Highlights of the Week

- Growth is cooling at the margin, not stalling; resilience remains the defining feature of this cycle. We expect growth to handily top consensus estimates.

- Inflation data noise persists, but housing disinflation is increasingly durable and broad-based.

- Lean inventories and a solid holiday season are quietly rebuilding the industrial pipeline.

- Manufacturing and logistics are setting up for a rebound in 2026 driven by normalization, not excess.

- 2026 will be a momentous year for the U.S., marking the nation’s 250th anniversary, the hosting of the World Cup, the expiration of key provisions of the 2017 tax cuts, a scheduled USMCA review, and concluding with midterm elections.

Confidence, Constraints, and Narrowing Margins

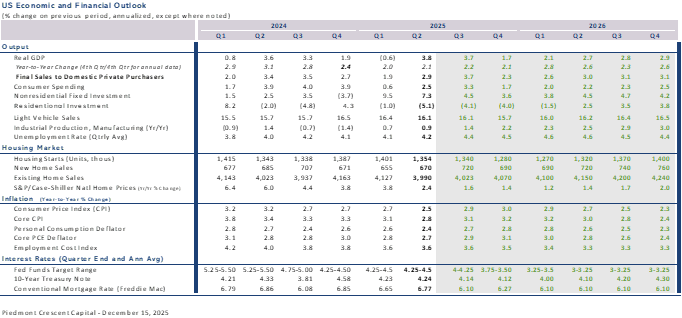

The U.S. economy is closing out the year with more resilience than many expected. While the runway is a bit foggy, Santa’s sleigh looks likely to make its rounds with ease. Low inventories, a solid holiday season, and a growing sense that the economy bends rather than breaks are setting the stage for a rebound in manufacturing and logistics as 2026 approaches.

Recent data reinforce that view. Existing home sales remain subdued, but pricing pressure is easing as inventories slowly rebuild. Consumer sentiment has improved modestly, consistent with real income growth continuing to outpace headline inflation. We are also seeing more promotional activity at grocery stores, as food companies reintroduce discounts to support volumes. The picture is not one of acceleration, but of durability.

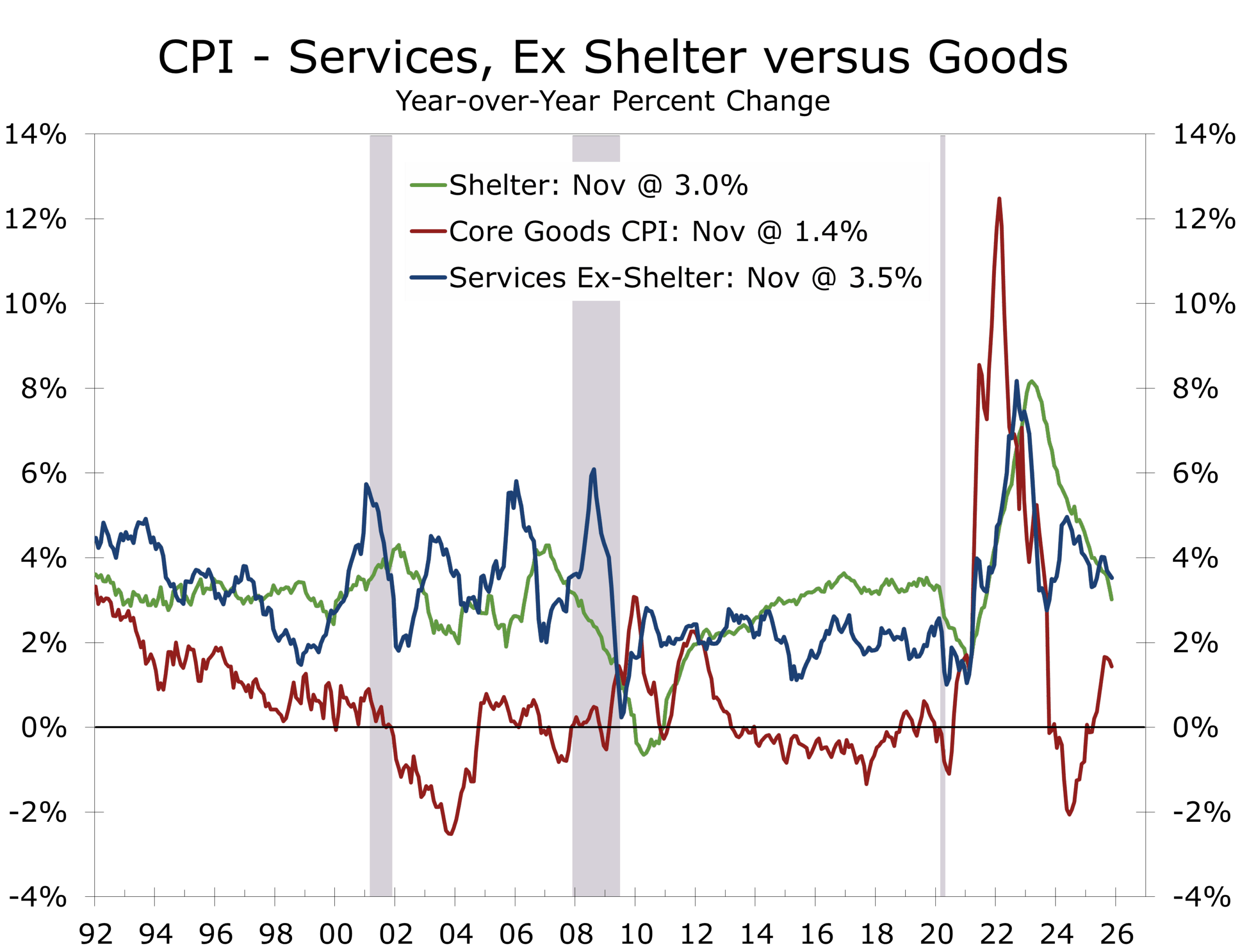

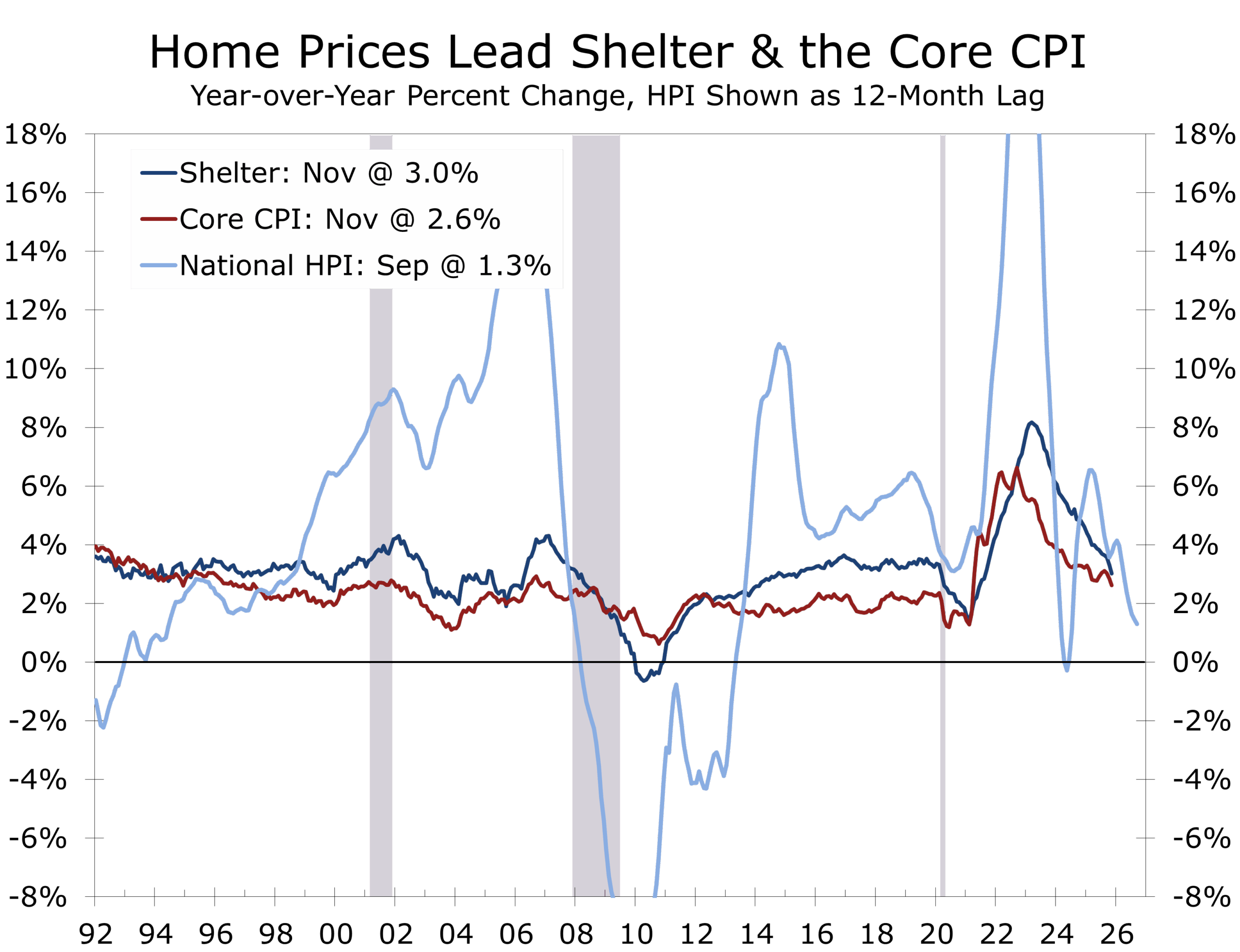

Inflation dynamics continue to evolve in the Federal Reserve’s favor. Housing costs are clearly decelerating, both in market rents and in forward-looking measures embedded in CPI. While debate persists around the precision of the latest CPI report, there is far less disagreement about direction. Housing prices have fallen sequentially in five of the past six months, and the year-over-year increase has slowed to roughly 1.3%. More importantly, inflation is likely to improve more meaningfully in 2026, as changes in home prices and rents filter gradually into official measures.

Inflation is no longer broad-based; it is now concentrated, political, and idiosyncratic.

Consumers may also receive relief on another front. Despite the horrific fires in Los Angeles that opened 2025, the year ultimately saw fewer catastrophic weather events, with no major hurricanes making landfall. As a result, property and casualty insurance costs are likely to ease in 2026. Energy costs are also likely to provide consumers with a meaningful break.

Inflation: data noise versus durable signals

Concerns about persistent data distortions in inflation reports are understandable—but they risk overshooting the runway.

The data may be noisy, but the housing signal is clear—and it points to durable disinflation.

Some CPI and PCE components will remain noisy due to survey timing, seasonal adjustments, and lingering post-shutdown effects. But the most important inflation component—housing—is sending a consistent and reassuring signal across multiple independent measures. Market rents have flattened or declined year over year, new lease growth has cooled materially, and multifamily completions remain elevated. Owners’ Equivalent Rent, slow by design, is now catching up to reality.

The takeaway is straightforward: the instruments may wobble, but the destination is clear. Housing disinflation is real, durable, and likely to continue capping inflation prints well into 2026, making today’s debate about missing data petty and insignificant.

Looking ahead, insurance costs are the next swing factor. Fewer catastrophic storms should ease property and casualty premiums. Health insurance remains the wild card, with policy choices likely to distort pricing regardless of the macro backdrop.

Financial markets reflect this mix. Equities have moved higher with narrow leadership, Treasury yields have drifted lower, and credit spreads remain contained. The message is not exuberance, but confidence that policy tightening has done enough. Markets continue to assume that the Federal Reserve can move from restraint to calibration without triggering a downturn.

Manufacturing and logistics: setting up the rebound

One of the more underappreciated developments this year has been inventory discipline. Firms entered the holiday season lean, and early indications point to solid seasonal demand.

Late-cycle rebounds are often industrial and investment driven, not consumer-led.

Low inventories, improving demand visibility, easing inflation and lower interest rates create fertile ground for a rebound in manufacturing and logistics. Even modest restocking can translate into a meaningful pickup in orders, production, and freight volumes.

Piedmont Perspective: The Election Year Economy

Political handicapping currently point to a decisive midterm outcome. Both traditional forecasters such as the Cook Political Report and market-based indicators like Polymarket reflect today’s dissatisfaction with affordability and inflation.

That view risks underestimating how different the economy may look by November 2026.

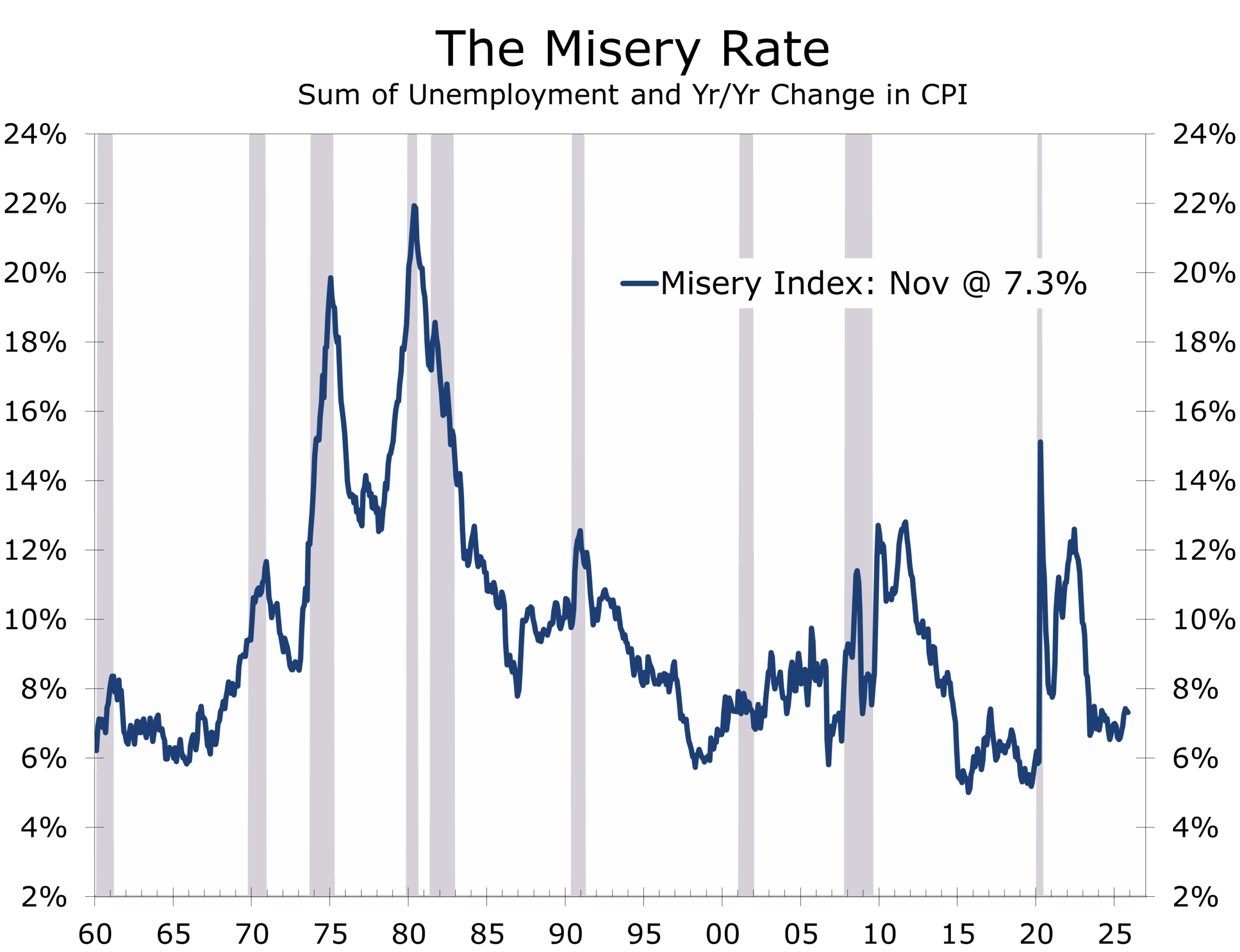

Elections tend to be driven less by economic levels than by economic direction. Several indicators that historically correlate more closely with electoral outcomes are likely to improve over the next year. The Misery Index should decline as inflation cools and labor-market softening remains orderly. Real per-capita disposable income should improve as nominal growth again exceeds inflation.

With Republicans controlling the White House and both chambers of Congress, messaging is likely to emphasize progress—cooler inflation, steadier growth, and rising real purchasing power. Democrats are likely to stress persistent affordability challenges, particularly groceries, housing, and healthcare.

In an era that feels like permanent campaign season, both narratives can coexist. The economy does not need to boom to alter the political landscape; it simply needs to improve. We expect the election outcome to become a closer call as we get closer to November.

Tuesday, December 23

A heavier-than-usual holiday calendar, though most data is shutdown-delayed and backward-looking:

- GDP (Q3, delayed estimate)

- Durable Goods Orders (October, preliminary)

- Industrial Production & Capacity Utilization (November)

- Consumer Confidence (Conference Board)

- New Home Sales (October, delayed)

GDP will attract the most attention, but holiday liquidity and timing limit reaction.

Wednesday, December 24 (Christmas Eve)

Early market close. No major releases. Liquidity thin.

Thursday, December 25 (Christmas Day)

U.S. markets closed.

Friday, December 26

Markets reopen with limited participation. Any releases should be treated cautiously.

Final Thoughts: policy, permanence, and perception

This cycle continues to defy simple labels. Growth is slower but intact. Inflation is cooling, even if the data occasionally obscures the trend. Housing is no longer a drag, inventories remain lean, and investment is quietly reasserting itself as a stabilizing force.

Slower growth, cooler inflation, and a cautious Fed are reshaping the cycle without breaking it.

What distinguishes the current environment is the durability of policy choices shaping it. Trade policy, often framed as tactical, is increasingly being applied with longer horizons in mind—reshaping supply chains, redirecting capital, and reinforcing geopolitical objectives with limited inflationary spillover.

That durability matters in an era that feels like perpetual election season. By the time voters head to the polls in 2026, the economy they experience is likely to look meaningfully different from today’s debate. Cooler inflation, steadier growth, and rising real incomes would complicate prevailing narratives—without requiring an outright boom.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 22, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000