Driving While Distracted Can Prove Perilous

An Unusually Divided Economy

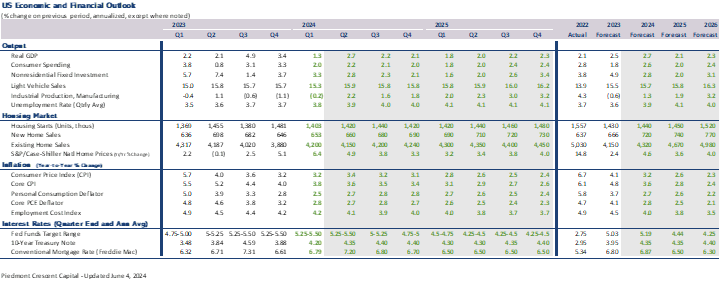

- The second revision to first quarter real GDP shows economic growth slowed more sharply than previously thought. Real GDP grew at just a 1.3% annual rate, down from a previously report 1.6% pace. Consumer spending on goods proved to be even weaker than first thought, declining at a 1.9% annual rate in Q1. Business fixed investment and residential construction were slightly stronger, however. Inventory building slowed slightly more than reported earlier, which should boost growth prospects for the second quarter.

- The softer GDP data are at odds with the strong job growth reported during the first quarter. Most survey data have been notably softer, however, and more closely align with recent announcements from major retailers, restaurant chains and grocers suggesting that middle and lower income households are tightening their belts. By contrast, upper end households continue to spend freely for services, experiences, and personal care.

- Slower economic growth should help tame inflation. We have been expecting inflation to cool off during the second half of this year. Several major retailers, including Walmart, Target and Walgreens have announced plans to reduce prices on many everyday items. Restaurants are also increasingly offering discounts to lure back more value-conscious consumers.

- There is also a growing geographic divide, with job growth notably slower in many of the nation’s largest metro areas. The latest Quarterly Census of Employment and Wage data show notably slower job growth in many of the nation’s largest urban areas, which may become a political issue this fall. Politics remains the widest divide and Donald Trump’s conviction in Manhattan state court will likely harden attitudes of both sides, while increasing global geopolitical risks.

- We continue to look for GDP growth to moderate in the second half of this year, as businesses and consumers pull back on capital spending and big-ticket purchases ahead of the November election. The labor market should move further into balance, with hiring moderating across most industries. We look for the Fed to cut the federal funds rate a quarter point in September but expect Treasury yields to decline only modestly reflecting persistent large budget deficits.

Economic activity has been confounding through the first half of 2024. Following a string of stronger employment gains and robust retail sales reports, economic growth turned out to be much weaker than expected, with the revised data now showing real GDP grew at just a 1.3% pace during the first quarter. Conditions were not nearly as weak as the headline data suggests, however, as private final domestic demand – the sum of consumer spending, business investment and residential construction – rose at a 3.1% pace, which is roughly in line with the prior two quarters.

One of the more confounding aspects of the current economic environment is the persistently low levels of consumer sentiment and business confidence amidst seemingly solid economic growth. Consumer sentiment and Small Business Confidence remain at levels more commonly associated with recessions, even though real GDP—the broadest measure of economic activity—has grown 3% over the past year and the unemployment rate has remained below 4% for the past two years. Various explanations for this discrepancy have been offered, ranging from consumer views being tainted by political bias to a hangover from the pandemic.

We do not see anything sinister behind the split in consumer confidence. Economics is simply common sense made difficult. The survey data largely reflect common sense views, while the hard data come from incomplete data sets that are often revised repeatedly. By contrast, common sense—and most measures of consumer and business confidence—tend to hold near their original readings. Some of the strongest short-term relationships between confidence measures and hard economic data come from comparisons of irrefutable measures, such as swings in gasoline prices. The idea that this relationship would hold constant while biases are present elsewhere in the same data set is simply not credible.

There are some real issues with the soft data. Survey responses have fallen considerably since the pandemic, and many surveys have switched from telephone to computer-based methods. The pandemic itself also led to wide swings in various confidence measures. Relief payments caused a huge spike in confidence measures, as did initial news about a vaccine. Business surveys, such as ISM and NFIB, were significantly impacted by supply shortages, leading to unprecedented swings in supplier deliveries and new orders, which are now settling.

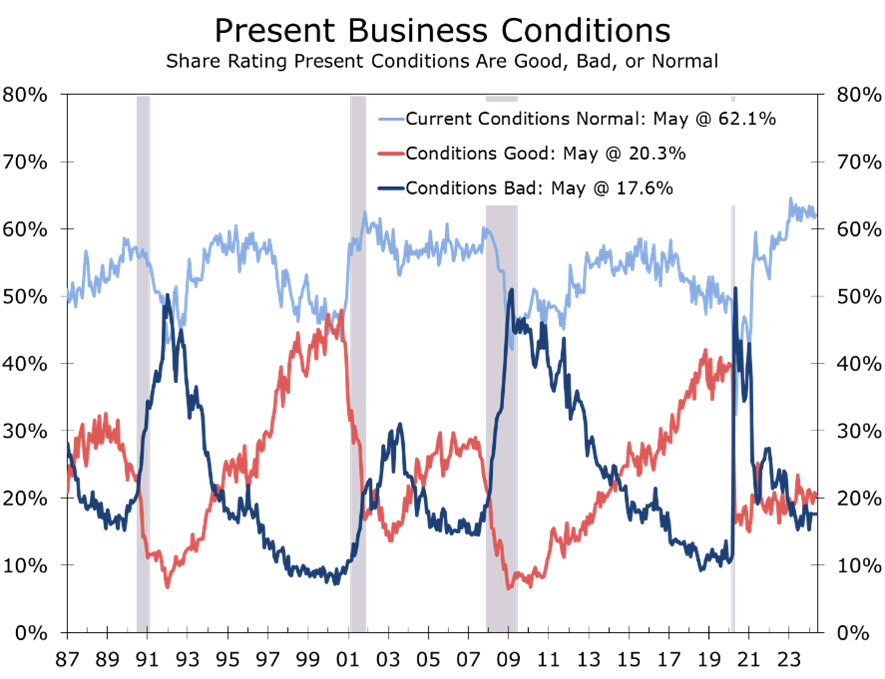

More recently, the survey data suggest the economy is stagnating. Much of this stagnation results from a decline in the proportion of consumers rating current economic conditions as ‘bad’ and a rise in those reporting conditions as ‘normal’. While overall, slightly more consumers rate current business conditions as ‘good’ rather than ‘bad’, the share rating current conditions as good is about half its pre-pandemic level, while the share rating conditions as bad is nearly one-and-a-half times higher. This assessment seems appropriate with the unemployment rate near its pre-pandemic level, but inflation considerably higher and the data closely resemble the Misery Index, which is the sum of the inflation rate and unemployment rate. The share rating conditions as normal is well above the highs seen in prior business cycles and is notably different from prior cycles.

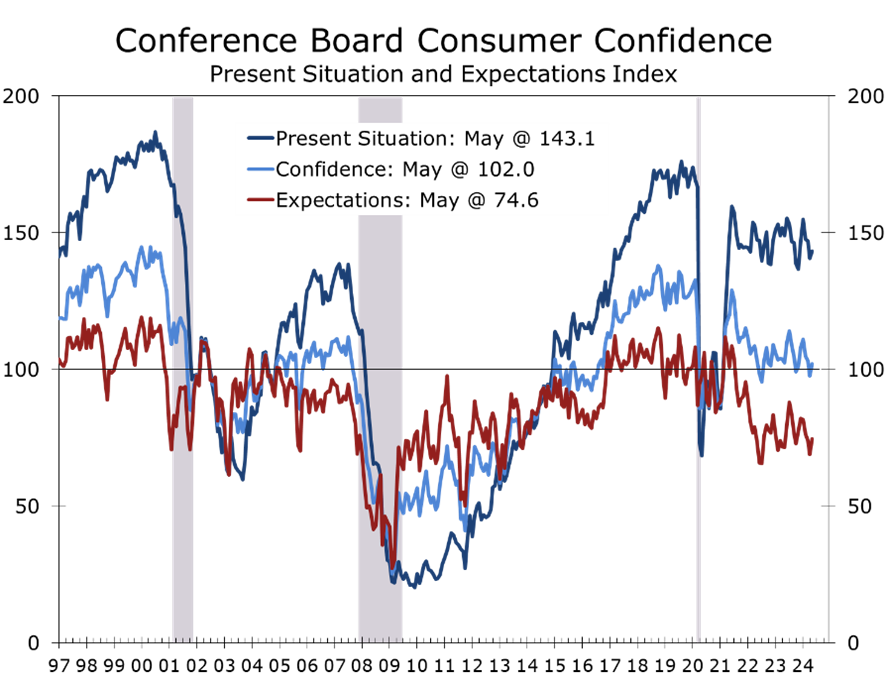

The Consumer Confidence Index is comprised of five questions—two on the current state of the economy and three on the economy’s ‘future prospects’, or six months ahead. In addition to consumers’ views on current business conditions, their view on the current state of the labor market remains unambiguously positive. The share of consumers who believe jobs are ‘plentiful’ (37.5%) vastly outnumbers those who believe ‘jobs are hard to get’ (3.5%). Despite this advantage, consumers’ assessment of the current economic environment, which rose 2.5 points in May to 143.1, remains 26.2 points below its pre-pandemic level.

While consumers remain relatively optimistic about the present economic situation, they are deeply concerned about the economy’s future prospects. The expectations series is derived from three questions about the economy’s future prospects: an assessment of future business conditions, labor market conditions, and income prospects for the next six months. The expectations series rose 5.8 points in May but remains a significant 33.5 points below its pre-pandemic level and is now at a level, 74.6, that is typically seen only in recession periods. When asked about the likelihood of a recession within the next 12 months, 69% of consumers, up 4 points from April, said a recession was either ‘somewhat or very likely’.

Consumers’ lingering caution is evident in other surveys, including the University of Michigan Consumer Sentiment Survey, Gallup’s long-running most important problem survey, and most notably in a recent Guardian/Harris poll, which found that 56% of consumers feel the economy is currently in recession. The preponderance of survey evidence suggests a significant gap between solid economic data and individual perceptions of the economy.

One variable every survey shows as the top concern for consumers is the persistent rise in prices, particularly for everyday items such as groceries, gasoline, and housing. While the rate of inflation has moderated, the cumulative price increases since the pandemic are taking a toll on consumer finances. Grocery store prices are 26% higher than they were prior to the pandemic, while gasoline prices are up 39%. Apartment rent is up a cumulative 21%, and mortgage rates and financing costs for new and used vehicles have more than doubled. As a result, families earning the median income or less, which is more than half the country, are being squeezed and are making difficult choices on what to cut from their budgets.

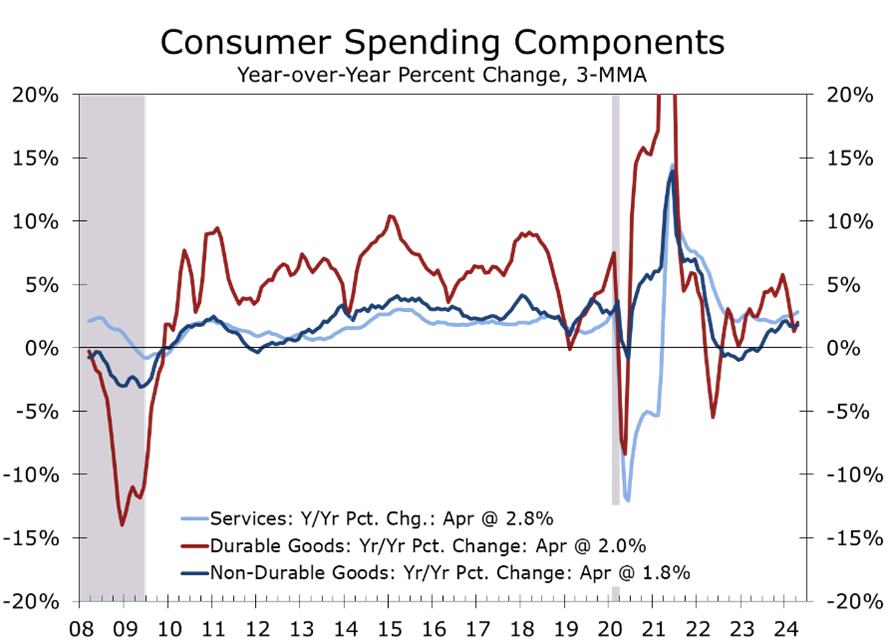

The squeeze on household budgets has become increasingly evident in consumer spending data. Estimates for first-quarter retail sales were revised down sharply, and overall consumer spending, adjusted for inflation, rose at just a 2.0% annual rate. Moreover, all of that increase came from services, which climbed at a 3.9% annual rate. Spending on goods fell at a 1.9% pace, with outlays for durable goods declining at 4.1% and spending on nondurables, the majority of which are everyday items, falling at a 0.6% pace.

The pullback in consumer spending continued into the second quarter, with real personal consumption declining 0.4% in April. Spending on goods retreated further, with spending on nondurable goods tumbling 0.5% and spending on big-ticket items declining 0.1% in inflation-adjusted terms. Services outlays inched up just 0.1% after inflation, marking the smallest increase in eight months.

The weakness in goods spending reflects some underlying deterioration in household finances. The saving rate has fallen to just 3.6%, well below its long-run average of 5.8%. Delinquency rates on credit cards and car loans have risen in recent months, particularly among younger households.

Overall, balance sheets remain healthy. Household wealth has soared to new heights due to rising home values and a buoyant stock market. The economic split is significant. Homeowners who financed during the ultralow interest rate era have locked in housing costs and benefited from the strong run-up in home prices since the pandemic. Higher interest rates have also boosted interest earnings for upper-income households. For those earning the median income or less, it is a different story. These households are more likely to rent and less likely to own significant financial assets. Becoming a homeowner has become more difficult due to soaring home prices and higher mortgage rates.

The economic divide is affecting consumer spending. Families earning the median income or less are cutting back on non-essential purchases, impacting sales of goods and restaurant dining. Such cuts are necessary as groceries, housing, and transportation account for a larger share of their budgets. Spending on goods has decreased in three of the past four months and is now lower than it was at the start of the year. Upper-income households are faring much better. While middle and upper-income households account for the bulk of overall consumer spending, a larger share of their spending is on services, including travel, leisure, entertainment, wellness, and health care. Services outlays have held up well, rising in three of the past four months.

The financial divide among households is evident at major retail and restaurant chains. Walmart, Target, and Walgreens are cutting prices on thousands of everyday items, while McDonald’s, Wendy’s, and Taco Bell are expanding their value meals. This trend is visible at nearly all retailers and restaurants targeting middle- and lower-income consumers, leading to sales declines and plans to close underperforming locations. Cutbacks are particularly notable in areas where the minimum wage has increased substantially.

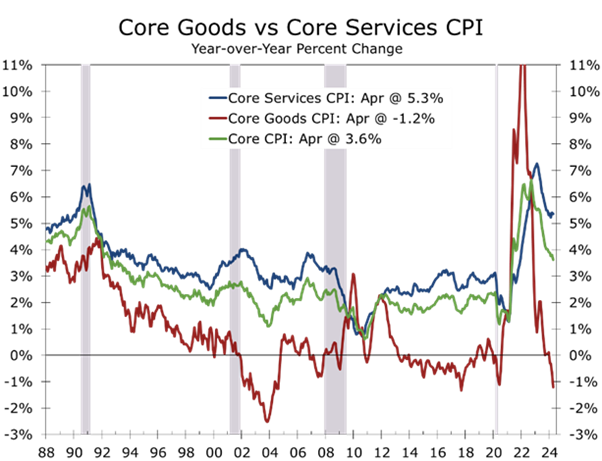

Increased discounting by retailers and restaurants will likely have only a modest impact on overall inflation. Goods, including food and energy, make up only 35% of consumer spending, with core goods accounting for less than 19% of the Consumer Price Index. Inflation has not primarily been driven by goods prices. Post-pandemic car prices spiked due to supply shortages and a shift from urban centers to car-dependent suburbs, but these shortages have since been resolved, and new and used vehicle prices have moderated.

Food price inflation has also subsided, although most households are unlikely to notice. Food prices have risen just 1.1% over the past year but remain roughly 25% higher than they were prior to the pandemic. While Walmart, Target, and several major grocery chains have committed to slashing prices on many widely used grocery items, food prices remain vulnerable to various external shocks. Labor costs at grocery stores have also risen along with prices, or even more in many markets, which will limit the extent of price markdowns.

Energy prices also show some signs of moderation. Gasoline prices have risen just 1.2% over the past year, and oil prices have slipped back below $80 a barrel in recent weeks. While energy production has ramped up in the United States, prices still remain vulnerable to geopolitical events around the world, as well as weather conditions closer to home. There is less capacity to accommodate a supply shock today. Strategic oil and gasoline stockpiles were tapped to help alleviate prices ahead of the midterm election and have not been replenished.

Core services prices remain the most challenging aspect of the inflation outlook. Much attention has been focused on housing costs, where asking prices for new rental apartments have fallen amidst an onslaught of new apartment completions. However, higher home prices and higher mortgage rates are keeping renters in place, and rents for renewals are still rising solidly. Price increases for many other key services, including health care, motor vehicle insurance, and admissions to concerts and sporting events, also remain problematic.

Inflation is expected to continue moderating as slowing economic growth cools off demand. Our forecast now calls for real GDP growth to rebound to a 2.7% annual rate. Consumer spending is packing much less punch than previously thought, and the housing market is struggling with higher mortgage rates. With home sales on a slower track, spending on furniture, appliances, and home furnishings is lagging, adding to the challenges retailers face from inflation-weary consumers. Business fixed investment is also expected to moderate this summer, as uncertainty about the presidential election causes businesses to hold off on capital projects.

While growth is slowing, Fed Chair Jay Powell made it clear that he does not see stagflation as a threat, and neither do we. Inflation should gradually decelerate but remain above the Fed’s target well into 2026. This will not prevent the Federal Reserve from cutting interest rates but will limit the extent of cuts outside of an outright recession. We expect the Fed to cut rates twice this year, with cuts in September and December, and anticipate two more quarter-point cuts in 2025. After that, with the economy still at full employment, we expect the Fed to hold the federal funds rate steady at a level roughly equal to nominal GDP growth.

The combination of full employment, near-potential real GDP growth, large federal budget deficits, and gradually decreasing inflation will keep long-term interest rates above 4%. We see upside risk to the 10-Year Note, particularly if the economy reaccelerates after the election. The FOMC has been steadily increasing its estimate of the long-run federal funds rate and we expect it to eventually rise from its current 2.60% to 3.25%, which would push the 10-Year Note to 4.80% with a normal upward-sloping yield curve.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable.

© 2024 CAVU Securities, LLC

June 4, 2024

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000