Highlights of the Week

- The U.S. economy shows signs of slowing beneath the surface: consumer spending, housing, and employment have softened, while a spike in aircraft orders drove a jump in durable goods orders.

- Consumer Sentiment rebounded on easing tariff fears and market gains, while Consumer Confidence slipped amid diminished hiring.

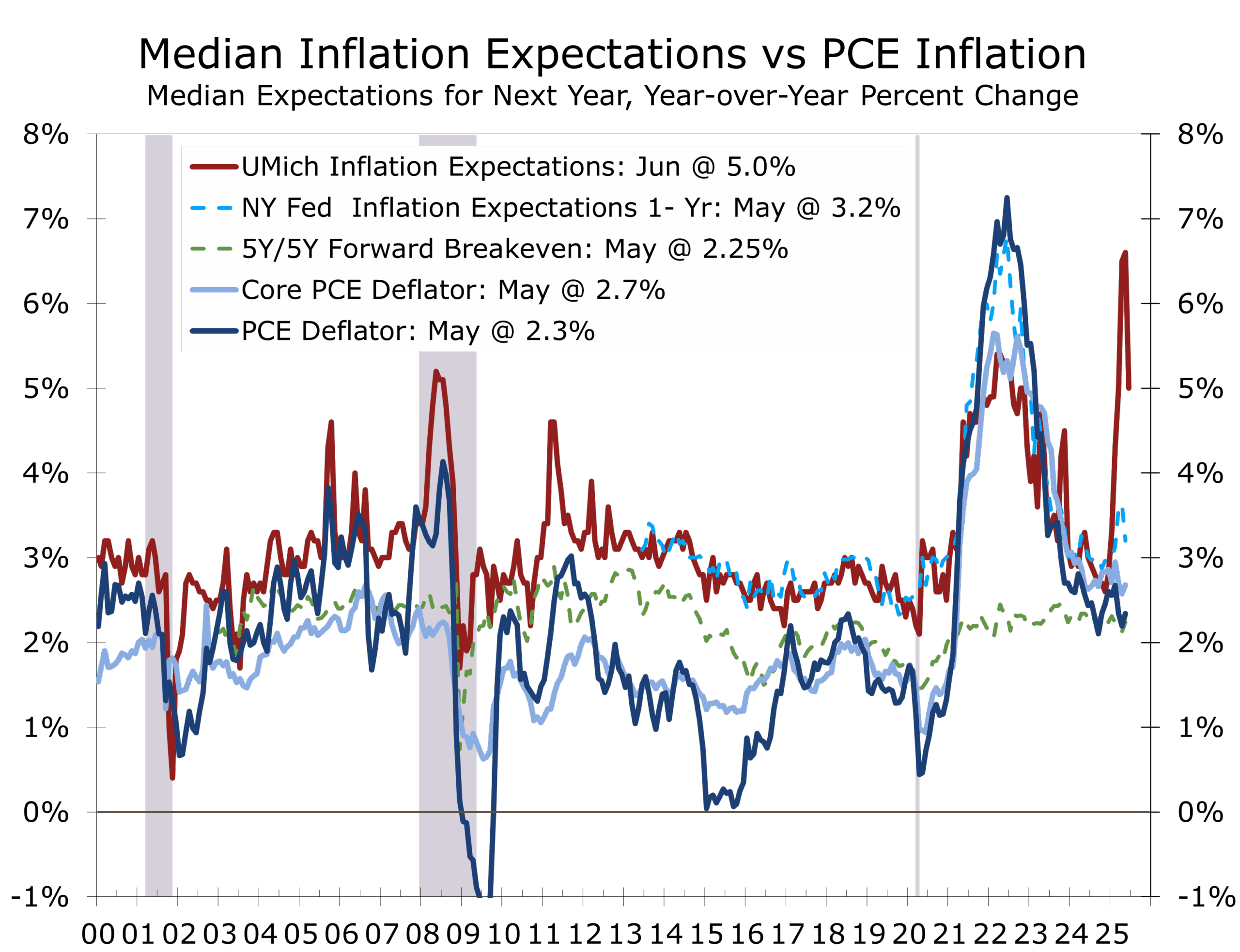

- Core PCE inflation is tracking below 3%, strengthening expectations for a rate cut.

- The U.S. and Israel dealt a strategic blow to Iran’s nuclear infrastructure in a coordinated air campaign, significantly degrading Iran’s enrichment capabilities and command structure.

- Trump’s influence is growing across foreign policy, trade, and fiscal negotiations, as G7 nations recalibrate and momentum builds to end the Gaza War and expand the Abraham Accords.

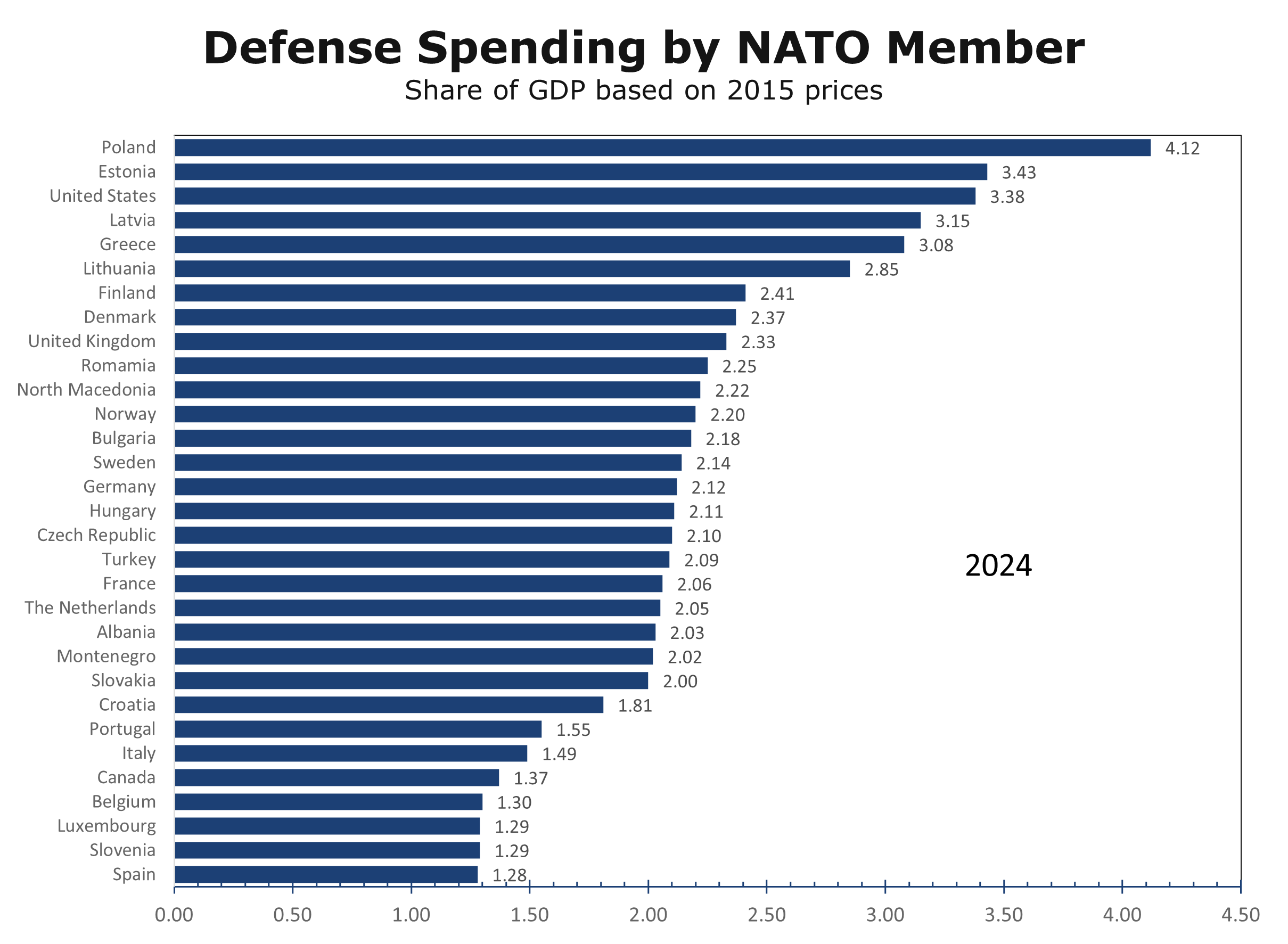

- The NATO summit marked a dramatic political win for Donald Trump, securing European pledges to raise defense spending to 5% of GDP.

- The financial markets are taking note of the improved economic and geopolitical trend, sending share prices to new highs.

Beneath the Resilience, a Slowing Core

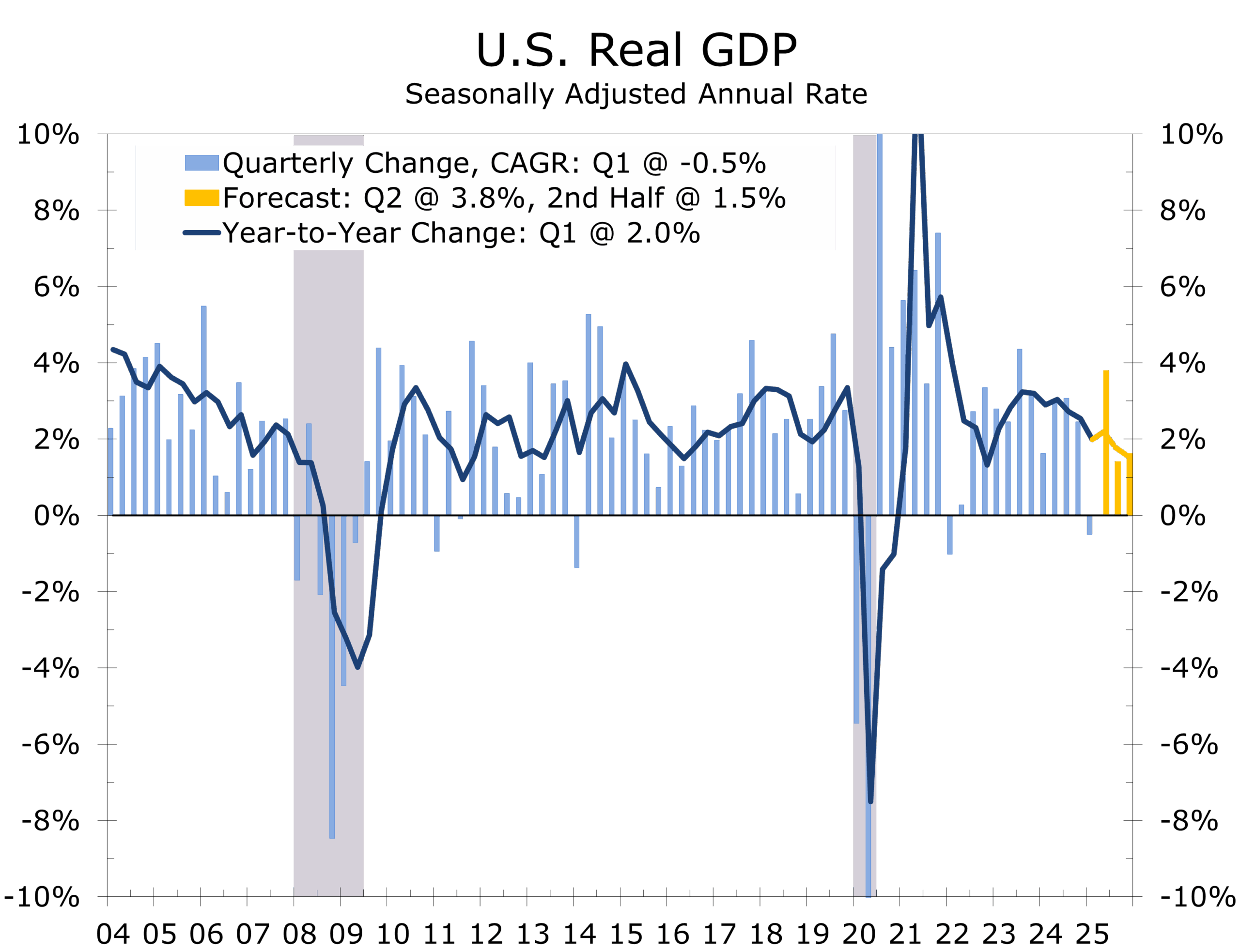

Economic data for the week offered a mixed view: on the surface, business investment and durable goods orders showed surprising strength, but underlying demand is softer than earlier thought and many key measures are flashing warning signals.

Real consumer spending was flat in May, with a downward revision to April. The details were more concerning: services spending fell outright, and goods spending gains came from volatile durables, not essentials. Real disposable income is running below 2% year-over-year, even as the savings rate edges higher — a sign tariffs and broader geopolitical, fiscal and labor market risks weighed on consumer behavior this past spring.

After pulling big-ticket purchases forward ahead of tariffs, consumer spending has moderated.

Consumer sentiment rebounded in June, following six consecutive months of declines. The index was revised higher to 60.7, up 8.5 points or 16% from May, as easing tariff pressures, falling energy prices and rebounding share prices bolstered household finances. Notably, high-income households reported the largest improvement in buying conditions for durable goods. Moreover, the absence of a tariff-induced price surge is improving consumer psyche. Year-ahead inflation expectations fell to 5.0% — still elevated but down significantly from May’s 6.6%.

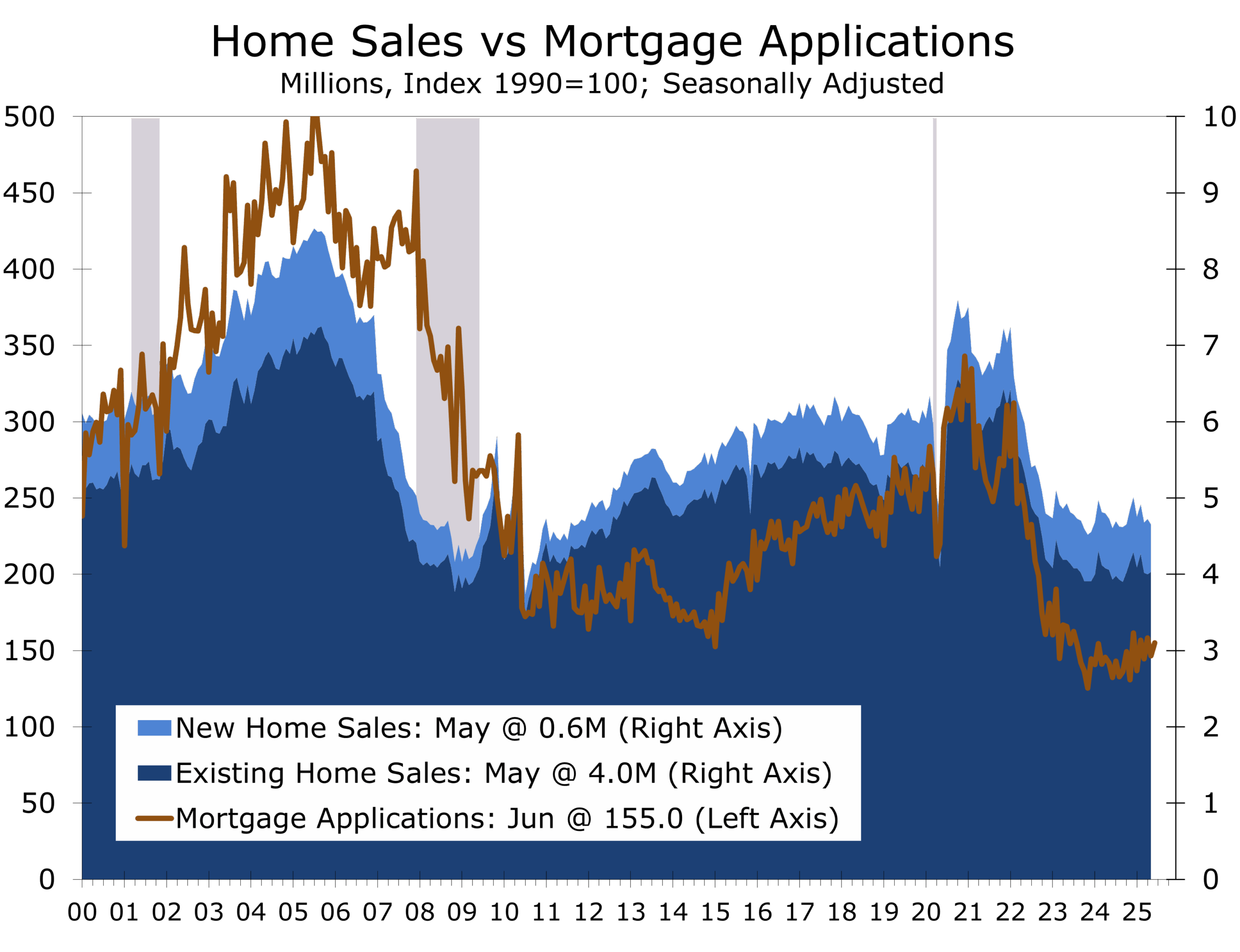

Pending home sales rebounded in May but only partially offset April’s decline. Mortgage rates hovered near 7%, and affordability challenges continue to weigh on demand, especially in the resale market. New home sales also fell, dropping 13.7% to a 623,000-unit pace — the slowest since October 2024 — despite generous builder incentives.

The slowdown in home buying is rebalancing the housing market, with sellers now outnumbering buyers in many areas. Existing home inventory has risen to a 4.4-month supply, while new home inventory has climbed to 9.8 months at May’s pace. This added supply is pressuring prices: the median existing home price is up just 1.7% year-over-year, and new home prices, though higher in May, are down 1.9% on a three-month average.

A surge in commercial aircraft orders sent factory orders soaring in May.

Durable goods orders surged 16.4% in May, the largest increase in over a decade, driven almost entirely by a 230% spike in commercial aircraft following a major Boeing deal with Qatar. Excluding transportation, orders rose a more modest 0.5%, with broad-based gains led by computers, electrical equipment, and fabricated metals. Core capital goods shipments — the key input for GDP business investment — also rose 0.5%, raising expectations for Q2 growth.

Revised GDP data revealed that Q1 growth was even weaker than previously reported. Headline growth was downgraded to a -0.5% annualized pace, as downward revisions to consumer spending and inventories outweighed a modest upside in net exports. More importantly, real final sales to domestic purchasers — a key gauge of underlying demand — rose just 1.9%, the slowest pace in over two years. Nonetheless, our internal tracking model still estimates Q2 GDP growth at 3.8%, supported by resilient consumer spending and business investment in capital equipment.

Awaiting Clarity on the Labor Market and Inflation

Powell reiterated in his congressional testimony that the Fed is “well positioned to wait.” The June SEP projections imply two cuts in 2025, but the dot plot reflects a wider divergence in view. September remains the most likely time for the next Fed move.

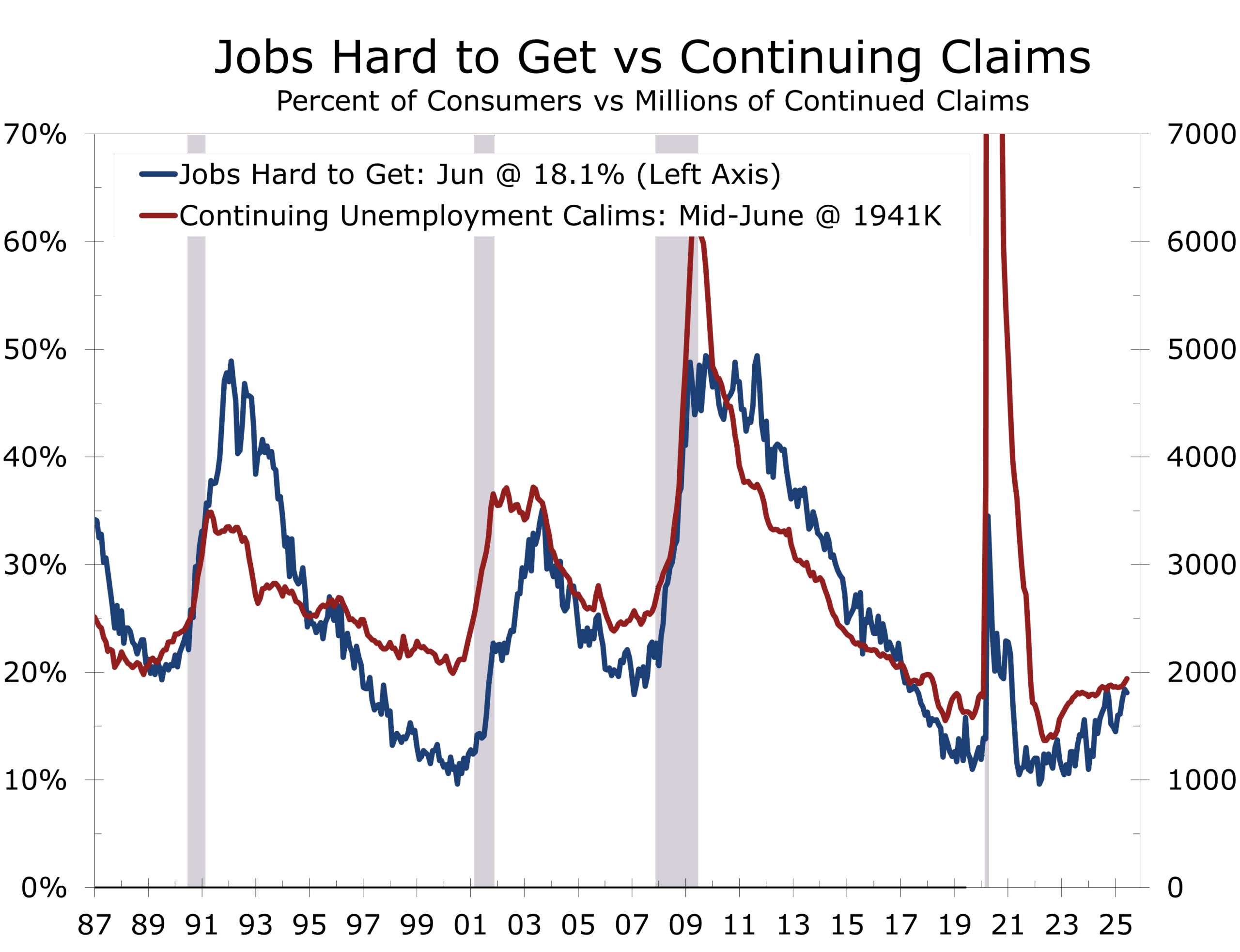

The labor market continues to lose momentum. While initial jobless claims declined modestly in the latest week, continuing claims — a better gauge of trend softness — rose again, hitting the highest level since November 2021. The rise in continuing claims suggest job seekers are having a harder time landing a new job and matches the climb in the share of consumers stating that jobs are hard to get in the Conference Board’s Consumer Confidence survey.

Inflation continues to cooperate. May’s PCE deflator and core PCE deflator came in close to expectations. While inflation remains above the Fed’s 2% target, the trend is moving in the right direction, particularly for problematic areas like core services’ prices.

Precision Strikes, Summits, and Shifting Alignments

The past two weeks marked one of the most consequential periods in global security since the Cold War. Israel launched a coordinated campaign against Iran’s nuclear infrastructure — including the Fordow and Esfahan enrichment sites — in response to what it determined was an “imminent” threat. The United States played a decisive supporting role, deploying B-2 bombers and submarine-launched cruise missiles to finish the job and neutralize deeply hardened targets. The IAEA has confirmed that Fordow’s centrifuges are “no longer operational.”

While Israeli forces led the majority of the strikes, U.S. capabilities were instrumental in penetrating Iran’s fortified facilities. The use of overwhelming force has significantly delayed — and possibly neutralized — Iran’s near-term nuclear breakout potential. Still, uncertainty lingers over whether Tehran managed to relocate any enriched uranium or advanced centrifuges in advance of the strikes. Recent intelligence casts doubt on those claims, and Israel’s targeting of military leadership, nuclear scientists and Iran’s classified nuclear archive will make any restart more costly, complex, and time-consuming.

Back in Washington, public debate focused more on language than results. The strikes’ effectiveness became a political flashpoint, as critics questioned terminology (such as the meaning of obliterated) rather than impact. In reality, Operation Midnight Hammer was a tactical and geopolitical success — the product of operational discipline, deliberate deception, and precision targeting. In an age of leaks, the mission’s secrecy underscored the professionalism of those involved and restored confidence in the Pentagon’s ability to deliver under pressure.

The political implications are equally significant. The operation’s success shifted the landscape, which is likely the driving pushback from outlets historically critical of the administration. While some coverage attempted to reframe the strikes through a partisan lens, the result was unambiguous: the White House delivered on its 60-day ultimatum, and the Pentagon executed with precision and resolve, dispelling lingering doubts about American credibility that had persisted since the failed Afghanistan withdrawal.

A ceasefire between Israel and Iran was announced shortly after the operation concluded. Though early hours saw sporadic retaliatory fire, President Trump moved quickly to deescalate. In a widely reported moment before boarding Marine One en route to the NATO summit, Trump dropped the “F-bomb” in pointed and targeted way before the press. Trump’s use of profanity is rare and deliberate—something he notes in Trump: The Art of the Deal, strategic disruption can be an effective negotiating tool. In this case, the expletive underscored the urgency of de-escalation, sent a clear message to both allies and adversaries, and ultimately helped lock in the ceasefire.

At the NATO summit in The Hague, Trump translated that momentum into broader geopolitical capital. All but one alliance member — Spain — committed to raising defense spending to 5% of GDP over the next decade. It marked a break from post–Cold War norms and reasserted NATO’s relevance in a more volatile multipolar world. Trump’s blend of hard-power diplomacy and political theater resonated, resetting the alliance’s deterrence posture in real time. Trump’s reception at the summit was, by far, the best that he has seen as president.

Meanwhile, the Abraham Accords are regaining momentum. U.S. and Israeli officials have signaled that Saudi Arabia and Syria may be open to joining as part of a broader regional stabilization framework. Proposals are under discussion for temporary Arab League oversight of Gaza and the release of remaining hostages. Trump and Netanyahu are reportedly aligned on a phased ceasefire and long-term political settlement. In a region long defined by deadlock, this moment represents rare forward movement — and the window for action may not remain open for long.

On the trade front, the U.S. and China reached a limited trade agreement late last week, ironing out the details of the Geneva agreement reached to earlier in the month. In addition to a partial rollback of tariffs and renewed Chinese commitments to purchase U.S. agricultural and energy exports, the agreement includes critical provisions on rare-earth minerals. China agreed to resume and expedite rare-earth exports to the U.S., addressing a key bottleneck in supply chains essential for electric vehicles, defense systems, and semiconductors. The deal removes a major overhang for U.S.-based EV and battery manufacturing projects, many of which had stalled due to input shortages and uncertainty around equipment sourcing. While the agreement remains narrow in scope, it serves as a strategic reset—intended to stabilize trade flows, support industrial investment, and ease bilateral tensions ahead of broader negotiations later this summer.

Political Capital Meets Legislative Headwinds

Despite recent geopolitical victories, including the Iran ceasefire and NATO defense pledges, progress on President Trump’s reconciliation package has run into some additional resistance from budget hawks in the Senate. While the administration originally targeted passage before the July 4 holiday, the president has since acknowledged that the timeline is flexible and that negotiations may extend into mid-July.

The most significant development came last week when the Senate parliamentarian ruled that several Medicaid-related provisions — projected to generate roughly $600 billion in savings — violated reconciliation rules. Proposals to cap provider taxes and tighten eligibility standards were deemed noncompliant with the Byrd Rule, which prohibits policy provisions lacking a direct budgetary impact. The ruling forced Senate Republicans to revise the bill’s fiscal framework, removing key offsets and increasing pressure to pare back the legislation’s scope.

While party leaders remain optimistic about passage, the final package is now expected to focus on more politically viable components, including extending the lower tax rates from the 2017 tax bill, some modest tax reforms, energy permitting, and trade enforcement measures. Broader entitlement reforms are likely to be deferred to future legislation.

Headed into the Second Half of the Year

The first half of 2025 has been marked by rapid and consequential shifts on both economic and geopolitical fronts. One theme has emerged with unmistakable clarity: the reassertion of U.S. leadership. From brokering an end to the India–Pakistan conflict to coordinating precision strikes on Iran’s nuclear infrastructure and halting the 12-Day War, the White House has reestablished its strategic presence. A reinvigorated NATO defense posture and renewed momentum behind the Abraham Accords have further reshaped the global security landscape.

Meanwhile, the U.S. economy has navigated a complicated mix of disinflation, softening consumer demand, and intensifying policy debates over trade, tariffs, and fiscal strategy. From the battlefield to the bond market, the first half of the year was defined by disruption, recalibration, and strategic signaling. After early volatility, markets appear to be adjusting to a faster, more forceful pace of change.

As the second half begins, attention will likely turn from disruption to execution. The challenge now lies in translating bold strategic moves into durable outcomes—whether through stabilizing trade relations with China, securing passage of a restructured fiscal package, or reinforcing fragile geopolitical agreements. Institutional resilience, rather than headline momentum, will define this next phase. Financial markets will look for policy follow-through in an environment of cooling growth and rising policy complexity. We continue to expect two rate cuts from the Federal Reserve, with the first likely in September. The path forward may be less volatile, but will demand discipline, coordination, and an ability to manage through this new rapid tempo without making a policy misstep.

Looking Ahead: Week of July 3, 2025

- Chicago Business Barometer (June) – Monday, June 30:

A quiet start to the week, with the Chicago PMI as the sole release. While regional, the index offers an early read on manufacturing sentiment heading from a manufacturing intensive area in a holiday-shortened but consequential week. - ISM Manufacturing Index (June), JOLTS (May), Construction Spending (May) – Tuesday, July 1:

Manufacturing continues to hold its ground amid tariff disruptions. Lean inventories and strong backlogs should keep the ISM index in the high 40s—above the 43.7 level typically associated with recession.

JOLTS job openings will be closely watched. Rising continuing claims and a decline in the share of consumers saying jobs are plentiful suggest growing friction for job seekers.

Construction spending likely declined in May, as residential and commercial activity softened. Data centers remain a key area of strength, but tariffs on Chinese equipment are delaying major manufacturing projects.

- ADP Employment Report (June) – Wednesday, July 2:

ADP payrolls have shown more weakness than the official jobs report, though they may better align with revised BLS data over time. We expect another soft print, though some upward revision to the prior month wouldn’t be surprising. - Employment Situation Report (June), ISM Services (June), U.S. Trade Balance (May), Initial Jobless Claims – Thursday, July 3:

Nonfarm job growth has averaged 135,000 over the past three months, driven by healthcare, hospitality, and local government. We estimate true underlying job growth is closer to 100,000 and are forecasting a 115,000 gain in June. Seasonal noise tied to the school calendar and summer hiring may lead to downside volatility.

ISM Services is expected to rebound modestly, pushing the index back above the key 50 break-even threshold.

Trade data and jobless claims will round out a dense morning of macro releases.

- Geopolitical Watch:

The Big Beautiful Bill could pass the Senate early this week, though reconciliation with the House remains. Final passage is likely by mid-July, with key changes expected on healthcare offsets and fiscal scope.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 28, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000