Highlights of the Week

- Incoming data continue to support a soft-landing narrative, but the composition of growth is shifting in a more durable direction.

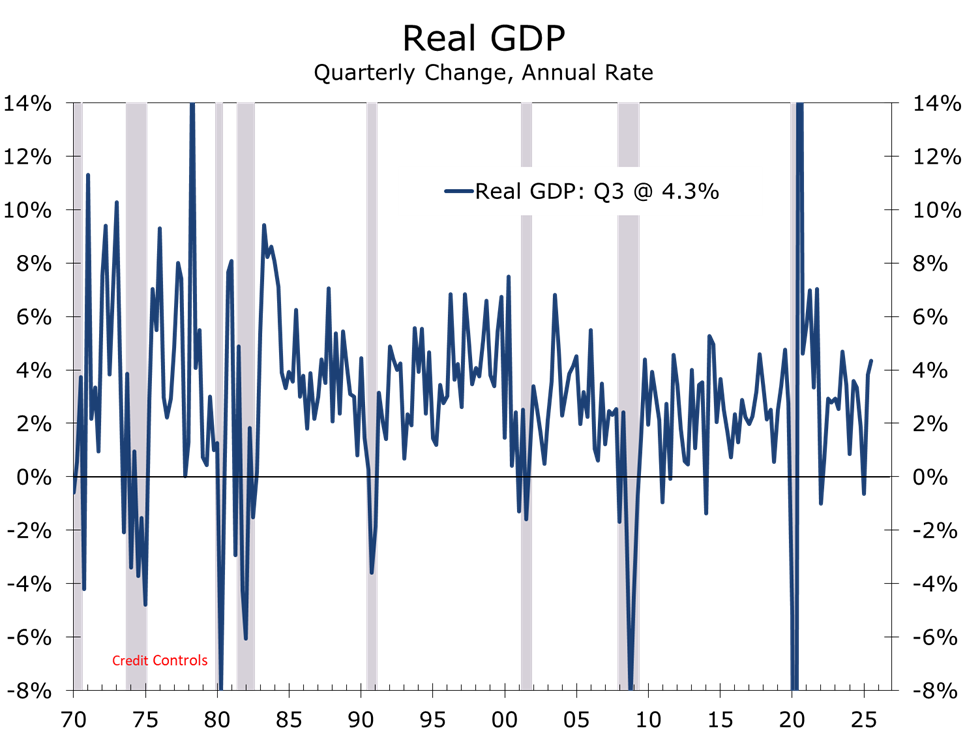

- The latest Atlanta Fed GDPNow projects Q4 real GDP growth at a whopping 5.3% pace, though likely overstated by unusually wide swings in international trade and inventories.

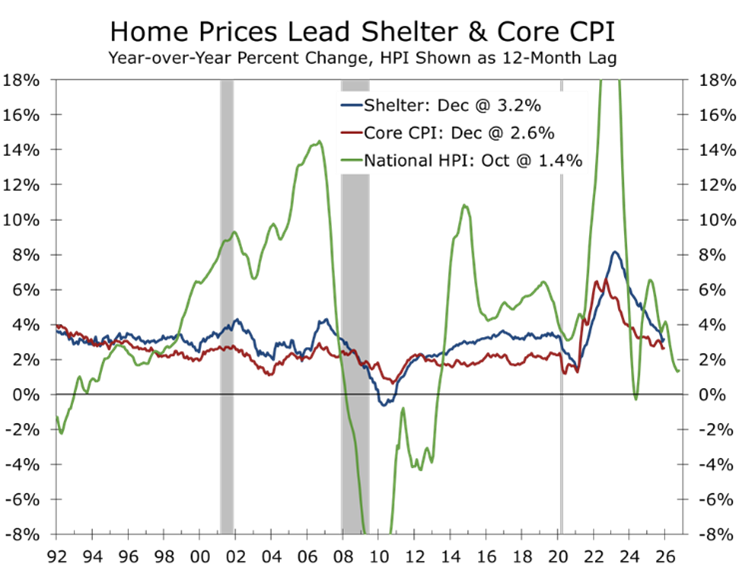

- Inflation is cooling unevenly, with shelter remaining the last mile, yet underlying cost pressures are easing more convincingly.

- Financial markets are repricing term premia and institutional risk, not growth.

- The economic script has flipped toward capital-led growth, pointing to stronger growth, lower inflation, and lower interest rates in 2026.

- U.S. real GDP growth in 2026 now looks likely to run close to 3 percent.

- This week’s Piedmont Perspective revisits credit controls through the lens of Jimmy Carter’s 1980 experiment, with uncomfortable parallels to current policy proposals

Data That Anchored the Narrative

The past week delivered a dense run of economic data that reinforced—rather than altered—the prevailing macro story. Growth is cooling toward trend but remains intact. Inflation continues to ease, though not smoothly. The labor market is adjusting through slower hiring rather than rising layoffs. Against that backdrop, markets spent the week trimming expectations rather than reassessing direction.

Inflation: The Signal Beneath the Noise

Core CPI rose 0.24 percent month-over-month in December, leaving the year-over-year rate at 2.6 percent. On the surface, the print fits neatly within the soft-landing narrative. Beneath the surface, the trend looks even better.

The three-month annualized change smooths through distortions created by the government shutdown and seasonal noise. On that basis, core CPI is running at roughly 1.8 percent annualized, or closer to 2.0 percent after accounting for the known downward bias in shelter that will not see a full offset until April. In short, the inflation trend is better than the monthly prints imply once shutdown noise and shelter timing are stripped out.

Manufacturing is contracting overall but expanding in capital-intensive segments.

Shelter remains the last mile, but not the obstacle. Outside of housing, inflation continues to cool as goods disinflation persists and services inflation grinds lower alongside improving productivity.

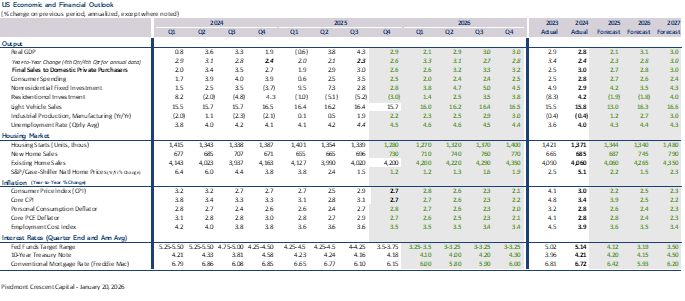

The federal statistical agencies continue to catch up on delayed data releases, including the closely watched personal income and spending figures, with October and November data due this Thursday. The core PCE deflator—the Fed’s preferred inflation gauge—is likely to paint a slightly less optimistic picture, finishing 2025 just under 3 percent year-over-year. The monthly path will be uneven, but the direction remains favorable. We expect core PCE inflation of 0.2 percent in both October and November, followed by a firmer 0.3 percent reading in December, which will be released in February.

Preliminary January consumer sentiment data suggests households increasingly believe the worst of tariff-driven inflation is behind them. Inflation expectations remain elevated relative to recent realized inflation and measures of price breadth, but market-based inflation expectations, which the Fed weights more heavily, remain well anchored just above the 2 percent target.

Revisions suggest underlying demand is cooling beneath still-strong GDP growth.

Based on the latest employment and retail sales data, along with revisions to prior months, we estimate personal spending was flat in October and rose 0.4 percent in November. We have trimmed our estimate for fourth-quarter consumption modestly while raising our estimate for inventory accumulation. Our fourth-quarter GDP forecast remains well above consensus, near a 2.9 percent annualized pace.

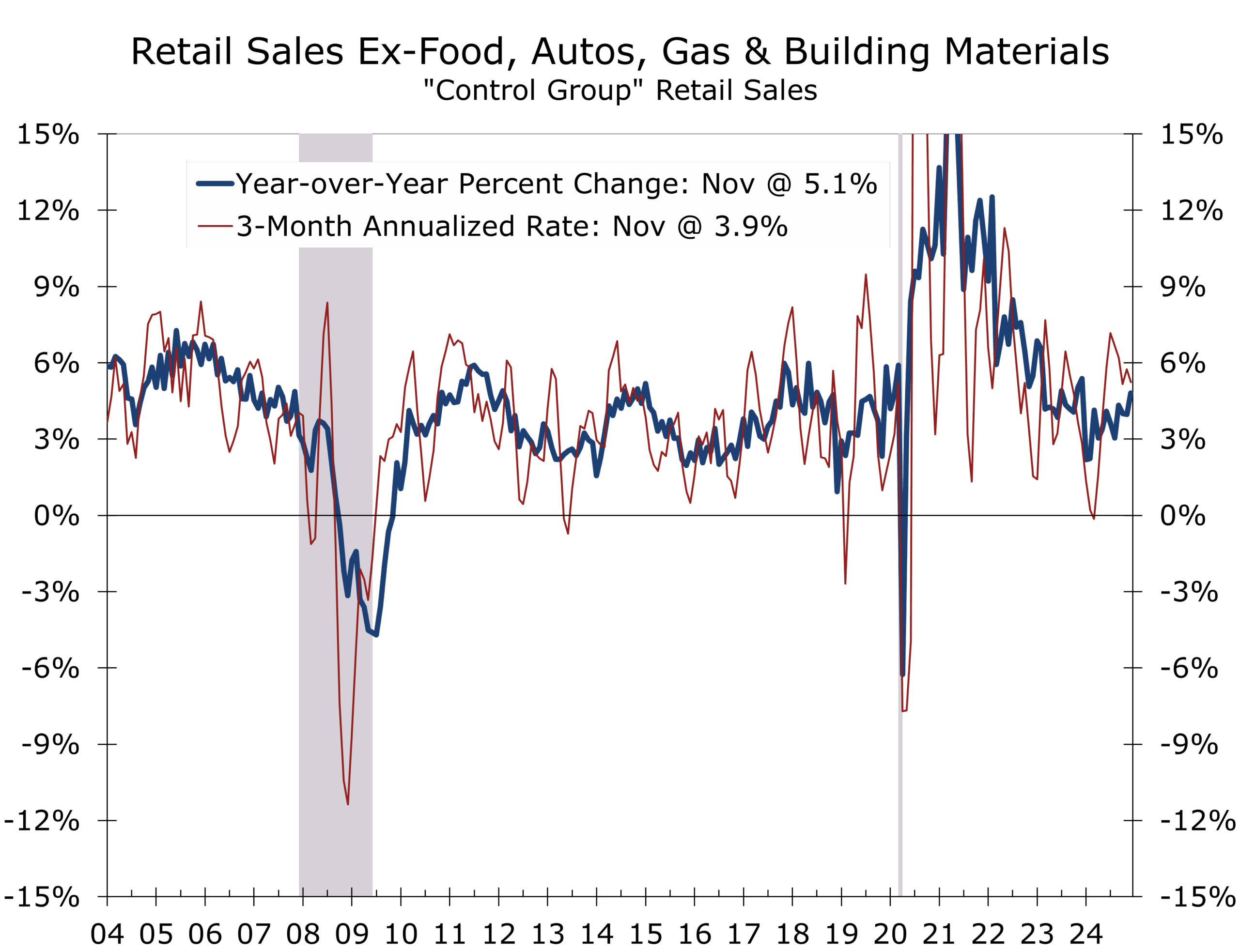

Industrial production rose 0.4 percent in December, with manufacturing output up 0.2 percent, reinforcing the view that activity remains firm in capital-intensive sectors. Core retail sales rose 0.4 percent in November, but downward revisions to September and October trimmed cumulative momentum. Both the Empire State and Philadelphia Fed manufacturing surveys surprised to the upside in early January, suggesting factory output is stabilizing and potentially gaining traction.

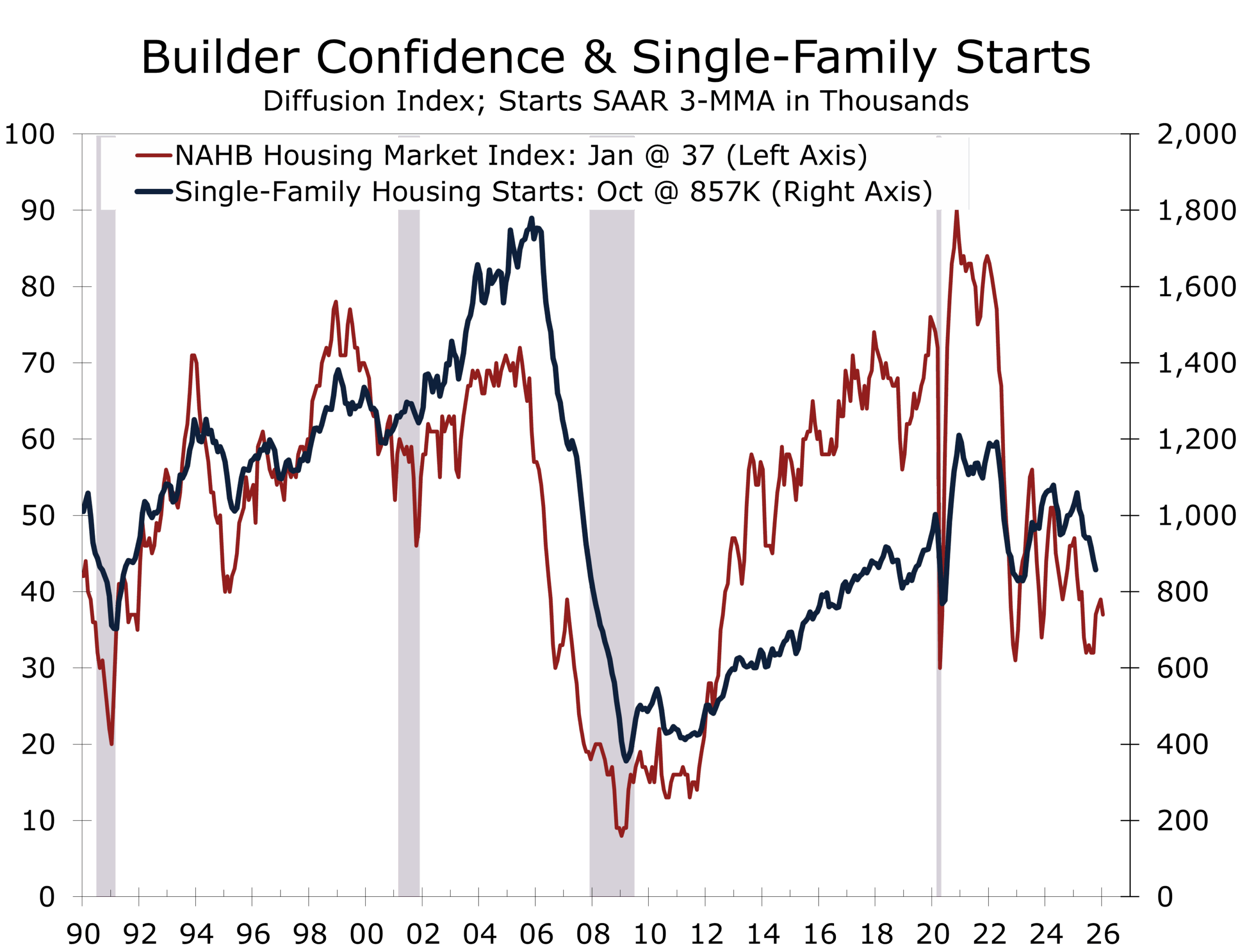

Homebuilder sentiment weakened at the start of the year as inventories of completed homes increased and near-term demand softened. Incentives remain widespread. Lower mortgage rates should provide incremental relief, but housing remains constrained by supply rather than collapsing demand. Existing home sales surprised to the upside, rising to a 4.35-million-unit pace, the strongest reading since early 2023.

Housing is lagging the cycle but no longer leading it lower.

We expect an elongated housing recovery in 2026, with sales improving in the first half of the year as mortgage rates drift back toward the 6 percent range. Elevated inventories of unsold homes are likely to restrain new construction, particularly given repeated bouts of policy uncertainty that have contributed to volatility in bond markets and mortgage rates.

Credibility Risk Replaces Timing Risk

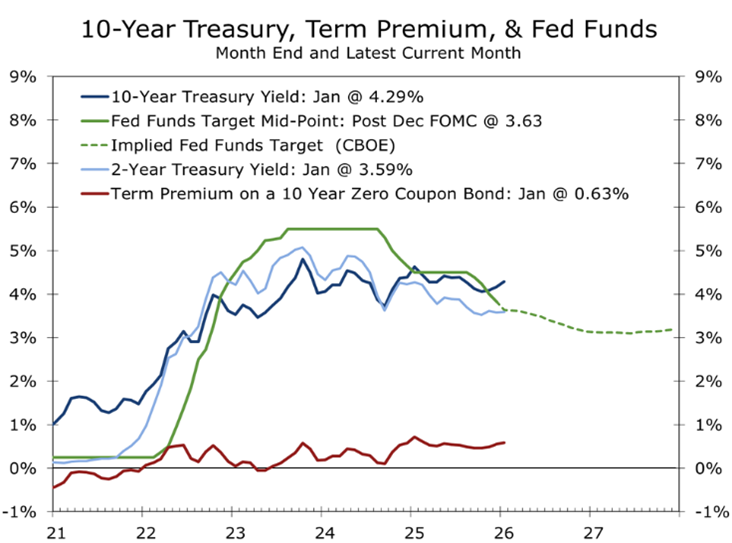

Markets are no longer debating the precise timing of rate cuts. They are increasingly pricing institutional credibility as a balance-sheet risk variable.

The recent market configuration is instructive. Global equities sold off while the dollar weakened and gold rallied. In a conventional risk-off episode, investors would expect dollar strength and falling long-dated yields. That pattern did not materialize. Instead, the price action reflects uncertainty around policy consistency and governance rather than an imminent downturn in demand.

For corporate treasurers, the implication is that long-term funding costs may remain volatile even as inflation cools. Term premia, not short-rate expectations, are driving rate moves. Investors are assigning a small but non-zero probability that political pressure could influence monetary or trade policy at the margin. That risk shows up in the cost of duration, FX hedging, and insurance.

Credit markets remain orderly. Spreads are contained and access to funding is intact. The adjustment is occurring through hedging costs and risk premia, not a withdrawal of liquidity.

This environment favors funding discipline over rate-cut optimism. Opportunistic term issuance, stress-testing of cash and FX hedges, and flexibility in duration exposure matter more than precisely timing the first rate cut.

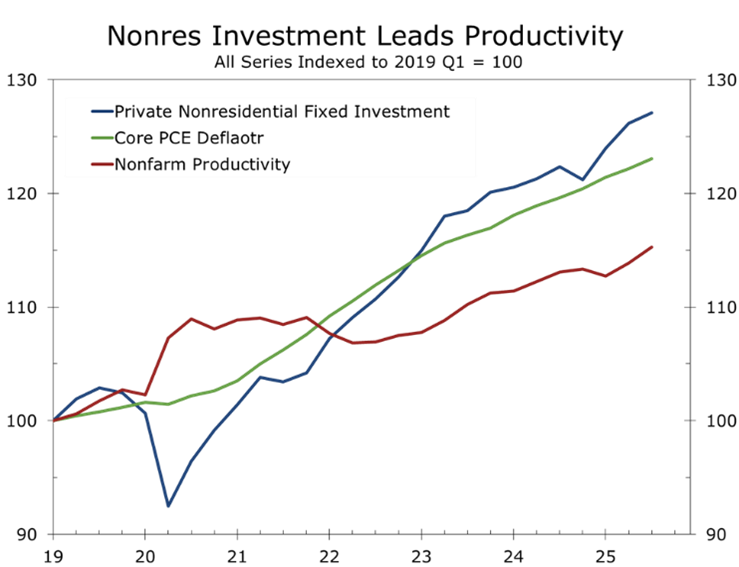

The Script Has Flipped: Capital Over Calories

For much of the past decade, growth relied on consumption, leverage, and fiscal sugar highs. That model delivered speed, not durability.

This cycle looks different. Growth is increasingly driven by capital investment in AI infrastructure, power generation, advanced manufacturing, aerospace, biopharma, and defense—long-cycle investments tied to productivity and resilience rather than leverage.

This is a capital-fed expansion, not a credit-fed one. Stronger growth can still be disinflationary.

Productivity has surged, and the multi-year trend since 2019 is consistent with roughly 2 percent annualized growth. Inventory rebuilding and reshoring reinforce the durability of the expansion.

Setting the Stage for 2026

The data and the evolving composition of growth argue for a more constructive 2026 than consensus implies. A capital-led expansion supported by productivity gains and inventory rebuilding is well positioned to deliver stronger real growth with less inflation pressure.

Under this mix, U.S. real GDP growth in 2026 now looks likely to run close to 3 percent. Lower interest rates become the outcome of disinflation, not its precondition.

Policy remains the wild card.

Piedmont Perspective

Echoes of Jimmy Carter: Credit Controls Revisited

President Trump’s proposal to cap credit-card interest rates at 10 percent reflects a familiar impulse. Affordability pressures rise, and policymakers reach for visible solutions.

Credit controls do not make borrowing cheaper. They make credit scarcer.

The closest historical parallel is President Jimmy Carter’s 1980 credit controls. Inflation did not fall. Credit availability collapsed, consumer spending retrenched sharply, and the economy entered a steep recession. Real GDP declined at an 8% annual rate in Q2 1980, marking one of the steepest quarterly drop on record.

A rate cap would operate through the same channel today. Credit would contract most sharply where marginal propensities to spend are highest. History suggests such policies stick briefly, then snap—and make a mess.

Greenland in the Crosshairs

Ukraine and the Middle East continue to add background risk rather than acute shocks. The more consequential geopolitical development for markets this week has emerged from the Arctic. The escalating U.S. push to assert control over Greenland has become a flashpoint, underscoring how trade policy is increasingly being used as geopolitical leverage and why the Arctic is no longer a peripheral theater.

President Trump’s posture has hardened since early January, following what the administration views as a successful assertion of hemispheric control in Venezuela. The Greenland episode fits a familiar strategic pattern: advancing foreign policy objectives through executive action amid domestic legislative gridlock and heightened judicial scrutiny. Trump’s negotiating style has long relied on opening from an extreme position, forcing counterparts to engage from ground they would not otherwise accept.

The centerpiece of the strategy is a tariff ultimatum announced via social media. Beginning February 1, the United States would impose 10 percent tariffs on imports from Denmark and seven European allies—Norway, Sweden, France, Germany, the United Kingdom, the Netherlands, and Finland. Those tariffs would rise to 25 percent by June 1 unless a deal is reached for what the president described as the “complete and total purchase” of Greenland.

Greenland’s strategic value explains the intensity of the standoff. The island occupies a central position in Arctic missile-defense architecture, hosting early-warning radar systems critical to U.S. and NATO detection of ballistic and hypersonic threats from Russia. Control of Greenland also strengthens oversight of North Atlantic and Arctic shipping corridors as melting ice opens new routes between Asia, Europe, and North America. These developments carry commercial promise but introduce new security and surveillance challenges.

Layered on top of defense and shipping is geology. Greenland holds significant rare-earth deposits essential to advanced electronics, renewable energy systems, and defense manufacturing. Any disruption to Arctic cooperation or European alignment would have second-order implications for supply chains already undergoing reshoring and diversification.

European leaders have responded forcefully, warning that the move risks fracturing NATO and triggering a retaliatory trade cycle. U.S. imports from the targeted countries have averaged roughly $360 billion annually over the past three years, while European officials have identified more than $100 billion in potential countermeasures. In Greenland itself, protests underscore local resistance, and Danish officials continue to reaffirm sovereignty.

From a market perspective, the episode matters less because conquest is likely and more because escalation is plausible. The probability that the United States would attempt to seize Greenland by force appears exceptionally low—likely 20 percent or less—given institutional constraints, waning public support, bipartisan opposition in Congress, and legal limits embedded in the National Defense Authorization Act. The odds that emergency tariffs ultimately survive judicial scrutiny have also diminished. In short, checks and balances still matter.

Markets are not pricing certainty. They are pricing tail risk.

That is exactly what they are doing. Volatility has risen, term premia have widened, and classic insurance assets have been bid. The VIX has moved to three-month highs, not because global growth is in doubt, but because alliance stability and policy predictability have become less certain. We do not envision an outcome that materially jeopardizes NATO. Still, markets remember how aggressively Trump has pressed allies in the past—on defense spending and Nord Stream among them—and are struggling to price a negotiating style that deliberately tests institutional boundaries.

Bottom Line

The macro story still reads soft landing. The growth story reads capital led. The market story reads credibility sensitive.

This is a regime adjustment, not a regime break. The repricing is quiet at first and historically modest. The implications are not.

The Week Ahead: Validation, Not Revelation

The coming week is less about new information than confirmation. With the Fed in blackout ahead of the January FOMC meeting, markets will focus on data consistency rather than policy signaling.

What Matters

Construction Spending and Pending Home Sales (Wednesday)

Core PCE inflation (Thursday). We expect monthly gains of 0.2 percent in both October and November, corresponding to year-over-year rates near 2.7–2.8 percent. Confirmation would reinforce confidence that disinflation remains intact despite December noise.

Personal income and spending. Income is expected to rise 0.2 percent in October and 0.4 percent in November, with spending flat in October and up 0.4 percent in November, broadly consistent with recent retail sales data.

Labor market consistency. Initial claims are expected to rebound toward 210k. As long as claims remain at historic lows and continued claims do not trend higher, the labor market will be viewed as cooling, not cracking.

PMIs and sentiment. January preliminary PMIs and final Michigan sentiment will help gauge whether risk headlines are bleeding into real activity.

What Matters Less

Headline rate volatility absent a sustained move in term premia.

Geopolitical headlines that do not disrupt energy flows or trade logistics.

Bottom Line for the Week

The burden of proof remains on downside risks. Absent a negative inflation or labor-market surprise, markets are likely to continue trading the same theme that has defined the start of the year: steady growth, cooling inflation, and rising sensitivity to policy credibility rather than actual cyclical stress.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 20, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000