What a Difference a Month Makes

-

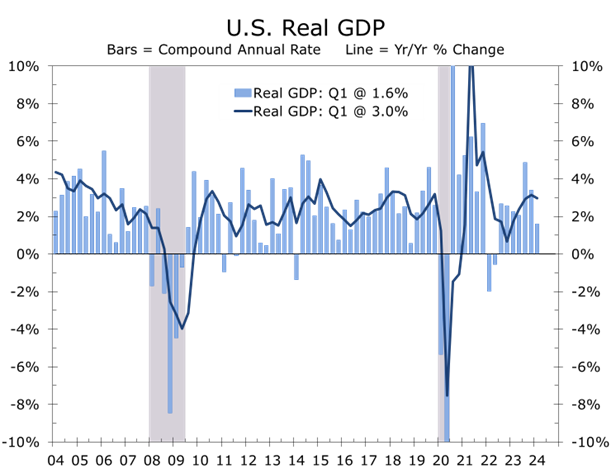

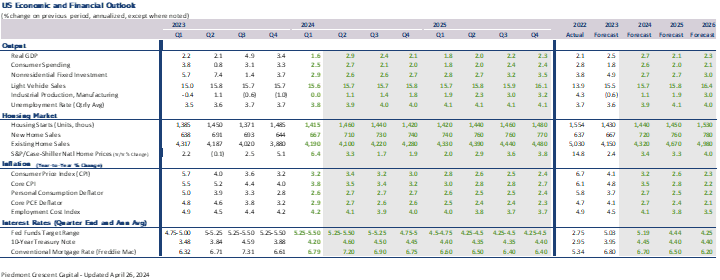

- First-quarter Real GDP growth was weaker than expected, increasing by only a 1.6% annual rate. This was due to a significant slowdown in exports, a slowdown in inventory building, and reduced federal spending. Additionally, consumer spending on goods inexplicably declined. Private final domestic demand (core GDP) grew at a healthier 3.1% annual rate, consistent with the previous two quarters. Core GDP is a better indicator of the economy’s underlying strength.

- While slower headline GDP growth is consistent with a soft landing, the financial markets are focused more intently on the continuing inflation The GDP deflator rose at a 3.1% pace in the first quarter, up from a 1.9% pace in the prior quarter. The PCE deflator rose at a 3.4% pace, while the core PCE deflator rose at a3.7% pace, up from 1.8% and 2.0% in Q4, respectively.

- The higher inflation evident in the GDP report amplifies concerns raised by the recent string of hotter-than-expected rises in the Consumer Price Index. Both the core and headline CPI rose 4% in March and climbed at a 3.8% and 4.2% pace, respectively in Q1. Persistently higher inflation has reversed all the optimism about lower rates that followed the December FOMC meeting. A growing number of forecasters now call for no cuts in the federal funds rate this year.

- Heightened geopolitical risks were the other major complicating event this past month, with Iran’s massive drone and missile barrage against Israel successfully being thwarted by Israel, the U.S., Saudi Arabia, Jordan and France. Israel responded with a limited, precise attack on a key radar facility, which has subsequently reduced tensions. In the wake of these events, congress passed a $95-billion military aid package for Ukraine, Israel, and Taiwan.

- We have made significant adjustments to the We now see economic growth remaining more resilient over the next couple of years and inflation proving slightly more persistent. We are still looking for the Fed to ease this year but now look for just two quarter-point cuts (September and December) followed by two more in early 2025. Long-term rates are expected to remain higher over the forecast period, although they should ease slightly this summer on softer economic data and slightly lighter Treasury issuance, thanks to stronger tax receipts.

Views on the economy have changed considerably over the past month. Economic growth has proven stronger than expected, while inflation remains too high and has proven more persistent. Attitudes hardened following a larger than expected increase in the Consumer Price Index for March, which saw both the headline and core CPI rise 0.4% and marked the third consecutive higher-than-expected CPI report. Many forecasters either pushed out the timing when they believed the Fed would begin to cut interest rates or removed any cuts from this year entirely. We still believe the Fed will cut the federal funds rate twice this year, with the first quarter-point cut coming in September and a second coming at the December FOMC meeting.

Most key economic reports continue to show the economy growing solidly. Nonfarm employment posted another outsized gain, with employers adding 303,000 jobs in March and job growth for the prior two months being revised slightly higher. The household employment data were also strong, with hours worked and average hourly earnings slightly topping expectations. The unemployment rate fell 0.1 point to 3.8%. Employers have added an average of 276,000 jobs a month over the past three months, which is well above the 244,000 jobs added per month over the past year.

Strong employment numbers are becoming routine. Increased immigration and an easing in work-permit restrictions are boosting hiring in occupations that have faced difficulty restaffing since the pandemic. Hiring continues to be skewed toward less skilled positions in health care, leisure and hospitality and state and local government. The strength in payrolls has bolstered personal income growth. Wages and salaries rose 0.7% in March and climbed at a 6.4% annual rate during the first quarter, fueling strong gains in consumer spending.

Within the GDP report, consumer spending rose a bit differently. Expectations for Q1 GDP growth jumped following a much stronger than expected retail sales report, which showed core retail sales surging 1.1% in March and rising at a 3% pace in the first quarter.

The apparent strength in consumer spending had pulled estimates for Q1 GDP growth to around 3% and the widely followed Atlanta Fed GDPNow projection was at 2.7% prior to the advance release of first quarter real GDP growth. Reports on industrial production and new home sales also boosted expectations, with manufacturing output rising amidst higher light vehicle assembles.

With everyone geared up for another red-hot report, first quarter GDP turned out to be a dud. Real GDP rose at just 1.6% annual rate, the slowest pace since the second quarter of 2022 when economic growth temporarily throttled back after surging when following the re-opening of the economy. The Q1 shortfall was mostly due to a widening in the nation’s trade deficit, which sliced 0.9 percentage points off growth. Export growth slowed, while imports ramped up. Business inventories also grew more slowly, slicing 0.4 percentage points off growth, and federal government spending fell, reflecting the lull in military aid to Ukraine. Consumer spending rose at a solid 2.5% pace, with all the growth in services. Goods spending declined at a 0.4% pace.

The financial markets reacted harshly to the GDP release, with bond yields surging and the stock market selling off. The markets were fixated on the combination of weaker headline GDP growth and higher inflation. The GDP deflator rose at a 3.1% pace in the first quarter, up from a 1.9% pace in the prior quarter. The PCE deflator rose at a 3.4% pace, while the core PCE deflator – the Fed’s preferred price measure — rose at a 3.7% pace, up from 1.8% and 2.0%, respectively, in Q4. A handful of analysts even raised the prospect of stagflation.

Surprises in quarterly GDP growth are not unusual. International trade and inventories, which account for the bulk of the shortfall in Q1 growth, are two of the hardest variables to estimate, particularly for the Advanced report. The widening in the trade deficit makes intuitive sense, as the stronger dollar reduces the price of imports to domestic buyers and makes US exports more expensive to overseas buyers. Trade will add little to growth over the balance of this year but should not be a significant additional drag either. Moreover, a stronger dollar should hold down import prices and help restrain inflation.

The continued slowdown of inventory building also makes sense, as goods consumption has been soft for the past year and half, leading to a decline in orders and output. Most of the first quarter’s weakness occurred at the start of the quarter, with spending on durables tumbling 2.7% in January and spending on nondurables declining in both January and February. In contrast, spending on durable goods rose solidly in February (1.4%) and March (0.9%) and spending on nondurables jumped 1.3% in March. Overall spending on goods rose 1.1% in March, matching the rise in core retail sales. The rebound in goods spending suggests orders and output will rise a bit more rapidly in the coming quarters. Inventories, which have subtracted from GDP growth the past two quarters, should add to growth later this year.

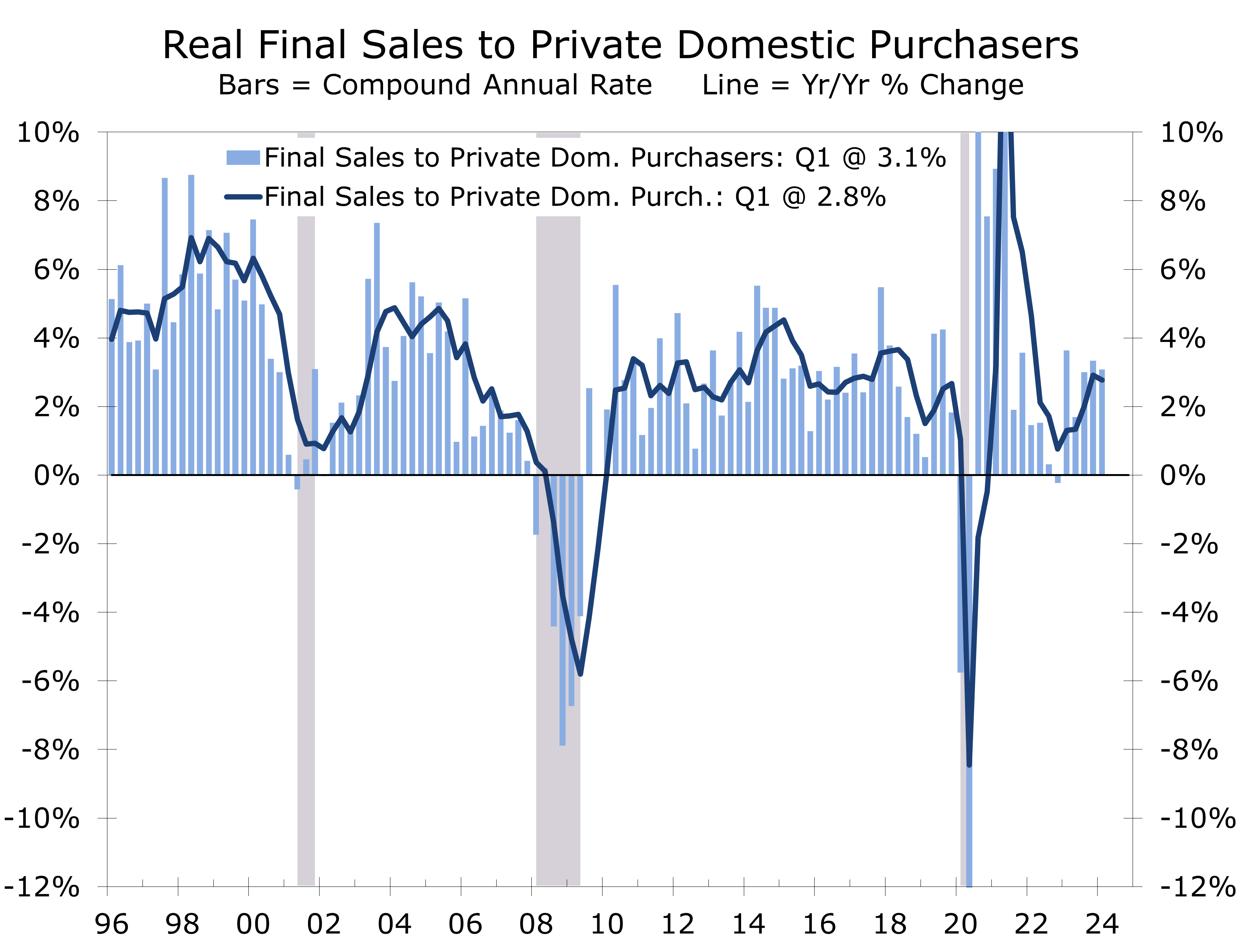

As far as fears about stagflation are concerned, we have often noted that final sales to private domestic purchasers, or core GDP, is the best way to measure the economy’s underlying momentum. This measure is the sum of consumer spending, business fixed investment and home building. Not only does this measure exclude the volatile trade and inventories component but, by focusing on the private sector, zeroes in on the part of the economy where monetary policy has the most influence. Core GDP grew at a 3.1% annual rate during the first quarter and has risen 2.8% over the past year. Moreover, core GDP has risen at better than a 3% pace in four of the past five quarters, indicating the economy still has strong momentum.

Rather than stagnate, we see economic activity accelerating in the current quarter and remaining strong through the end of the year. Overall personal consumption ended the first quarter on a high note and will grow at better than a 2% pace, even if consumer spending is unchanged in April, May, and June. Early Nowcasts estimates for second quarter GDP, peg growth at well over 3%. We raised our estimated for Q2 GDP growth to 2.9%.

Not only have we raised our estimate for second quarter GDP growth, but we see meaningful upside risks to subsequent quarters. The long drawdown in inventories has brought inventories back in line with their historic norms and led to a modest rise in orders for consumer goods and business equipment. One area where this is becoming apparent is light vehicle assemblies, which are ramping up. Moreover, the Q1 lull in military aid to Ukraine that restrained federal spending will reverse in the current quarter. Federal pump priming may add to growth in other ways, as money is finally flowing from the CHIPS and Science act, which will bolster construction spending and equipment purchases.

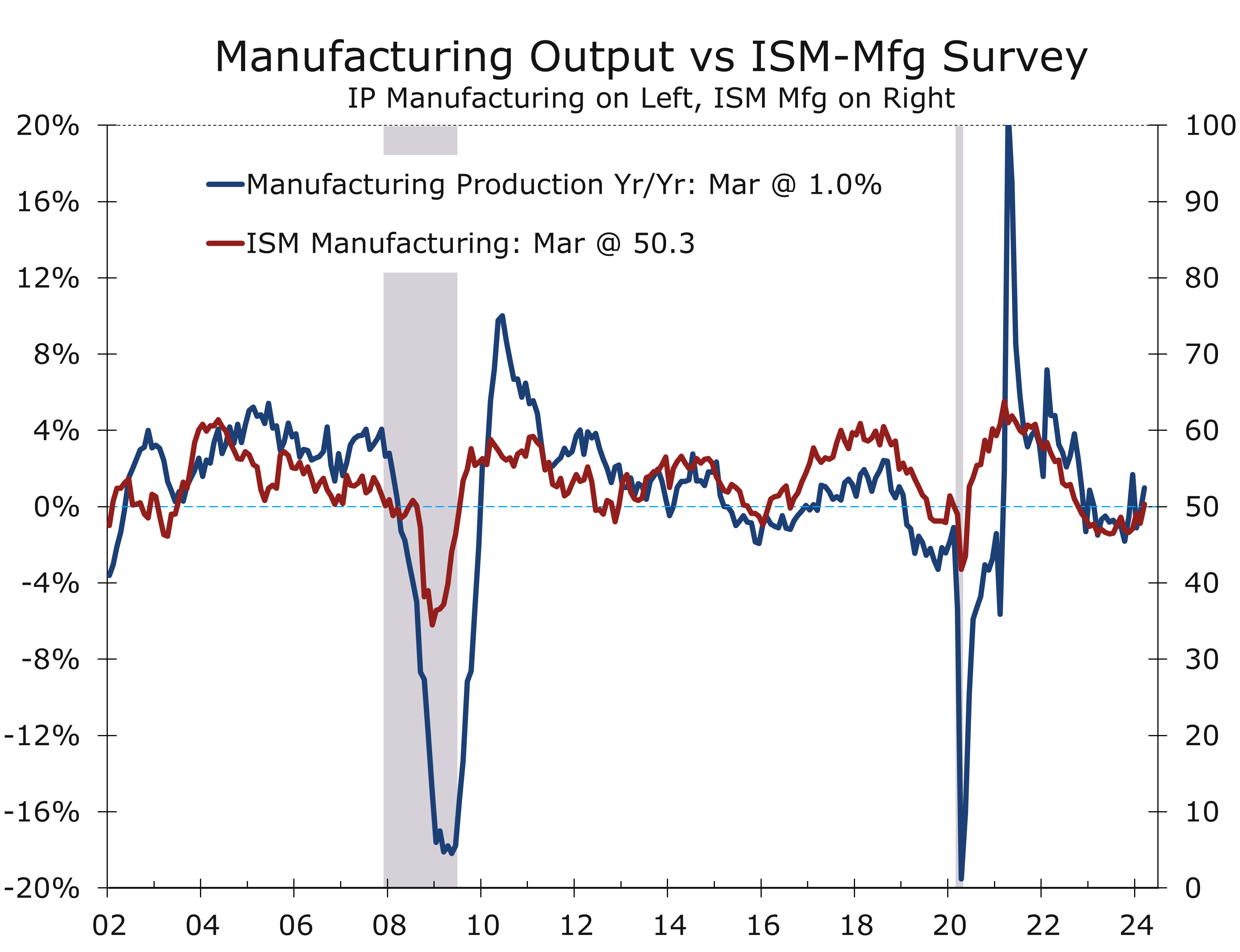

We may be on the verge of a resurgence in manufacturing along the line we saw in the latter part of the last decade. The ISM-Manufacturing Index, which tracks the breadth of the strength or weakness in the factory sector, rose back to 50.3 in March, marking its first reading above the key 50 break-even level since September 2022. The recent improvement in the ISM index was driven by increases in production and new orders. Customer inventories are also reported to be low, which means orders and output will likely rise further. Manufacturing employment, however, will take longer to improve.

While manufacturing accounts for a smaller share of economic activity, it still provides the cyclical impulse to the broader economy. An improvement in manufacturing activity leads to a larger increase in overall activity. Manufacturing output rose 0.5% in March following a 1.2% rise the prior month and is now 1% higher than it was a year ago. We expect output to strengthen further in coming months, driven primarily by rising motor vehicle assemblies, and increased output of other assorted consumer goods, tech hardware and defense and aerospace products. The one downside to an improving manufacturing sector is that past rebounds have tended to be associated with higher inflation. The Fed has tended to hike interest rates following past mid-cycle manufacturing rebounds (the second half of the 1980s, 1990s and this past decade).

While it has been a momentous month, we do not believe the inflation picture has changed all that much. The upside surprises to the CPI and PCE deflator were less than a tenth of a percentage point and may have been augmented by seasonal factors. There has been a tendency for price indices to register larger gains in the first half of the year than in the second half and this anomaly has intensified since the pandemic.

We have long noted it would be difficult to bring inflation down to 2% on a sustained basis without enduring a recession. The post-pandemic economy has been difficult to read, as massive supply-chain disruptions have gradually eased but massive fiscal stimulus aimed at boosting the economy from the pandemic has steadily intensified. While fiscal stimulus has many goals, including reducing the threat of climate change, providing resilience for critical global chains and promoting national defense, one overriding goal is to avoid a repeat of the slow recovery from the Global Financial Crisis, which was in-part due to constraints on federal spending.

The amount of fiscal stimulus in the pipeline – American Rescue Plan, CHIPS and Science Act, Infrastructure Act, Inflation Reduction Act — is enormous and is the primary reason economic growth has mostly surprised to the upside in recent years. The arrival of so much fiscal stimulus late in the business cycle, when the economy was already at full employment, is also why inflation has proven so persistent and will continue to do so. Moreover, massive fiscal intervention in the economy always breeds malinvestment and inefficiency that will weigh on productivity growth for years to come and will be difficult to reverse. This is why we have long felt that, without a recession, inflation will not likely return to the Fed’s 2% goal on a sustained basis until 2026.

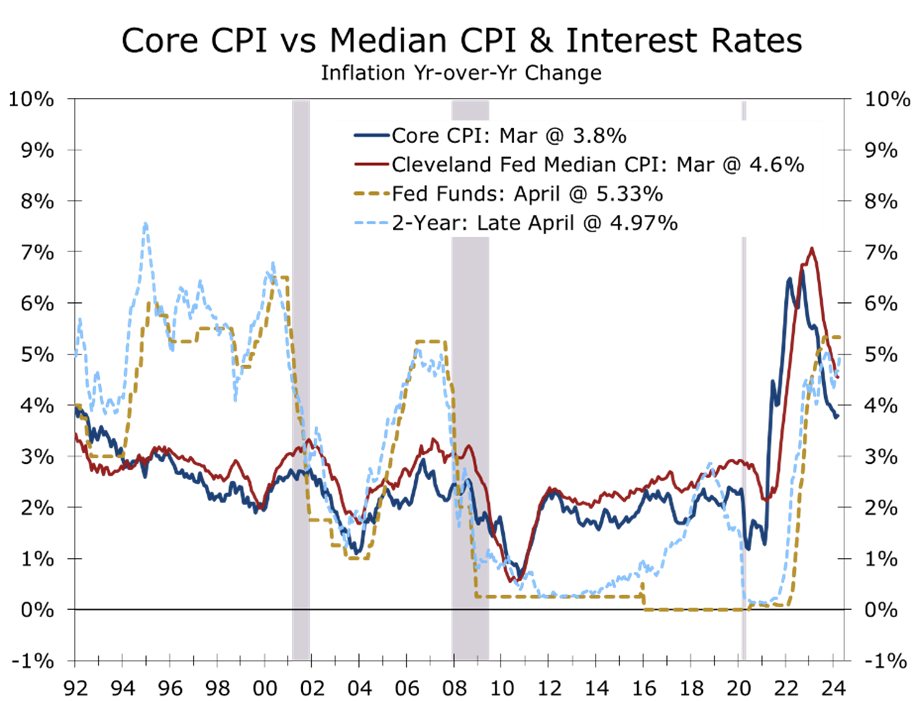

While 2% inflation may be a way off, the Fed should still be able to lower interest rates. The core PCE deflator – the Fed’s preferred price measure — topped out two years ago at 5.5% and has risen just 2.9% over the past year. As we have pointed out previously, however, the core prices measures, which exclude only food and energy prices, provide an exaggerated view on how fast inflation has come down due to the enormous swings in prices for a handful of items, including new and used light vehicles, health care, and residential rent. This is why we prefer measures such as the Cleveland Fed median CPI or trimmed mean CPI, which provide a better indication of how inflation is moderating in an overall sense. The direction and timing is roughly the same, but the magnitude of improvement has been much less by these more accurate measures.

The 2% handle on the core CPE deflator and expected continuing deceleration should provide the Fed enough confidence to begin reducing the federal funds rate by September. By then, the core PCE deflator should be nearing 2.5%, and economic growth should be slightly slower. We expect nonfarm employment growth to slow to around 160,000 per month leading up to the September FOMC meeting, and the BLS should provide an early estimate of annual benchmark revisions in line with recent QCEW data trends.

Lowering interest rates in an election year always sparks concerns about Fed independence. Delaying rate cuts when they are necessary, however, also puts the Fed’s independence into question. Monetary policy operates with a long lag, so the Fed must be preemptive. We now expect just four quarter point cuts over the next year and expect the Fed to adopt neutral bias after that – meaning their next move could be up or down.

We have also raised our forecast for long-term rates over the forecast horizon, reflecting slightly stronger economic growth and continued massive funding needs for the US Treasury. Those funding needs may ease a bit this spring, allowing the yield on the 10-Year Treasury Note to fall back to 4.50%. We look for long-term rates to remain around 4.50% throughout the forecast period. This merely brings long-term rates back into the range they have averaged since 1990, a period in which inflation was lower than what is currently projected.

The economy should adjust reasonably well to the higher interest rate environment. While the rate-lock effect on the existing home market will take a little longer to unwind, the new home market will continue to benefit as more buyers opt for a new home. The spread between mortgage rates and the 10-Year Treasury is also expected to narrow over the forecast horizon, gradually returning to its long-term norm by the end of next year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable.

© 2024 CAVU Securities, LLC

May 1, 2024

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000