Hiring Remains Soft, As Job Gains Narrow

- Nonfarm payrolls rose by 147,000 in June, narrowly above the revised May figure of 144,000 and in line with the 12-month average of 146,000.

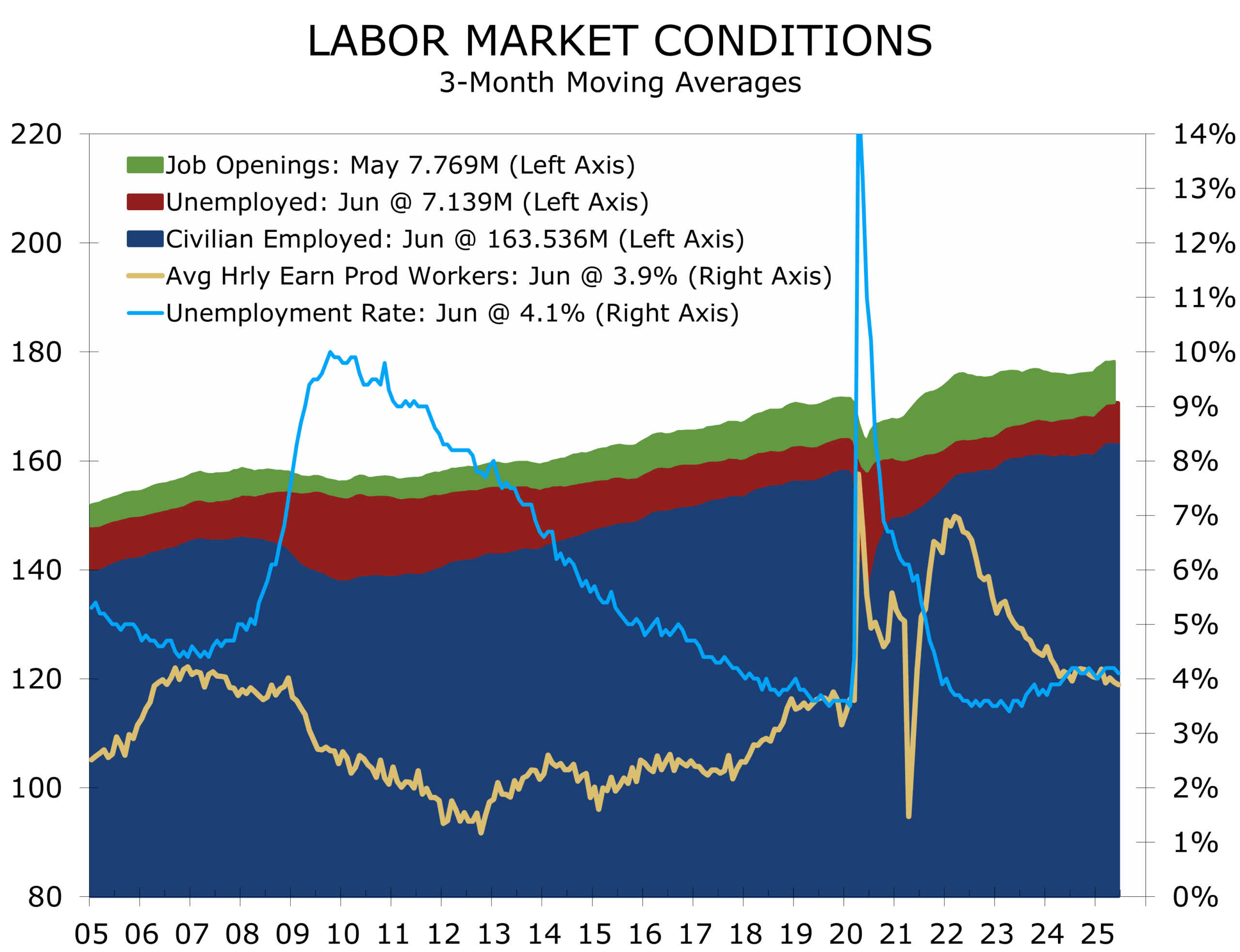

- The unemployment rate ticked down to 4.1%, but underlying slack continues to build, with long-term unemployment and marginal labor force attachment both rising.

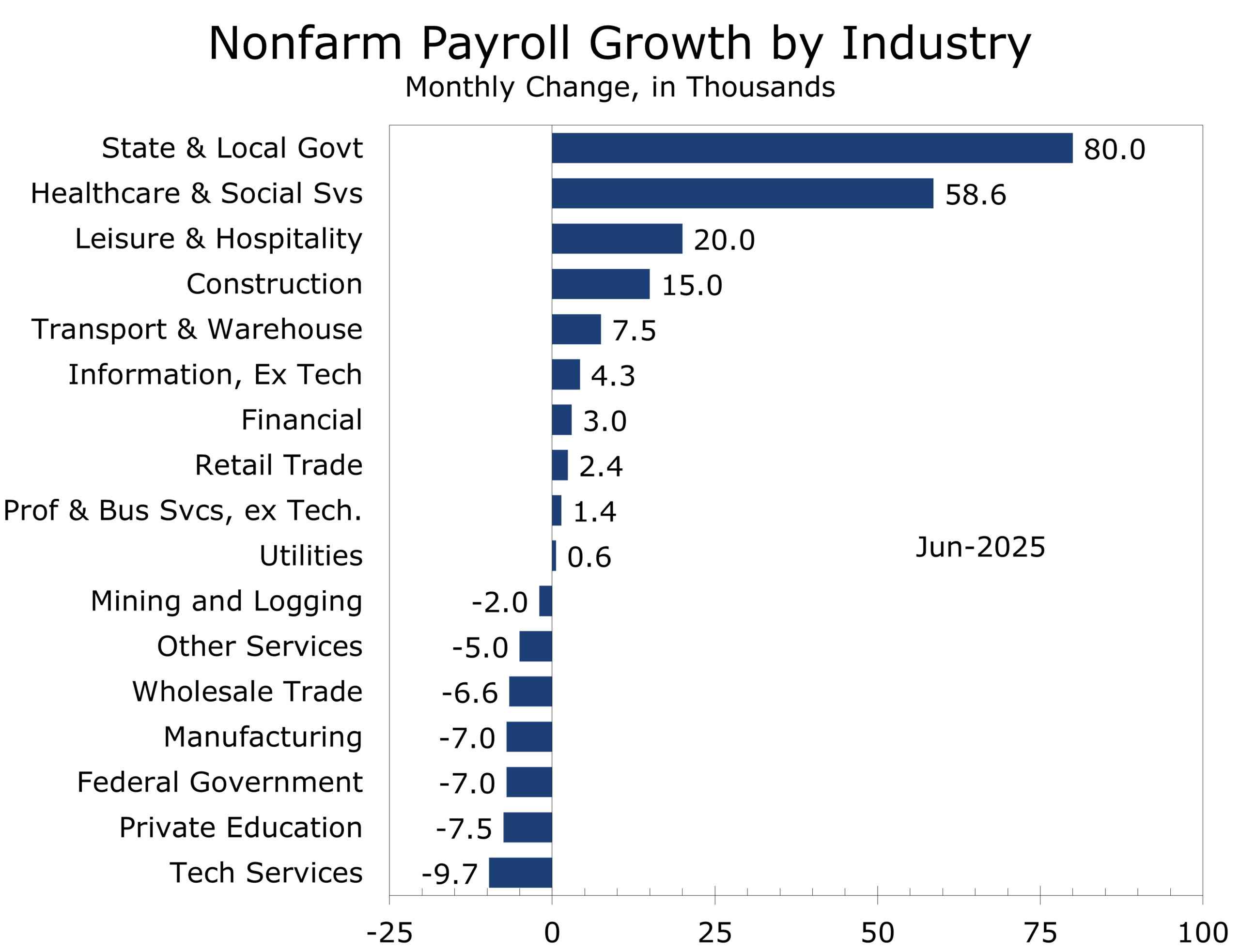

- Headline strength masked concentration: state and local government, health care, and social services accounted for nearly all of June’s job gains.

- Federal payrolls declined again, bringing cumulative losses to 69,000 since January.

- Construction added jobs, but only in specialty trade contractors—typically late-cycle hires—suggesting project backlogs are being completed, not expanded.

- Tech-related hiring remained flat, with no net gains in professional and technical services or the information sector—further evidence of AI-driven disruption and cautious budgeting.

- Financial markets were surprised by the stronger-than-expected headline, but the soft internals justify the Fed’s cautious stance and leave the July cut discussion on the table. We still expect the Fed to kickoff the next round of rate cuts in September.

Jobs Report: Nowhere Near as Strong as the Headline

The June employment report delivered a superficially strong headline—nonfarm payrolls rose 147,000, and the unemployment rate edged down to 4.1%—but the underlying data tell a more fragile story. Hiring continues to slow, with gains increasingly dependent on just a few sectors. The three-month average now stands at 143,000, and job gains were narrowly concentrated in public education, health care, and social assistance. These sectors added over 120,000 jobs combined, while most other areas—including retail, manufacturing, transportation, and finance—were effectively flat.

Federal employment fell another 7,000 and is down 69,000 cumulatively since January. While court rulings have temporarily halted some layoffs, voluntary quits, and retirements continue to chip away at headcount. The public sector’s strength lies entirely with state and local governments, particularly in education (65.5K).

Job growth is dependent on just a handful of sectors, as hiring remains largely on hold.

Construction saw a moderate increase, but all gains were in specialty trade contractors—workers typically hired at the tail end of building projects. Combined with softer construction spending and housing starts, this points to waning momentum and fewer new projects entering the pipeline.

Tech-related hiring remains under pressure, with IT services shedding 9,700 jobs in June. The AI-driven transformation, combined with ongoing cost discipline, continues to suppress hiring—particularly in white-collar roles. Unemployment is rising for programmers. Despite the productivity narrative, the headcount story remains defensive, as firms reassess staffing under mounting pressure to demonstrate returns on AI investment.

Despite booming equity values, high tech firms are continuing to reduce head count.

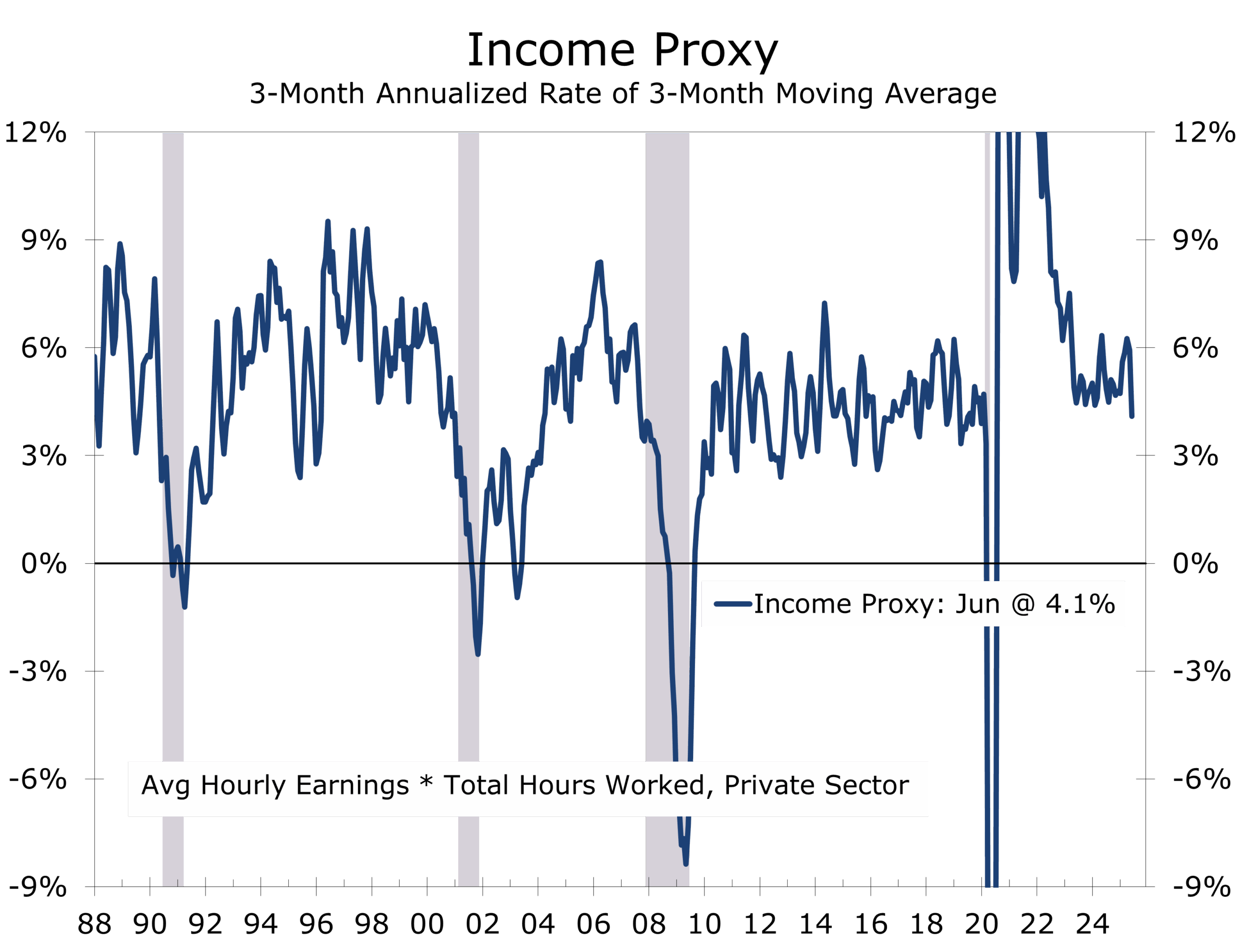

Elsewhere, job growth was notably absent. The diffusion index dropped back below the key 50 break-even level. Wage growth also cooled noticeably. Average hourly earnings rose just 0.2% in June, down from 0.4% in May. On a year-over-year basis, wages rose 3.7%, decelerating from 3.9%. The average workweek slipped to 34.2 hours. Together, this data points to softening labor demand, lower aggregate income gains and cautious consumer spending. Our income proxy has slowed just a 4.1% annual rate.

The underlying data are consistent with the market’s expectation for a weaker report. Businesses are not slashing payrolls; they are just reluctant to add to staff. The Conference Board’s measure of job availability has continued to weaken. While JOLTS job posting rose in May, hiring managers are clearly being more selective.

Markets briefly reacted to the stronger headline print, but internals quickly tempered the response. The Fed is likely to remain on hold in July, albeit with a less hawkish tone. Decelerating wages, flat private hiring, and rising slack strengthen the case for a rate cut later this summer, particularly if tariff risks, final demand, and global tensions continue to ease.

Tariffs—and the reluctance to appear politically influenced—continue to cloud the Fed’s decision.

FOMC Implications – July Rate Cut Talk Still in Play

June’s report reinforces the Fed’s wait-and-see stance. A strong headline justifies holding in July, but soft internals—slower wage growth, narrowing job gains, and rising long-term unemployment—keep a summer cut in play. With inflation subdued but tariffs still fueling inflation expectations, the bar for easing is high but increasingly within reach. The most likely kickoff remains the September FOMC meeting.

The labor market is not yet unraveling, but it is leaning harder on government and care-sector hiring. Private sector hiring largely remains on hold, while state and local governments and government-adjacent sectors continue to add staff. As H2 2025 begins, this narrow foundation limits upside surprises and reinforces a cautious policy bias.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 3, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

704-458-4000