Inflation Continues to Frustrate Consumers

- This past week’s inflation reports came in slightly above expectations but still showed inflation decorating back toward 2%.

- Lower gasoline prices helped restrain inflation, with the Consumer Price Index rising 0.2% in September, pulling the year-to-year change back down to 2.4%.

- Prices excluding food and energy items rose 0.3%, paced by another large increase in motor vehicle insurance costs, a rebound in airfares and continued pressure on rents.

- Core goods prices fell by 0.2%, following a 0.3% decline in August, and have increased only 0.2% over the past year.

- The Fed has shifted their focus from preventing the labor market from cooling too much. For consumers, however, inflation remains their primary concern.

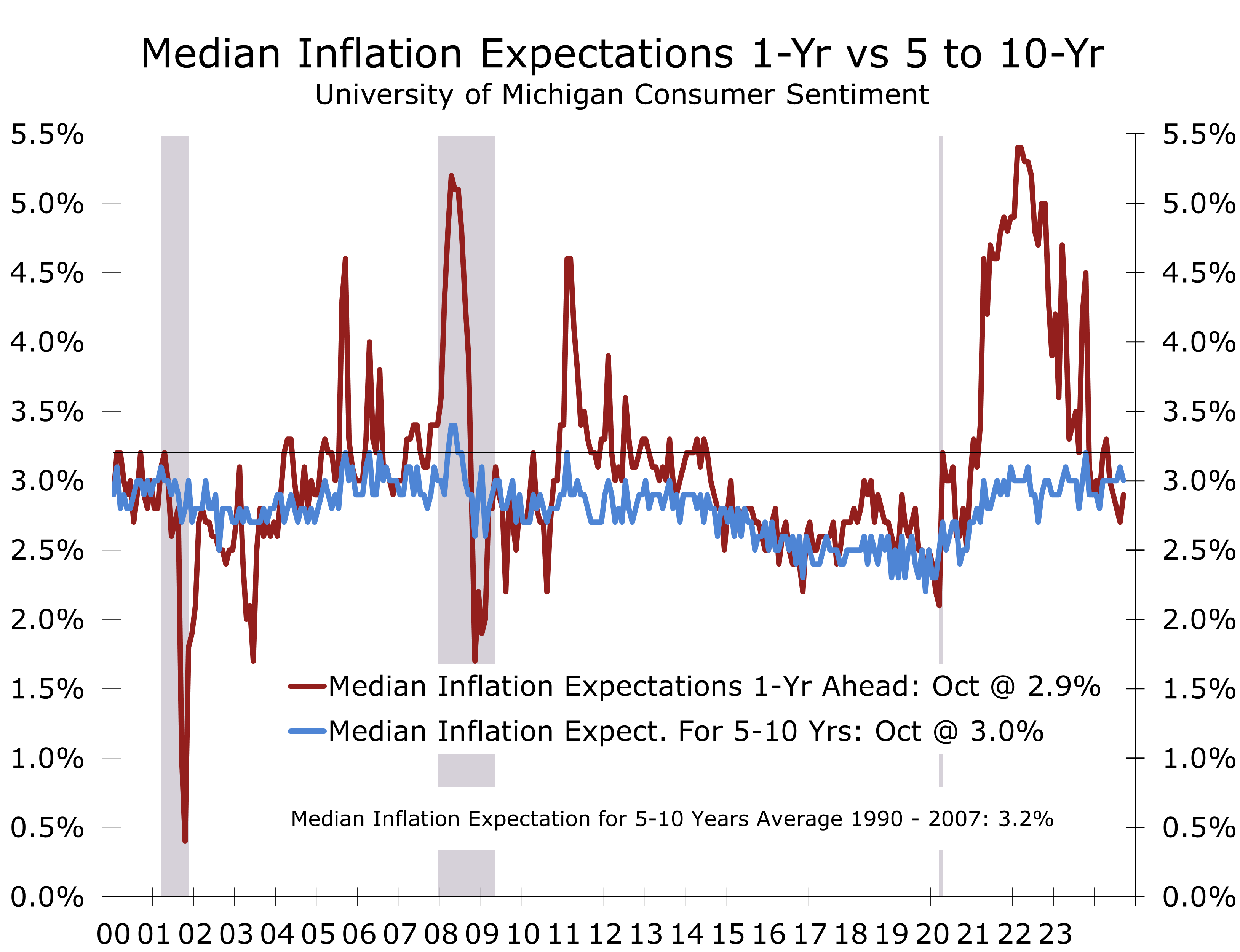

- The early October read on Consumer Sentiment came in below expectation, with the headline index falling 1.2 points to 68.9. Inflation expectation increased, however.

Inflation took center stage last week as the markets continued to digest September’s stronger-than-expected jobs numbers and the earlier upgrades to GDP and National Income data. The economy looks far more resilient today and less in need of aggressive interest rate cuts. Moreover, September inflation data came in slightly hotter than expected, suggesting the balance of risks has shifted slightly more toward inflation taking longer to return to the Fed’s 2% target. The Fed now seems set to cut the federal funds rate by a quarter percentage point at the November and December FOMC meetings, while a half-point cut now seems off the table.

The Consumer Price Index (CPI-U) increased 0.2% in September, matching gains in August and July. Year-over-year, the index rose 2.4%, marking the smallest 12-month rise since February 2021.

While the headline inflation rate shows improvement, the underlying details are less encouraging. A 4.1% drop in gasoline prices helped hold down the overall CPI, but that decline seems to have ended. Grocery prices surged 0.4% in September, with meats, poultry, fish, and eggs experiencing a notable 0.8% increase. Dining out costs rose 0.3%, with full-service restaurant prices increasing more sharply than those at fast-food and other limited-service restaurants.

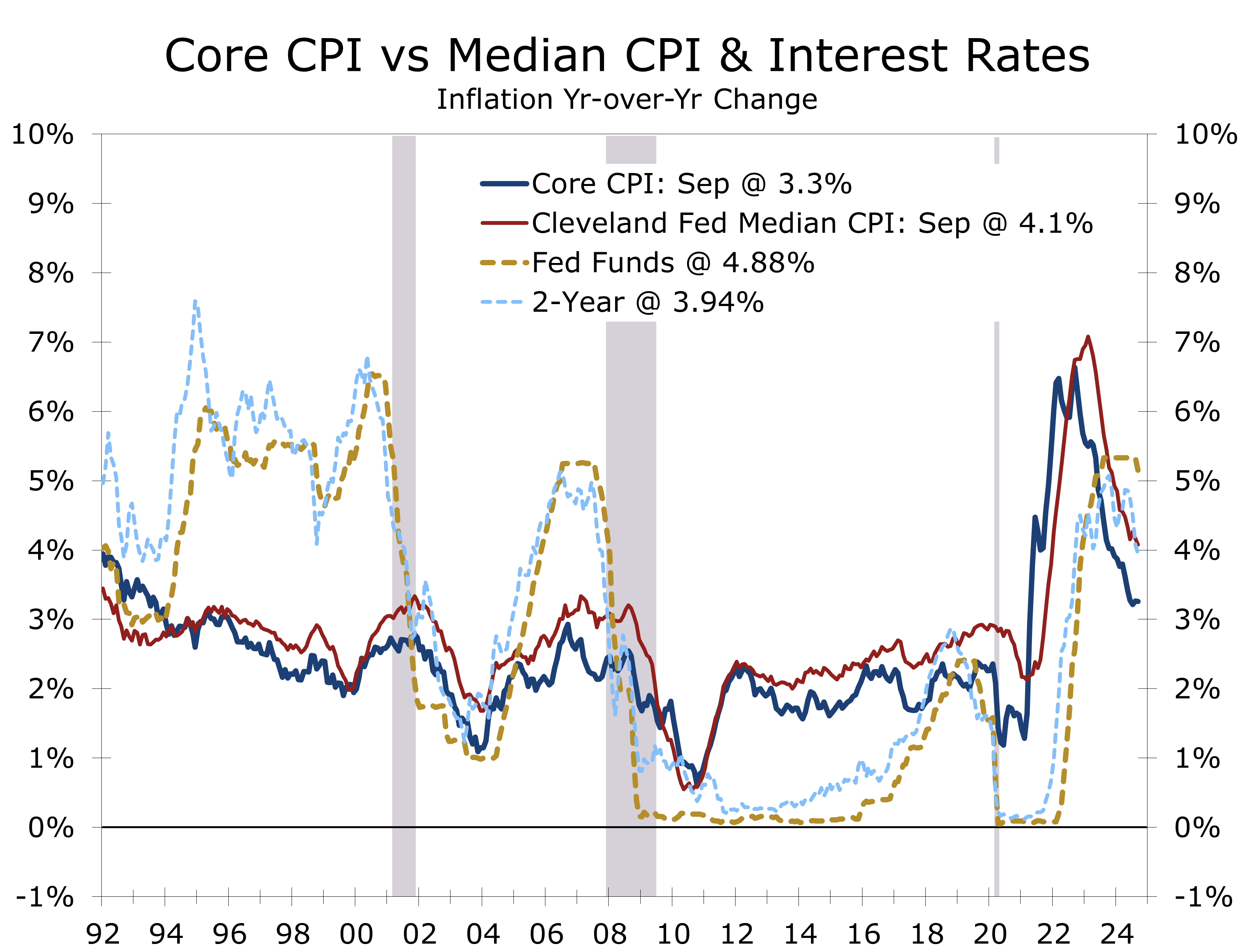

Excluding food and energy, the core CPI increased 0.3% in September and 3.3% over the past year, driven by sharp gains in motor vehicle insurance (16.3%) and medical care (3.3%). The Fed breaks inflation into three buckets: core goods, services excluding shelter, and housing costs. Core goods prices are declining, supported by China’s export-driven growth, but core services and housing prices are moderating at a slower pace. Shelter costs have risen 4.9% over the past year.

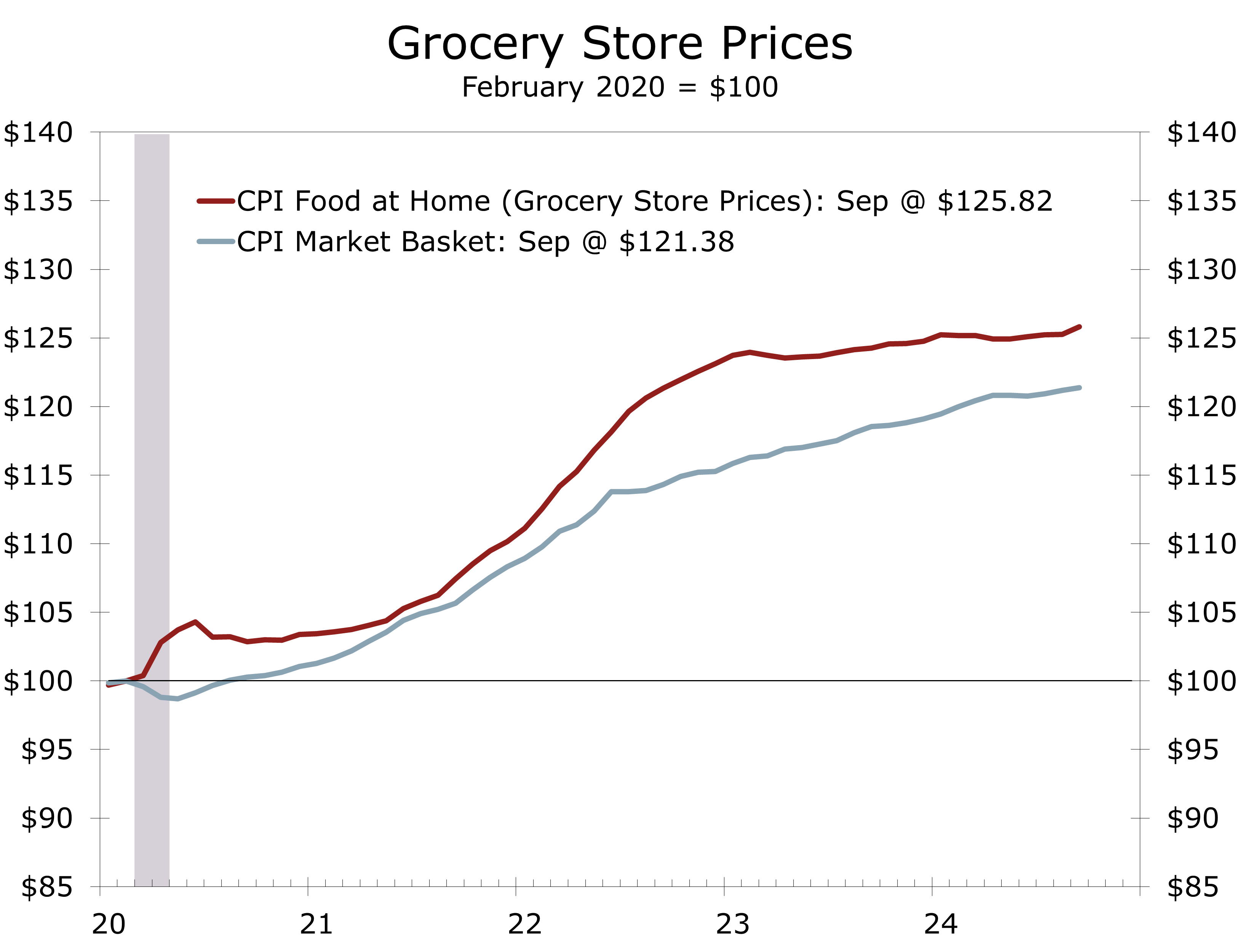

While the headline inflation rate has fallen from its June 2022 peak of 9.1% to 2.4%, consumers have not seen much relief. This lower inflation rate reflects only a slower pace of price increases, not a reduction in prices. Since February 2020, the Consumer Price Index (CPI) has risen by a cumulative 21.4%, meaning prices remain significantly higher than before the pandemic.

One of the clearest examples is grocery costs, with food prices for home consumption up 25.8% since early 2020. A family that spent $100 a week on groceries before the pandemic now spends $125.82 for the same items. Meat, poultry, and fish have seen particularly steep increases, with prices up nearly 30%.

Housing costs have also surged. Shelter costs, which include residential rent, owners’ equivalent rent, and lodging away from home, have risen by 25% for rent-related components and 10% for lodging. Home prices, as measured by the S&P Case-Shiller Home Price Index, have increased by 58% since before the Pandemic, while apartment rents have climbed 21.2%, according to ApartmentList.com.

Higher prices for necessities mean the impact of inflation is affecting a broad range of households. Additionally, the increased costs of regularly purchased items, such as groceries and rent, keep inflation at the forefront of consumers’ concerns, weighing on consumer sentiment.

The early October reading of the University of Michigan’s consumer sentiment came in softer than expected, falling from 70.1 to 68.9. Both current conditions (-0.6 points to 62.7) and future expectations (-1.5 points to 72.9) declined, reflecting lingering concerns about inflation, economic growth, large federal deficits, and political dysfunction.

Consumers were more pessimistic about their personal finances, though their outlook on business conditions and buying plans improved, likely influenced by the still solid job market and expectations of additional Fed rate cuts. Although high prices—particularly for food and shelter—remain a concern, a growing share of consumers expect their income to outpace inflation over the next five years.

Year-ahead inflation expectations edged up from 2.7% to 2.9%, slightly higher than they were prior to the pandemic, while long-term expectations dipped slightly to 3.0%. The increase in short-term inflation expectations may have been influenced by the recent uptick in grocery prices, which rose 0.4% in September—the largest jump in 20 months.

Consumer sentiment often pulls back ahead of presidential elections and rebounds afterward, regardless of the outcome. The resilience in buying plans suggests that consumer spending should hold up reasonably well heading into the holiday season.

One issue weighing on inflation concerns is how Israel will respond to Iran’s launch of 180 ballistic missiles at Israel earlier this month. We noted last week that Israel needs to tread carefully, as another demonstration strike—showing Iran that they can hit its most sensitive sites—is unlikely to intimidate Iranian leadership. Israel must also guard against upsetting current U.S. leadership, which would not look kindly on being drawn into a conflict just as the U.S. holds its presidential election. The post-election environment may provide a greater degree of freedom.

We would be surprised if Israel simply targeted Iran’s energy infrastructure.

We believe that all options are on the table, and a response after the U.S. presidential election is likely to be more disruptive than what Western leaders have feared. We would be surprised if they simply targeted energy infrastructure, as that would provide only ephemeral satisfaction and offer little to no long-term deterrent.

In the near term, we expect Israel to continue pressing hard against Hezbollah and what remains of their leadership. Israel aims to destroy as much military infrastructure in Southern Lebanon as possible and push the UN to enforce earlier agreements. Israel also has more work to do in Gaza and would like to wrap up military operations there by the end of the year.

The U.S. election has tilted back in Trump’s favor, with three weeks to go until Election Day. The popular vote is roughly even between Harris and Trump, but Trump is leading in all the swing states. The GOP also looks poised to regain control of the Senate, while the Democrats are likely to take over the House.

Long-term interest rates have risen since the disappointing September CPI report. Inflation came in hotter than expected, and the only reason the overall CPI improved on a year-to-year basis is that gasoline prices plummeted. Food prices spiked, however, and core inflation remains stubbornly high. Rents are showing signs of accelerating, as a rising tide of renters is renewing their leases at rates roughly 3.5% higher than they were a year ago. We expect residential rents to rise by at least 3.5% in 2025, despite new supply.

The bond market senses that bringing inflation back down to the Fed’s 2% target on a sustained basis will be difficult, particularly with increased government spending, persistent large federal deficits, and a bloated Federal Reserve balance sheet. The market’s expectations for the federal funds rate one year out are now pricing in four more quarter-point cuts: two this year and two more in the first half of next year. We continue to expect five more quarter-point cuts, as we foresee growth slowing over the next two quarters.

Lower short-term interest rates will help the economy. Credit lines tied to short-term rates will reprice lower, and consumers should also be able to borrow at lower rates to purchase motor vehicles and other big-ticket items. Monetary policy, however, is not as easy as it used to be. The Fed will need to weigh how further rate cuts will impact long-term interest rates. Bond yields are now back near the levels that prevailed prior to the half-point September rate cut. Mortgage rates have spiked recently, which is having a chilling effect on home sales and mortgage refinancings.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 14, 2024

Mark Vitner, Senior Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000