Highlights of the Week

- This past week’s data painted a mixed picture: personal income and spending were firmer, but confidence slipped on labor market and tariff concerns.

- Home prices lost momentum this summer, pending sales softened, and trade flows widened the goods deficit—all adding downside risks for Q3 GDP.

- Durable goods orders signaled resilience in equipment spending, with AI investment still a powerful driver.

- Treasury curve steepening accelerated, fueled by expectations of a September Fed rate cut and political pressure on the Fed.

- Geopolitical tensions remain elevated: Israel widened strikes across the region, Russia increased missile and drone strikes on Ukraine and ramped up information warfare with Europe and the U.S., while the U.S. Navy increased its presence near Venezuela ahead of Guyana’s election.

- Risks to watch include tariff-driven inflation re-acceleration, further Fed independence challenges, Treasury market liquidity strains, and potential energy disruptions tied to geopolitics.

Consumer Sector: Dancing but Uneasy

July’s personal income and spending report showed households still have stamina. Personal income rose 0.4%, wages and salaries 0.6%, and real spending advanced 0.3%, led by a 2.0% jump in durable goods. The personal saving rate ticked down to 4.4% but remains sturdier than the sub-4% lows of 2023.

Inflation surprised slightly on the soft side, with headline PCE up 0.2% and core PCE 0.3%, running near 2.9% y/y. Consumption is supported by wages, not savings drawdowns, reducing the risk of a sudden stop. Upside potential, however, looks limited.

Consumer spending is off to a solid start in Q3, despite concerns over tariffs and job growth.

Sentiment tells a different story. The Conference Board’s confidence index slipped, with households citing job worries and tariff-driven inflation fears. The University of Michigan’s final August sentiment reading echoed that unease, hitting its lowest since last fall. This divergence between steady data and sour mood underscores the risk that spending momentum might fade.

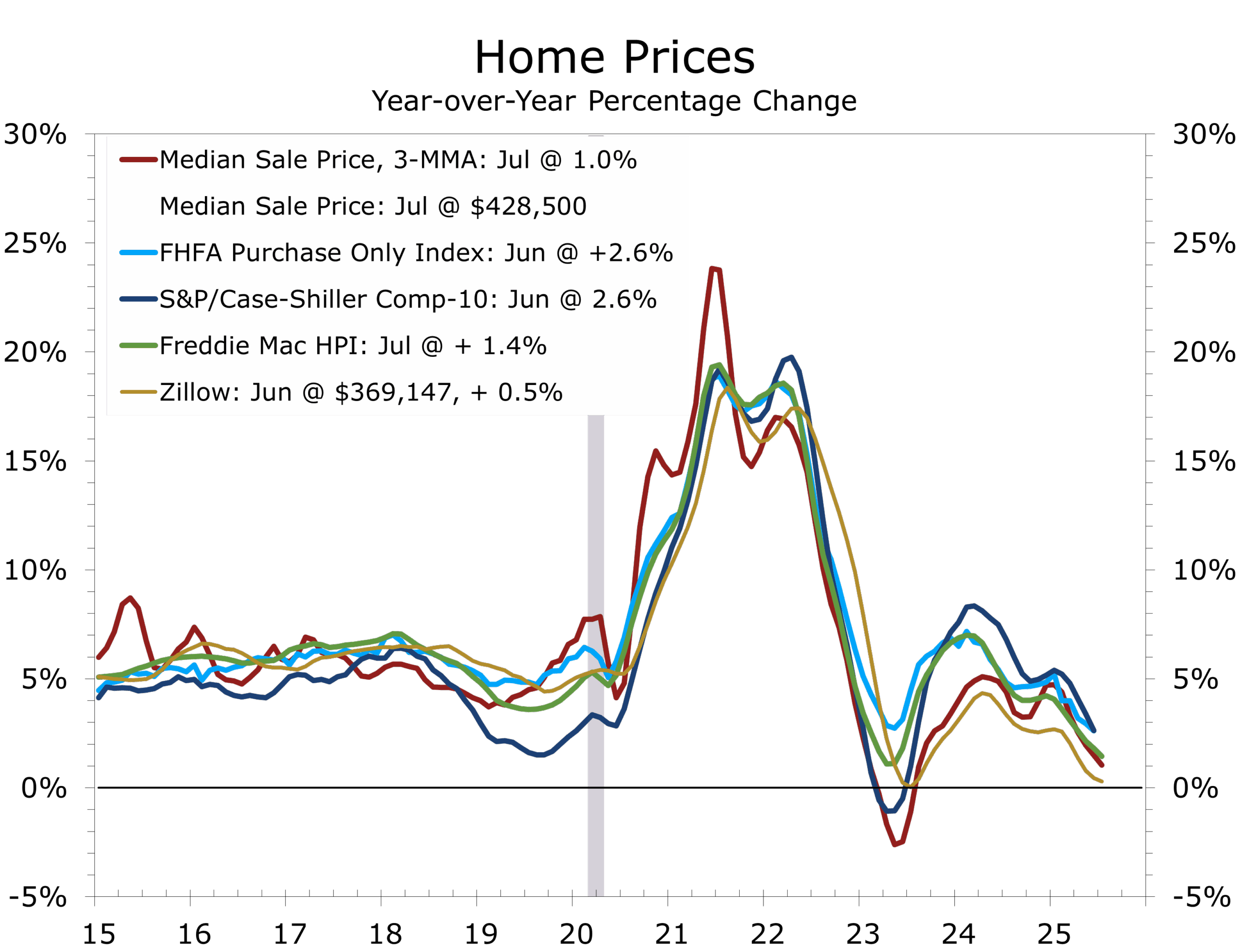

Housing: Momentum Slips Further

Housing markets cooled further in midsummer. Case-Shiller home prices fell 0.3% in June, slowing to their weakest annual gain since July 2023, with several Sun Belt metros seeing outright declines. The FHFA series posted its softest growth since 2012, and the Freddie Mac National Home Price Index fell 0.22% in July and is now up just 1.4% yr/yr. Pending home sales fell 0.4% in July, pointing to weaker existing sales in August.

Affordability remains stretched, and with labor market worries mounting, buyers are staying cautious despite modest rate relief. For housing-related industries, the implication is a prolonged plateau rather than an imminent rebound. Mortgage rates would likely need to fall below 6% to produce a meaningful jump in sales, which looks unlikely before spring 2026.

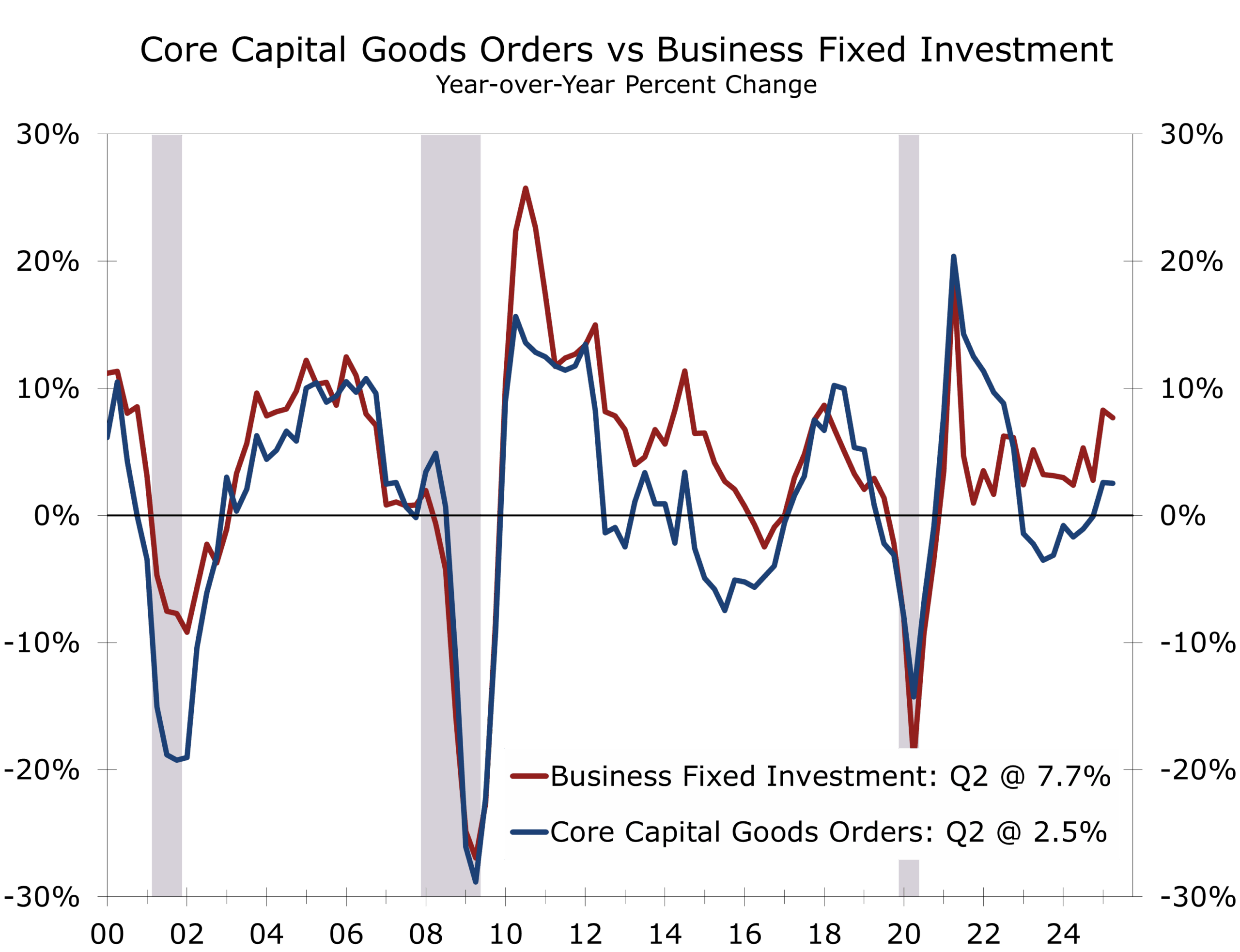

Business Investment: Still Carried by AI

Durable goods orders continue to show resilience. Headline orders fell 2.8% in July on weak aircraft bookings, but core capital goods orders rose 1.1%, a stronger-than-expected sign that equipment spending is holding up. Shipments also improved, suggesting Q3 equipment investment may grow at a 3.2% pace versus 2.5% in Q2. While aircraft orders fell, they are up a whopping 139% year-to-date through July.

The AI buildout, aerospace, and defense continue to drive capital spending, which began Q3 strong.

Q2 GDP was revised higher, reflecting gains in structures, equipment, and intellectual property, with AI-related outlays masking broader softness. Corporate profits rebounded 1.7% in Q2, but tariff effects on margins are likely to show up in Q3. The equipment cycle remains intact, though narrowly concentrated in AI, electronics, and related capital goods. Aerospace and defense are other key drivers.

.

Trade: Import Surge Widens the Deficit

The July goods trade deficit widened by $18.7B to $103.6B, largely on industrial supplies and capital goods imports. Some of this reflects AI demand but also catch-up in orders previously delayed by tariff uncertainty. Exports were flat.

The larger trade deficit adds downside risk to Q3 GDP after Q2’s upside revision. Longer term, tariffs are providing meaningful federal revenue—estimated at $2.6T through FY2034—but at the cost of growth. Higher import costs and supply chain uncertainty are complicating capex decisions. Some major projects are moving forward under temporary tariff reprieves.

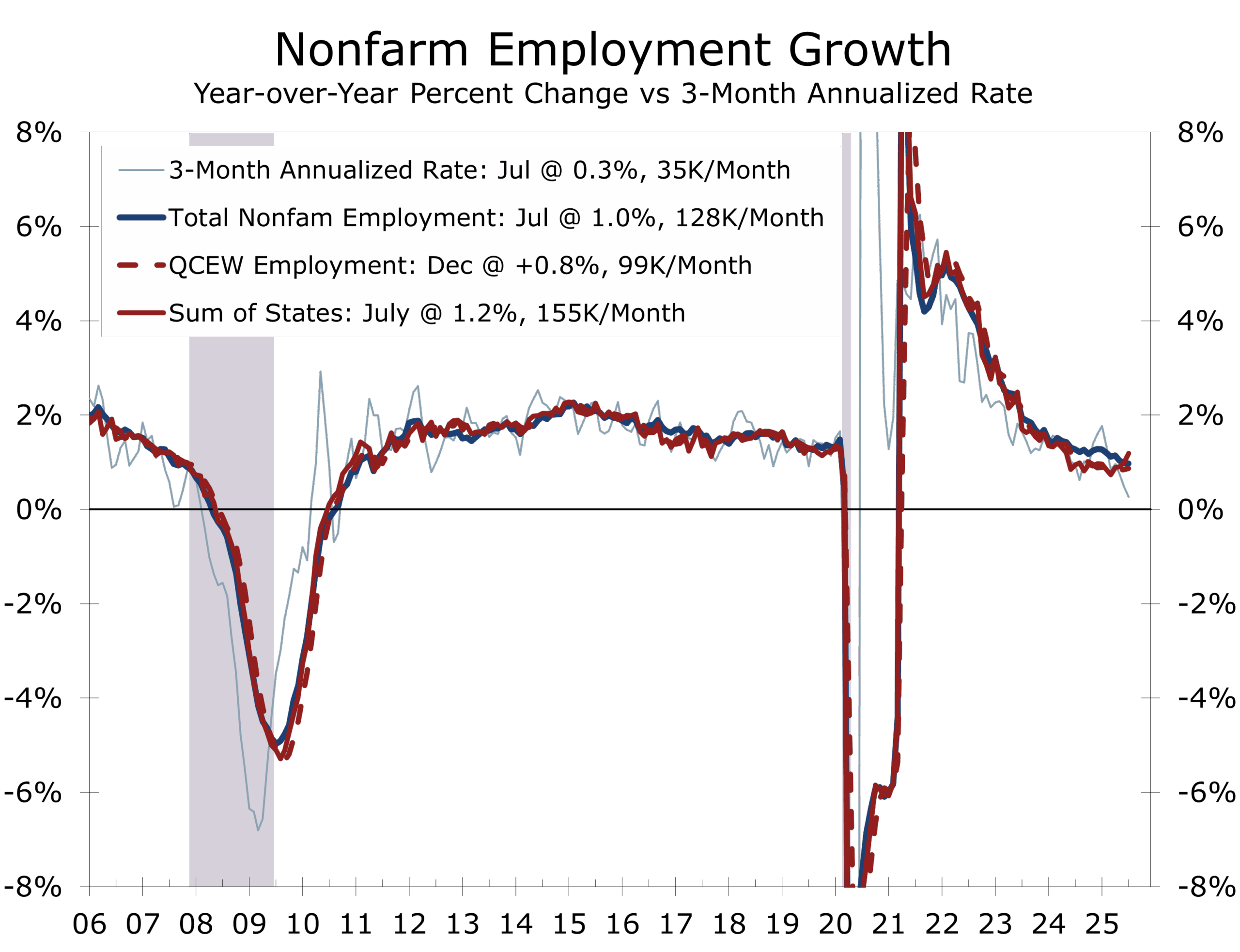

Labor Market: Cooling but Not Cracking

Weekly claims remain contained, but slower hiring remains a key theme. August payrolls are expected to rise by just 60,000, with unemployment edging up to 4.3%. Immigration declines are weighing on labor force growth, particularly in states that previously absorbed large inflows.

Slower payroll growth and higher unemployment signal easing wage pressures. But persistently low layoffs suggest firms are still hoarding labor, reflecting the high pace of retirements and tighter immigration enforcement. AI is also slowing hiring in IT fields, leading to a rising unemployment rate for young, college graduates.

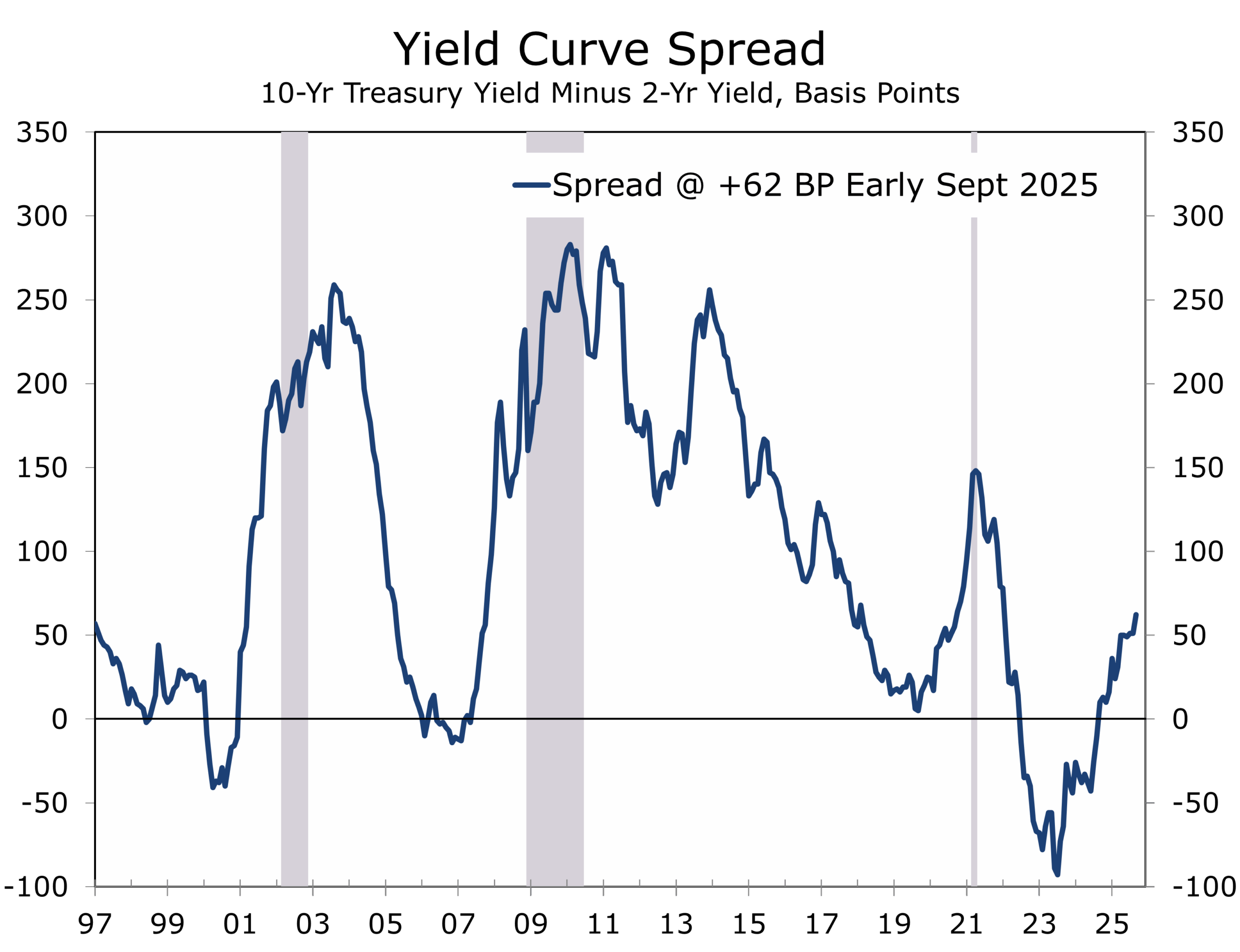

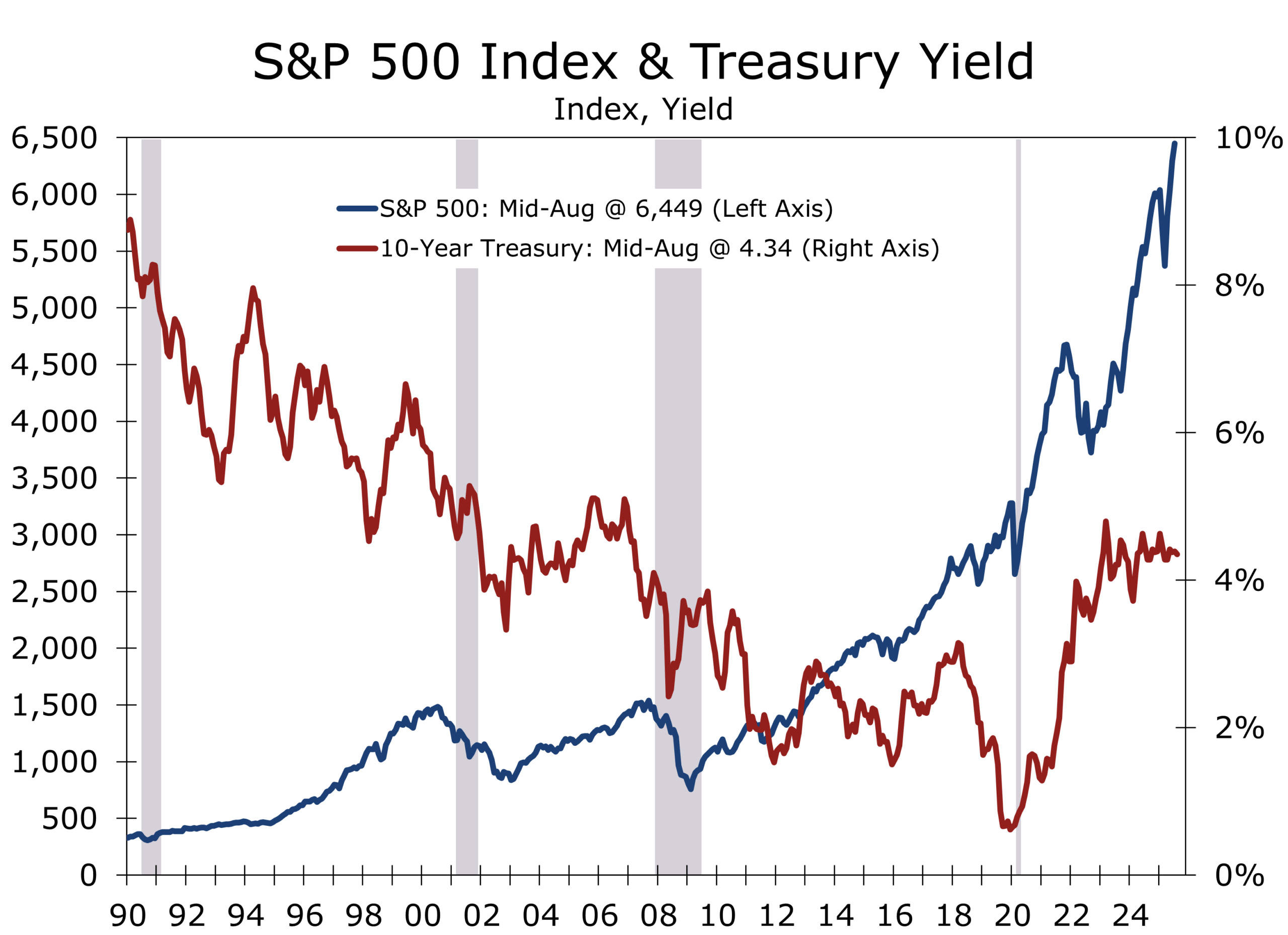

Credit and Rates: The Curve Steepens

Treasury markets digested Powell’s Jackson Hole dovish tone, only to be jolted by President Trump’s firing attempt of Fed Governor Lisa Cook. The episode raised additional questions about Fed independence, pushing term premiums slightly higher, and accelerated curve steepening.

Markets are keeping an eye on threats to Fed independence but show minimal concern.

Two-year yields fell 6–8bps while long bonds edged higher. The 2s/10s spread broke out to 63bps, the widest since early 2022. Corporate spreads remain historically tight, with IG spreads near late-1990s lows. Funding remains accessible, but the risk of abrupt repricing lingers.

A September rate cut remains likely—but will not necessarily be the start of a deep easing cycle. Markets may be over-pricing cuts. Front-end relief is likely, but long-end volatility remains a risk.

Geopolitical Developments: A World on Edge

Israel expanded its proactive military posture, successfully striking targets in Yemen, Syria, and Gaza City. These operations underscore Israel’s view that it is fighting for its survival against adversaries determined to erase it from the map. The elimination of Hamas propagandist Abu Obeida was both a symbolic and operational success, weakening Hamas’s highly effective psychological warfare machine.

Russia has intensified its information warfare campaign across Europe and the U.S., leveraging nuclear threats, propaganda about “inevitable victory,” and divisive rhetoric aimed at weakening Western resolve. Ironically, the strong show of unity among European leaders during recent Oval Office meetings may have hardened Putin’s determination to divide the West. Look for the U.S. to boost armament shipments to Ukraine via European partners.

The Western Hemisphere is also in flux. Guyana’s elections highlighted the fragility of regional stability. Violence erupted when ballot boxes traveling through the disputed Essequibo border region—claimed by Venezuela and rich in hydrocarbons—came under fire from across the border. Venezuela, having ignored a UN ruling to refrain from holding referenda in the territory, continues to challenge Guyana’s sovereignty. Against this backdrop, the U.S. Navy’s deployment of destroyers, amphibious ships, and a submarine near Venezuela is more than counter-narcotics enforcement—it is a signal that Washington is prepared for contingencies in a region where disputed oil wealth and authoritarian governance collide.

Geopolitical pressures continue to fester on multiple fronts but with minimal market impact.

Recent developments point to persistent geopolitical tail risks. Israel’s widening front raises the prospect of an endgame in Gaza and renewed push for the Abraham Accords. Iran will likely attempt to disrupt that timetable. Russia’s disinformation efforts could inject volatility into European assets and policymaking. And in the Americas, Guyana’s elections and the U.S. Navy’s posture near Venezuela tie local politics to global energy dynamics, with potential consequences for oil supply and market volatility.

Appeals Court on Tariffs: Exec Authority Checked

The Court of Appeals for the Federal Circuit dealt the administration a setback last week, ruling 7–4 that the president exceeded his authority in imposing broad-based tariffs under the International Emergency Economic Powers Act (IEEPA). The decision effectively affirmed a lower court’s judgment that tariff authority resides with Congress, not the White House. For now, however, the tariffs remain in place. The court stayed its ruling until mid-October and further delayed enforcement should the administration, as expected, appeal to the Supreme Court. That appeal could extend the tariffs’ life until at least June 2026.

While the ruling clipped one legal avenue, it did not strip the president of tariff powers altogether. The administration could lean on other statutes, including Section 122, which permits tariffs of up to 15% for seven months, or Section 301, which allows for country-specific tariffs, as was used against China in 2018–2019. Both tools are more limited and cumbersome, and an eventual shift away from blanket IEEPA tariffs may push the administration toward narrower sectoral levies—particularly in areas like semiconductors, pharmaceuticals, or furniture—rather than sweeping reciprocal duties.

The administration will likely pivot on tariffs toward specific targeted industries and regions.

How the Supreme Court would rule is far from a sure thing. The majority of the Appeals Court judges were appointed by Democrats and two of the three Republican-appointed justices sided with the president. Treasury Secretary Bessent has argued that tariffs are a tax and would thus be deflationary, which provides a wedge for opponents to argue against tariffs in court. Only congress has the ability to levy taxes. The counter argument is that tariffs work like a tax and are allowed to be placed by the president for several reasons, including national defense and in response to unfair practices overseas.

The implications are threefold. First, the ruling introduces fresh uncertainty into the investment climate. Companies that front-ran imports to avoid tariffs are unlikely to adjust quickly given the possibility of a Supreme Court appeal and continued tariff exposure. Second, the prospect of refunds or retroactive claims if the tariffs are struck down creates fiscal and market volatility, with potential knock-on effects for Treasury issuance and long-term yields. Finally, the case reasserts judicial limits on executive trade powers, a reminder that tariff-first diplomacy, while potent, may prove less durable when tested in court. For markets, the net effect is more uncertainty rather than less.

Risks to Watch

- Tariff-driven inflation: Core PCE is expected to rise back slightly above 3% later this year. A larger move would complicate the Fed’s easing path and likely unnerve the financial markets.

- Fed independence erosion: The markets have largely ignored the Lisa Cook controversy. Further political interference could increase long-end yields, raising borrowing costs even as front-end rates fall.

- Treasury market liquidity: With deficits wide and issuance heavy, even modest shocks could trigger funding stress, ending what has been an unusually good borrowing environment.

- Energy and commodity shocks: Israel’s strikes and U.S. naval moves near Venezuela raise the risk of sudden supply disruptions. WTI oil appears anchored between $60 and $80 a barrel. The markets are pricing in a status quo for both issues, as well as Ukraine-Russia.

The Week Ahead

- Tuesday, Sept 2: ISM manufacturing and construction spending. Manufacturing remains near the 50 threshold; construction is soft, with upside from nonresidential projects like data centers and pharma.

- Wednesday, Sept 3: JOLTS job openings, Beige Book, Auto Sales. Look for continued declines in job openings and quits; Beige Book should reveal tariff effects. Auto Sales likely steady at 15.5–16.0m units.

- Thursday, Sept 4: ADP employment, productivity, jobless claims, trade balance, ISM services. ADP’s deviation from BLS is now seen as more realistic. Productivity should improve modestly; services index watched for hiring/pricing.

- Friday, Sept 5: August nonfarm payrolls, unemployment, wages. Expect around 60k payrolls, unemployment at 4.3%, and 0.2% wage growth. Initial August readings are often inexplicably weak and later revised higher.

Key Takeaways

Last week reinforced a central tension: the economy is resilient enough to keep consumers spending and businesses investing in select sectors, yet fragile enough that the Fed is poised to ease. The prudent course is to secure near-term funding at lower front-end yields, hedge long-end risk, and prepare for tariff-induced surprises.

Geopolitics remain a wild card. Israel’s regional strikes, Russia’s disinformation push, and U.S. naval maneuvers underscore the unpredictability of global risk. The appeals court ruling on tariffs adds another layer of uncertainty, reminding markets that policy made by executive fiat may not withstand judicial scrutiny.

The economy, like the dance floor in July’s income report, still feels steady—but the band is about to change tunes, and no one wants to be caught mid-step when the tempo shifts.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 2, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000