Growth Worries Overtake Inflation Concerns

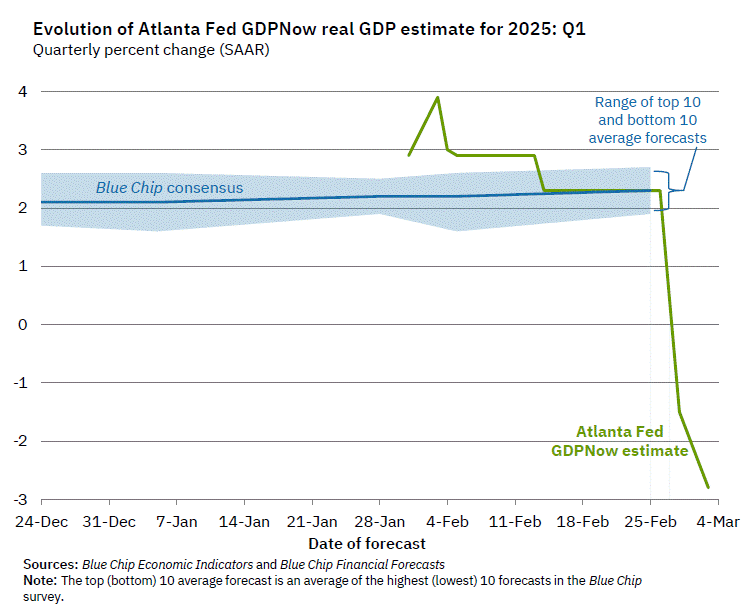

- Growth concerns retook center stage with the Atlanta Fed’s GDPNow forecast plunging 5.5 points since Thursday to -2.8% for Q1, mostly due to a surge in imports.

- Consumer spending fell 0.2% in January, and consumer confidence saw the largest decline since 2021.2%.

- Consumers also feel less upbeat about the labor market, and weekly first-time unemployment claims rose to 242,000.

- Inflation moderated slightly, with the overall PCE price index decelerating to 2.5% year-to-year in January. The core PCE decelerated to 2.6% year-to-year.

- The U.S. trade deficit widened to a record $153.3 billion in January, driven by a surge of imports ahead of expanded tariffs.

- The February ISM Manufacturing PMI and January construction spending both came in weaker than expected, contributing to growth concerns.

- The S&P 500 sold off sharply on tariff concerns, falling 4.8% since February 19. Bond yields have also fallen sharply, with the 10-Year Note falling below 4.20%.

Recent economic data reveals a mixed picture: inflation is easing, but growth is slowing sharply, as evidenced by the Atlanta Fed’s GDPNow forecast plummeting from 2.3% to -2.8% in just a few days. This, coupled with rising geopolitical uncertainty, creates a volatile economic landscape.

The sudden shift in the Atlanta Fed measure suggests that economic growth has slowed from its recent strong pace. The latest data show real GDP grew at a 2.3% pace in the fourth quarter. Private final domestic demand, our preferred output measure, grew at a 3% pace, which is roughly in line with its average for the past two years.

More recent data suggests downside risks to economic growth have risen. Consumer spending fell 0.2% in January, the largest drop in 4 years. This drop may be partly due to unseasonably cold weather, which kept buyers away from car dealers. The Los Angeles wildfires and post-holiday seasonal factors may have also exaggerated the extent of January’s weakness.

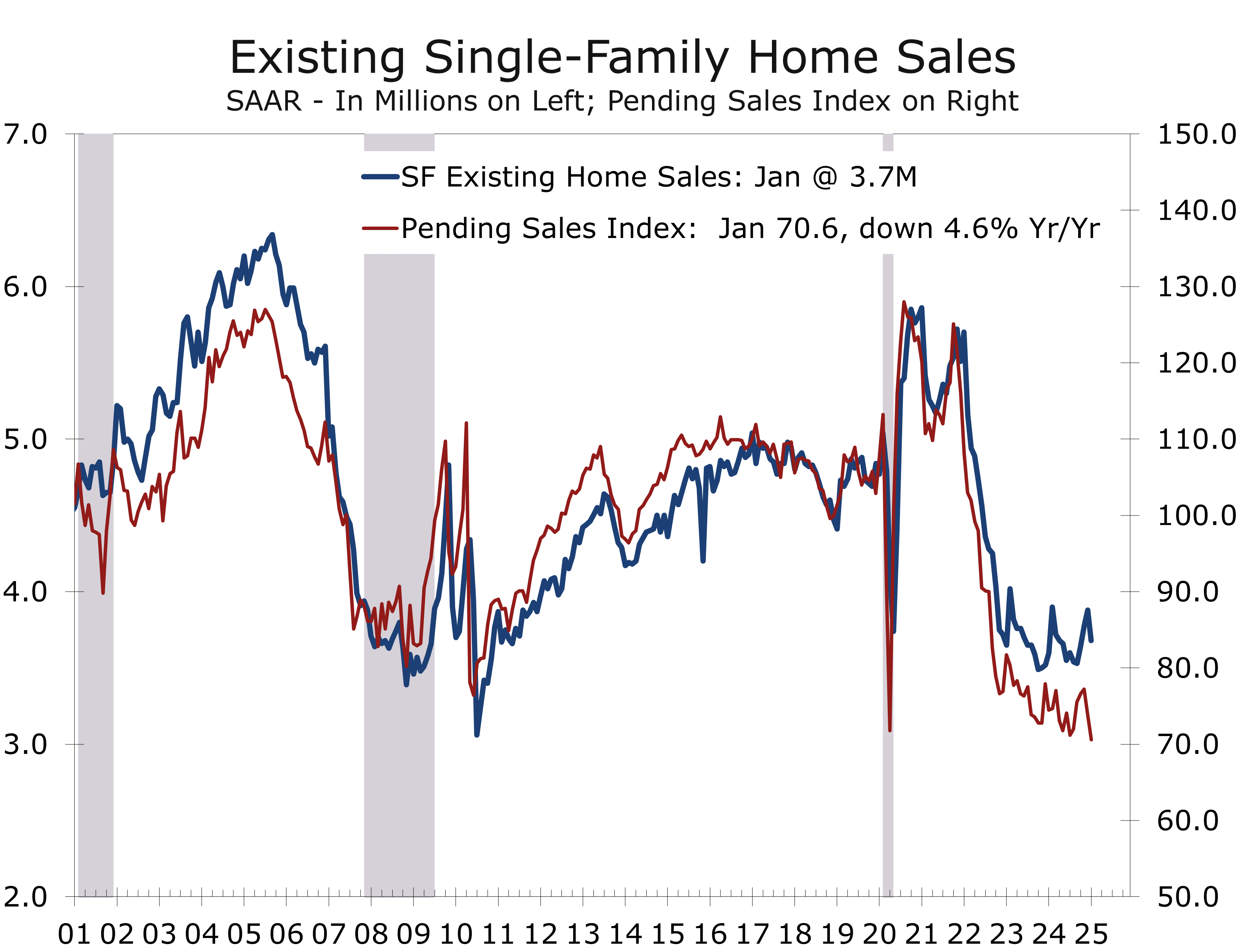

Part of the spending pullback is legitimate, however, and reflects a downshift in economic growth. Both new and existing sales remain exceptionally weak and pending home sales, which lead existing home sales by a month of two, plunged to an all-time low in January. The weakness in home sales is carrying over into reduced demand for household durable goods and home furnishings. The recent slide consumer confidence validates the slowdown and hints that February’s spending, which should show some improvement, will likely be weak as well.

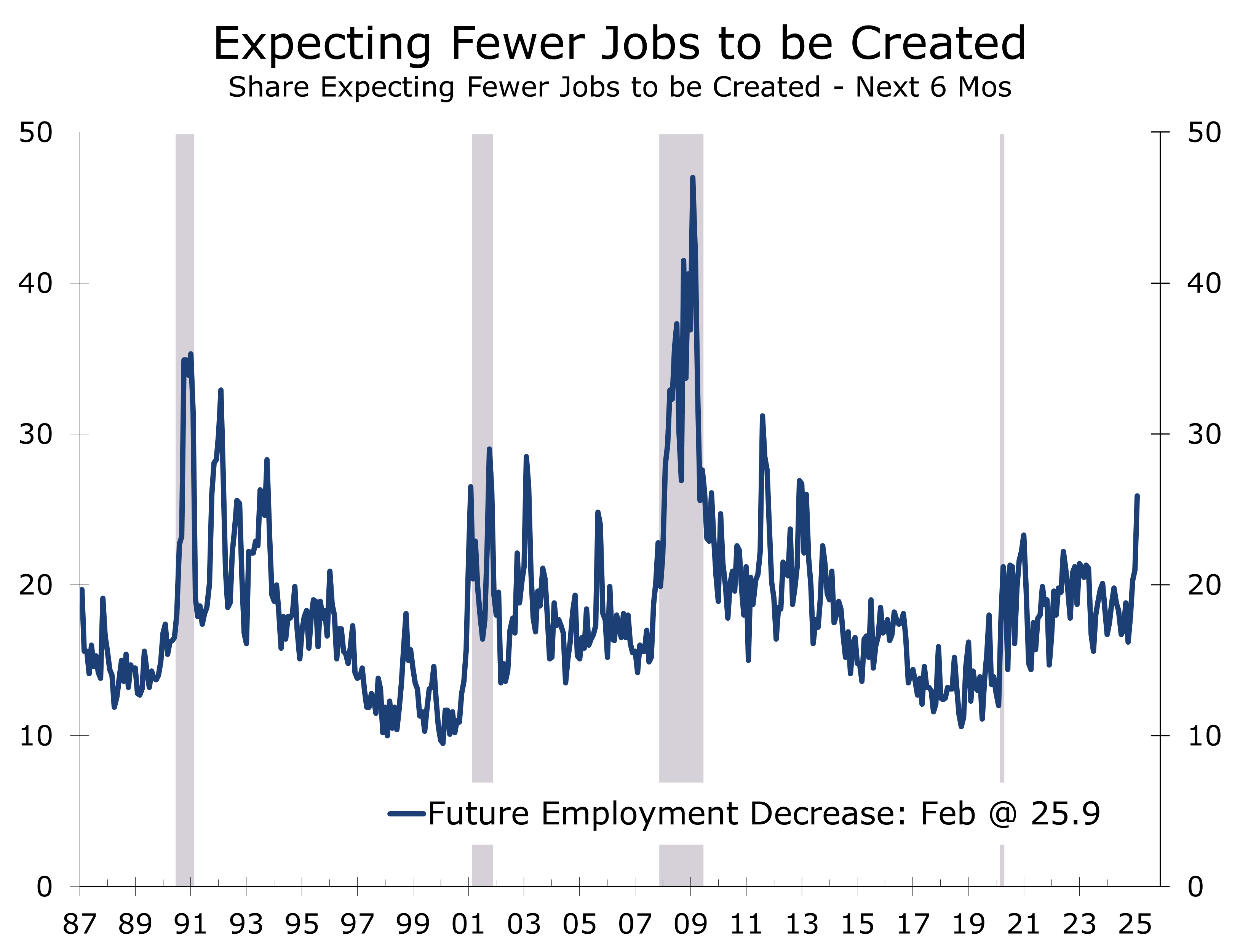

Consumer confidence took a big hit in February 2025, with the Conference Board’s index posting its largest monthly decline since 2021, falling to 98.3 from 105.3 in January. Both current conditions and future expectations worsened, with expectations plummeting nearly 10 points to 72.9. The labor differential, the difference between the share of respondents saying jobs are ‘plentiful’ versus ‘hard to get’, decreased for the second straight month and is near a cycle low. Moreover, more consumers expect fewer jobs to be created over the next six months (25.9%) than any time since the pandemic.

We are beginning to see some cracks in the labor market. Weekly first-time unemployment claims rose last week to 242,000 from 220,000, with claims in Washington, D.C., roughly four times higher than they were this time last year, likely evidence of Trump’s layoffs of government employees and belt-tightening by contractors. Jobless claims remain historically low, and most forecasts have the unemployment rate holding steady at 4% in February.

January’s PCE inflation moderated to 2.5% year-over-year, down from 2.6% in December. The core PCE deflator also decelerated to 2.6% in January, down from 2.9% in December. The better PCE news is a relief following more problematic gains in the CPI and PPI earlier in February and rising inflation expectations in the Consumer Sentiment survey.

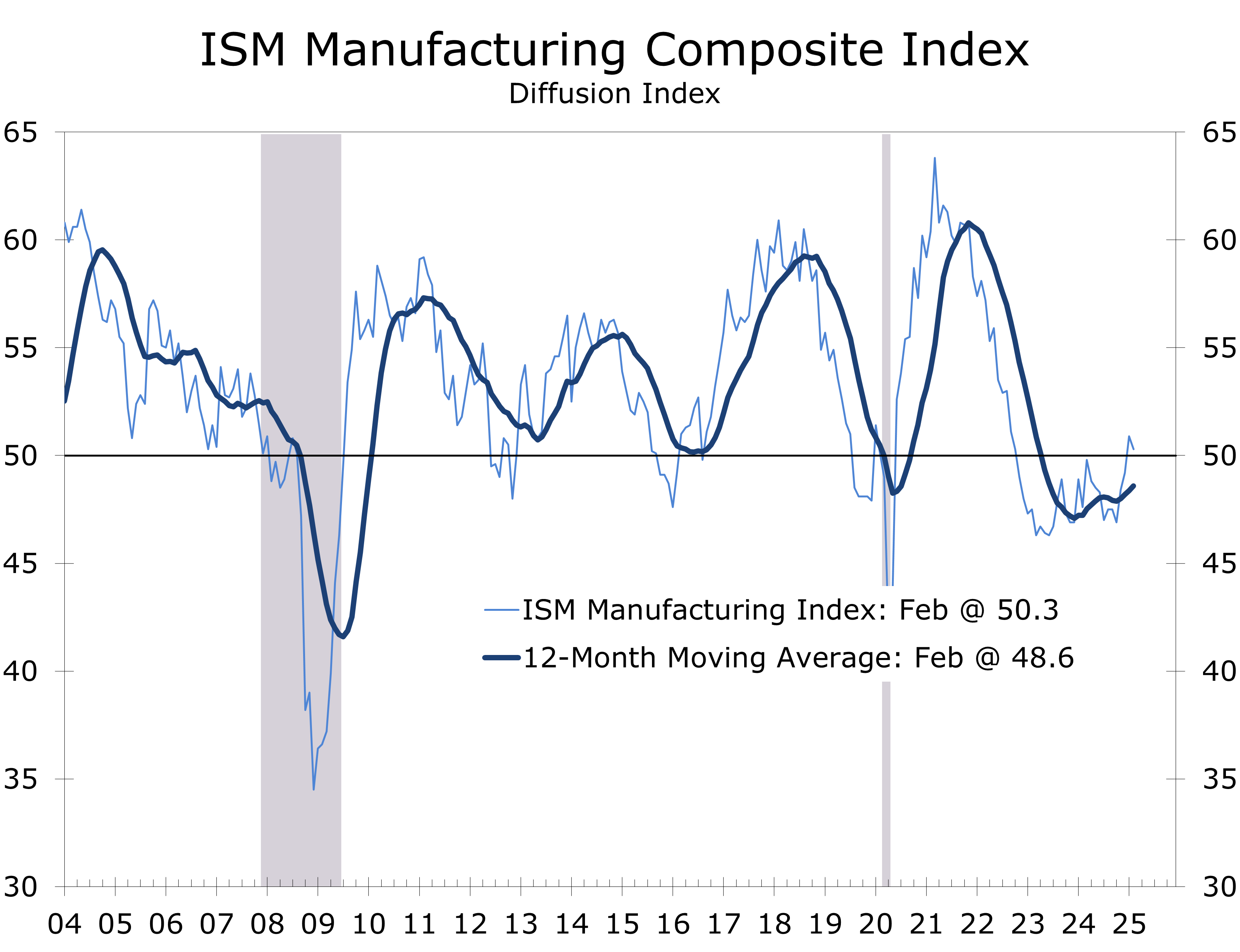

The ISM Manufacturing Purchasing Managers Index (PMI) fell slightly more than expected, falling 0.6 points to just 50.3 in February. The PMI held just above the key 50 break-even level, which signals expansion in manufacturing, for the second consecutive month, following 26 months of contraction.

The underlying data in the PMI were weak, including New Orders, which dipped to 48.6 and Production, which slipped to 50.7, showing continued expansion. The Employment Index fell to 47.6, suggesting some softening in manufacturing jobs, while the Prices and Suppliers Delivery indices both jumped to their highest levels since 2022. Tariffs were mentioned 20 times in the ISM report, highlighting the impact that policy uncertainty is having on businesses and supply chains.

The front loading of imported goods and materials has caused imports to skyrocket and widened the trade deficit to a record $153.3 billion in January. Industrial supplies accounted for much of the increase and some of that will likely end up in inventories, which will partially offset the hit to Q1 GDP growth.

The sharp reversal in the closely watched Atlanta Fed GDPNow forecast has garnered significant attention. The index plunged a combined 5.5 points Friday and Monday, reflecting weaker consumer spending, the deluge of imports and weaker January residential construction spending.

GDPNow provides a highly mechanical estimate of GDP by extrapolating the latest economic data based on historical relationships. While valuable, it should be used with caution. Much of the recent weakness stems from a surge in imports as businesses move to get ahead of tariffs. These imports will increase inventories, consumer spending or investment, which will show up later in GDPNow, partially offsetting the drag from the widening trade deficit. Additionally, gold imports—excluded from GDP—also surged.

As a result, while Q1 GDP growth will likely be weaker, a -2.8% contraction seems overstated. Our forecast now stands at +0.9% and assumes a rebound in consumer spending, large rise in inventories and a narrowing trade gap in the coming months.

Atlanta Fed GDPNow is a highly mechanical tool and likely exaggerates the recent deterioration.

Financial market volatility has risen as market participants’ primary concern has shifted from inflation back to economic growth. The S&P 500 has fallen 4.8% since February 19, with about one-third of that drop coming Monday after President Trump affirmed that 25% tariffs on Canada and Mexico would go in effect on February 4. Bond yields have also plummeted, with the 10-year Treasury yield falling from 4.79% on January 14 to just 4.16% on Monday. The yield on the 10-Year Treasury is now back below the 3-Month T-Bill. The 10-Year yield still remains above the 2-Year, but the spread has narrowed in ways that have historically signaled slower growth ahead.

Trump-Zelenskiy Meeting and Fallout

President Donald Trump and Ukrainian President Volodymyr Zelenskiy held a tense meeting at the White House on February 28, ending with Trump canceling a planned news conference and asking Zelenskiy to leave. Tensions escalated when Zelenskiy pressed for security guarantees, and Vice President Vance pushed back, raising a range of other grievances. The fallout from this clash could weaken U.S. support for Ukraine at a critical moment in its war with Russia. It also heightened concerns about ongoing tariff negotiations, adding to supply chain concerns.

Elon Musk’s Call for U.S. to Leave NATO and UN

Elon Musk publicly called for the U.S. to withdraw from NATO and the United Nations over the weekend. This move aligns with growing skepticism within the Trump administration towards international organizations and alliances. We do not see a scenario where the U.S. pulls out of NATO. We also see little prospect that Trump will let Russia run over Ukraine. The rhetoric is dangerous, however, and could serve to bolster Russia’s confidence and demoralize Ukraine. History has shown time again that appeasing an aggressor only leads to more destructive aggression.

Cultural Reflection: The 2025 Oscar Ceremony

“Anora” dominated the Academy Aways, winning best picture, director, actress, editing, and original screenwriting. Sean Baker won for directing, editing, and writing, while Mikey Madison won best actress and Zoe Saldaña won best supporting actress for “Emilia Pérez.” Hollywood is one of the world’s leading U.S.-based institutions that has the heft to promote freedom, human rights, and ideals to move mankind in a positive direction, even if we often collectively shake our heads at what passes for entertainment.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 4, 2024

Mark Vitner, Senior Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000