Highlights of the Week

- The economy continues to expand above trend, but confidence is deteriorating, leaving markets increasingly sensitive to governance and policy credibility.

- Growth is being driven by capital spending and productivity rather than labor or consumer leverage, producing a job-light expansion.

- Inflation is cooling toward trend, but uneven upstream pressures and energy volatility are keeping term premia elevated.

- Kevin Warsh’s nomination refocuses markets on credibility and balance-sheet policy rather than the near-term rate path.

- Corporate behavior has shifted toward paying for certainty as policy, geopolitical, and duration risks crowd the outlook.

The Data Beneath the Noise

This past week reinforced a theme that has been building quietly but persistently. The U.S. economy continues to expand at a healthy pace, yet confidence is eroding. Markets are increasingly pricing governance risk, policy credibility, and term-premium dynamics rather than cyclical deterioration.

From a cyclical standpoint the economy is looking a little stronger, as data continues to surprise to the upside. Business investment remains a clear bright spot, particularly in equipment tied to artificial intelligence, automation, energy infrastructure, and advanced manufacturing. Core capital goods orders rose again in November, reinforcing that firms are still deploying capital even as surveys signal caution.

Most of the other data released in this past week’s holiday shortened calendar reinforced a tension that has been building for months: the economy continues to expand, even as markets behave as though the margin for error has narrowed.

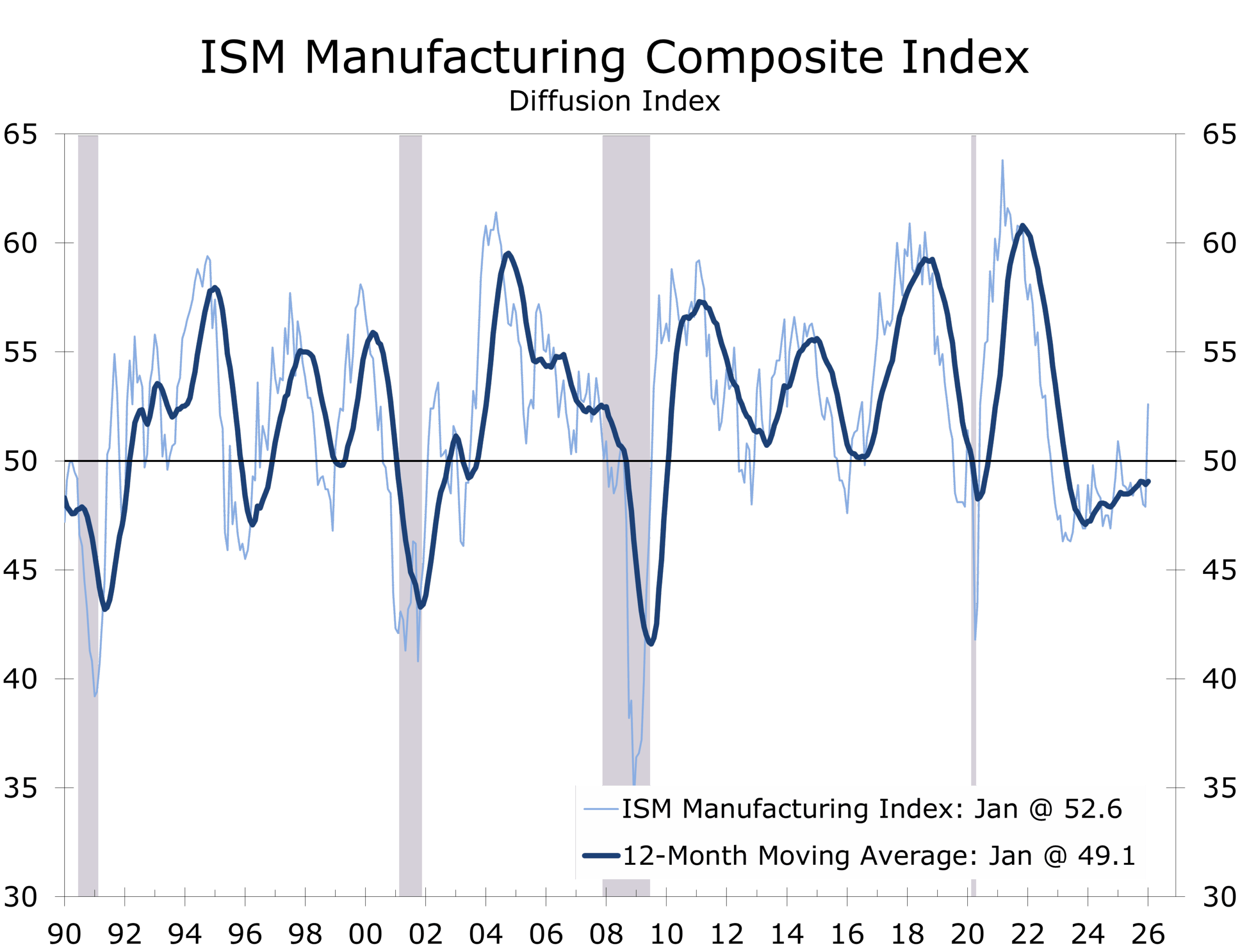

Manufacturing Momentum Breaks Through the Noise

Today’s ISM manufacturing report delivered a decisive upside surprise and reinforced the resilience of the production side of the economy. The headline index rose to 52.6 in January, returning to expansionary territory for the first time in a year. The improvement was broad-based. New orders surged, production accelerated, and the employment component firmed, though it remains consistent with a job-light expansion rather than a hiring boom.

Manufacturing has re-entered expansion. Hiring has not. That gap defines this phase of the cycle.

The stronger ISM report provides confirmation of a capital-driven growth model in which firms expand output through investment, automation, and productivity rather than payrolls. Supplier delivery times lengthened modestly, pointing to firmer demand and emerging capacity constraints. Price pressures edged higher but remain well below prior-cycle peaks. Tariff uncertainty featured prominently in survey commentary, underscoring how policy signaling, rather than demand continues to shape sentiment.

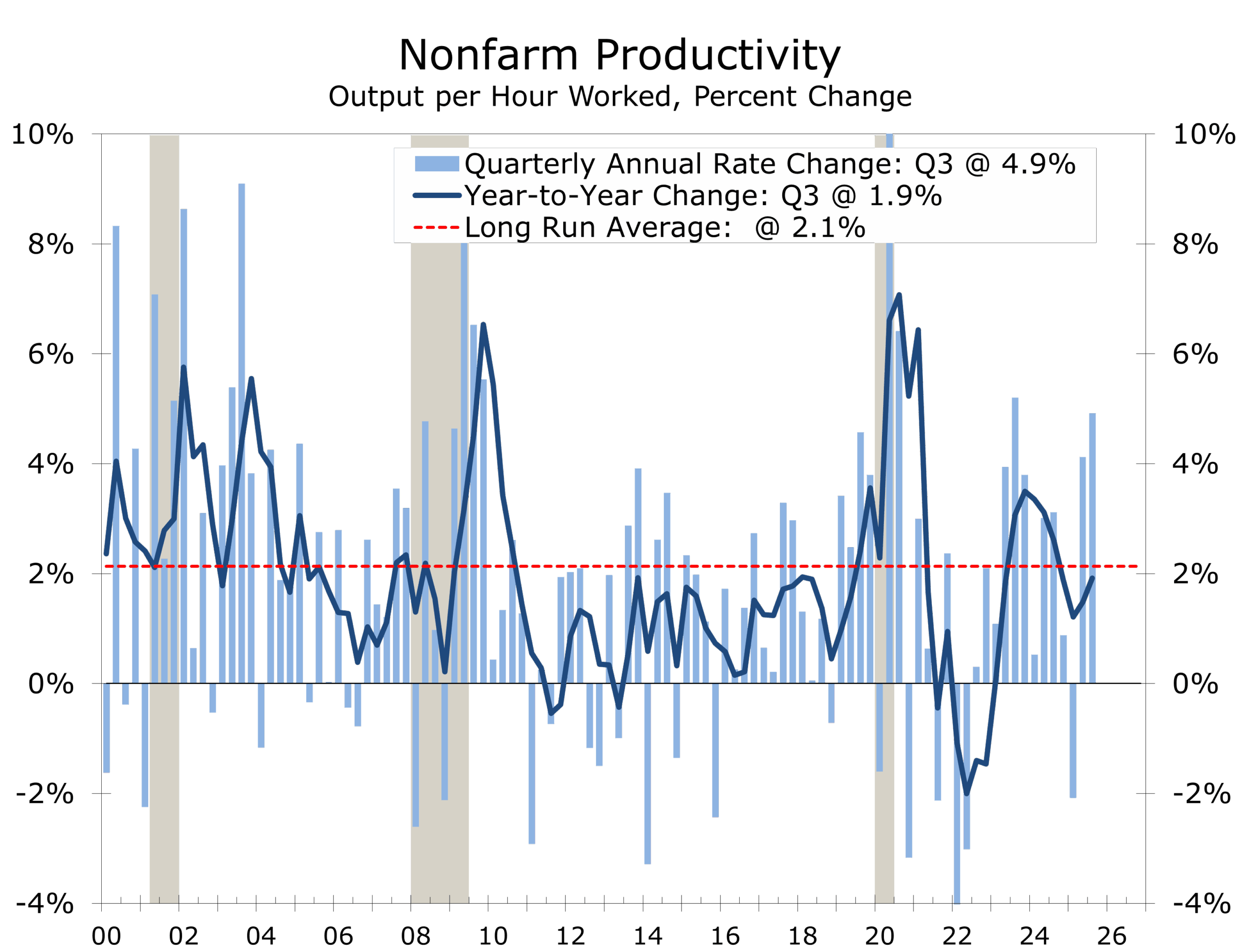

Productivity as the Critical Offset

Productivity growth remains the central stabilizer. Third-quarter productivity held at a strong pace, with gains broad-based rather than confined to technology. That breadth matters. It raises the economy’s effective speed limit and allows growth to run faster without reigniting inflation, even as hiring remains subdued.

The result is a defining feature of this cycle: a job-light expansion. Firms are producing more with fewer incremental workers. Layoffs remain low, hiring remains historically soft, and labor leverage continues to erode. The firewall against recession remains intact, but it is thinner than in past cycles.

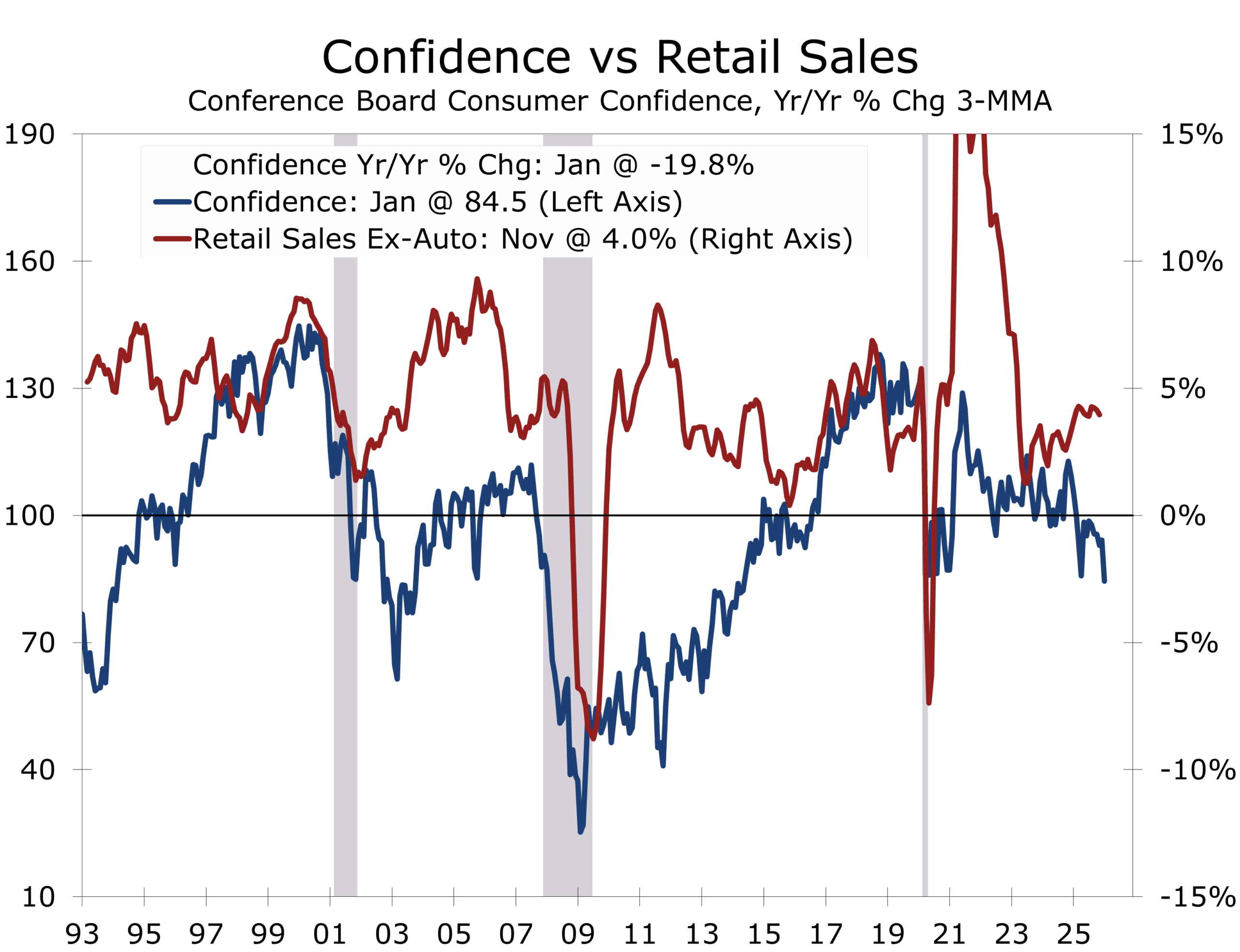

The Consumer Split Widens

The sharpest divergence last week came from the consumer. Confidence fell sharply at the start of the year, reaching its lowest level in more than a decade, driven by concerns about prices, tariffs, and job availability. Yet spending continues to hold up.

Consumer spending is holding up. Confidence is not, as worries about the labor market mount.

The explanation lies in a bifurcated consumer. Higher-income, asset-rich households continue to drive discretionary spending, supported by equity gains and accumulated wealth. Lower- and middle-income households remain constrained by the level of prices, not the rate of inflation. Lower inflation helps, but it does not reset affordability.

Piedmont Perspective: Identifying Productivity Gains

Kevin Warsh will step into the Fed chair with a mandate to restore credibility. Markets have translated that mandate into balance-sheet discipline and firmer control over term premia. His immediate challenge, however, will be to recognize productivity gains before they appear in the official data.

Today’s capital-driven expansion is likely to see productivity move past its long-run average.

In the 1990s, productivity surfaced first in margins and capital spending, not statistics. The same pattern is emerging today. Output remains firm even as employment growth slows. Credibility is not preserved by rigidity. It is preserved by recognizing change as it occurs and before it is reported.

A longer standalone version of this Piedmont Perspective is available on our website.

Markets Are Paying for Certainty

Across asset classes, behavior is shifting. Corporate treasurers are locking in funding. Investors are paying for insurance. Energy-intensive firms are prioritizing reliability over price.

Energy markets delivered a parallel signal. Winter weather disruptions stressed grids and pushed wholesale power prices sharply higher in some regions. Energy risk now includes availability and resilience, not just price

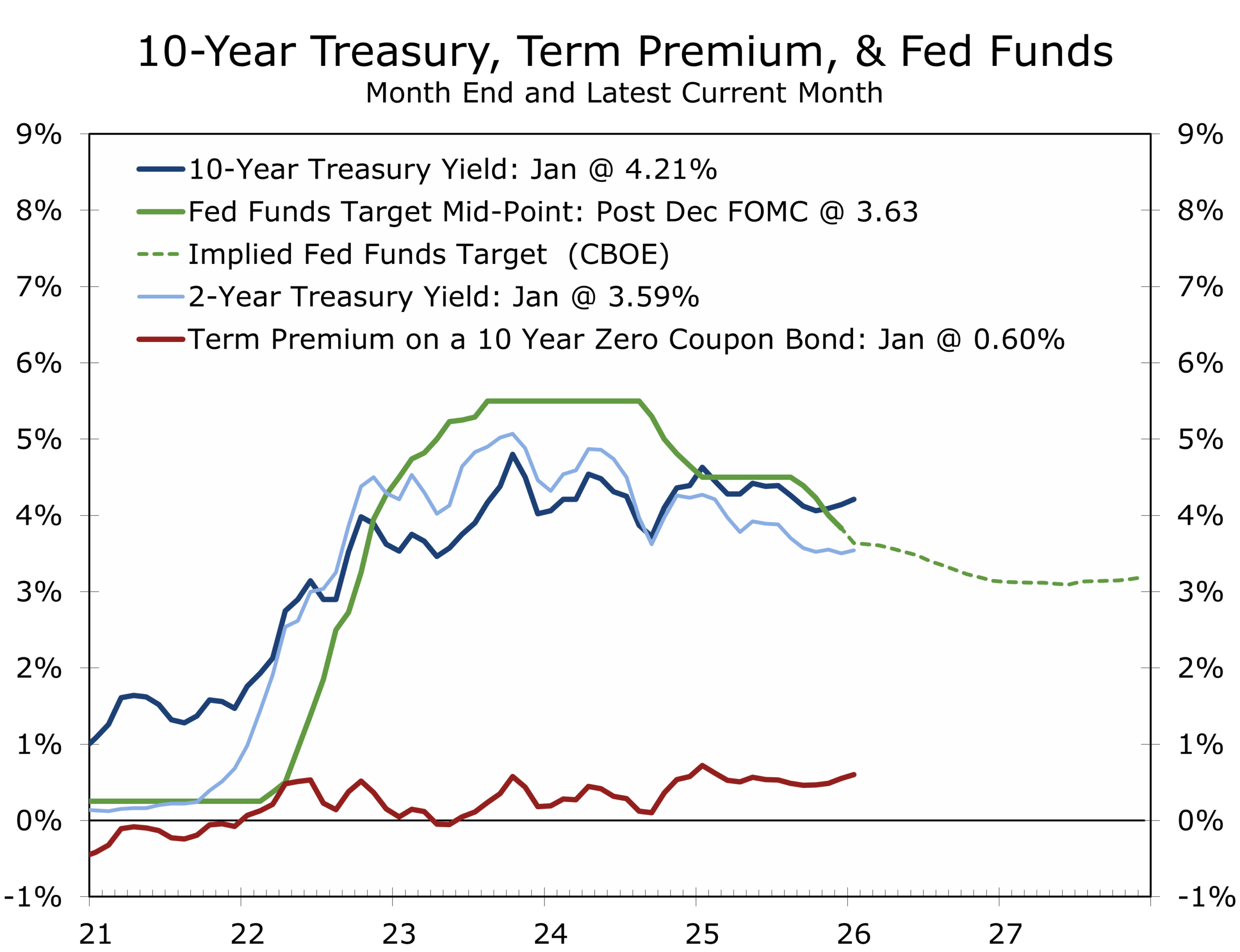

Warsh: Credibility First

President Trump’s nomination of Kevin Warsh as the next Federal Reserve Chair resolved one uncertainty while sharpening the market’s focus on credibility and balance-sheet policy. Warsh’s hawkish reputation is well earned but narrowly targeted.

Warsh is hawkish on the balance sheet and inflation, but less so when it comes to growth.

Warsh has consistently drawn a line between interest-rate policy and balance-sheet expansion. His framework allows rates to support real activity as inflation cools while restraining balance-sheet tools that distort capital allocation and weaken institutional credibility.

Inflation continues to decelerate towards trend, but upstream pressures remain uneven, particularly in services and energy-linked categories. Credibility, not complacency, now sets the price of capital.

For treasury teams, this matters. Long Treasuries remain liquid and credit-safe, but they are no longer immune to flow-driven volatility.

Expectations for an aggressive balance-sheet unwind should be tempered. Structural support for an ample-reserves framework remains strong, even as balance-sheet discipline tightens at the margin.

A Crowded Geopolitical Map, With Iran Back in Focus

Geopolitics continue to act as a volatility amplifier rather than a growth shock. Iran stands out as the most immediate source of asymmetric risk, with heightened rhetoric around proxy activity, shipping security, and sanctions enforcement.

The transmission channel is familiar. Energy markets react first, followed by shipping and defense costs, with inflation expectations moving at the margin.

Relations with Canada have also grown more contentious, adding friction to trade, energy flows, and cross-border investment. These are not growth threats, but they add uncertainty in a market already sensitive to policy signaling.

Parting Thoughts

This was not a week about cycles. It was a week about confidence. The data describe an economy that is expanding and cooling gradually, not one on the brink of recession. Markets, however, are pricing governance risk, credibility, and global term-premium dynamics with increasing urgency.

The most important signal did not come from a data release. It came from behavior.

Quiet Data, Missing Payrolls, Loud Signals

The coming week is light on top-tier economic releases but heavy on signaling risk. ISM services, jobless claims, and consumer credit should confirm ongoing expansion rather than alter the outlook.

Notably, the Bureau of Labor Statistics has announced that the January employment report will not be released this week due to the government shutdown. The January data are believed to be complete and will contain revisions dating back to early 2024 and will provide a better read on the current pace of job growth The absence of payrolls data increases the market’s reliance on surveys, high-frequency indicators, and Fed communication.

In an environment where confidence is fragile and positioning is cautious, missing data tends to amplify noise rather than dampen it. For corporate treasurers and CFOs, the message remains clear: this is a market that rewards preparedness, not precise timing.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 2, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000