Highlights of the Week

- Q4 2025 GDP was distorted by the government shutdown, contributing to volatile quarterly readings, though underlying growth remains resilient.

- Consumer spending remains resilient but faces headwinds from slower job growth and tariff adjustments, with imports and inventory dynamics shifting post-Supreme Court ruling.

- Consumer sentiment remains subdued amid geopolitical tensions and policy fog, though it has rebounded slightly from historic lows.

- Business activity is expanding at a moderate pace, with signs of stabilization in the labor market and broadening capital spending.

- Strategic geopolitical pressures continue to pose cascading risks to confidence, markets, and economic stability, amplified by recent tariff resets and the escalation in Iran-US tensions.

A Blizzard of Economic Data Ahead of the Blizzard

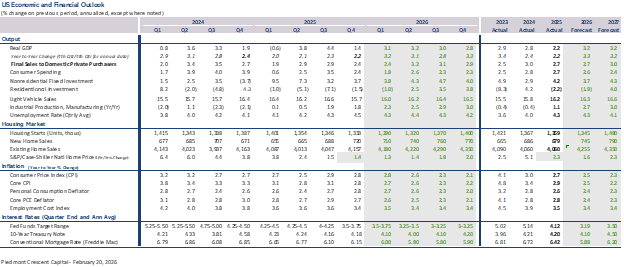

Government statistical agencies are still diligently working to catch up on lost time from the shutdown, resulting in the latest data reflecting a mix of tail-end Q4 2025 and early Q1 2026 figures. While headline growth was softer than anticipated—partly due to the shutdown subtracting from activity—underlying final demand showed resilience. We estimate that the end of the shutdown will add a 1.3pp boost to Q1 2026 growth, pushing our tracking estimate to 3.4% annualized. Real final sales to domestic purchasers advanced solidly, climbing at a 2.4% annual rate. While that is a touch below its recent trend, it is strong enough to support a continued broadening in economic gains.

The shortfall in Q4 growth is not a warning about slower economic growth. Instead, it is evidence that growth faced temporary drags from the government shutdown. The underperformance will likely continue in Q1 due to losses tied to unusually harsh winter weather across much of the U.S. during February. Even with weather distortions, continued productivity gains from AI investment will provide a strong counterbalance to these distortions, and we expect strong Q1 GDP growth.

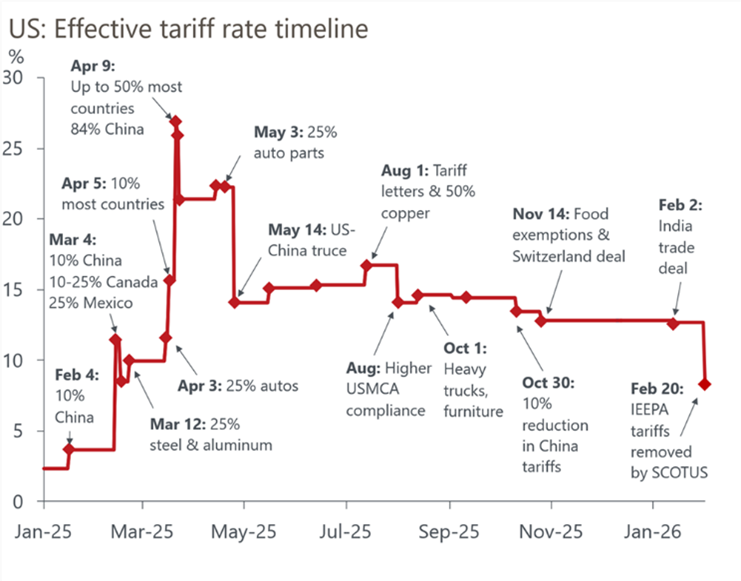

Consumer spending has shown resilience, supported by strong household balance sheets and wealth effects from asset markets. Spending has been bolstered by higher-income households, while broader outlays face pressure from lingering inflation and policy fog. Recent data, however, indicate narrowing breadth. Retail sales ended 2025 on a soft note, and weekly tracking data from the Chicago Fed point to a slight decline in retail sales in January. The Supreme Court’s February 20, 2026, ruling striking down IEEPA tariffs reduced the effective tariff rate from 12.7% to 8.3%, offering a modest boost, though offset by President Trump’s announcement of a new 10-15% global tariff under Sec. 122.

There has been a great deal of discussion recently on who bears the burden of tariffs. We continue to believe the burden has been shared between producers, shippers and wholesalers, retailers, and consumers. Inflation ran about 0.4 percentage points higher in 2025 than it would have otherwise. Nearly all of that showed up in higher prices for goods. The substitution effect has reduced the overall impact. Monetary policy has also remained tight. As a result, higher prices for imported have left consumers with less to spend on other goods and services, which has reduced inflation in these categories.

The bulk of tariff passthrough is now behind us, and we estimate it increased core PCE prices by about 0.7% through January, with a further 0.1% increase in the remainder of 2026. We expect the burden from tariffs to diminish this year and look for inflation to gradually decelerate back to the Fed’s 2% target by year-end.

Sentiment: Subdued and Uneven

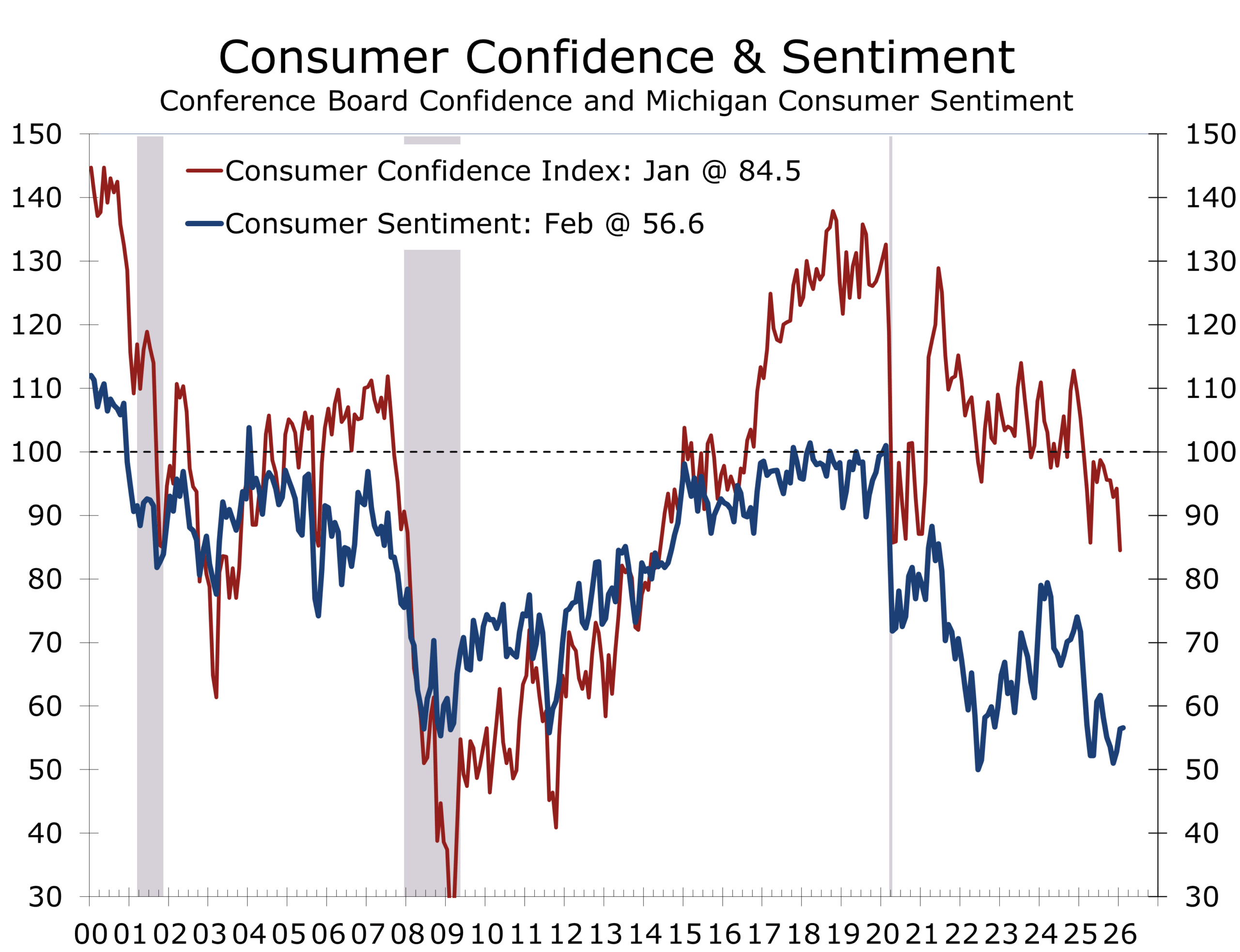

Measures of consumer confidence have stabilized but remain historically low. The two most widely followed measures from the Conference Board and University of Michigan are roughly 15-20% below their year-ago levels amid slower job growth, reflecting the lingering effects of prior inflation, slower job growth, and ongoing geopolitical tensions. Recent improvements reflect the waning impact of tariffs and diminished inflation overall, particularly in gasoline prices and grocery prices other than beef products.

Business Activity: Green Shoots?

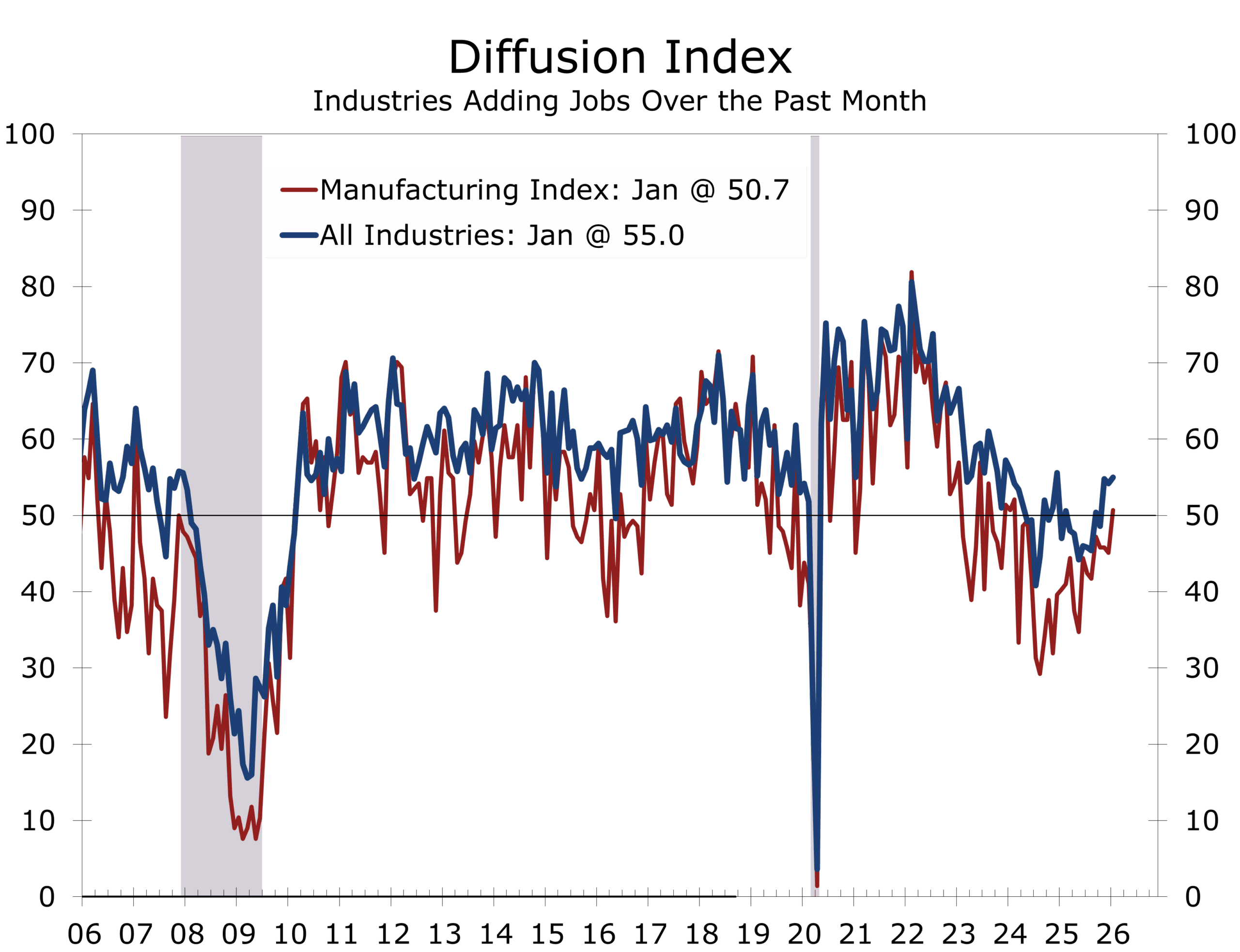

Recent PMI readings and industrial production data show the factory sector improving. The ISM Manufacturing index rose to its highest level since 2022 in January, while manufacturing payrolls posted their first increase in 14 months and gains were broad-based, with the diffusion index for manufacturing employment rising back above the key 50 level. The diffusion index, like the ISM Manufacturing survey, is a measure of the breadth of the strength in the factory sector. A reading above 50 means more industries are expanding and adding to their payrolls than are contracting or reducing staffing.

Consumer and Housing: Weather, Not Weakness

Consumer spending softened at the start of the year, but the weakness appears more short-term oriented. Overall retail sales were flat in December and core retail sales fell 0.1%. Even after the cooldown, holiday retail sales turned in a solid performance, rising 3.7%. December’s drop reflects payback effects from earlier strength and harsh winter weather weighing on activity. Final demand remains supported by steady employment and easing inflation, limiting downside.

This looks like weather distortion and seasonal payback, not a demand pullback.

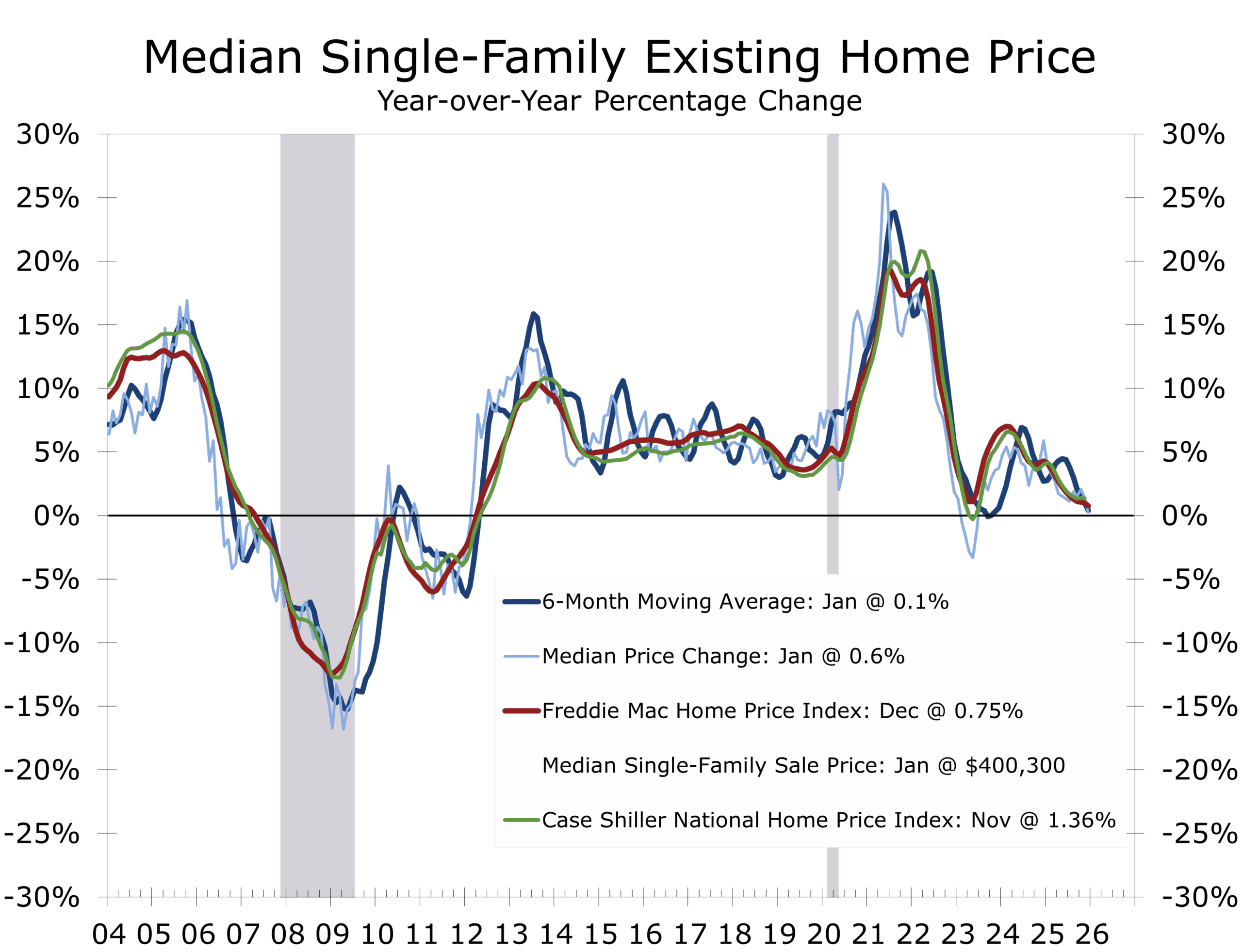

Housing activity also started 2026 on a weak note. Existing home sales fell 8.4 percent in January to a 3.91 million annual pace, well below expectations, with prior months revised lower. Harsh winter weather likely contributed to the decline, and tight inventories compounded the slowdown. For-sale supply slipped again in January and remains constrained, though inventory typically improves heading into spring.

Median home prices fell 2 percent and are up just 0.9 percent over the past year. As mortgage rates ease and labor markets stabilize, sales should gradually climb back. We are looking for a solid spring selling season and look for housing to add to economic growth in the second half of 2026.

The advance PMIs for February released this past week fell back slightly, possibly impacted by the harsh winter weather, but remain in expansion territory. Both the manufacturing and services indices dipped slightly during the month, but both remained above the key 50 break-even level that signals growth in the factory sector.

Core factory orders also remain solid, although the headline data continues to be battered around from month-to-month by swings in orders for commercial aircraft. Shipments were up solidly in December, which means the factory sector likely entered this year with solid momentum.

The apparent improvement in the factory sector is a green shoot worth watching. We have been expecting to see a rebound in the most cyclical parts of the economy, which were hit hard by tariff uncertainty and inflation fatigue among consumers. We expect that rebound to become apparent later this spring or early this summer. The January data suggest the rebound might come even earlier.

Blizzard Navigation: Interpretation

Three themes emerge from the data:

- Momentum Is Moderating, Not Collapsing. Household consumption is positive but facing tariff-related headwinds. Despite the slowdown in headline GDP growth, the economy is still growing solidly. Final Sales to Domestic Purchasers rose at a 2.4% pace in Q4 and rose 2.7% Yr/Yr in Q4. For 2026, real GDP is likely to rise 3.3% Q4/Q4, thanks to the lower comp, while Final Sales to Domestic Purchasers rises at the same 2.7% pace it did this past year.

- Income and Wealth Divergence Matter. Spending strength is concentrated among wealthier households, while middle- and lower-income segments continue to exhibit caution. This pattern has implications for durable goods, housing, and discretionary services, especially with AI-driven productivity offsetting some labor pressures.

- Policymakers Are Flying Through Fog. With core inflation still above target and growth stabilizing, the Fed faces a delicate balance: ease too soon and risk reaccelerating prices amid tariff volatility; wait too long and risk tightening into a slowdown. FOMC minutes from January highlight hawkish tones, with some members open to hikes if inflation persists. We believe such talk is simply the Fed’s Open Mouth Policy intended to reassure the bond market.

Businesses, investors and consumers are behaving like drivers in heavy snow. They have slowed down, are proceeding more cautiously, and remain overly responsive to short-term visibility changes rather than structural conditions.

The Piedmont Perspective

Strategic Pressure: Why Weakness on One Front Would Likely Snowball Across All Fronts

The economy today is not just an aggregation of GDP figures and spending patterns. It is tightly connected to the strategic pressures facing U.S. policymakers—and investors are pricing that in. The Trump Administration’s emphasis on tariffs and trade deals blends seamlessly into geopolitics, often touted as a tool for ending conflicts or pressuring adversaries toward negotiations. This heightened role of trade and tariffs is critical to understanding the current long list of global hot spots, where economic leverage intersects with security concerns.

President Trump’s emphasis on tariffs and trade deals blends seamlessly into geopolitics.

Across multiple theaters—Venezuela, Iran, Taiwan, Russia/Ukraine, Israel-Hamas-Hezbollah, and most recently Mexico’s drug cartel crisis—the U.S. faces simultaneous stress tests. Each region bears its own risks, but they are interrelated in ways that amplify economic uncertainty.

- Venezuela’s Output and Oil Dynamics. Persistent instability keeps global oil markets on edge. The recent departure of Cuban advisors from Venezuela marks a potential shift, reducing some foreign influence and creating an opening for U.S. engagement. This has been framed as a “stand tall” moment in broader negotiations with China, which has significant investments in Venezuelan oil. The current Venezuelan regime is working closely with the Administration, which could aid supply normalization. The seizure of sanctioned tankers is also helping ease supply concerns at the margin.

- Iran and the Gulf. Escalating tensions, including Iran’s military drills restricting parts of the Strait of Hormuz, elevate risk premia. Disruptions in the Strait or Red Sea corridors ripple through global supply chains and commodity markets—impacting prices, production costs, and confidence. Brent prices rose 6% last week amid these tensions, though we expect easing once de-escalation occurs. Negotiations remain fraught, with tariffs positioned as leverage to curb Iran’s nuclear ambitions and regional influence.

- Taiwan and the Tech Supply Chain. Taiwan remains the central node in global semiconductor production, particularly in advanced logic chips critical to AI infrastructure, cloud computing, and next-generation defense systems. Any escalation in cross-Strait tensions would represent more than a geopolitical flashpoint; it would constitute a direct supply-side shock to the capital investment cycle that has underpinned recent productivity gains.

The current AI build-out is capital-intensive and hardware-dependent. A disruption to Taiwanese semiconductor output would slow equipment investment, compress earnings expectations across the technology complex, and raise global risk premia. Financing conditions would tighten not because of monetary policy alone, but because uncertainty would lift required returns on capital.

Trade agreements and semiconductor partnerships serve a dual function: economic integration and strategic deterrence. The deeper the cross-border commercial ties, the higher the cost of escalation.

Reports that Beijing is pressing Washington to delay or dilute an agreed arms package to Taiwan—using the prospect of postponing high-level meetings as leverage—introduce an additional layer of uncertainty. Markets will focus less on the diplomacy itself and more on the signal. A perceived weakening of deterrence would likely raise volatility across technology equities, defense names, and Asia-linked assets. Reinforcement would signal policy consistency and reduce tail risk.

From a macro perspective, Taiwan is not a peripheral issue. Stability in the Taiwan Strait underpins a substantial portion of global capital formation, productivity growth, and equity market valuation. Credibility in that theater carries economic consequences within and well beyond the region.

- Russia/Ukraine and Energy/Defense Markets. The prolonged conflict keeps energy markets and defense spending elevated. Escalation or stalled diplomacy maintains high risk premia, diverts capital toward safe assets, and compresses risk-asset valuations. Wheat prices have tracked higher due to geopolitical risk premiums from this flashpoint. Tariffs on Russian goods amplify economic isolation as a strategy to weaken resolve.

- Israel-Hamas-Hezbollah Centrifuge. The Middle East remains a powder keg. An expanded conflict could shock oil markets, complicate U.S. force deployments and alliances, and reinforce economic caution in corporate boardrooms globally.

The risk here mirror those with Taiwan/China. The buildup of U.S. forces in the region suggests a major intervention is likely soon. Iran will likely respond violently as the regime’s survival would be at stake. Iran would likely strike oil facilities in the Arabian Gulf, which would send oil prices higher but not threaten energy supplies in the U.S., which is amply supplied. Ultimately, we expect the Iranian region to be toppled this year. Anything less than that would make a Chinese move against Taiwan more likely.

- Mexico, Cartels, and Border Economics. Security instability along the southern border affects labor markets, supply chains, and cross-border commerce. Firms factor these into investment decisions and logistics costs, exacerbated by recent tariff changes on Mexico. The situation has intensified following the killing of a powerful drug lord by the Mexican military. The cartel has responded violently, but mostly by destroying property and overrunning airports in tourism-centric parts of Mexico.

Taken together, weakness on any one of these fronts would cascade:

- Commodity Price Shock → Feed inflation → Fed policy tightening or delayed easing

- Supply Chain Shock → Raise costs → Consumer price pressures → Consumer spending slows

- Risk Premia Shock → Raise discount rates → Lower asset valuations → Lower wealth effects

- Corporate Caution → Delay hiring & capex → Softening growth cycle

- The U.S. opts for Expediency: Effectively Showing Weakness → Emboldening China on Taiwan and Russia with Ukraine → Further Increasing Global Geopolitical Instability → Raising risk premia

In chess, a weakness on one flank invites attack across the board. In macro-geopolitics, a breakdown in any of these theaters tightens financing conditions, weakens confidence, and slows growth globally.

Today’s market blizzard isn’t snowflakes—it is the accumulation of strategic pressures with cross-linked knock-on effects, now compounded by the Supreme Court tariff ruling and policy responses.

Looking Ahead: The Week in Data and Policy

This week’s economic calendar features several key data releases that could provide further insights into the trajectory of growth, inflation, and labor market stability. On Monday, factory orders for December are expected to show a modest decline, reflecting ongoing manufacturing softness amid trade uncertainties. Tuesday brings housing market indicators with the S&P Cotality and FHFA home price indices for December, anticipated to post small gains, alongside Conference Board consumer confidence for February, which may edge higher following last month’s plunge. Thursday’s initial jobless claims will offer a timely read on labor market health, while Friday’s PPI report for January, which is projected to rise 0.3%, will be closely watched for signs of persistent price pressures, especially in core measures excluding food and energy. Construction spending data for December and November revisions round out the week, which should show weakening residential building and some stability in nonresidential construction.

Fed speakers will dominate the policy landscape, with multiple officials providing updates on monetary policy amid the tariff reset and geopolitical fog. Governor Waller speaks twice on Monday and Tuesday, likely reiterating his view that rates should move closer to neutral given inflation nearing target ex-tariffs. Other notable appearances include Governors Cook and Bowman, as well as regional presidents like Goolsbee, Collins, Bostic, Barkin, Schmid, and Musalem, many emphasizing caution on inflation risks despite labor market weakness. Adding to the week’s significance, President Trump delivers the State of the Union Address on Tuesday evening at 9 p.m. ET, where he is expected to outline priorities on the economy, trade deals, tariffs as a geopolitical tool, and ongoing conflicts, potentially influencing market sentiment and policy expectations.

Final Thought

Economic data from last week confirms a key theme: visibility has become a greater concern than slower growth. Growth is stabilizing, sentiment remains subdued, and consumer strength is uneven—making for tough sledding ahead—while strategic risks from oil to semiconductors to geopolitical flashpoints add layers of complexity that markets are pricing defensively.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 23, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000