spreads and suppressing volatility. Even without an imminent policy shift, the prospect of renewed discipline was enough to put investors on notice.

What makes this moment especially difficult to read is that productivity signals are emerging again before confidence, much as they did in the early 1990s. Markets are being asked to price gains that appear real but remain uneven, capital-intensive, and difficult to measure in real time.

Early market weakness was led by technology. Investors continued to reassess the cost, capital intensity, and evolving profit model of the AI buildout. The debate has shifted. AI’s transformative potential is no longer in question; the uncertainty lies in returns, timing, and who ultimately captures the surplus. Software stocks have been particularly vulnerable as investors weigh whether AI enhances pricing power or compresses it through commoditization.

Against that unsettled backdrop, last week’s economic data proved more constructive than early market sentiment implied.

The best ISM Manufacturing reading in three years may signal a turn in the factor sector.

The ISM Manufacturing Index surprised decisively to the upside, jumping 4.7 points to 52.6, its best reading in roughly three years. While activity is now back above the key 50 threshold separating expansion from contraction, the internal composition was notably stronger. New orders and production improved, supplier delivery times lengthened modestly, prices paid remained contained, and inventories stayed lean.

After a prolonged slump, manufacturing appears to be stabilizing, particularly in capital-intensive, defense-linked, and reshoring-oriented segments. A sustained improvement, however, will likely require greater stability on the tariff and trade front.

The ISM Services report was steadier, consistent with a services sector that is slowing but not rolling over. Business activity held firm, while new orders and employment softened. Pricing pressures moderated further. Together, the ISM surveys point to an economy rotating away from post-pandemic excess toward a more sustainable growth profile

Labor market indicators reinforced that theme. ADP private payroll growth came in below expectations, reflecting a gradual downshift in hiring momentum. Job gains remain concentrated in healthcare and population-driven services, while professional and business services continue to lag. Firms are adjusting primarily through hiring restraint rather than layoffs.

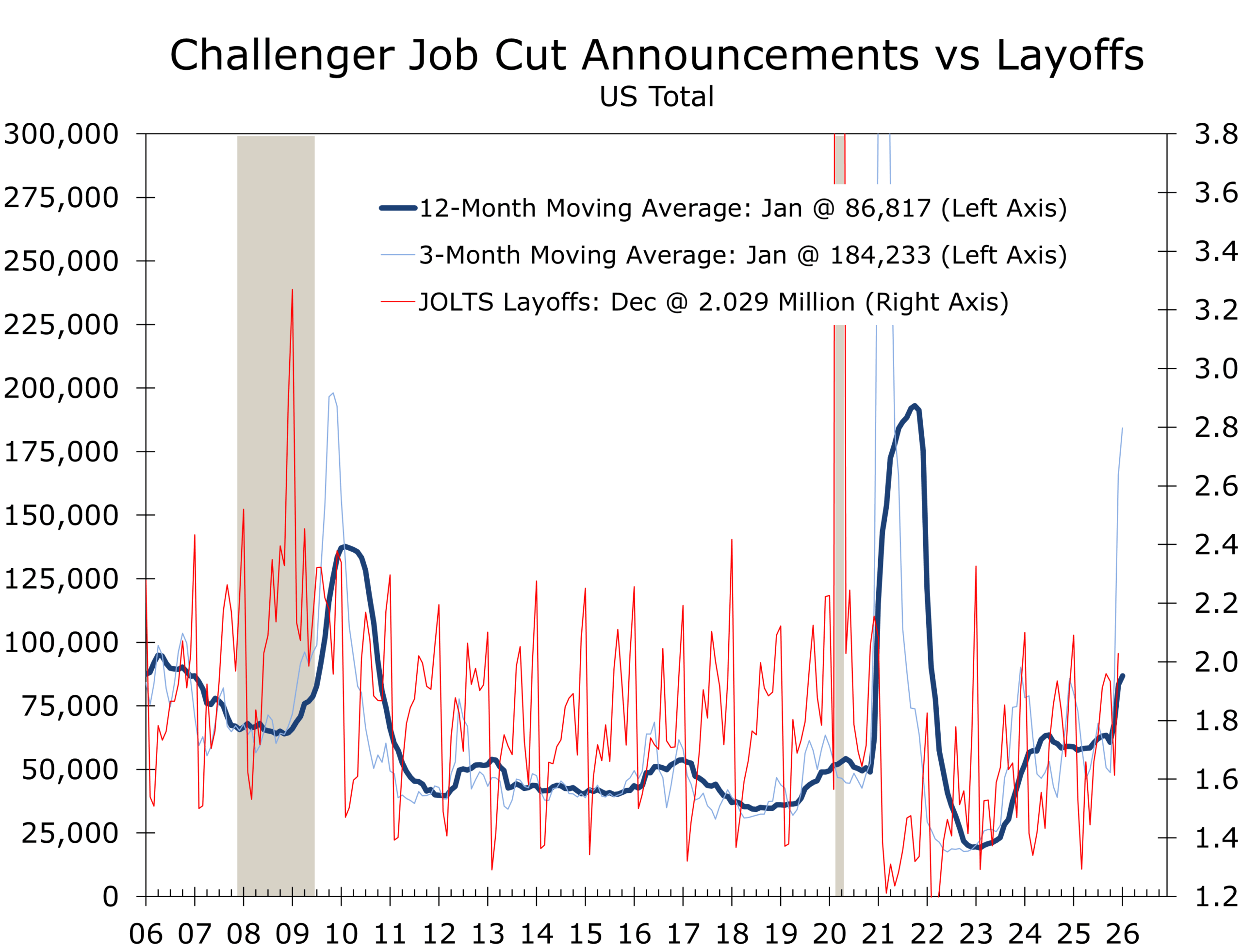

Challenger layoff announcements increased, driven largely by technology and other white-collar sectors. Importantly, these announcements reflect restructuring and productivity initiatives rather than broad financial distress. Layoff levels remain low by historical standards and are not corroborated by required government filings on mass layoffs (WARN notices) or by the Job Openings and Labor Turnover Survey (JOLTS), which shows a far more muted rise in separations.

The start of the year also tends to generate a flurry of restructuring announcements during earnings season, which likely pushed January’s totals higher. Weekly jobless claims rose to their highest level since early December but remain well below recessionary thresholds. Initial claims are drifting higher, continuing claims remain elevated, and labor-market turnover is subdued. Employers across sectors report that voluntary turnover remains exceptionally low. This low-hire, low-fire dynamic helps explain why unemployment pressures can build gradually even as layoffs remain contained.

The labor market continues to cool via less hiring, not more layoffs.

On the consumer side, sentiment data were cautiously encouraging. The University of Michigan survey posted its first significant improvement in headline confidence in several months alongside a sharp drop in one-year inflation expectations. Longer-term expectations edged slightly higher but remain anchored. Consumers continue to report pressure on household finances, but fear of accelerating inflation is fading and will likely slide further in coming months.

That message was reinforced by the New York Fed Survey of Consumer Expectations, which showed further easing in short-term inflation expectations and stable longer-run views. Concerns about credit availability persist, but inflation fears continue to fade.

By week’s end, markets reconciled these crosscurrents. Despite early volatility and lingering unease, the Dow Jones Industrial Average reached an all-time high, reflecting the resilience of large-cap, cash-generative firms. Leadership narrowed, rotation replaced retreat, and durability once again commanded a premium.

Funding, Liquidity, and Capital Allocation

Liquidity risk has re-entered the conversation in a meaningful way. Even speculation about renewed Federal Reserve balance-sheet discipline has reminded markets that monetary accommodation is no longer a background condition. Balance-sheet flexibility, diversified access to funding, and disciplined capital allocation are becoming more important as markets grow less forgiving of leverage that depends on benign liquidity conditions

The era of liquidity as a background condition is fading, requiring greater scrutiny of leverage and capital deployment.

Capital discipline is back in focus. Investors are increasingly scrutinizing returns on invested capital, particularly in AI-related spending where upfront costs are large and payoff horizons uncertain. Firms that can sequence investment and demonstrate measurable productivity gains are being rewarded over those pursuing scale for its own sake.

Labor market softening remains orderly but real. Hiring has slowed, turnover is lower than usual, and adjustment is occurring primarily through restraint rather than layoffs. This argues for cautious workforce planning that preserves critical talent while avoiding commitments based on a broad-based resurgence in demand that has yet to materialize.

Inflation risk continues to diminish. Pricing power is becoming harder to sustain outside essential services and regulated industries, shifting margin management toward cost control, productivity, and procurement discipline. A growing number of food companies are rolling back prices, reflecting consumer pushback as well as subtle shifts in tastes and preferences toward healthier lifestyles.

Finally, selective resilience is creating opportunity. Firms with strong cash flow and modest leverage retain strategic optionality in a more cautious macro environment. That optionality is once again a competitive advantage.

Geopolitical Developments

Geopolitical risk remains elevated but, for now, largely contained from a market perspective. In the Middle East, tensions involving Iran and Israel continue to generate episodic volatility, particularly in energy markets. Pricing behavior suggests investors are assigning a modest risk premium rather than anticipating imminent disruption. The risk, however, is that markets may be extrapolating from recent experience, expecting any confrontation with Iran to resemble limited U.S. involvement in the 12-Day War or the relatively contained Venezuelan operation. That assumption may prove complacent. A direct conflict involving Iran would likely be viewed by its leadership as existential, raising the odds of escalation and materially greater disruption to energy flows and regional stability.

Markets are pricing geopolitical risk as a premium rather than a shock, a posture that leaves little margin for escalation.

The conflict in Ukraine grinds on, reinforcing Europe’s longer-term recalibration toward higher defense spending, energy security, and industrial resilience. Both sides increasingly appear to be waiting for a more favorable negotiating position, with Ukraine’s leverage arguably improving over time. While the war remains economically consequential, its marginal impact on global markets has diminished as it has become embedded in baseline expectations.

In Asia, recent Japanese election outcomes provided a measure of political clarity while renewing longer-term questions around fiscal sustainability and policy coordination. Markets have treated the results as incremental rather than transformative. Developments in the Japanese government bond market nevertheless remain a useful leading indicator for global duration markets, including the United States.

Taken together, these geopolitical crosscurrents matter less for near-term growth than for financial conditions. They add friction to global supply chains, volatility to commodity markets, and a persistent upward bias to global term premia, an underappreciated constraint in an already liquidity-sensitive environment.

Looking Ahead

The coming week features a dense economic calendar that will test the market’s emerging narrative of cooling growth, easing inflation pressures, and a patient Federal Reserve.

Key releases include retail sales, the January employment report, and the January CPI report. Retail sales will offer an important read on whether easing inflation expectations are translating into firmer real spending or whether consumers remain cautious amid slower job growth and tighter credit conditions.

The employment report will be closely watched for confirmation of slower payroll growth, revisions tied to the annual benchmark update, and signals from wages and the unemployment rate. We are expecting substantial downward revisions to the previous data but the recent ADP data hint that the recent payroll data could show more resiliency.

The CPI remains the key element to the policy outlook, particularly as seasonal factors and tariff-related distortions complicate the near-term inflation picture. January oftentimes surprises to the upside as firms rush to implement price hikes at the start of the year.

In addition, the week features a heavy slate of Federal Reserve speakers, including Governors Waller and Miran, Vice Chair Bowman, and several regional Fed presidents. Markets will be listening for clarity on how officials are balancing slowing labor momentum against inflation that clearly appears to be decelerating but remains above target, and whether balance-sheet policy is beginning to re-enter the discussion more explicitly.

Taken together, this week’s data and commentary should help determine whether last week’s resilience hardens into confidence, or whether volatility remains the dominant feature of a Year of the Horse still finding its stride.

The Piedmont Perspective – Breaking in the Horse

The Year of the Horse is rarely about comfort. It is about motion, force, and the test of control. Historically, such periods expose imbalances rather than resolve them. Both 1978 and 1990 were years of disruption, marked by inflation, recession, geopolitical shock, and policy uncertainty. The payoff, when it came, arrived later.

That history resonates today. Productivity gains are real, but uneven. As in the early 1990s, they are showing up first in capital-intensive sectors and operational processes rather than in headline data or confidence measures. Markets are struggling to price gains that are still being discovered.

The risk is not that this expansion lacks power. It risks outrunning understanding. When liquidity expands faster than productive capacity, markets move quickly and often misprice risk. When credibility weakens, momentum does not slow. It veers. Record index levels can coexist with uncertainty when prices run ahead of comprehension.

This expansion is not broken. But it has not yet been fully broken in. The task for policymakers is to reassert credibility without choking off productivity gains that are quietly reshaping the economy. The task for investors and executives is to listen carefully for those signals, while avoiding the noise that surrounds them.

In the Year of the Horse, credibility is the saddle, liquidity is the rein, and productivity determines whether the ride ultimately rewards patience or punishes excess.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 9, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000