Strong Equipment Investment, Solid Spending Blunt Much of the Trade Drag

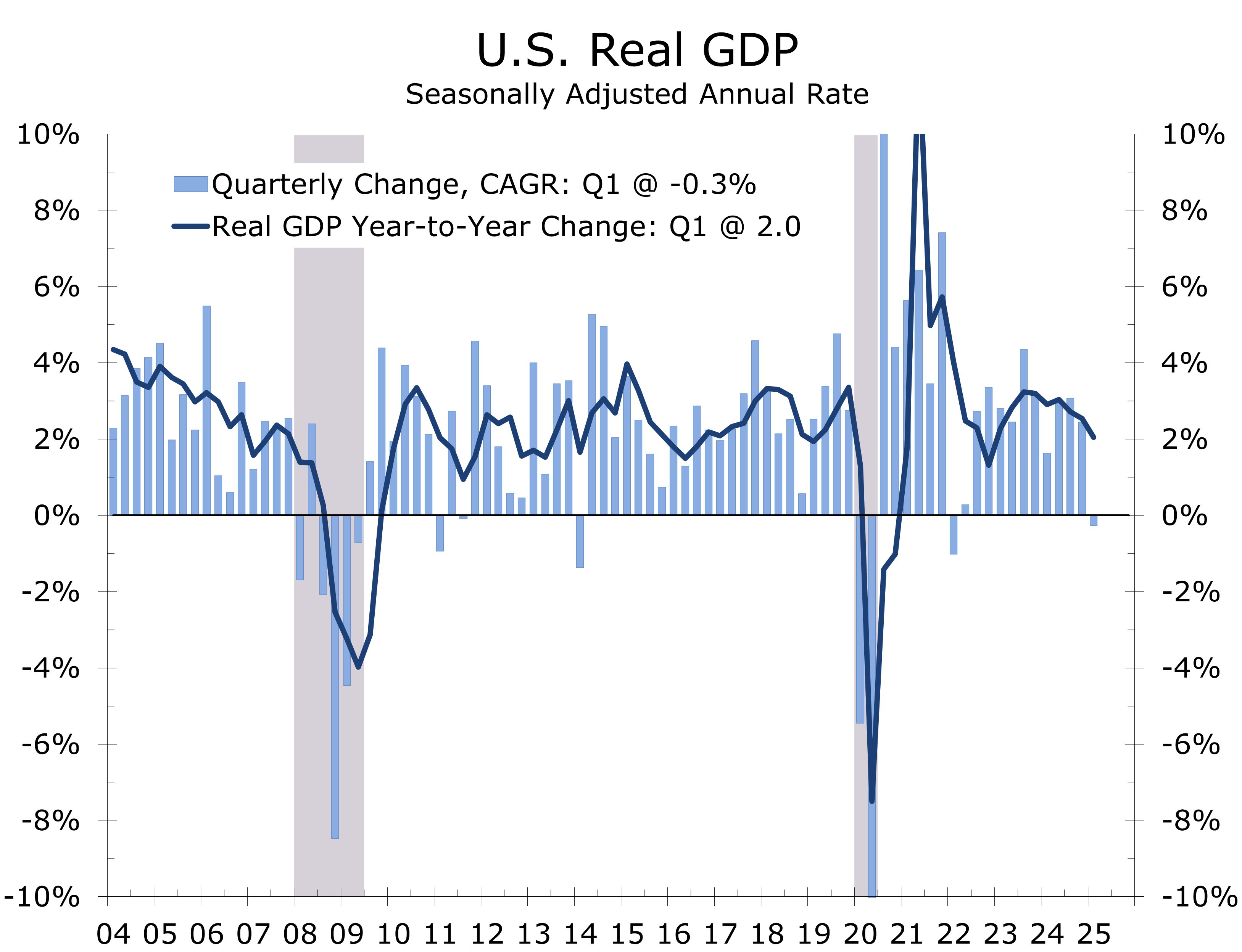

- Real GDP declined at a -0.3% annual rate in Q1, in line with expectations for a modest contraction.

- Net exports subtracted a record 4.8 percentage points from growth, as firms front-loaded imports ahead of tariff hikes.

- “Core” GDP—comprising personal consumption, business fixed investment, and residential investment—rose at a solid 3.0% pace.

- Equipment investment surged 22.5% annualized, driven by a historic 70% spike in information processing equipment and a rebound in aircraft production.

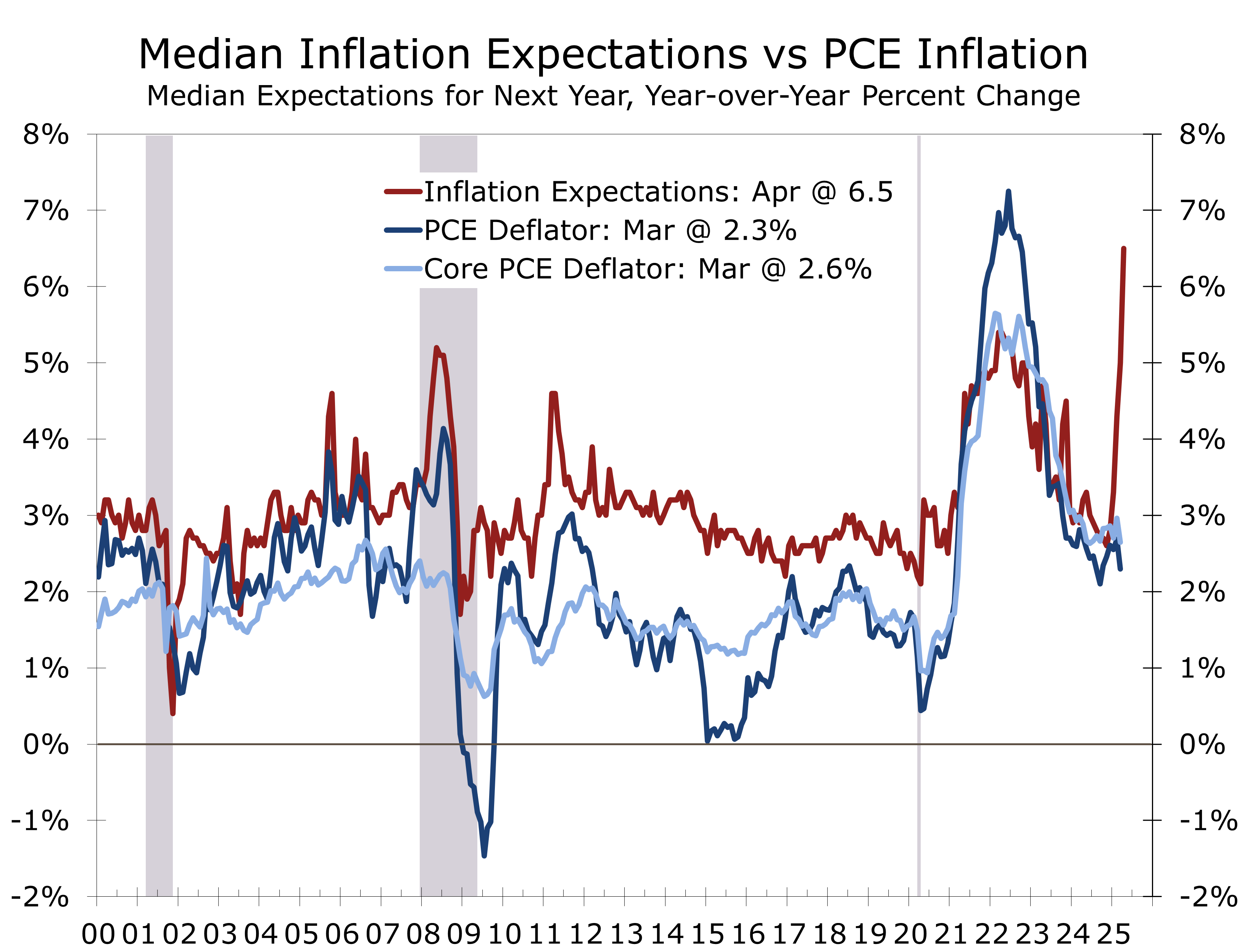

- The GDP price index rose at a 3.7% annualized rate, while the Core PCE deflator rose 3.5%—hotter than expected.

- Q1’s GDP contraction was more noise than signal. One-off drags—import distortions, government pullbacks, and anomalies—obscured a solid 3.0% gain in private domestic demand. Strong investment and firm inflation support the Fed’s “higher for longer” stance, but also suggest a slowing, not stalling, economy.

U.S. real GDP contracted at a 0.3% annualized rate in the first quarter of 2025, just below the consensus forecast of a 0.2% decline. While the negative headline figure may stir recession concerns, the underlying components of demand suggest a more mixed picture, with resilient consumer activity and a notable surge in business investment pointing to continued economic momentum.

The largest drag on growth came from international trade. Net exports subtracted 4.8 percentage points from GDP—the largest drag since at least 1947—as businesses aggressively pulled forward imports in anticipation of scheduled tariff increases. This inventory build-up was not fully matched by concurrent increases in consumption or domestic stockpiles, a common quirk in early GDP estimates that was greatly exaggerated by the huge tariffs announced this year that were announced in early April.

A deluge of imports in the first quarter drowned out otherwise strong underlying growth.

Domestic demand remained firm beneath the surface. Personal consumption expenditures grew at a 1.8% annual rate, notably slower than Q4’s 4.0% gain, but still respectable given the weather-related disruption to January retail sales, the drag from the Los Angeles wildfires, and the exceptionally late Easter holiday.

Business fixed investment jumped 9.8% in Q1, driven by a 22.5% surge in equipment investment. Within that, information processing equipment soared 70%, adding a full percentage point to GDP — the largest contribution on record — likely reflecting major corporate investments in generative AI infrastructure. Transportation equipment also rebounded, rising at a 13% pace, as Boeing resumed normal operations following a resolution to the machinists’ strike.

The AI boom led to a surge in investment in information processing equipment in Q1.

Residential investment provided a modest boost, rising at a 1.3% pace. The gain largely reflects the large pipeline of projects currently underway. Together, personal consumption, business fixed investment, and residential construction, comprise final private domestic demand, or what we often refer to as “core” GDP. Core GDP rose at a 3.0% annual rate, matching its pace over the past year. Core GDP is the portion of economic activity most influenced by monetary policy and remains firmly expansionary.

Government spending was a mild headwind. Federal outlays fell at a 5.1% annual rate, reflecting an 8% pullback in defense spending following a strong finish to 2024. State and local spending was essentially unchanged.

Inflation came in hotter than expected. The GDP price index rose at a 3.7% annualized rate, with firm gains in consumer goods (+3.6%) and residential investment (+3.9%). Core PCE inflation—the Fed’s preferred gauge—ran at a 3.5% pace, while the year-over-year GDP deflator rose to 2.6% from 2.4%.

Tariffs have led to a spike in inflation expectations that might become a self-fulfilling reality. While market-based measures remain stable, surveys from the University of Michigan and the Conference Board have surged. Worries about tariffs might cause consumers to pull purchases forward and drive prices higher.

This puts the Fed in a tight spot. The labor market appears to be cooling, with ADP data coming in weak and wage growth easing in the Q1 Employment Cost Index. If labor trends continue to slow, the Fed might need to cut rates this summer despite sticky inflation.

Recession risks remain elevated amid trade policy uncertainty. Still, the Atlanta Fed’s GDPNow model sees 2.4% growth in Q2, driven by consumer spending and business investment. Trade and inventories are expected to subtract from growth, but if domestic demand holds, Q1 could mark only a brief dip in an otherwise subdued yet resilient expansion.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 30, 2025

Mark Vitner

704-458-4000