Highlights of the Week

- Growth signals remain bifurcated. Manufacturing continues to contract, services have re-accelerated, and GDP tracking models still point to a very strong fourth quarter. The economy is advancing on parallel rails, not in a straight line.

- The labor market is cooling without cracking. Hiring has slowed materially, wage growth is easing, and productivity is doing more of the work. This is a low-hire, low-fire environment, not a recessionary one.

- Financial conditions remain supportive. Credit markets reopened forcefully, issuance surged, and risk assets are behaving as though policy is restrictive only at the margin.

- Policy risk has shifted from inflation to institutions. Political pressure on the Federal Reserve introduces a new variable that could extend policy restraint even if inflation continues to improve.

- Geopolitics has moved from background noise to event risk, but markets are still treating it as a premium rather than a macro shock.

U.S. macro: mixed signals, durable momentum

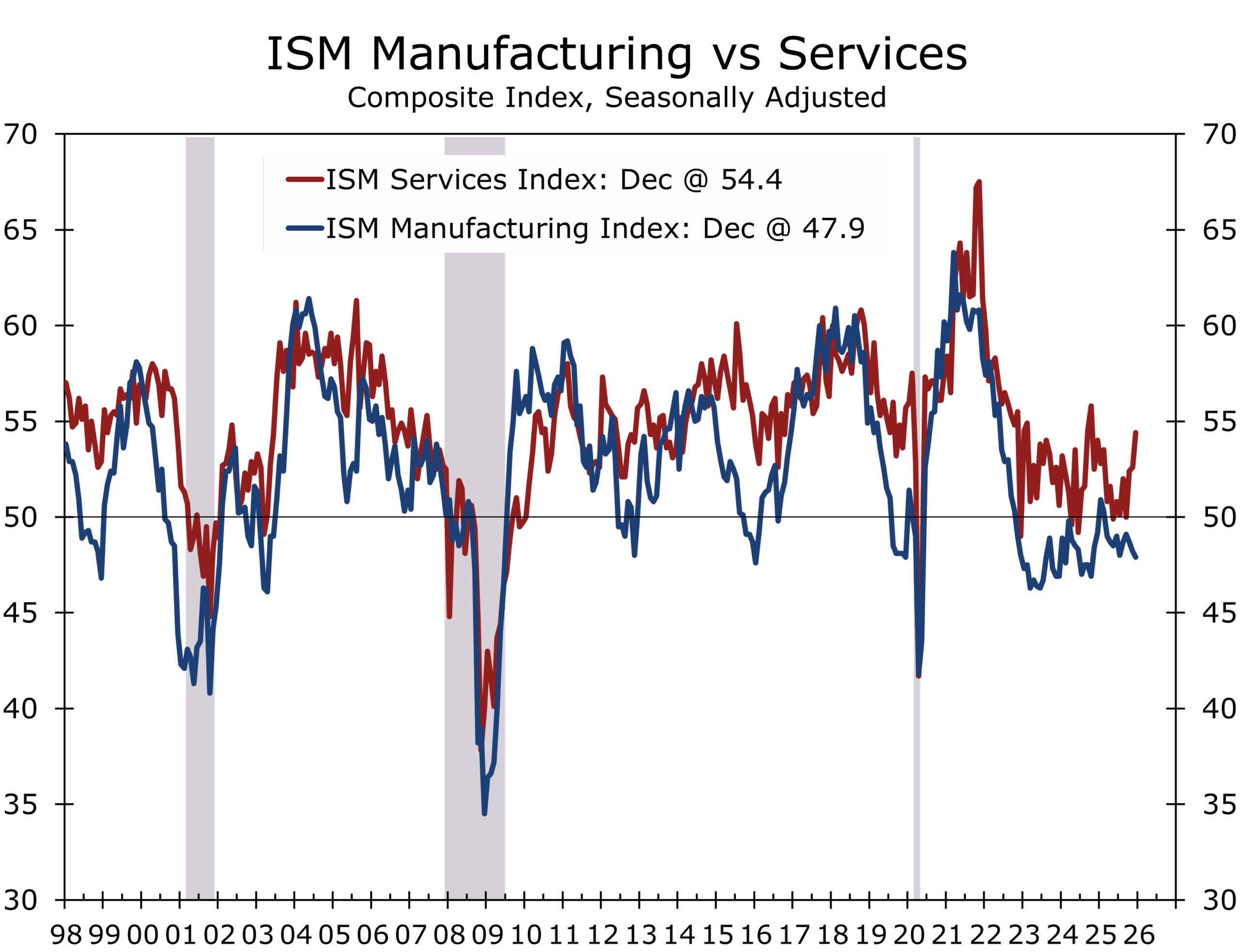

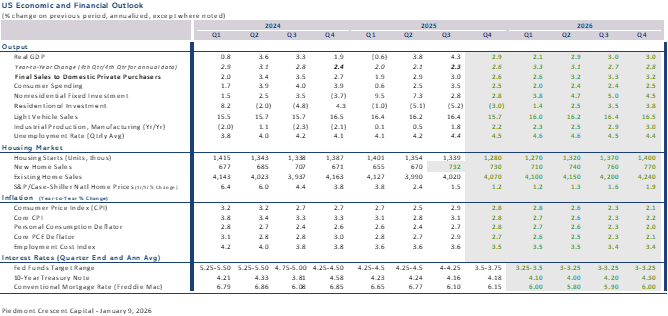

Manufacturing ended 2025 on a softer note. ISM Manufacturing fell to 47.9 in December, pushing further into contraction and underscoring how sensitive the sector remains to policy uncertainty and uneven global demand. But the weakness is not uniform. Manufacturing is increasingly bifurcated.

Output of consumer goods rose just 1.4% year over year, while output of business equipment surged 12.5%. That strength is narrowly concentrated in capital-intensive segments—aerospace and miscellaneous transportation equipment, including shipbuilding, where output jumped 25.2%, and semiconductors and related components, up 16.5%. Even within nondurables, pharmaceutical and medicine production stands out, rising roughly 6–7% over the past year.

The signal from industrial production is clear: this is not a consumer-led manufacturing cycle. It is a capital-, defense-, technology-, and innovation-driven expansion operating alongside a still-soft factory backdrop. Reshoring will become more evident during 2026, with pharmaceuticals and steel likely to be two of the earliest beneficiaries.

Manufacturing is contracting overall but expanding in capital-intensive segments.

Services, meanwhile, continue to do the heavy lifting. The Institute for Supply Management Services index climbed to 54.4 in December, signaling sustained momentum in business activity, new orders, and hiring. This is now the economy’s center of gravity. Large, scalable service platforms benefit from recurring demand, pricing power, and operating leverage. Unlike goods production, services are less constrained by inventories and more adaptable to shifts in labor and capital mix.

GDPNow, trade, and the arithmetic of growth

Atlanta Fed GDPNow remains eye-catching. As of January 9, the model was tracking Q4 real GDP growth above 5%, even after a modest pullback. The strength is not coming from housing or consumer excess. It is coming from trade arithmetic and capital spending.

October trade data showed a sharp narrowing of the trade deficit, driven largely by tariff-related timing effects. Pharmaceutical imports reversed abruptly after September front-loading, while capital goods imports surged, reflecting sustained spending on AI infrastructure, data centers, and high-tech equipment. Exports were also boosted by an unusual spike in gold shipments, which flatters the headline trade balance but contributes little to real GDP.

GDPNow captures the arithmetic of the moment; forecasting requires judgment about what lasts.

We adjusted our Q4 real GDP forecast modestly higher following the trade release, but not nearly to the levels implied by GDPNow. The model is deliberately mechanical. When net exports swing sharply and equipment spending remains firm, it upgrades growth aggressively, even if some of that strength is likely to reverse as gold flows normalize and import-timing effects fade. Our 2026 growth forecast remains above consensus, with risks currently skewed to the upside.

Labor market: slow lane, not pile-up

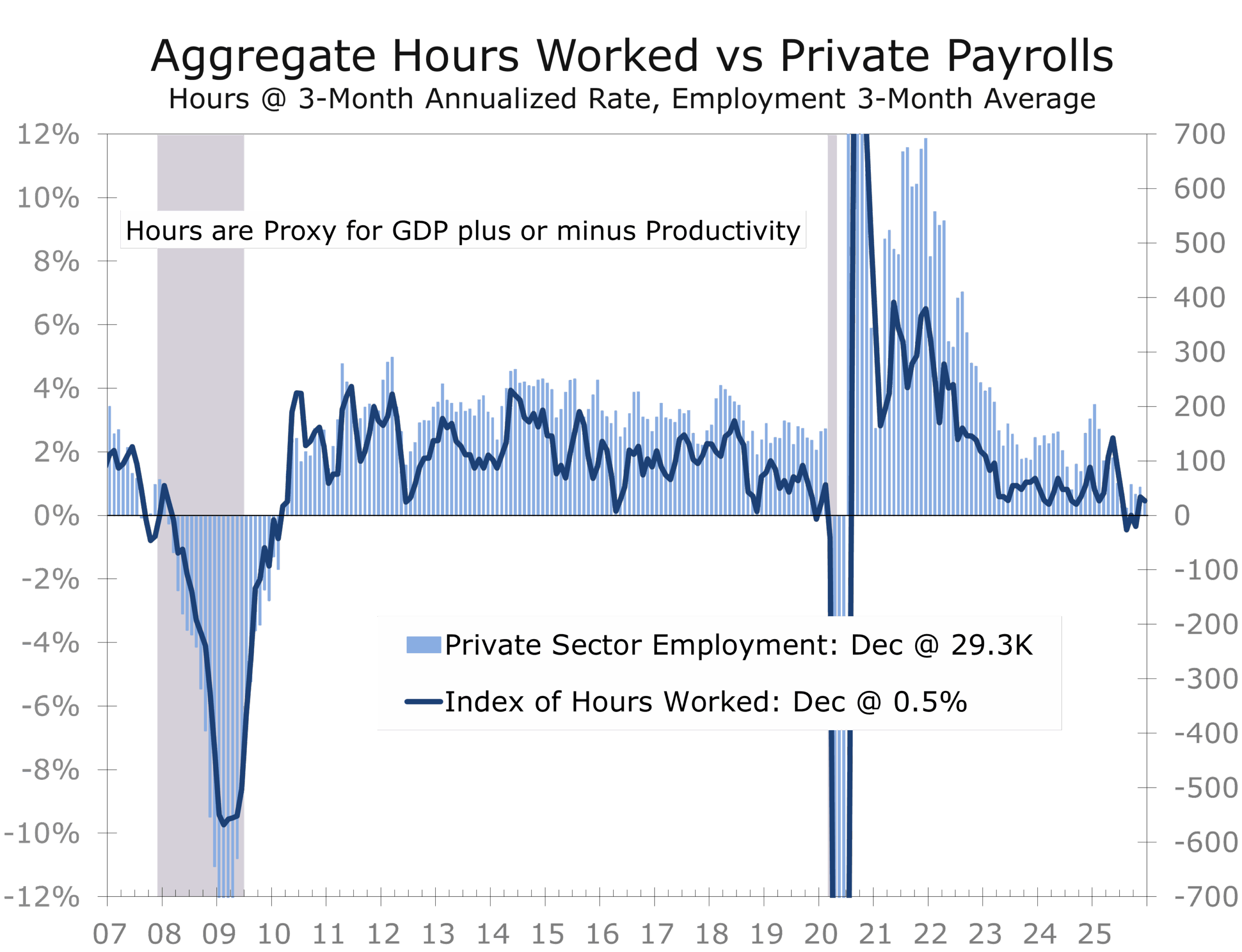

The December Employment Situation capped a notably slower hiring year. Payroll gains averaged roughly 49,000 per month in 2025, a sharp deceleration from prior years, with the unemployment rate ending the year at 4.4%. Wage growth cooled but did not collapse, with average hourly earnings running in the high-3% year-over-year range—firm enough to support consumer spending while remaining consistent with a disinflationary labor backdrop.

Hiring remains narrowly concentrated, with many cyclically sensitive industries showing little net change. Layoffs remain historically low, however, reinforcing the view that firms are reluctant to shed labor. Adjustment continues to occur primarily through hours rather than headcount, with aggregate hours worked declining modestly and underemployment edging higher at the margin. Productivity is doing more of the work. After a strong third quarter, nonfarm productivity remains up roughly 2% year over year, underscoring a meaningful improvement in output per worker even as hiring slows.

Slower hiring reflects higher productivity and tighter labor supply, not labor-market stress.

Quarterly productivity readings are inherently noisy. The more reliable signal comes from year-over-year trends and multi-year averages, which point to underlying productivity growth closer to 2%, with scope to rise toward 2½%–3% as capital deepening, AI adoption, and the buildout of digital infrastructure shift a larger share of growth toward capital rather than labor. At the same time, businesses are pruning lower-return activities, retaining higher-quality workers, and becoming more selective in hiring; reinforcing the productivity rebound.

This increasingly resembles a low-hire, low-fire equilibrium. Employers are cautious about adding workers but reluctant to cut existing staff. The implication is straightforward: labor costs are becoming more predictable, not more volatile, reducing downside risk to margins even as top-line growth moderates.

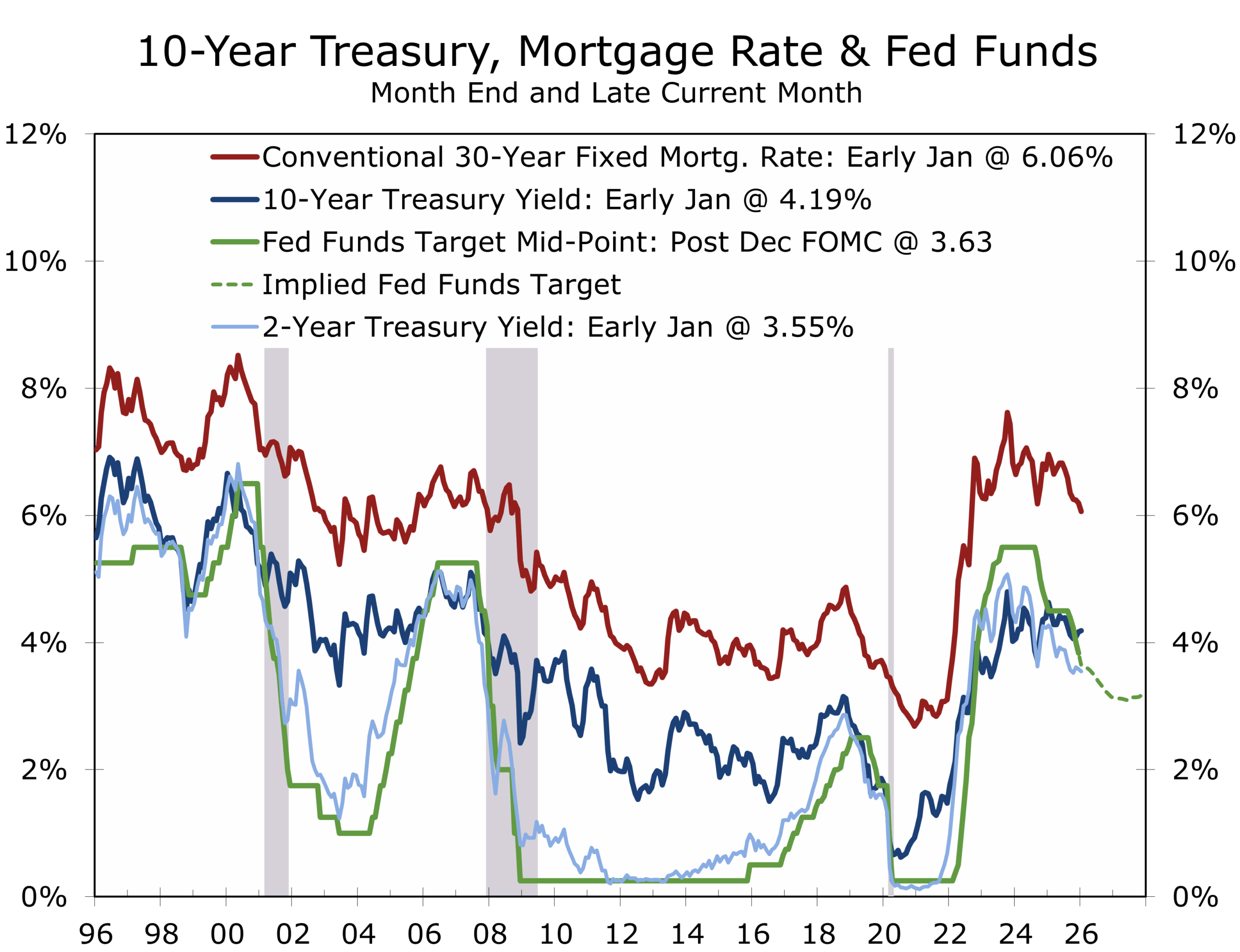

Rates, financial conditions, and policy risk

Markets have shifted toward a patient Fed narrative. Rate cuts remain priced for later in 2026 if inflation cooperates, but near-term urgency has faded. Financial conditions reinforce that view. Credit spreads remain contained, issuance has surged, and risk assets are not behaving as though policy is overly restrictive.

A new variable entered the equation this week: direct political pressure on Federal Reserve leadership. The Administration publicly accused Chair Powell of misconduct tied to his prior regulatory decisions and indicated support for potential legal action, an extraordinary step that reframes the policy outlook—not through inflation or employment, but through institutional credibility.

Central Bank independence is a policy tool. Undermining it raises the cost of easing.

Markets have largely discounted immediate consequences, assuming the Fed’s reaction function remains intact. That assumption appears reasonable. Inflation expectations remain well anchored, rate pricing has barely moved, and financial conditions show no signs of credibility shock. Policy is still being set inside the FOMC, not outside it.

History, however, offers an important guide. Episodes of political pressure on central banks rarely result in faster accommodation. More often, they produce the opposite outcome. When independence is questioned, policymakers tend to lean more heavily on process, caution, and institutional legitimacy. Powell’s response fits that pattern. His remarks were institutional, procedural, and deliberately defiant. He made clear that the Federal Reserve’s mandate, framework, and decision-making process remain unchanged. That message was not accidental. It was designed to reinforce credibility at a moment when it was being tested.

Threats to Fed independence rarely hasten easing. They usually reinforce caution.

The irony is that the macro backdrop would otherwise support patience. Growth remains solid, labor markets are cooling without distress, and funding conditions are accommodative. Political pressure risks turning what could have been a benign pause into a longer one, even if inflation continues to drift lower.

This episode is best viewed as a test of norms rather than a transfer of authority. The Federal Reserve’s independence ultimately rests not on rhetoric or statute alone, but on credibility and the willingness of its leadership to hold the line. On that front, Powell has been clear.

Equity and credit: funding windows reopened

Investment-grade credit markets opened the year with force. Roughly $95 billion in U.S. corporate bond issuance marked the busiest first full week since early 2020. This is classic January front-loading, amplified by strong demand and a desire to lock in funding early.

That behavior is inconsistent with a narrative of tightening liquidity. It suggests that access to capital remains available, terms are competitive, and balance-sheet strategies are being executed from a position of relative strength.

Equities have reflected a similar message: growth intact, wage pressure easing, and margins supported by productivity rather than labor expansion.

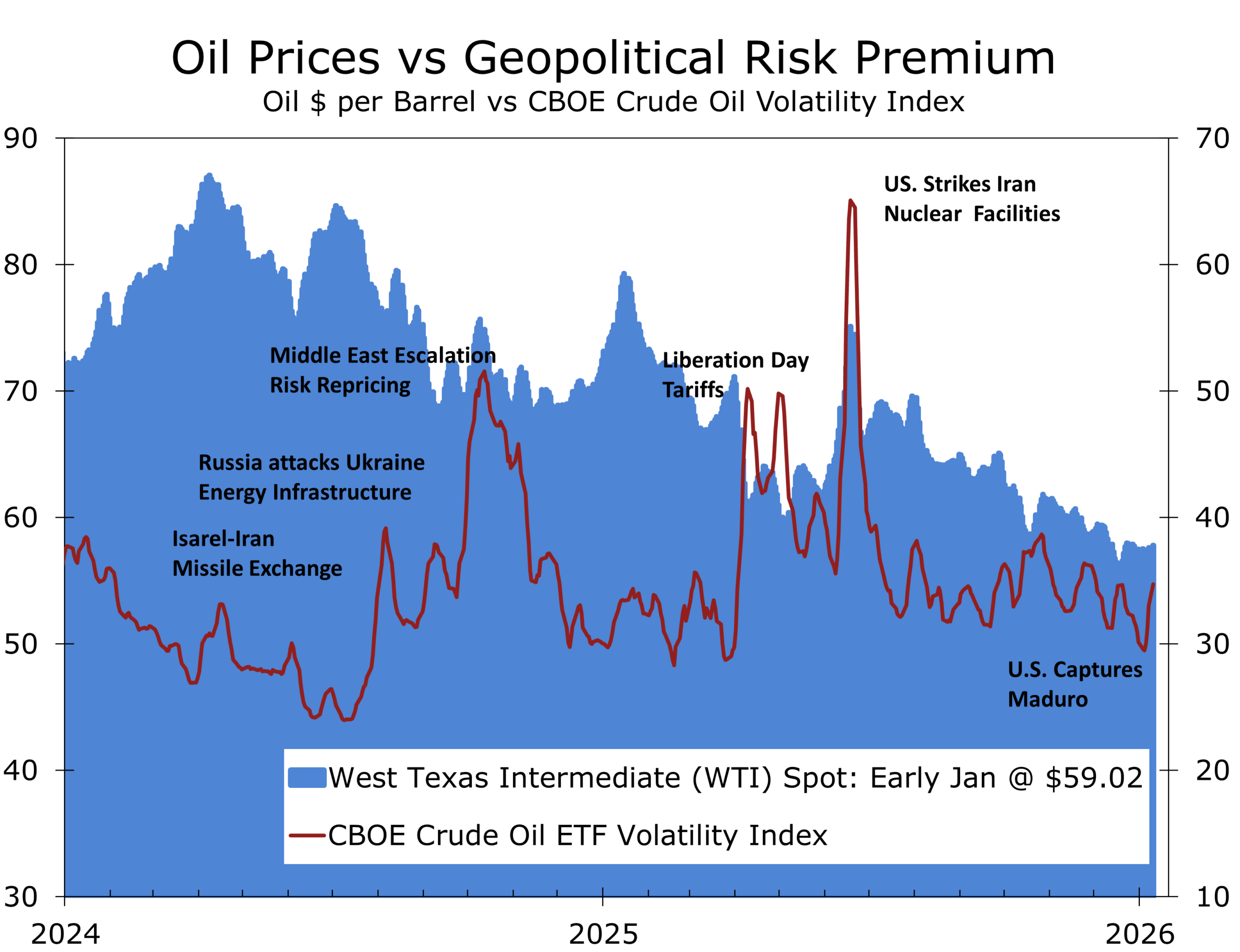

Geopolitics: risk premium, not shock yet

Venezuela was the headline shock. The U.S.-led capture of Nicolás Maduro sent a clear signal about hemispheric control, inviting comparisons to the 1989 intervention in Panama. Markets have so far treated the episode as a geopolitical risk premium rather than a systemic macro event, with oil prices and broader risk assets largely contained.

Russia intensified strikes on Ukrainian infrastructure during extreme cold, raising humanitarian and energy-system risks. Iran escalated rhetoric toward Israel and the United States, keeping the Middle East risk envelope wide, while renewed movement around Aleppo underscored Syria’s continued volatility. These developments reinforce a backdrop of persistent geopolitical tension without triggering outright disruption.

Geopolitical risk is being priced through volatility and term premia.

The timing matters. Geopolitical assertiveness abroad is coinciding with institutional tension at home, a combination markets typically price with a lag. After a strong start to the year, this raises the likelihood of intermittent volatility, making early-year issuance and proactive funding decisions look increasingly well timed.

Theme: geopolitics, pricing power, and term premia

The common thread across these developments is not immediate disruption but option value. Supply chains remain intact, yet redundancy, inventory buffers, and routing insurance continue to carry a cost. That dynamic keeps a floor under goods inflation even as headline pressures ease. In fixed income, the transmission runs less through near-term rate expectations and more through term premia, as investors demand compensation for geopolitical uncertainty, policy risk, and elevated fiscal supply. The result is a curve that resists flattening and volatility that reappears episodically rather than persistently.

The week ahead: data that can move the narrative

This week’s calendar is dense enough to stress-test the emerging patient-Fed consensus.

Tuesday: December CPI and the NFIB Small Business Optimism Survey. Inflation remains the gatekeeper, particularly core services and shelter. We expect a better-than-feared print, helped by softer grocery prices and easing rent pressure. NFIB sentiment will be closely watched for signs of stabilization.

Wednesday: Retail sales and existing home sales. Control-group sales will shape Q4 GDP tracking and early-year consumer momentum.

Thursday: The Empire State and Philadelphia Fed manufacturing surveys will provide early insight into how manufacturing entered 2026. The data have been volatile, but orders, shipments, and pricing matter more than the headlines.

Friday: Industrial production, capacity utilization, and the NAHB Housing Market Index will round out the week.

The Beige Book will be quietly influential throughout. Confirmation of a low-hire, low-fire labor market would reinforce patience into the spring. With Chair Powell under scrutiny, Fed communication will be parsed less for timing and more for institutional resolve.

Piedmont Perspective

Institutional Home Buying: Populism Meets the Balance Sheet

President Trump’s proposal to limit institutional purchases of single-family homes is best understood as a political signal rather than an economic lever. It speaks to real affordability frustration among younger households, but its economic impact is limited.

Institutional investors hold only 1–3% of single-family homes nationally and under 5% of single-family rentals. Where they matter is at the margin. Purchase flows can amplify price pressure in fast-growing metros during low-inventory periods, particularly in parts of the Sun Belt and Midwest.

Even there, institutions are not the root cause. The binding constraints are underbuilding, zoning restrictions, infrastructure costs, and in-migration. Since 2022, large institutional buyers have slowed acquisitions, shifted toward build-to-rent, and in some cases become net sellers. Restricting their participation risks slowing one of the few scalable sources of new housing supply without materially improving affordability.

Housing responds to capacity. Policies that expand it tend to work. Policies that constrain it tend to reshuffle ownership while leaving prices largely unchanged.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 12, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000