Highlights of the Week

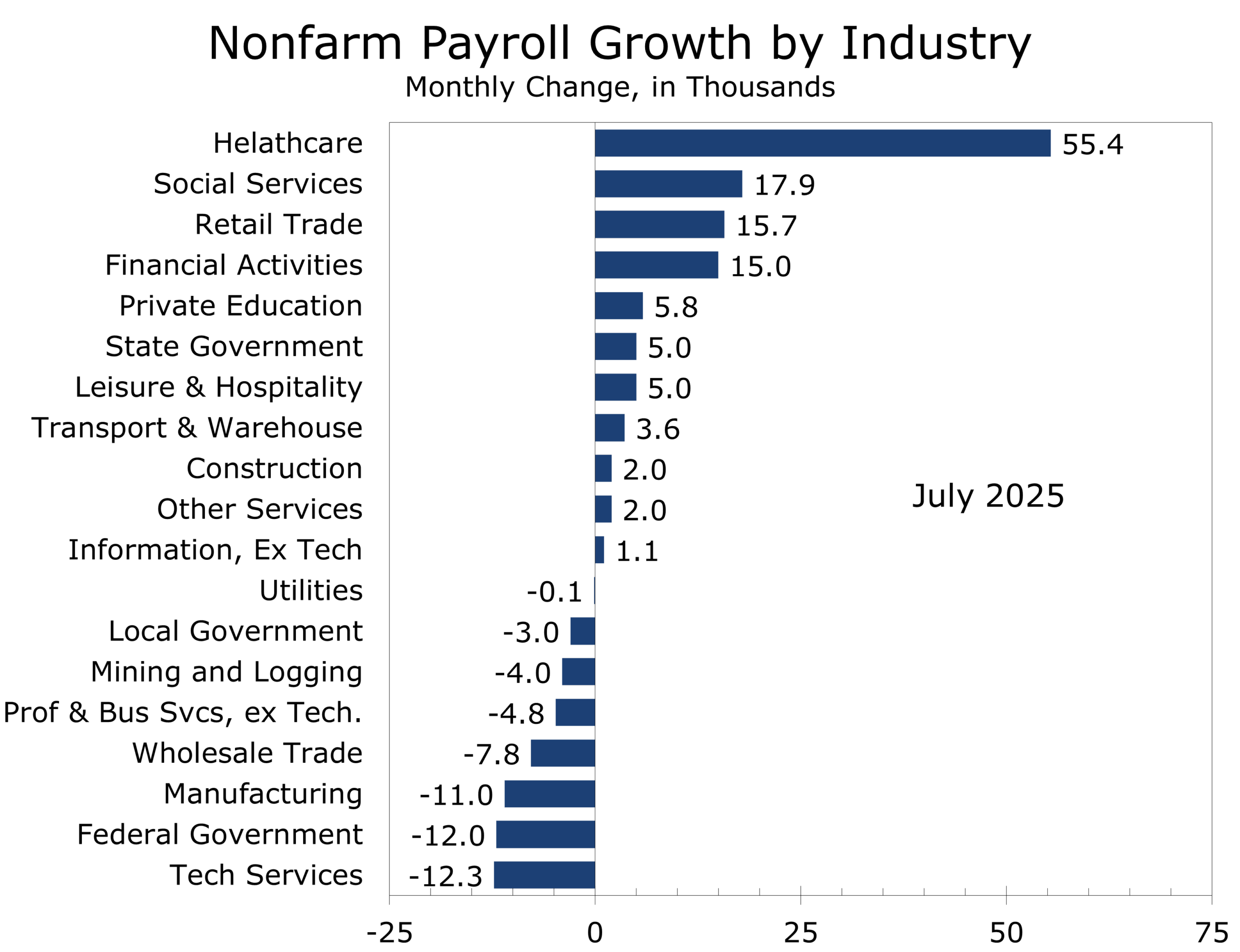

- July’s employment report confirmed a sharp deceleration—payrolls rose 73,000, and data for May and June were revised down by a combined 258,000 jobs.

- Private sector hiring has flatlined; healthcare and social services, finance and retail trade account for all net job growth.

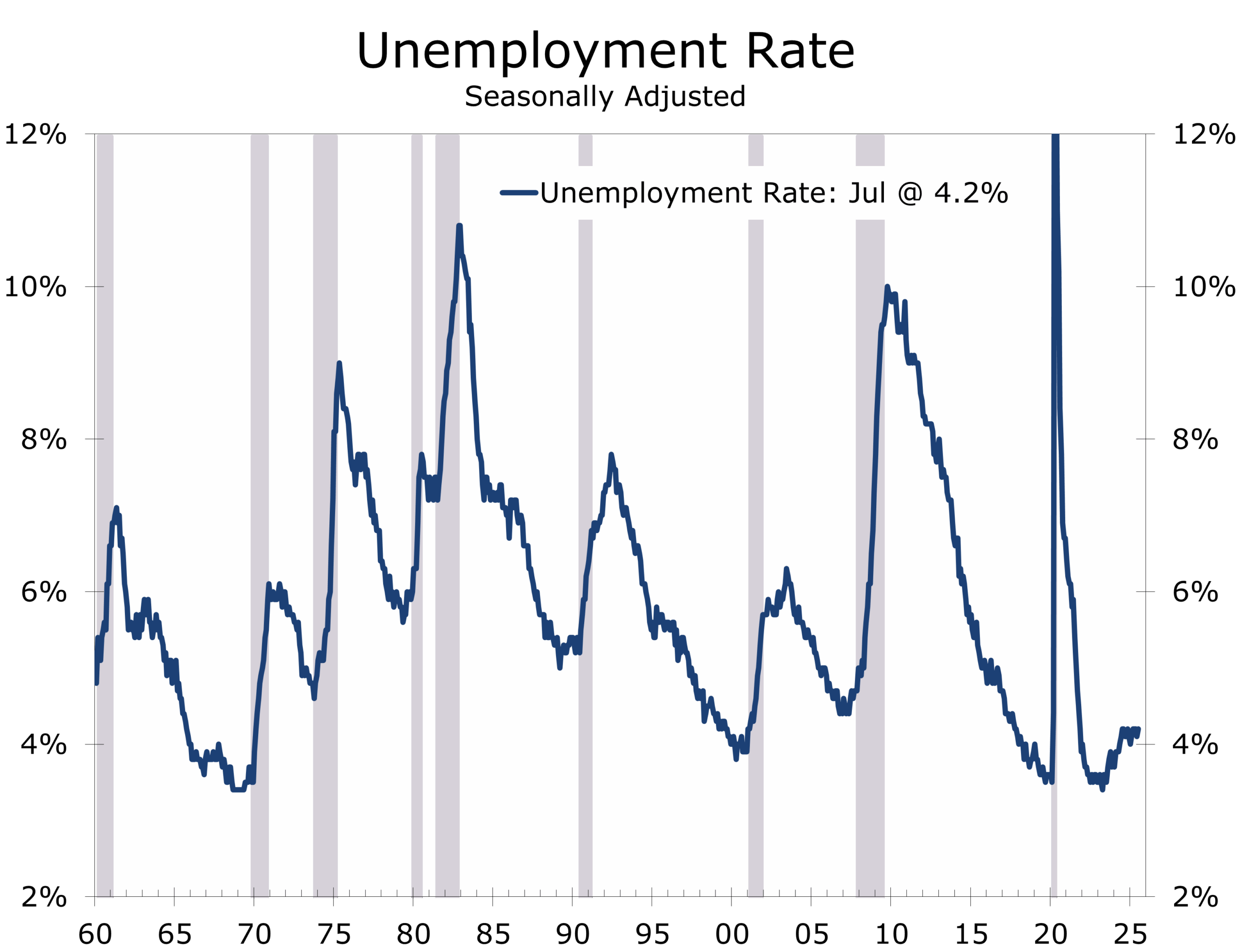

- Unemployment edged up to 4.2% (4.248% unrounded), while labor force participation slipped to 61.7%.

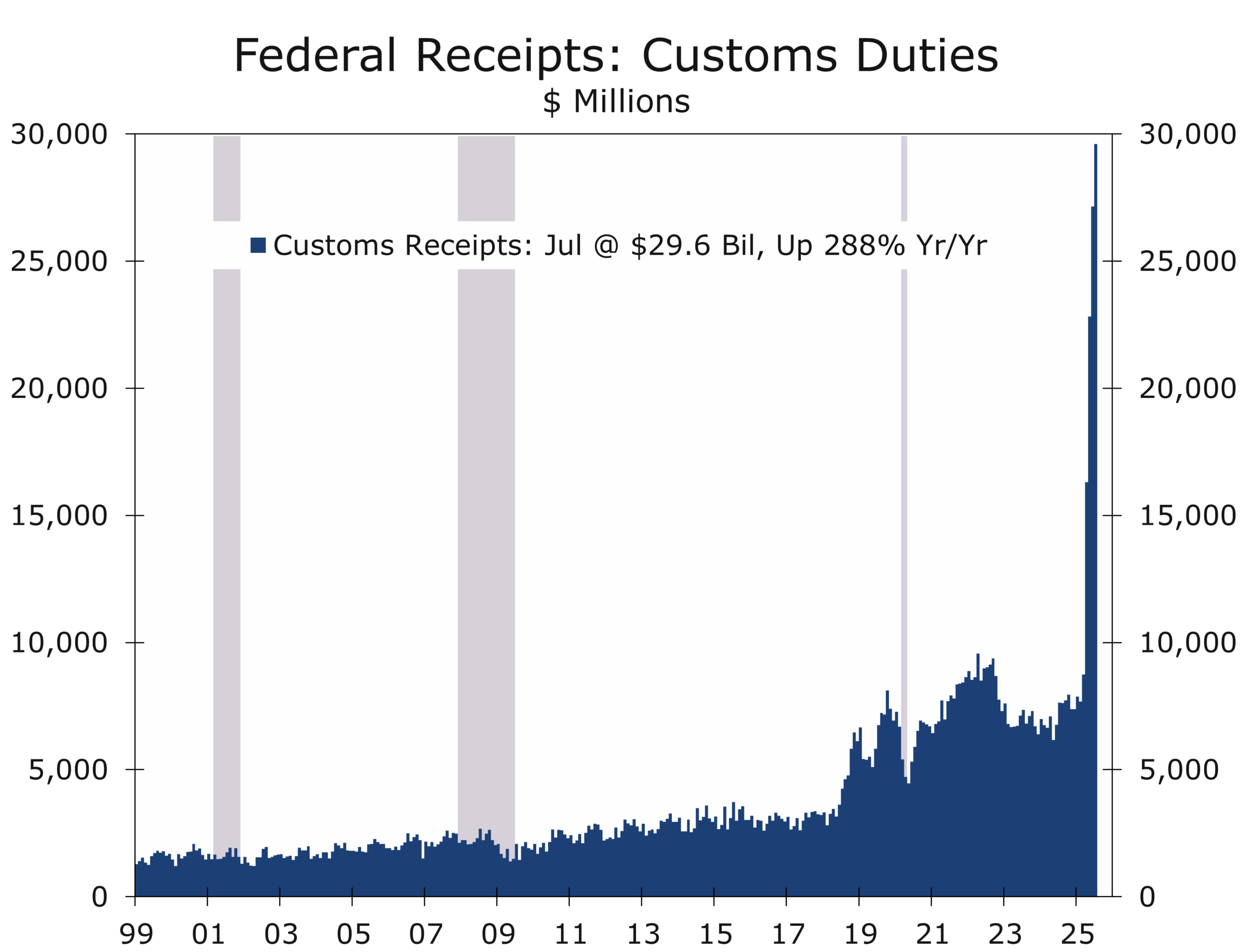

- President Trump’s reciprocal tariff regime took effect August 1, pushing effective U.S. tariff rates above 15%.

- Microsoft and Meta delivered strong earnings, reinforcing optimism around AI-driven investment and productivity.

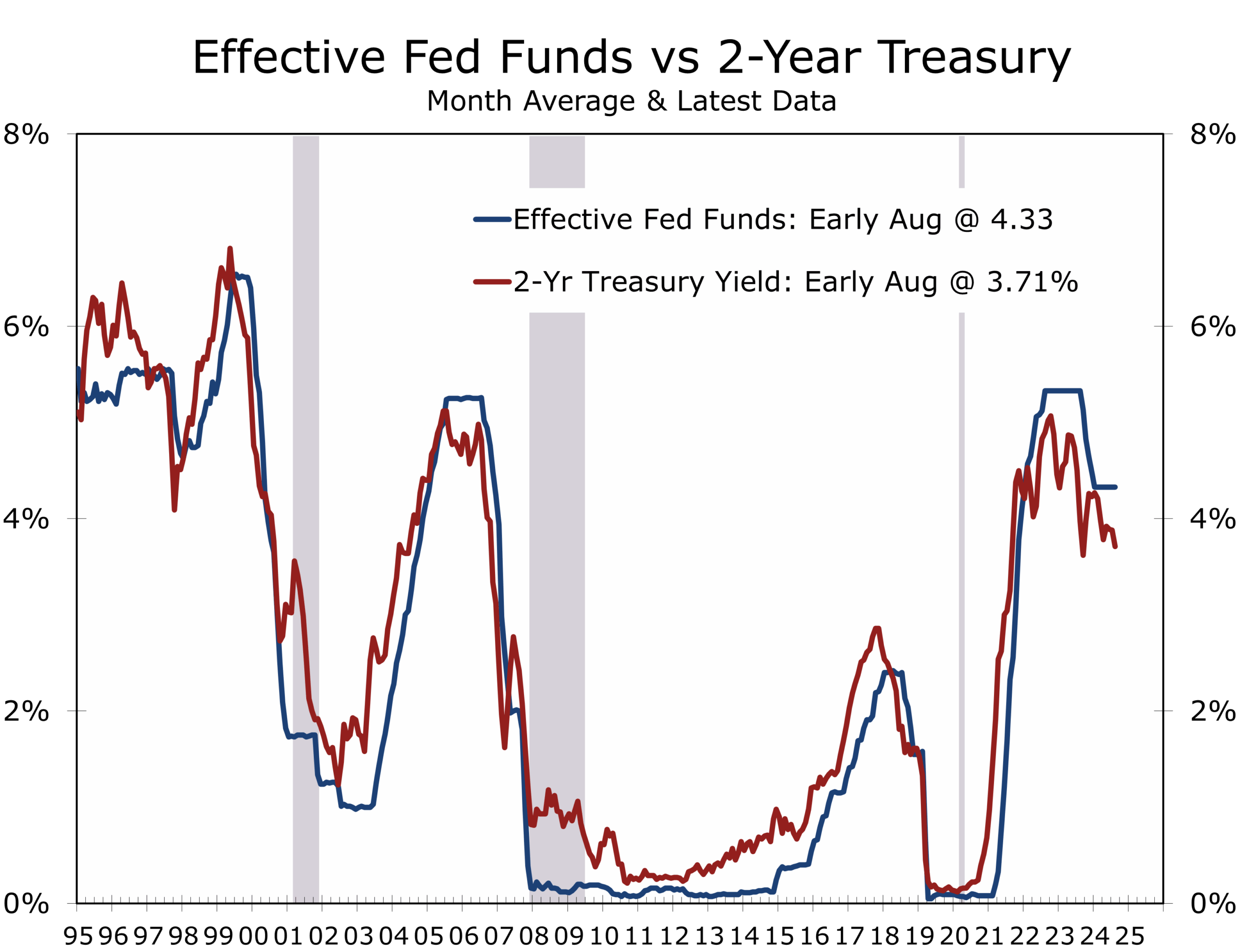

- Treasury yields fell and the dollar softened as markets priced in a September rate cut; equities posted their worst week since Liberation Day in early April.

- Russia launched its most intense weekly barrage in Ukraine since May, while famine in Gaza prompted diplomatic fractures among Western allies. In a notable shift, the Arab League officially condemned the October 7 attack on Israel and declared that Hamas should surrender and play no role in governing Gaza or any future Palestinian state.

- Markets now expect a September rate cut; this week’s data—services ISM, unit labor costs, inflation sentiment, and various Fed speakers—will be closely watched for clues into the underlying pace of growth and change in sentiment.

The Recovery Slows Beneath the Surface

The July employment report confirmed the labor market is softening. Nonfarm payrolls rose by just 73,000, well below consensus. Moreover, May and June data were revised lower by a combined 258,000. Over the past three months, the economy has added an average of just 35,000 jobs per month.

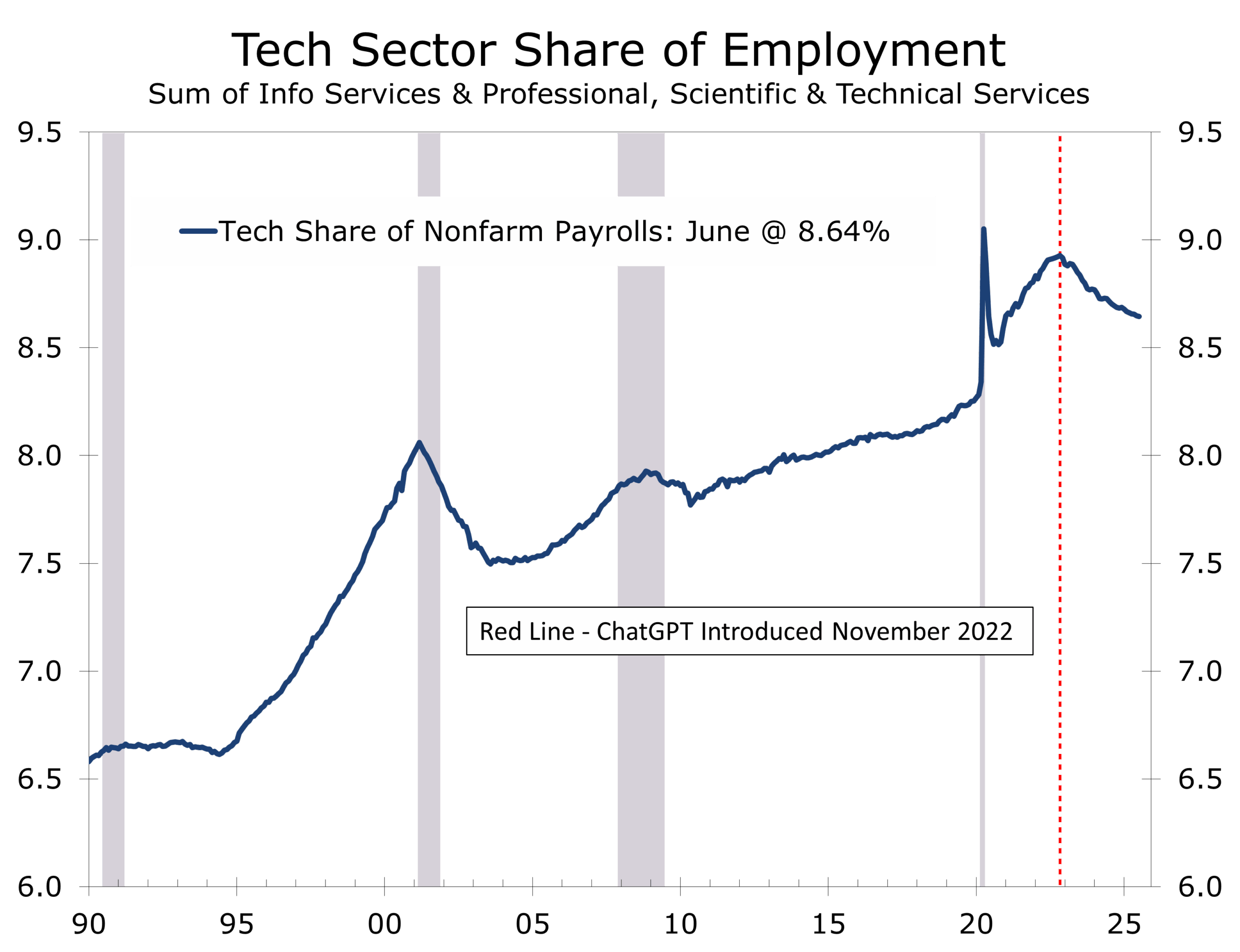

The private sector has held up slightly better, adding an average of 52,000 jobs a month for the past three months. Private-sector hiring is being carried by healthcare and social services. Manufacturing employment fell for the third straight month, while construction and professional services were flat. A subset of tech jobs we track within professional and technical services lost 12,300 jobs and has shed 33,200 jobs over the past three months.

Much of the downward revisions to May and June data was to state and local government. The timing of the end of the school year often leads to wide swings in the seasonally adjusted data this time of year. Still, downward revisions of this magnitude are rare. Federal government payrolls have declined for six consecutive months, reflecting DOGE cuts and retirements.

The unemployment rate rose to 4.2%, but the unrounded figure was 4.248%—the highest since November 2022. Labor force participation edged down to 61.7%, and the employment-to-population ratio slipped to 60.1%. Long-term unemployment rose to 1.8 million. The participation rate has fallen 0.5 percentage points over the past year, while the employment-population ratio has fallen 0.4 percentage points.

Structural shifts are becoming more apparent. A slowdown in immigration and an aging population have lowered the breakeven rate of job growth, making headline unemployment appear healthier than underlying conditions suggest. Broader measures of labor market health continue to deteriorate. Without the drop in labor force participation, much of which is tied to tighter immigration enforcement, the unemployment rate would easily top 4.5%

Tariffs in Effect: The Next Phase of Strategic Trade

President Trump’s reciprocal tariff order took effect on August 1, raising rates to 15% or more on imports from countries without new trade agreements. Some targeted nations—including Canada, Switzerland, Brazil, and Taiwan—face effective rates as high as 50% on select goods. Secondary sanctions on Russia could boost effective tariff rates even further, with India and China two of the most impacted nations

The move is part of a broader strategy to align trade with national security and industrial policy. Tariffs are now being paired with investment pledges in energy, logistics, and semiconductor supply chains. The average effective tariff rate has now likely risen above 15%, by far the highest in the modern era.

The inflation impact has so far been modest, with most firms absorbing costs through margin compression. But policy uncertainty is weighing on investment: core capital goods orders have now declined for three consecutive months, and ISM Manufacturing remains below 50. Retailers and manufacturers are adjusting inventories in anticipation of further disruption, and many firms have been waiting for tariffs to be finalized before deciding how much to pass on to consumers.

Geopolitics: Flashpoints and Fallout

Russia intensified its military operations in Ukraine last week, launching more than 300 drone and missile strikes—the most in a single week since May. Ukrainian infrastructure in Odesa and Kharkiv was heavily targeted, and Chasiv Yar, a key defensive position in Donetsk, appears to have fallen. Peace negotiations remain stalled. President Trump has moved up the deadline for Russia to respond to U.S.-led peace initiatives, warning that secondary sanctions will soon be imposed on nations that continue to trade with Russia, particularly in energy and dual-use technologies.

The move prompted a fierce response from Moscow. Russian Security Council Deputy Chair Dmitry Medvedev threatened that any escalation of Western involvement would trigger a reactivation of Russia’s “Dead Hand” nuclear response system—an automated retaliation protocol developed during the Cold War. Medvedev also warned that Moscow considers any economic siege an act of war, and state-controlled media began running simulations of nuclear attacks on European capitals. These provocations signal that the Kremlin is escalating not only militarily but also in the information and psychological warfare domains.

These threats suggest the Kremlin views the prospect of secondary sanctions as a serious escalation and threat—one that could strain Russia’s economic lifelines and test the cohesion of its leadership. Medvedev’s outburst may reflect growing internal anxiety over the potential for isolation from China, India and other critical trading partners. President Trump would like Indian refiners to stop purchasing Russian oil and commit to purchase more U.S. crude as part of a broader trade deal.

In the Middle East, Gaza’s deepening humanitarian crisis prompted Canada, the U.K., and France to announce plans to recognize Palestinian statehood at the upcoming U.N. General Assembly. The Trump administration responded swiftly, imposing new sanctions on Palestinian Authority officials and warning that such moves could jeopardize future trade cooperation, including under the USMCA framework. Secretary of State Marco Rubio criticized the recognitions as premature and even counterproductive, arguing they may embolden Hamas and undermine prospects for a lasting ceasefire.

The divergence between the U.S. and its allies reflects broader tensions over diplomatic strategy as well as greater tolerances for appeasement in Canada and western Europe. Critics of unilateral recognition argue that it offers symbolism without substance—particularly in the absence of a defined leadership structure or clear territorial boundaries. The Trump Administration continues to emphasize the potential of expanding the Abraham Accords framework as a more durable pathway toward Palestinian statehood and a broader, more equitable and enduring peace.

Markets and the Fed: September in Play

Markets are now pricing in a high probability of a 25bp rate cut at the September FOMC meeting, and potentially a half-point cut if labor market conditions deteriorate further. Two Fed governors dissented in favor of immediate easing at the July meeting—the most open policy division at the Board level in over three decades. Bond yields fell across the curve, and the dollar reversed its recent rally and edged lower. Equities sold off sharply on Friday, capping the worst week for stocks since the Liberation Day tariff announcement in early April.

The economy appears to be on the precipice of recession. Consumer spending has shown no net growth this year, after adjusting for inflation. Housing is in full retreat, with sales stumbling and new construction ramping down. Home prices are also weakening, which will undermine home improvement spending. Businesses are also holding off on capital spending, outside of AI and related power initiatives

Earnings: AI Delivers a Tailwind

Amid macro uncertainty, Q2 earnings from Microsoft and Meta offered a rare bright spot. Microsoft’s revenue rose 18% to $76.4 billion, driven by continued strength in cloud and AI services. Meta’s revenue jumped 22% to $47.5 billion, fueled by strong demand for AI-powered advertising tools.

Both companies raised capital spending guidance and emphasized productivity gains. Meta now reports that over 2 million advertisers are using its AI-generated ad content platform. These results reinforce the view that the AI investment cycle is maturing—providing near-term earnings support and long-term productivity gains.

The performance of these mega-cap firms has helped buoy equity sentiment even as broader growth softens. Investor appetite for firms with pricing power, capex discipline, and exposure to AI remains strong. There is a downside, however, as AI is increasingly displacing workers, both through layoffs and reduced hiring.

Looking Ahead: August Signals, September Setup

The back nine is proving to be as difficult as we feared. Labor market momentum has faded, real consumption is stalled, and tariff-related uncertainty continues to cloud the outlook. While the Fed retains room to ease, inflation data are likely to remain mixed. This week’s calendar is relatively light but still should provide a few key signals. The ISM Services Index will shed light on underlying demand and pricing power, both of which appear to be softening. Productivity and unit labor cost data may prove the most consequential—any improvement there would strengthen the case for near-term policy easing. Inflation expectations from the New York Fed and the preliminary University of Michigan sentiment survey also warrant close attention.

This Week’s Key Reports

Monday, August 4

• Factory Orders (June) – Expected to be soft due to volatility in commercial aircraft orders, which surged in May. Broader business investment remains cautious amid tariff uncertainty and unclear rate trajectory.

Tuesday, August 5

• ISM Services Index (July) – Forecast to rebound to 51.7. Watch for signals on service-sector demand and pricing pressure.

Wednesday, August 6

• Fed Speakers – Governor Lisa Cook and Boston Fed President Susan Collins will participate in a livestreamed panel discussion at 2:00 p.m. titled “A Central Bank Perspective on the Evolving Global Landscape.”

Thursday, August 7

• Q2 Productivity & Unit Labor Costs – A key read on whether the economy can sustain growth amid structural labor constraints driven by tighter immigration enforcement and accelerating AI adoption.

• Initial Jobless Claims – Seasonal adjustments may inflate the headline figure; continuing claims are expected to continue their gradual upward trend.

• New York Fed Consumer Expectations Survey – Closely watched for near-term inflation expectations, which several Fed officials have highlighted recently.

• Fed Speaker – Atlanta Fed President Raphael Bostic to deliver remarks.

• Consumer Credit (June) – Credit growth may slow as consumers grow more cautious about employment stability and future income.

Friday, August 8

• University of Michigan Sentiment (Prelim August) – Inflation expectations remain the key metric, particularly after their early-year spike and subsequent decline.

Final Points

The U.S. economy is not in crisis, but it is clearly losing altitude. Slower hiring, stagnant consumption, a weakening housing market, and rising trade friction are straining the expansion’s resilience. If policymakers misjudge the risks—or wait too long to cut rates—the glide path could steepen quickly. A September rate cut now appears likely, but the timing and tone of the Fed’s messaging will shape whether markets interpret it as a much-needed precautionary adjustment, a political capitulation, or a belated rescue move.

A precautionary adjustment is the outcome policymakers are aiming for. If executed successfully, it could bring down long-term interest rates and mortgage costs—relieving pressure in the housing market and reducing refinancing risk across the broader economy.

A Gun and a Grievance

On July 28, 2025, a mass shooting at 345 Park Avenue in Midtown Manhattan claimed four lives—including an off-duty NYPD officer and a Blackstone executive—and left another victim critically injured. The gunman, 32-year-old Shane Devon Tamura, a former Las Vegas casino worker, opened fire inside the building—home to the NFL’s headquarters—before taking his own life.

Tamura left behind a note blaming the NFL for his alleged chronic traumatic encephalopathy (CTE), a degenerative brain disease he attributed to playing high school football. Fueled by resentment and unmet medical needs, he drove cross-country to confront league officials. After mistakenly arriving on the wrong floor, he opened fire indiscriminately—turning a personal grievance into public tragedy.

The attack echoed the December 2024 assassination of UnitedHealthcare CEO Brian Thompson, who was gunned down on a Midtown sidewalk by Luigi Mangione—a man with no personal connection to Thompson or the company, but who viewed the insurance industry as emblematic of a system that had failed him. Both incidents reflect a disturbing trend: individuals channeling institutional resentment into targeted violence.

Though their motivations differed, both attackers believed the system had wronged them—and that violent retribution was justified. That segments of social media applauded their actions—celebrating Mangione’s murder and framing Tamura’s attack as a social protest—raises troubling questions about the normalization of vigilante justice.

These events carry serious economic consequences. After Thompson’s assassination, major insurers removed executive profiles from their websites and quietly upgraded security protocols. Following Tamura’s attack, the NFL and other tenants at 345 Park Avenue tightened access restrictions, while corporate security firms reported a surge in demand. Investor confidence, executive mobility, and board-level recruitment may all suffer if cities like New York are perceived as unsafe for business leadership.

At the foundation of functional capitalism lies the rule of law. Executives must be able to lead without fear of arbitrary violence. Markets thrive when disputes are resolved through legal channels—not through bloodshed or intimidation. When violence becomes an accepted or romanticized outlet for grievance, the cost of doing business rises and capital flows elsewhere.

The path forward requires a coordinated response: expanded mental health care, greater institutional accountability, enhanced urban security, and a firm recommitment to zero tolerance for violence—including on social media, university campuses, and within political discourse. However legitimate a grievance may be, redress must remain within the bounds of law.

The Midtown shooting is a grim reminder that public safety is not merely a civic issue—it is a moral and economic imperative. The protection of human life must remain the first responsibility of a functioning society, and the preservation of safe, open, and orderly environments is essential for commerce to thrive. In cities like New York, where trillions in capital flow each year and millions live, work, and lead, law and order is not a luxury—it is the foundation upon which both lives and livelihoods depend.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 4, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000