Highlights of the Week

- The Fed cut the funds rate by 25 bps to 3.75–4.00%, but Powell’s warning that “a December rate cut is not a foregone conclusion” caught markets off guard.

- Front-end yields rose 10–12 bps as traders recalibrated expectations; the dollar firmed and equities ended mixed.

- The latest CPI print continues to germinate across markets and policy circles, with shelter costs and core inflation moderating.

- Consumer confidence held steady at 94.6, showing households are adapting rather than retreating.

- Labor markets continue to cool: initial claims hover near 219,000, while ADP’s new weekly series shows modest but positive hiring.

- Across the Piedmont and the broader South, AI infrastructure, aerospace, shipbuilding, pharmaceuticals and energy investment keep regional growth above trend.

- In Texas, factory activity expanded modestly in October while service and retail sectors contracted further, highlighting the uneven nature of the slowdown.

- Globally, Trump’s Southeast Asia tour and the Busan APEC summit produced a fragile U.S.–China truce — a pause in tariff and rare-earth escalation, not a durable peace — while global central banks signal policy stability.

U.S. ECONOMY & FINANCIAL MARKETS

The Federal Reserve’s October 29 decision marked a shift from momentum to management. Policymakers trimmed the funds rate by 25 bps to 3.75–4.00% and emphasized that policy “is not on a preset course,” reflecting both the committee’s divisions and the information gaps created by the continuing government shutdown.

A measured cut, anchored yields, and a reminder: policy is not on a preset course.

The shutdown itself, now the longest on record, has had limited near-term market impact. Senate leaders have rejected calls to repeal the filibuster rule, virtually guaranteeing its survival and ensuring that fiscal legislation will remain constrained. While the shutdown is likely to end before Thanksgiving, its political fallout has kept Washington’s focus narrow, limiting fiscal risk in the near term.

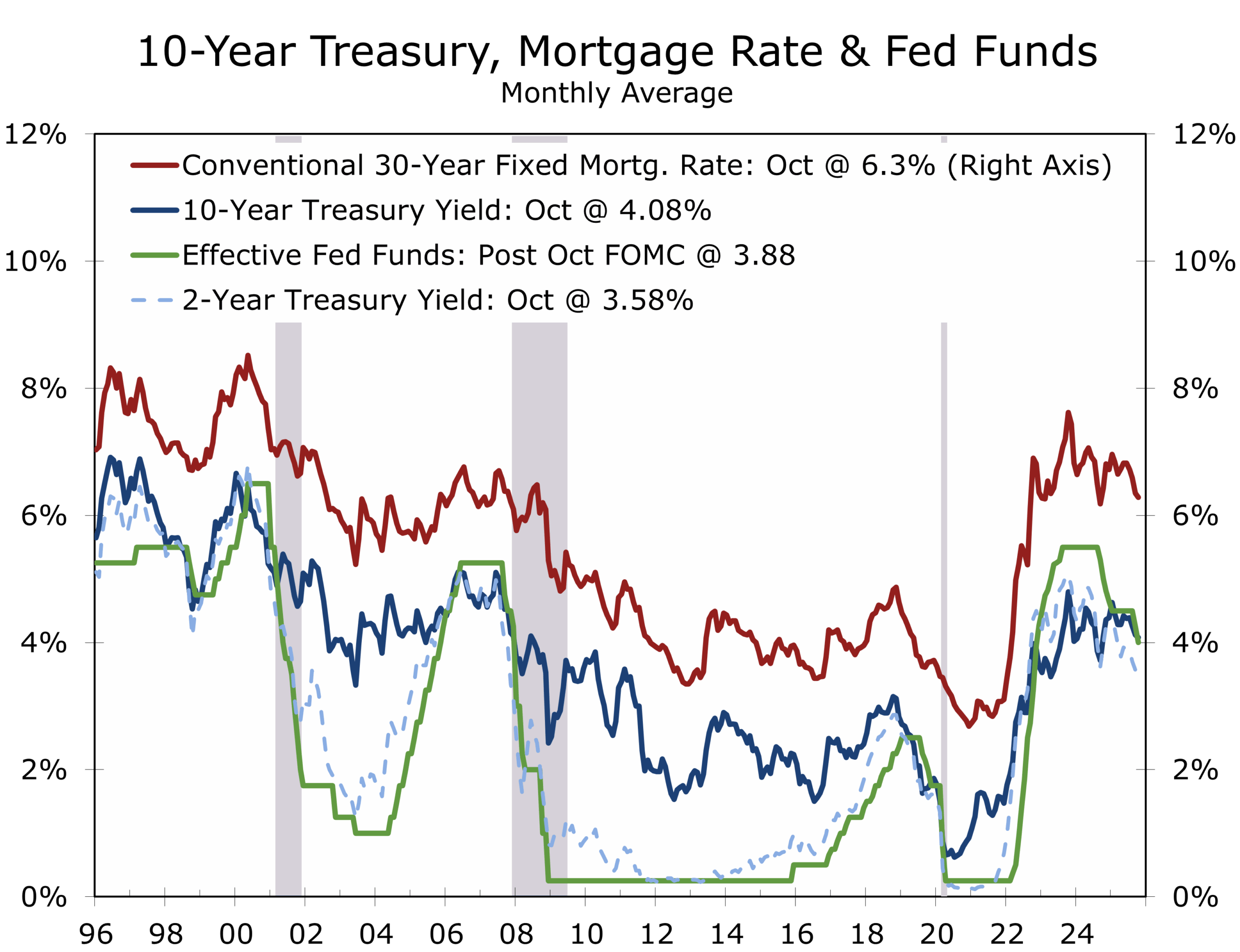

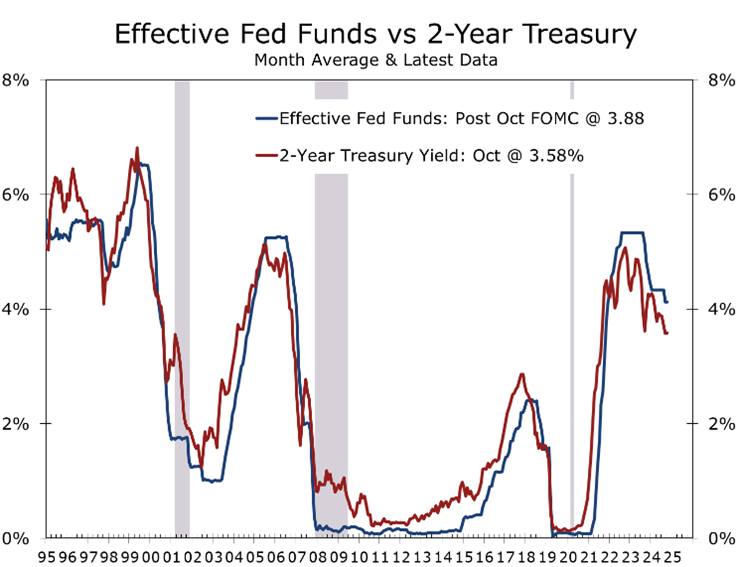

Markets reacted swiftly: the two-year Treasury yield rose to about 3.6%, the ten-year moved back above 4% and ended the week near 4.10%. The S&P 500 gained roughly 0.5%, supported by solid Q3 earnings and increased capex guidance from the major AI and cloud “hyperscalers.”.

The latest CPI print continues to germinate across markets and policy circles. Core CPI rose 0.2% in September, with shelter’s contribution the smallest since 2021. While some worry the softening may be temporary, private-sector data show rent concessions rising, especially in the South. Headline CPI and core PCE are on pace to finish the year near 3% and to ease toward 2½% by late 2025, giving the Fed room to cut gradually without re-igniting demand.

Consumers remain resilient. The Conference Board confidence index held at 94.6 despite the shutdown, and the “jobs plentiful minus jobs hard to get” spread stabilized — a sign of adaptation, not collapse.

Labor data confirm that cooling, not collapse, is underway. Jobless claims hover just above 219 k, the Chicago Fed’s real-time unemployment measure sits near 4.35%, and ADP’s weekly series shows modest private-sector gains — all consistent with a soft landing.

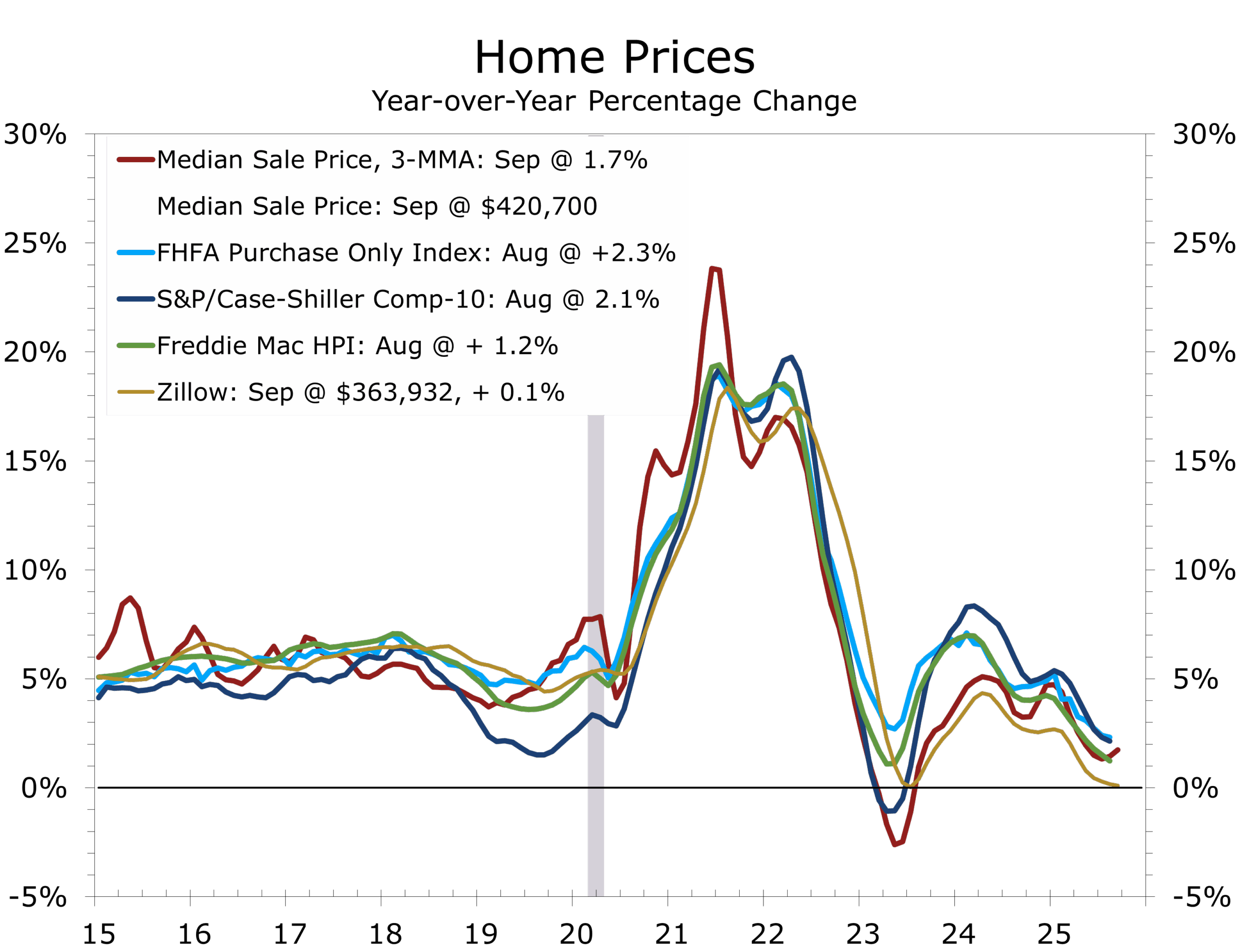

Housing is showing tentative signs of revival. The Case-Shiller index rose 0.2% in August — its first monthly gain since winter — as inventories normalized and sellers re-entered the market. Price growth has slowed to 1½% y/y but appears stable through year-end.

Dallas Fed surveys show a mixed regional picture — steady factory output but service and retail weakness. Manufacturing’s production index held at 5.2 with new orders (–1.7) and capacity utilization (–1.1) softening. Business sentiment remained slightly negative (–5.0) while employment rose marginally (2.0) and hours worked fell (–5.5). Services contracted again (revenue –6.4, employment –5.8), and retail sales fell sharply (–23.5). Overall, industrial and capital-intensive sectors remain firm while consumer-facing industries absorb the slowdown.

The Piedmont Crescent

The Piedmont Crescent — stretching from Birmingham and northern Alabama through Atlanta and up through the Carolinas and Virginia to the D.C. area — continues to outperform the nation.

Atlanta’s logistics and technology corridors are expanding, Charlotte’s finance and manufacturing bases remain steady, and Raleigh–Durham’s research and biotech clusters attract sustained venture capital. Greensboro and the Triad are emerging as electric-vehicle and aerospace hubs, while Richmond and Northern Virginia benefit from defense and data-infrastructure investment.

Migration, population growth, and corporate relocations keep housing active even as national demand cools. Infrastructure upgrades and energy-grid projects continue to anchor industrial expansion.

The Broader South

The South remains the nation’s growth engine. Texas leads in energy and semiconductors, Florida’s tourism and construction expand despite affordability strains, and Tennessee and Alabama capitalize on EV and aerospace investment.

South Carolina’s ports and manufacturing hubs run near capacity, Louisiana and Mississippi advance grid-modernization and petrochemical projects, and shipbuilding along the Gulf Coast — from Mobile to Pascagoula and into New Orleans — is gaining momentum on Navy, Coast Guard, and commercial orders. Together, these trends keep Southern output well above national averages even as the broader economy slows.

Outside the Region

The Midwest’s industrial renaissance continues through chip fabrication and EV supply-chains. The West Coast is stabilizing after a year of tech layoffs as AI capex revives growth from Seattle to San Jose.

Major markets in the Northeast received a boost this year from the return to the office, which also boosted retail trade and the hospitality sector. Financial services have also had a strong year. Divergences across regions are widening, however, a classic late-cycle phenomenon.

Outside the Country — The APEC and ASEAN Circuit

President Trump’s Southeast Asia trip dominated the week’s geopolitical landscape. Visits to Thailand, Malaysia, Cambodia, and Vietnam produced agreements on critical-minerals cooperation and supply-chain diversification.

At the APEC summit in Busan, the U.S. and China announced a one-year truce without teeth — the U.S. cut tariffs tied to fentanyl from 20% to 10% in exchange for Beijing committing to reduce precursor shipments and crack down on the fentanyl trade in general. In addition, China will resume soybean and energy purchases, and suspend rare-earth export curbs for a year. Tariffs on most other goods remain high, and no progress was made on Taiwan or Russia ties.

A fragile détente steadies markets but leaves rivalries intact.

The U.S.–South Korea defense accord was another notable development, allowing Seoul to purchase or jointly develop a nuclear-powered submarine using U.S. technology to be built in a U.S. yard with Korean investment — a move anchoring the peninsula more firmly within the Indo-Pacific security framework. An added plus: Korean investment might also help bolster the U.S. shipbuilding industry.

Europe appears to be settling into a soft landing. The ECB kept rates at 2% for a third meeting, while the Bank of Canada also paused after its cut. The Bank of Japan remains on track to raise to 0.75% by year-end, though Prime Minister Takaichi may delay if data soften. Global policy tone is one of hawkish stability — fine-tuning after a year of adjustment.

Risk tone brightened as Washington and Beijing reached a provisional framework pausing threatened 100% tariffs and rare-earths export curbs—pending Trump–Xi leader sign-off later this week. President Trump said he expects to “come away with a deal,” with China delaying export bans and boosting U.S. soybean purchases—tactically easing AI supply-chain stress and trimming term-premium risk.

Oil prices have stabilized near the low-$60s for WTI and mid-$60s for Brent as higher U.S. output offsets Middle-East risk and sluggish European demand. Argentina’s Javier Milei scored a decisive election victory that reinvigorated market-friendly reform momentum across Latin America. Globally, the backdrop remains one of managed fragility — diplomacy buying time for markets without resolving underlying rivalries.

Policy and Market Wrap-up

Regional Fed surveys paint a mixed picture: Richmond at –2, Dallas and Kansas City showing softer orders, and Atlanta’s business-inflation expectations slipping to 2.5%. Markets now price one more 25-bp cut by January, consistent with a soft-landing baseline.

Private-credit markets are also entering a more discerning phase as the “ghosts of 2020–2021 vintages” resurface. Select distress is emerging in legacy loan books, while AI-linked direct-lending remains active. Alternatives investors are turning more defensive — upgrading infrastructure and ports, re-entering senior housing, and keeping hedge-fund allocations tilted toward global macro.

Credit spreads remain tight, volatility subdued, and equity leadership concentrated in capital-intensive sectors — AI, energy, aerospace, and defense. Next week’s ISM and NFIB surveys will test whether late-year momentum can carry into 2026.

Bottom Line

The U.S. economy continues to evolve rather than erode. Inflation is cooling, labor markets are rebalancing, and policy is shifting from restraint to fine-tuning. Across the Piedmont and the South, industrial investment and migration remain core drivers. Abroad, diplomacy has bought calm but not certainty. Another showdown awaits.

Markets Exhale Amid Persistent Rivalry

The headlines out of Busan were celebratory, but the subtext was cautionary. The temporary U.S.–China thaw — the cut in fentanyl-related tariffs to 10% in exchange for Beijing reducing precursor shipments, the resumption of soybean trade, and a one-year suspension of rare-earth export restrictions — amounts to a cease-fire, not reconciliation.

The U.S. and China have stepped back from escalation, not rivalry.

Behind the smiles and handshakes lies a strategic recalibration rather than surrender. Both nations are buying time: Washington to shore up domestic supply chains through ASEAN partnerships, Beijing to manage capital flight and maintain export leverage. The détente narrows downside risk for AI-driven capex and commodity markets yet underscores how interdependence remains both weapon and weakness.

History suggests that pauses like this often precede a new phase of competition. The world’s two largest economies have stepped back from escalation but not from rivalry. For now, markets can exhale — but they would be wise not to forget to keep their running shoes on.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 2, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000