Capital Carries the Cycle

- The U.S. economy is slowing, not sliding into recession. Growth is decelerating as hiring cools and consumers become more selective, but underlying demand remains intact.

- The expansion is being carried by capital, not consumption. Private fixed investment in AI infrastructure, power, advanced manufacturing, aerospace and defense, and life sciences remains the primary growth engine.

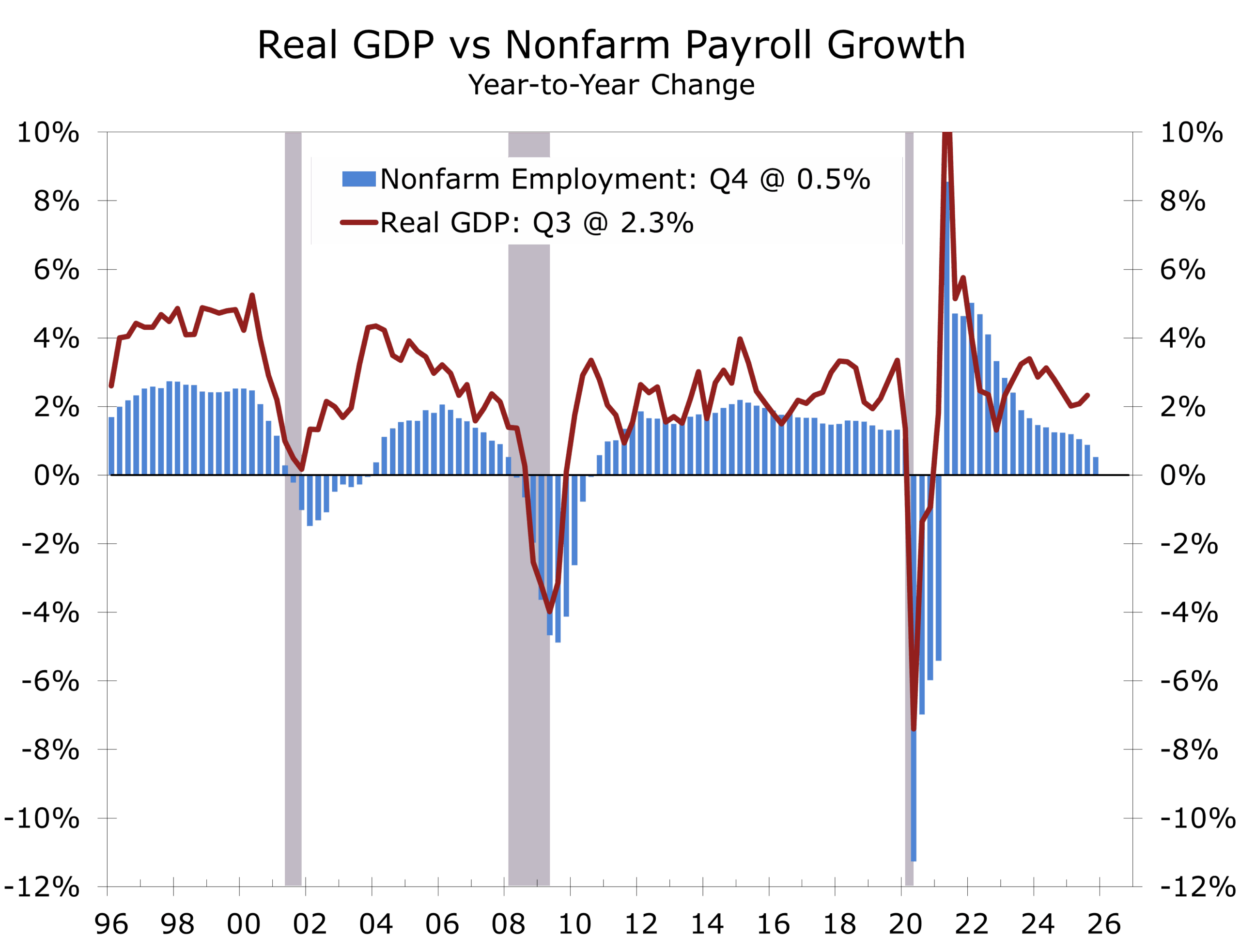

- Productivity is rising as payroll growth fades. Firms are producing more with fewer workers, signaling a job-light, capital-intensive phase rather than cyclical retrenchment.

- Policy uncertainty is raising the bar, not stopping investment. Capital is still being deployed, but with greater emphasis on scale, execution, and long-term returns.

- Charlotte is positioned to outperform. Its financial services depth, energy and infrastructure advantages, logistics connectivity, and expanding technology ecosystem align well with a capital-heavy, productivity-driven cycle.

A Productivity-Led Expansion

As the U.S. economy enters 2026, growth is cooling but not cracking. The December CAVU Compass captures this phase well: an economy pulling in different directions, with consumer spending becoming more selective, hiring slowing sharply, and policy uncertainty remaining elevated. Beneath those surface frictions, capital spending continues to anchor the expansion. For technology companies, that distinction matters. This is not a demand-driven slowdown. It is a transition toward a more capital-intensive, productivity-led cycle.

This is not a demand problem; it is a productivity shift. The economy is producing more with fewer new workers.

The backbone of the cycle remains private fixed investment. AI infrastructure, power and energy systems, aerospace and defense, biopharma, and advanced manufacturing continue to attract capital at scale. These are not short-cycle bets tied to consumer sentiment; they are long-duration investments driven by returns, resilience, and geopolitical recalibration. Arguments that growth would falter “without AI” miss the point. Capital would still flow to its highest risk-adjusted return. AI is simply where capital is flowing today, as expected risk-adjusted returns remain unusually attractive and AI use shifts from experimental to everyday applications.

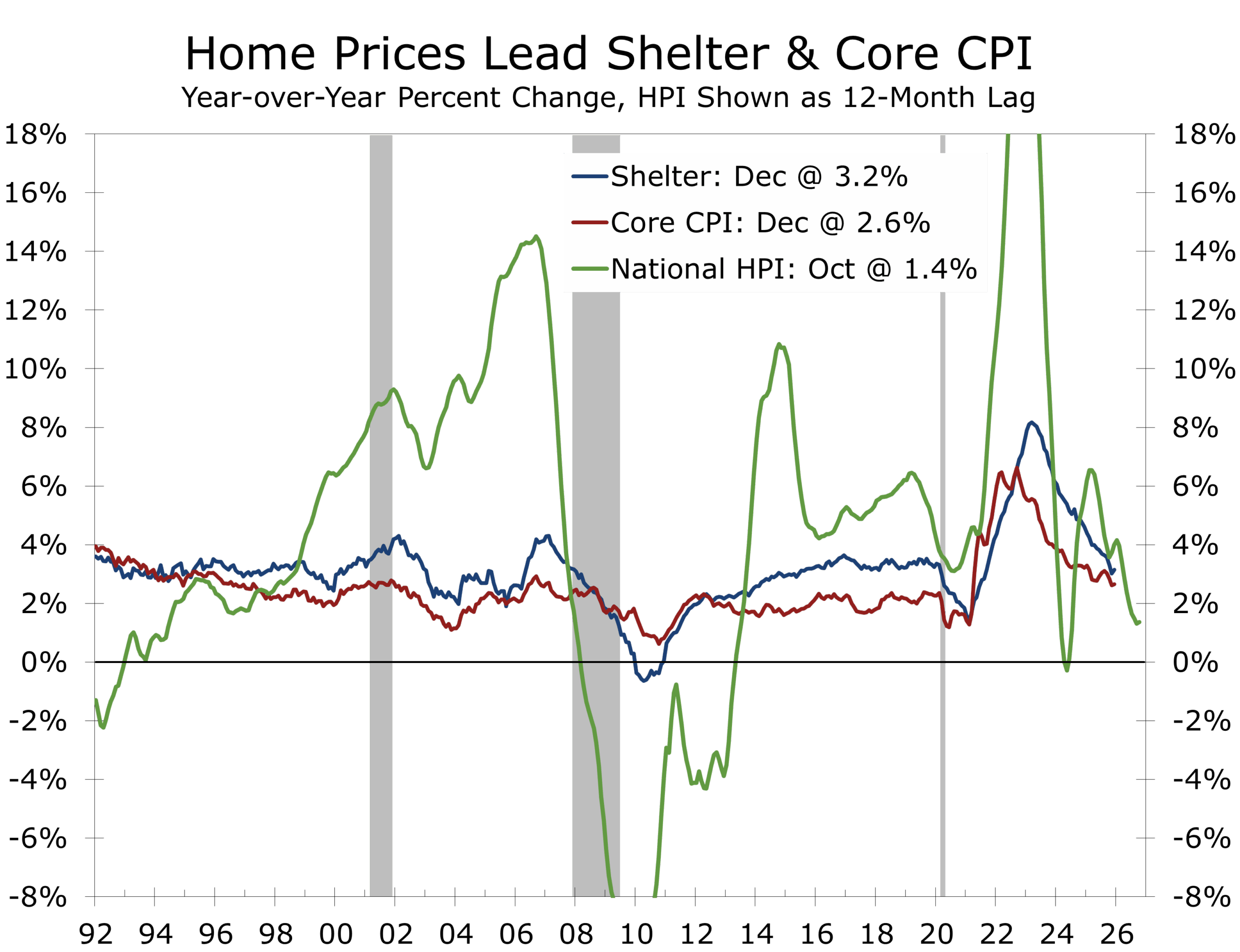

Inflation dynamics reinforce this constructive backdrop. Tariffs briefly interrupted the disinflation trend in 2025, but their inflationary impulse has largely passed. More importantly, shelter inflation—which accounts for roughly 44% of core CPI—is now decelerating as home prices flatten and rental supply rises. Our 2026 forecast calls for shelter CPI inflation to slow to 3% or less, pulling core inflation back under 2.5% by year-end. For technology firms, this matters less for headline inflation and more for margin stability and planning certainty.

Labor-market dynamics further underscore the shift underway. Early 2026 is shaping up as a near-jobless expansion, with payroll growth hovering near zero before improving later in the year. Demographics, tighter immigration enforcement, and slower labor-force growth are restraining hiring even as output holds up. Employers are not aggressively cutting staff, but they are increasingly reluctant to add headcount. This divergence is not a warning sign; it is a signal. Demand for automation, AI orchestration, workflow optimization, and data-driven productivity tools tends to rise precisely in this environment.

Businesses are increasingly worried about being left behind as competitors implement AI more effectively.

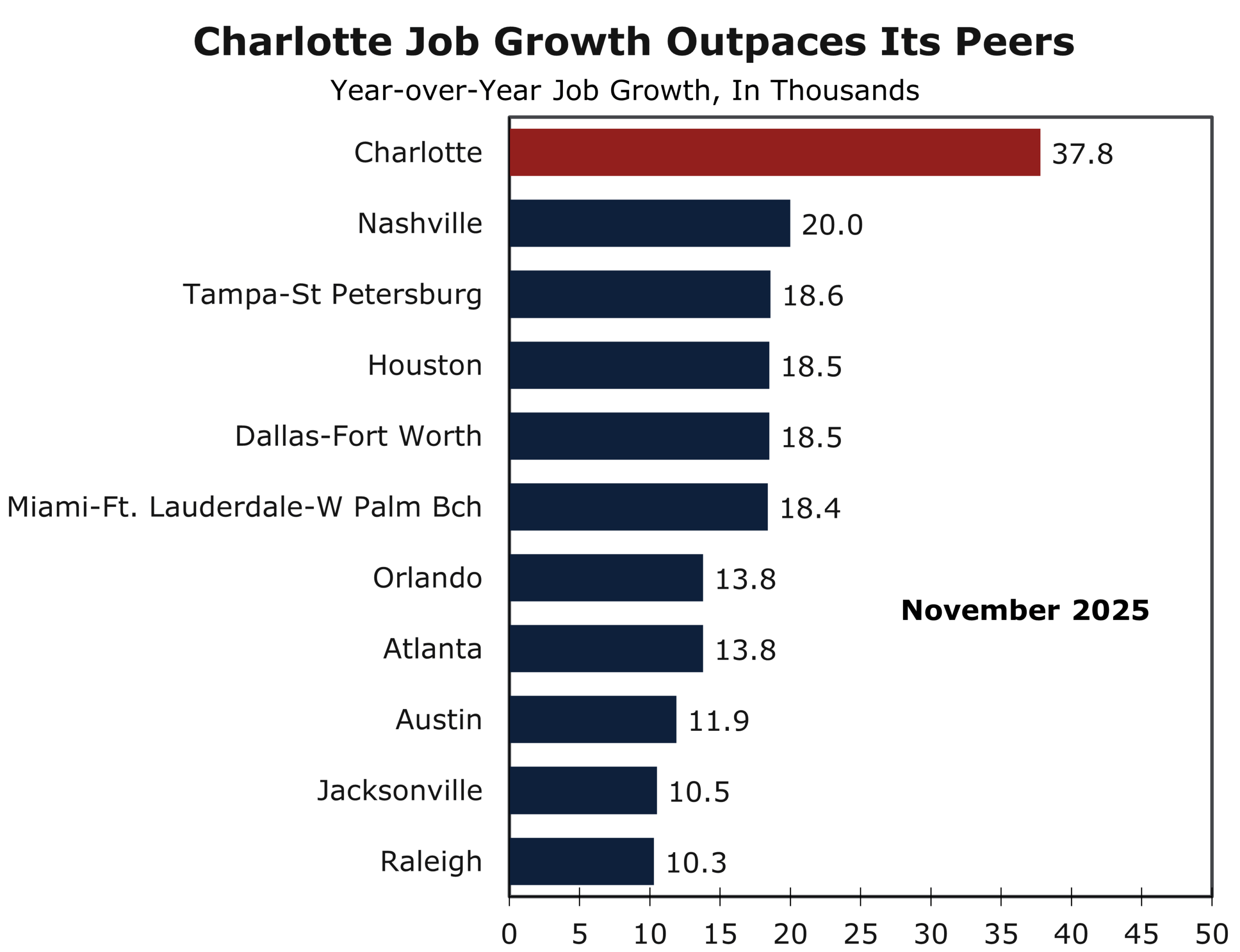

Regional divergence is widening as these forces play out, and this is where Charlotte clearly separates from many of its peers. While job growth has slowed in metros such as Raleigh, Nashville, Tampa, and Austin, hiring accelerated in Charlotte over the past year. Nonfarm employment in the Charlotte metro area increased 2.7% over the past 12 months, as employers added nearly 37,800 net new jobs. That performance places Charlotte among the fastest-growing large MSAs in the country, even as national hiring momentum cools. Net job creation also surpassed that of larger peer metros such as Atlanta, Dallas-Ft Worth, and Miami–Fort Lauderdale–West Palm Beach.

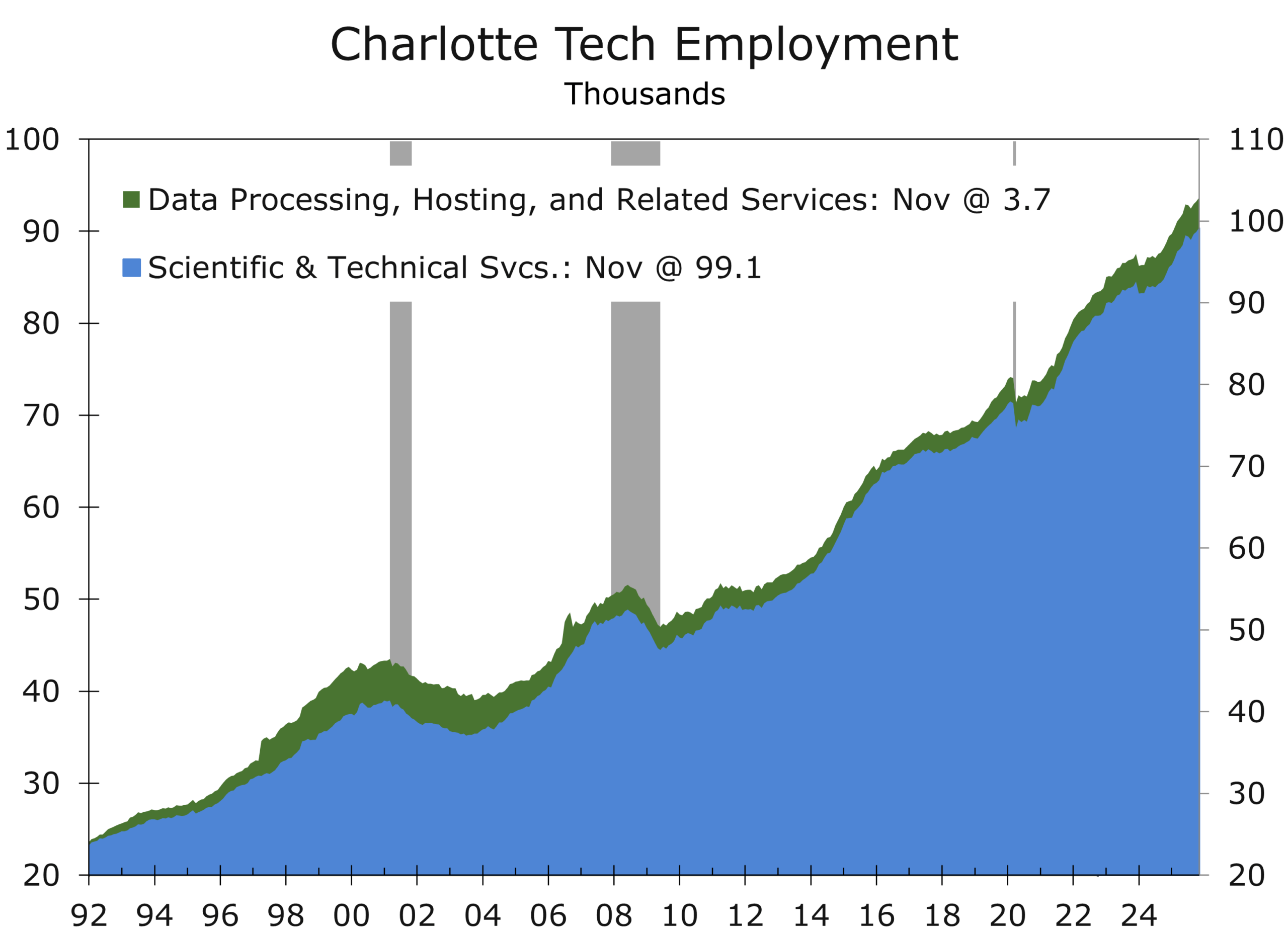

Charlotte’s strength reflects more than favorable timing. The region sits at the intersection of financial services, technology, healthcare, and logistics, supported by sustained population growth and rising capital inflows. Tech and healthcare hiring remain notable bright spots, while investments such as the Wake Forest School of Medicine; and more broadly, The Pearl innovation district, promise to further diversify the region’s economic base. Charlotte also continues to attract corporate and regional headquarters and scored a notable win by landing the new headquarters for Scout Motors. Unlike markets now confronting affordability ceilings and slowing migration, Charlotte continues to benefit from attainable housing, execution speed, and a growing talent pool.

Charlotte is accelerating while many peer tech metros are decelerating. Capital, people, and jobs continue to gravitate toward Charlotte.

While this report draws from discussions with leaders from Charlotte-area technology firms, its conclusions extend well beyond the tech sector. This is not a cycle defined by rapid hiring or outsized top-line growth; it is a capability cycle. Advantages will accrue to organizations that align with capital spending, invest in productivity-enhancing technologies, and operate in regions with durable execution capacity, such as Charlotte. If 2025 was the year the economy cooled without breaking, 2026 is shaping up to deliver growth with fewer workers, more capital, and increasingly calibrated policy. In that environment, discipline, scale, and execution will matter more than speed.

For Charlotte’s tech sector, 2026 is shaping up as a year of opportunity. Firms are accelerating the adoption of AI and automation to boost efficiency, while the sector continues to broaden beyond its historic dependence on the region’s large financial base. Healthcare, life sciences, and MedTech are emerging as particularly strong growth areas. Logistics, long weighed down by a protracted freight recession, is also positioned for a rebound, while financial services and FinTech stand to benefit from lower interest rates and an improving environment for lending and deal flow.

The broader economic outlook remains constructive. While job growth is likely to cool from the pace implied by preliminary data, the Charlotte region is still positioned to outperform the nation and most peer metros. The city’s core advantages remain firmly in place: a diversified economy, a high quality of life, and a well-located major airport hub that consistently ranks as one of the busiest in the world. Population growth continues to be fueled by domestic migration, led by inflows from the Northeast and Midwest, with rising contributions from other Southeast states—particularly Florida—as well as the West Coast. Charlotte also continues to rank among the top U.S. metros for attracting corporate and regional headquarters, reinforcing its long-term growth trajectory.

One of the questions we often get when speaking about the region’s economic performance is: Can this momentum continue, and what could trip Charlotte up? The answer to both is housing affordability. While home prices have risen in Charlotte, the region remains relatively affordable compared to its peers. As long as that remains true, the region’s competitive edge remains intact.

Charlotte is blessed with significant geographical advantages, including abundant land and water resources (including three lakes along the Catawba River). Most metro areas grow predominantly in one direction, typically to the north. In Charlotte, however, growth is roughly evenly split between the north and the south. Furthermore, the east (Cabarrus, Union, and Stanly counties) and west (Gaston and Lincoln) are currently the fastest-growing parts of the metro, benefiting from their own relative affordability.

A key reason these outlying areas remained accessible and affordable for so long is that Charlotte was one of the last major U.S. cities to complete a beltline expressway. The final leg of I-485 did not open until 2015, effectively “unlocking” vast tracts of land for development just as the national migration toward the Sun Belt accelerated. This delayed infrastructure has provided a critical safety valve for housing supply that many of Charlotte’s peers lack.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 9, 2026

Mark Vitner, Chief Economist

(704) 458-4000