PIEDMONT CRESCENT CAPITAL

A View from the Piedmont

Download the full report (PDF)

Last week’s holiday-shortened data flow reinforced a familiar but evolving narrative: the U.S. economy remains on a sound footing with resilient, if cooling, momentum, while geopolitics, the buildout of AI, and the structural shift toward electrification are reshaping relative advantages and investment opportunities. Markets digested a soft June jobs print, pragmatic signals from new Fed Chair Kevin Warsh at Sintra, further de-escalation on Iran, and the first signs of a modest rebound in residential investment. Primary dealer positioning in Treasuries continued to build, and the long-term Age of Electricity theme, highlighted in BCA Research’s latest special report, gained sharper focus amid AI-driven demand, a surprising June jump in EV sales, and ongoing grid constraints. We also take a step back this week, in our Piedmont Perspective, to consider what the primary season’s socialist wave says about an expansion that, so far, is being driven more by capital than by labor.

Key Economic Reports of the Week

A compact scorecard of the week’s major releases, with our one-line read on each.

| Report (period) | Reading | PCC read |

|---|---|---|

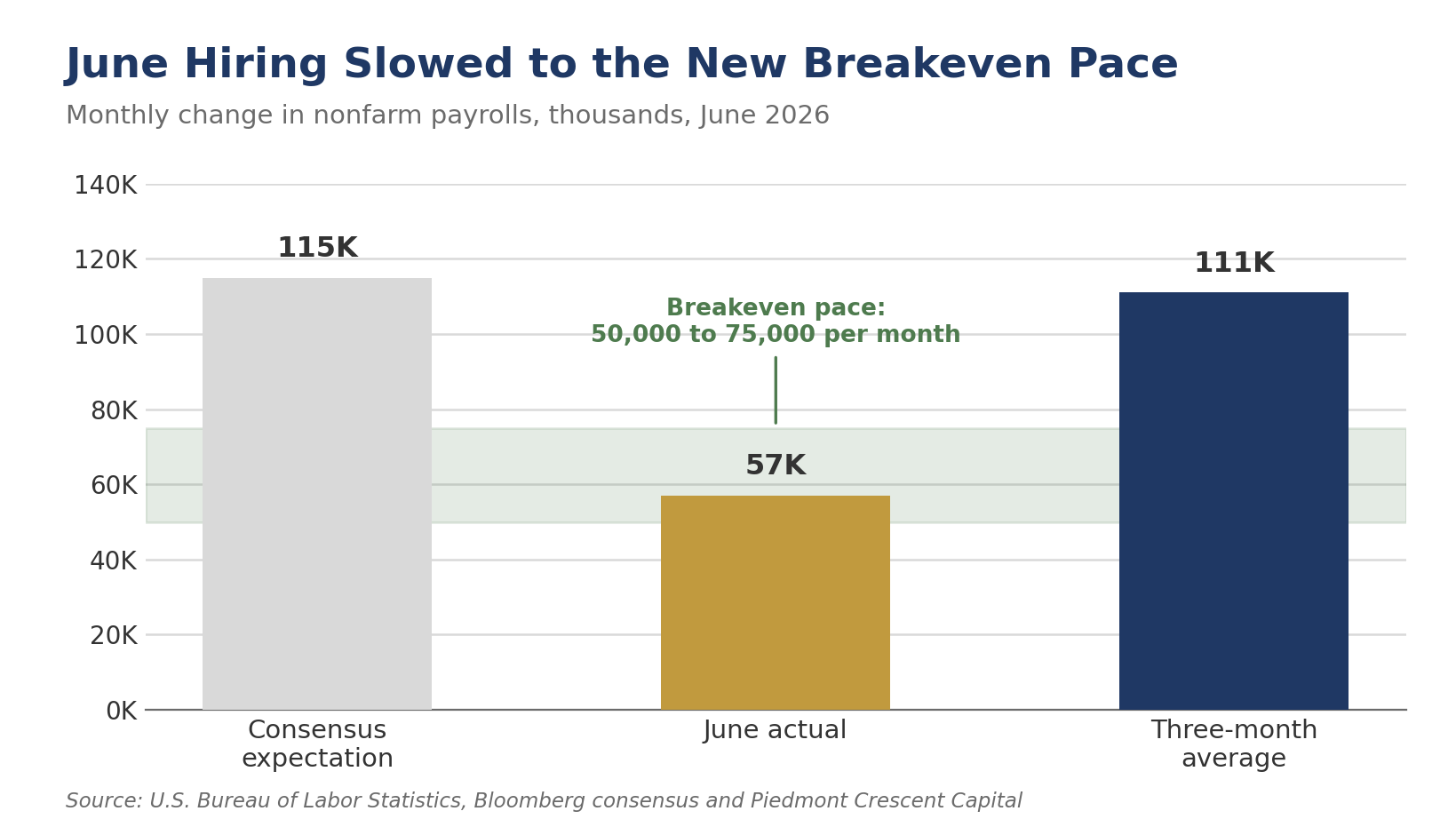

| Nonfarm payrolls (Jun) | +57,000 | Half of consensus, but the labor force fell 720,000; less slack than the headline implies. |

| Unemployment rate (Jun) | 4.2% | Lower, but on falling participation rather than stronger hiring. |

| ISM Manufacturing (Jun) | 53.3 | Sixth straight month in expansion; input-price index dived 9.1 points to 73.0. |

| ISM Services (Jun) | Due Jul 6 | May registered 54.5, a 23rd consecutive month of expansion; we look for confirmation. |

Also released: May construction spending (reviewed below) and a firmer late-June pace of vehicle sales, led by a jump in EVs.

The June ISM Manufacturing PMI, released July 1, fit our capital-led thesis. The headline eased to 53.3 from 54.0 but marked a sixth consecutive month of expansion, with new orders (56.0) and production (52.2) still carrying the recovery. Employment, by contrast, rose 1.1 points to 49.7 yet stayed in contraction for a 33rd straight month, the build-without-hiring pattern our productivity work anticipated: output rising on flat-to-falling hours is productivity, not weakness. The most telling line was on prices, where the input-cost index plunged 9.1 points to 73.0, its steepest drop since July 2022, as the Iran-war premium on oil and diesel receded, though 15 of 18 industries still reported higher costs. Lean customer inventories, at 42.3, point to further production ahead. The factory sector is not booming, but it is broadening, and its cost pressures are easing.

Labor Market: Fewer Workers, Not Fewer Jobs

The June Employment Situation report delivered a headline disappointment, but we read it as something more interesting than a labor market rolling over: an economy generating fewer workers, not fewer jobs. Nonfarm payrolls rose just 57,000, roughly half the consensus expectation, and April and May were revised down a combined 74,000. The unemployment rate nevertheless fell to 4.2%, but for a less obvious reason. The civilian labor force shrank by 720,000 in June, pulling participation down to 61.5%, its lowest level since early 2021. When labor supply is barely growing, it takes only 50,000 to 75,000 jobs a month to hold the unemployment rate steady, and June’s gain landed squarely in that band. The three-month average of 111,000 remains comfortably above breakeven.

The details support the more constructive reading. Leisure and hospitality shed 61,000 jobs, but the early Memorial Day pulled seasonal hiring into May, and the two months roughly net out; there were also fewer days between the April and May survey periods, which lifted the seasonal adjustment for May. The World Cup, which opened one day before the June survey week, is filling bars and restaurants across the country in the middle of the afternoon, though most of that activity shows up as longer hours rather than new headcount. Little of it came through in the June payroll count, which is why we are watching the July report closely. Meanwhile, manufacturing breadth quietly improved, with the factory diffusion index reaching its best level in more than a year and catching up to an ISM survey that has been in expansion all year. We see this as the early innings of the capital-led expansion broadening out, and we expect some follow-through in professional services in the coming months.

Average hourly earnings firmed to 0.3% for the month and 3.5% over the year. The gains were largest in financial services, information, professional services, and other services, which is not where the job growth has been. Our sense is that, with less turnover and fewer new hires, a more seasoned workforce is posting modest raises on a higher wage base, which lifts average hourly earnings more than the underlying pace of pay increases would suggest. That pace is not a source of fresh overheating pressure, but with underlying inflation still running near 2.9% on our preferred trend measure, neither is it yet consistent with a sustained return to 2%. The prime-age softness was concentrated in the 25-34 cohort, a detail we return to in this week’s Piedmont Perspective. The bottom line: the labor market has lost some luster but is not deteriorating, and the shrinking labor force means there is less slack behind the headline than the payroll number suggests.

Monetary Policy: Warsh Leans Pragmatic; Our Call Is Unchanged

Chair Warsh’s comments at the ECB Forum in Sintra, Portugal, were the week’s most market-moving policy development. He noted that inflation expectations and inflation risks have both come down over the past four weeks, gave renewed emphasis to the employment side of the dual mandate, and highlighted the potential medium-term disinflationary effects of AI-driven supply expansion. He also signaled openness to structural change through the new task forces on communications and real-time data. Forecasters responded by pushing out the timing of the next move: Oxford Economics now sees the next cuts in September and December of 2027, and the broader consensus has converged on no change in the funds rate for the rest of 2026. The Supreme Court’s decision preserving Governor Cook’s position bolsters institutional independence, though that fight will continue.

Our call is unchanged. We continue to expect no cut in 2026, with the next move more likely a hike than a cut, arriving in 2027 or early 2028 as stronger growth, coming at a time when the economy is already operating at full employment, bolsters wage gains, consumer spending, and corporate pricing power. This week’s news, a soft payroll print, falling energy prices, and a chair speaking to both sides of the mandate, extends the pause; it does not change the destination. The mid-July CPI report is the next big point of focus, with sharply lower gasoline prices widely expected to pull the headline into negative territory for the month. Rising memory prices are already reaching consumers, however, and could deliver an upside surprise in core goods.

Geopolitics and Energy: The Fever Has Broken, for Now

Progress on the Iran front continues to deliver relief. The U.S.-Iran memorandum of understanding provides a 60-day ceasefire window for negotiations, with extensions likely, and Strait of Hormuz traffic is recovering across bulk, container, LNG, and crude categories, though normalization remains incomplete. Crude benchmarks have retreated sharply from conflict peaks, and regular unleaded gasoline has fallen below $4.00 per gallon for the first time since late March, down 60 cents in four weeks. Risks remain, including the possibility of renewed hostilities closer to the November midterms and a lingering geopolitical premium, but the worst of the price shock appears to be behind us.

The Age of Electricity: China’s Scale, America’s Innovation

BCA Research’s lead special report provides the week’s most forward-looking thematic anchor. The world is entering an Age of Electricity, driven by transport, industry, buildings, and above all AI, with global electricity demand projected to rise roughly 40% by 2035 and the binding constraint shifting from generation to transmission, storage, and grid flexibility.

China’s advantages are structural: the world’s largest electricity system, an ultra-high-voltage transmission network, industrial power costs roughly 40% below Europe’s, and a planned grid and storage buildout on the order of RMB 8 to 10 trillion over the next five years. The United States counters with an innovation ecosystem that has thrived despite aging infrastructure and slow permitting, and data centers are the distinctive American demand driver, where the theme lands closest to home. The grid buildout is both an opportunity and a competitive pressure for the Carolinas and the broader Southeast, where utility capex plans, data-center recruitment, and manufacturing reshoring converge on the same constraint. Grid equipment, transmission, storage, nuclear-exposed utilities, and copper stand to benefit; we will return to the regional implications in upcoming client work.

Housing and Construction: A Modest Q2 Rebound

May construction spending left our Q2 tracking largely unchanged. Private residential investment is on track for an increase of roughly 1% at an annual rate, the first quarterly gain since late 2024, driven by home improvements, a pickup in existing home sales that is boosting brokers’ commissions, and a gradual recovery in single-family construction. Multifamily remains mixed, and the pipeline of both single-family and multifamily projects continues to wind down, trimming residential construction employment. Private nonresidential structures continue to contract, tracking a 4.7% annualized decline, weighed down by the long-running drop in factory construction. Data-center spending is surging and has been revised higher, but it represents less than a tenth of private nonresidential outlays; the larger AI-related dollars flow through equipment, software, and R&D. The slide in manufacturing construction appears to be tempering, however, and we are seeing gains in institutional projects and in some heavy energy and transportation infrastructure. Housing will struggle to replicate Q2’s momentum in the second half, as single-family builders work down a large stock of completed unsold homes against margin pressure and higher-for-longer interest rates. A modest rise in new home sales would set the table for residential construction in 2027.

Financial Markets and Positioning

Equities posted a constructive holiday-shortened week, with the Dow extending its winning streak to fresh records on the jobs-day relief rally, while the Nasdaq absorbed some chip-sector rotation following a strong second quarter. Primary dealers continued building fixed-income positions through late June, with Treasury holdings rising $23.1 billion to $515.6 billion, including another record in the long bond sector, while MBS holdings eased modestly. The positioning reflects inventory management, relative value, and expectations for a prolonged policy pause.

The Week Ahead: A Quieter Calendar, Loud Minutes

The data calendar thins out after a heavy stretch, and consensus figures below reflect market surveys rather than any single house. Monday brings the June ISM services index, the week’s marquee release; the services gauge held up at 54.5 in May, its strongest in three months, and consensus looks for a reading in the mid-53 to 54 area, still comfortably in expansion. Tuesday’s May trade balance is expected to show the deficit widening from April’s $55.9 billion as imports rebound, and Wednesday brings May wholesale inventories. Thursday rounds out the week with weekly jobless claims, seen near 220,000 after 215,000, and June existing home sales, where another gain would extend a tentative housing thaw. Friday has no major releases.

The main event is Wednesday afternoon’s minutes from the June 16-17 FOMC meeting. That meeting, Chair Warsh’s first, held the funds rate at 3.50 to 3.75 percent by a unanimous vote but paired the hold with a decidedly hawkish set of projections: the median 2026 dot jumped to 3.8 percent from 3.4 percent in March, flipping the implied path from a cut to a possible hike, with nine of eighteen participants placing at least one hike on the table and seventeen of eighteen judging the risks to inflation to the upside. We will read the minutes for how broadly that hawkish shift is held, how the committee separates the energy-driven part of inflation from the underlying trend, and for any detail on Chair Warsh’s communication overhaul, including the five new task forces and his decision to withhold a dot of his own. Little in the minutes is likely to disturb our house call of no cut this year, with the next move more likely a hike than a cut.

The speaking calendar reinforces the theme. Governor Waller appears Monday, and two voters, New York’s John Williams and Dallas’s Lorie Logan, speak Thursday. All three have leaned toward patience or caution of late, with Logan the most explicit that further tightening could prove necessary later this year if inflation does not resume its descent. We would treat any dovish surprise as the news, precisely because it would run against the grain the June meeting established.

THE PIEDMONT PERSPECTIVE | ABRIDGED

A Wake-Up Call

In the summer of 1991, a British band called Jesus Jones had the biggest song in America, and it was a song about watching history turn. “Right Here, Right Now” was written in the afterglow of 1989, as the Berlin Wall came down and hundreds of millions of people walked out of a failed economic experiment that had run for most of a century. Thirty-five years later, we find ourselves wondering where Jesus Jones is when we need them.

The Democratic Socialists of America are having their best election cycle in the organization’s history. On June 23, candidates endorsed by New York Mayor Zohran Mamdani swept their congressional primaries, unseating a five-term incumbent in Upper Manhattan. One week later in Denver, a 29-year-old democratic socialist toppled a congresswoman who had held her seat since 1997. A year ago the DSA counted two members of Congress; it is now on track for at least five, with roughly three dozen primary victories this cycle. This is no longer a New York story.

Step back from the primaries, though, and the national picture is ambivalence, not a groundswell. A late-January Pew survey found a 56 percent majority of Democrats neither like nor dislike leaders who call themselves democratic socialists; only 32 percent say they like them. And the affinity that exists runs upside-down, concentrated among affluent, college-educated, White, and politically engaged Democrats rather than the working-class base the ideology invokes. It is potent in a low-turnout urban primary and niche in the country at large.

We take the movement seriously because the grievances behind it are real, and our own research this week documents them. Our June employment report, “Fewer Jobs, Fewer Workers,” found the softness concentrated among workers aged 25 to 34, with the labor force shrinking and participation at a five-year low. Our companion report on the national capital cycle traced how narrowly this capital-heavy, employment-light expansion is concentrated by industry and by geography. For a young worker watching data centers rise while entry-level hiring stalls, the economy can feel like a party they keep seeing on social media but were never invited to, and that breeds resentment.

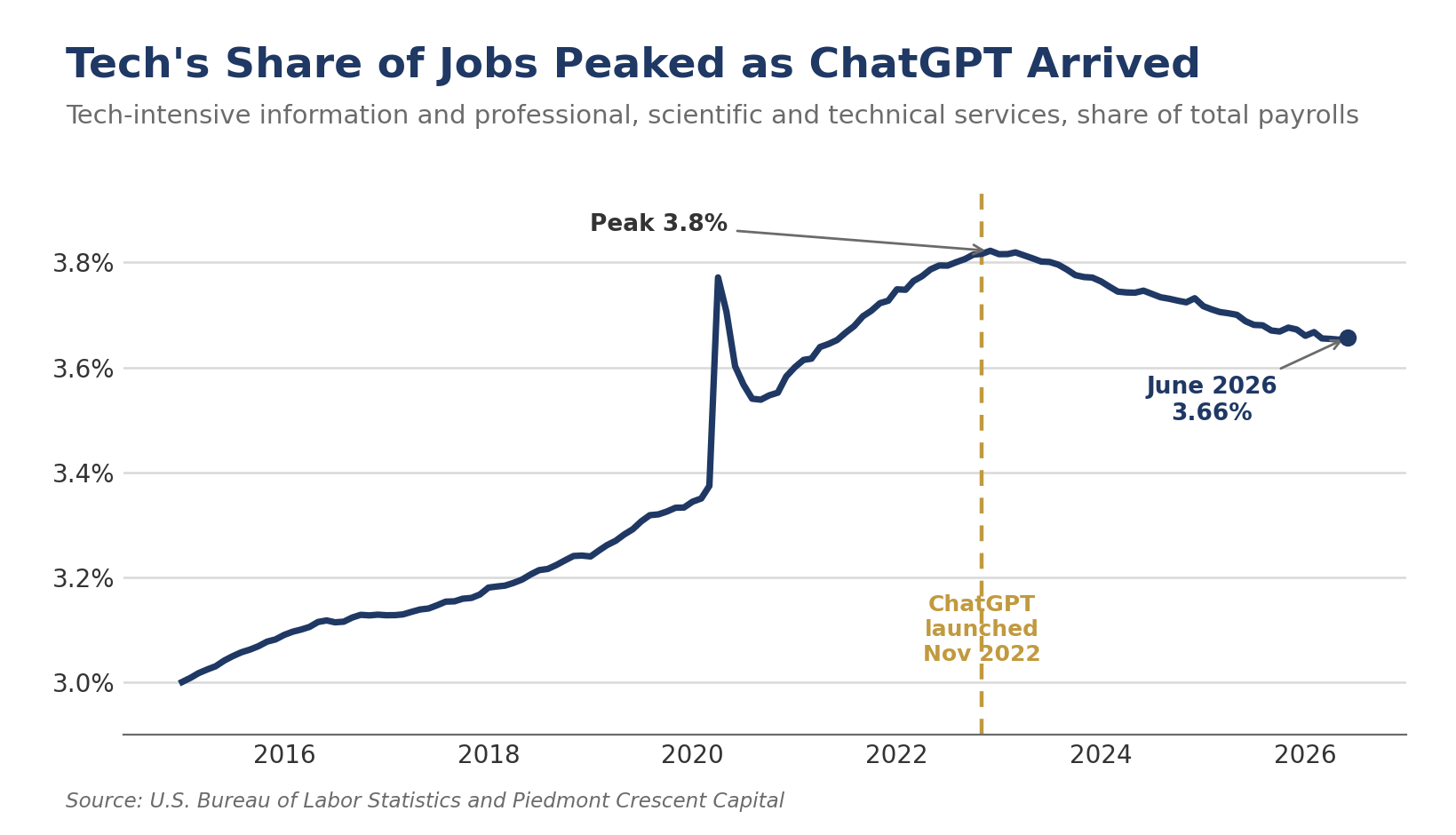

The frustration is legitimate. The prescription is not. Part of the current softness is AI itself. The tech-intensive share of employment climbed through the pandemic and peaked almost precisely as ChatGPT arrived in late 2022, and it has drifted lower ever since as firms learn to do more with the same headcount. We read that as a near-term adjustment, not a verdict. AI will be a powerful driver of growth and employment over time, and we expect that hiring momentum to become more evident in the second half of 2026.

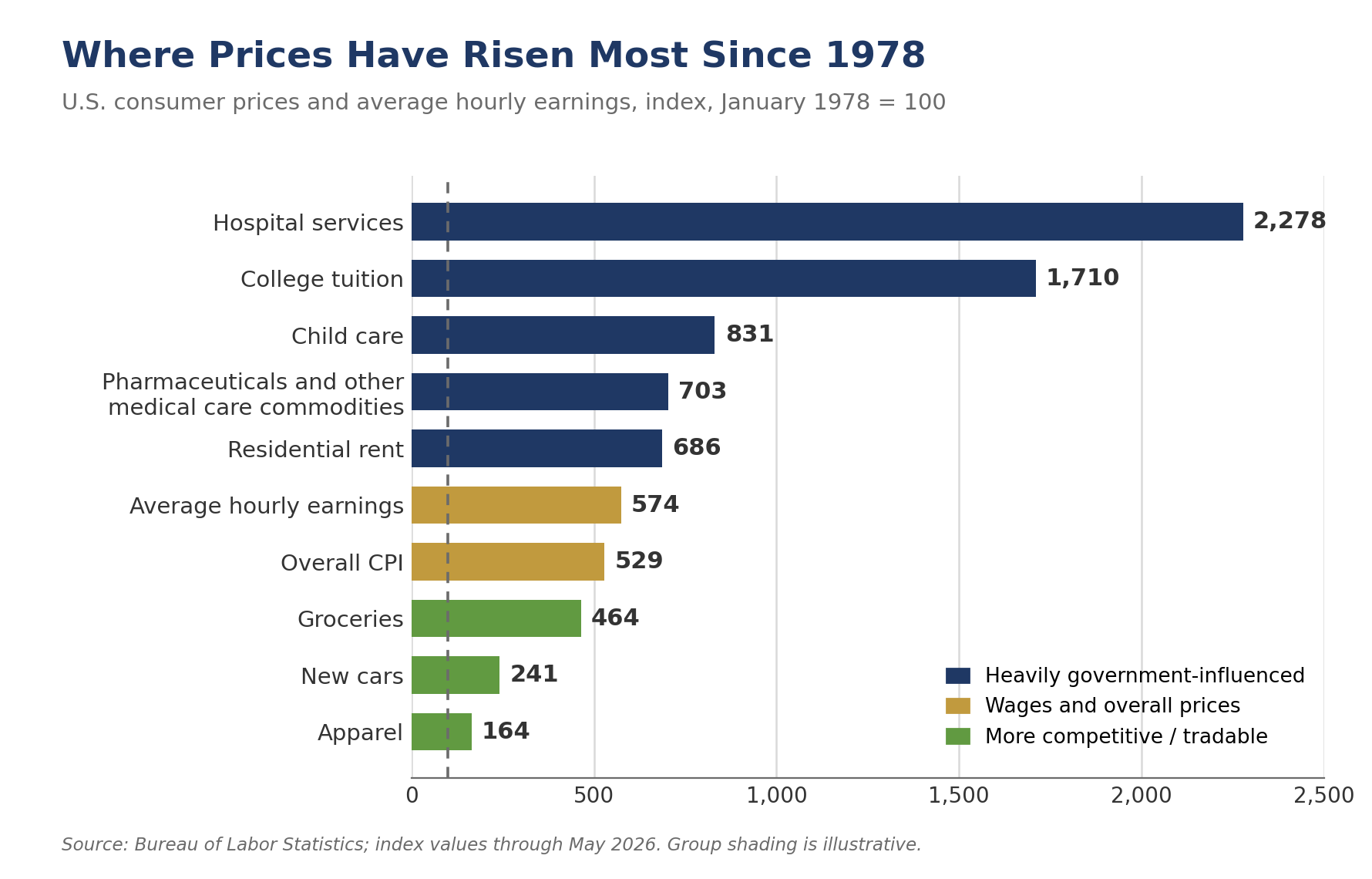

The second source of frustration is the affordability crisis. The steepest cost increases powering these campaigns are concentrated in housing, healthcare, and higher education, the three markets where government already does the most to underwrite demand and constrain supply. Since the late 1970s, prices in the most heavily managed sectors have risen several times faster than in the most competitive ones, where quality-adjusted costs have often fallen. In these markets, healthcare, higher education, child care, and housing, we do not need more socialist policy. We need less of it.

We would remind the pessimists that we have seen this movie before, and we remember how it ended. In the late 1980s, the fashionable book among skeptics of American dynamism was Paul Kennedy’s The Rise and Fall of the Great Powers, which argued that imperial overstretch doomed the United States to decline. I remember discussing it in graduate school and arguing that its logic made a better case for the collapse of the Soviet Union than of the United States. It did not win me any points with my professors. Within a few years, it was the Soviet Union that ceased to exist. Declinism had the direction of history backward, and this summer’s World Cup visitors, marveling on social media at the everyday abundance of American life, are supplying the counterpoint in real time.

The deepest cost of the socialist prescription is not redistribution. It is shrinkage. Dull the incentives to invest, build, and take risk, the very forces carrying this expansion, and the pie does not get divided differently; it gets smaller. Argentina entered the twentieth century among the wealthiest nations on earth and legislated itself into decades of stagnation. The young voters powering this wave deserve answers: more housing supply, more competition in healthcare, more accountability in higher education, and an economy that converts a remarkable capital cycle into broad-based hiring. What they do not deserve is a return trip to the thing the whole world woke up from in the late 1980s, right here, right now. Among the events of the long holiday weekend was a wedding at Madison Square Garden; we will borrow and rephrase a single line from the bride’s songbook, that socialism is an alluring daydream on its surface but always ends as a nightmare, and this time we would do well to stay awake.

The full-length essay, with charts and sources, is available as a standalone Piedmont Perspective.

Treasurer and CFO Corner

Translating this week’s data into the questions we are hearing from corporate finance teams.

- Funding and duration. With the Fed on hold and our next-move call a hike rather than a cut, treat the current window as a chance to term out funding rather than wait for cheaper money. On the investment side, we would stay cautious on duration: the front end is well anchored, but the long end holds more term premium than a soft-landing narrative implies.

- Energy and input costs. The retreat in crude and gasoline, echoed by the nine-point drop in the ISM prices index, is a natural moment to revisit fuel, freight, and commodity hedges. We would not treat the relief as permanent, since a geopolitical premium could return ahead of the November midterms.

- Pricing and margins. Headline inflation is cooling, but underlying inflation near 2.9% keeps wage and services costs firmer than the CPI suggests. Rising memory and AI-hardware prices are a fresh source of goods cost-push worth building into 2027 budgets, so we would hold pricing discipline.

- Labor and capital spending. In a capital-led, employment-light expansion, the marginal return sits in equipment, automation, and software rather than headcount. A cooling but low-turnover labor market rewards retention over aggressive expansion hiring.

Bottom Line and Regional Implications

The week’s data and commentary describe an economy in a summer pause that refreshes. Cooling labor momentum alongside a gradually broadening hiring base, falling energy prices providing much-needed relief to consumers, and policymakers showing pragmatic flexibility set the stage for stronger growth in the second half of the year. For clients and regional stakeholders, lower energy prices and a patient Fed are supportive for housing-sensitive sectors and consumer-facing activity in the near term. Longer term, the electricity and grid buildout represents both opportunity, in utilities, transmission, copper, and data centers, and competitive pressure from China’s cost and scale advantages in energy-intensive production. Trade policy adds complexity, with the USMCA now on an annual review cycle. Risks remain, including lingering Iran and Hormuz volatility, sticky core inflation, and the possibility that grid constraints begin to bind innovation, but the base case is continued expansion with policy optionality preserved, and with the next Fed move, in our view, still more likely a hike in 2027 or 2028 than a cut this year.

Mark P. Vitner | President and Chief Economist | Piedmont Crescent Capital | Charlotte, North Carolina