A VIEW FROM THE PIEDMONT · Weekly Commentary on Money, Credit, Exchange Rates & Geopolitics

As the Tanker Turns

Oil fell even as the ceasefire was tested, May inflation likely marked the peak, and the hawkish turn at the Fed gained a fresh convert.

Week of June 26, 2026 · Updated Saturday, June 27 · Mark Vitner, President & Chief Economist

Market Snapshot

| Indicator | Close | Week | Note |

|---|---|---|---|

| S&P 500 | ~7,350 | −1.5% | Flat on the day; rotation out of tech |

| Nasdaq Composite | ~25,300 | ~−4% | Worst week in months; AI fatigue |

| Dow Jones Industrial | ~51,850 | +0.6% | Non-tech leadership; record midweek |

| Russell 2000 | ~3,000 | higher | Rotation winner; SpaceX added to R1000 |

| 2-yr Treasury | 4.20% | lower | Eased as oil fell after PCE |

| 10-yr Treasury | 4.40% | lower | Back below 4.5% |

| Brent crude | $72.55 | −3.2% | Lowest since before the February war |

| WTI crude | $69.21 | −3.1% | Fell even on the Hormuz drone report |

| Gold | ~$4,085 | higher | Safe-haven bid on soft monthly PCE |

| VIX | ~19 | higher | Tech volatility leads |

Levels as of the close, Friday, June 26, 2026. Oil and gold are settlement prints; equity index and Treasury levels are approximate.

On the Data Tape

| Release | Reading | Read-through |

|---|---|---|

| Headline PCE (May) | 4.1% y/y | Three-year high; energy-led and likely the peak |

| Core PCE (May) | 3.4% y/y | Sticky services; the monthly read was soft |

| Q1 GDP (third est.) | 2.1% SAAR | Revised up from 1.6%; growth firmer |

| Durable goods (May) | −4.5% | Transport-led drop; core capital goods firm |

| New home sales (May) | −7.3% | Housing still pinched by rates |

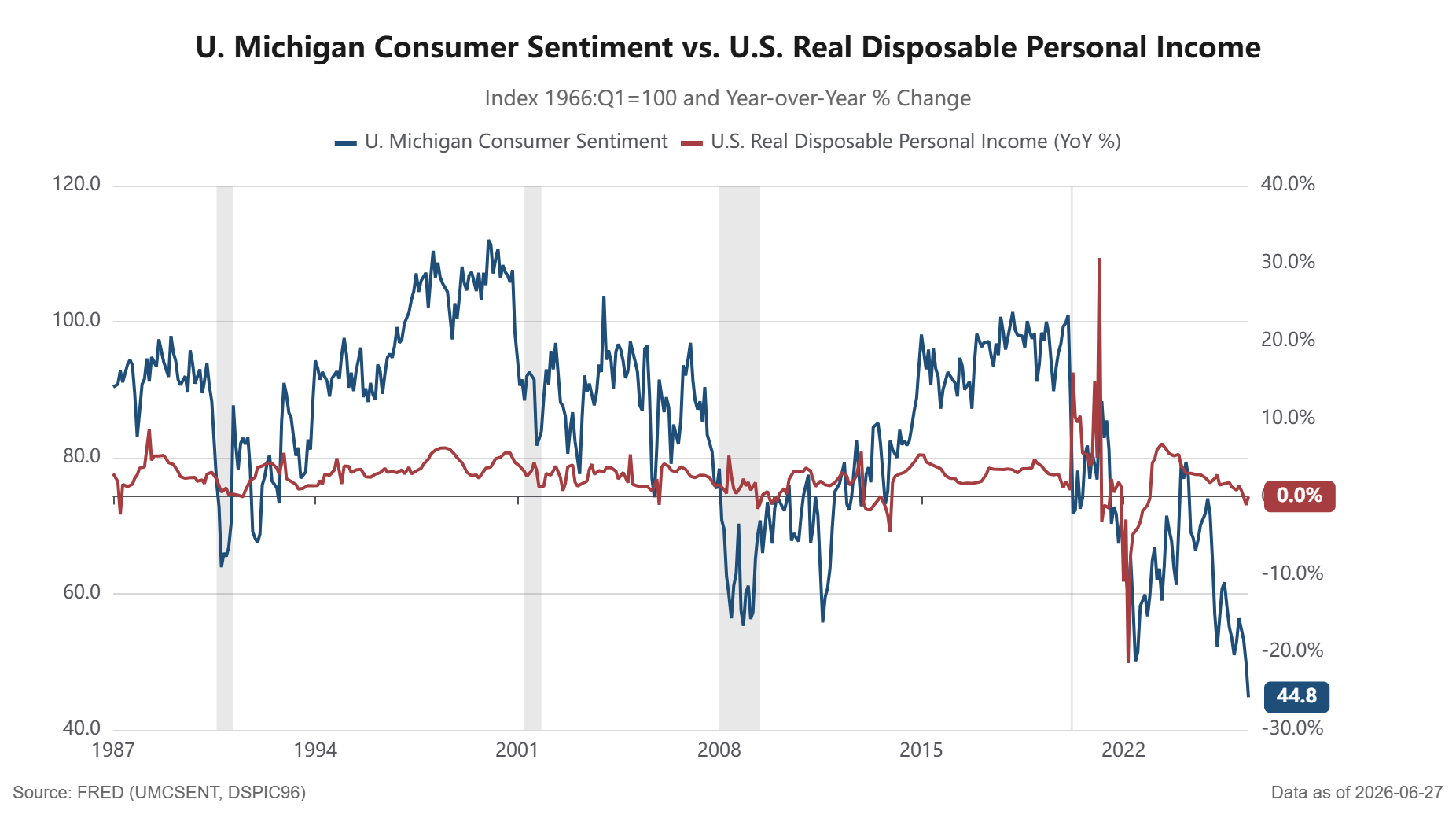

| UMich sent (June, final) | 44.8 | Inexplicably weak; we look to the detail |

The Week in Brief

Inflation reached a three-year high, oil kept falling, and the AI trade lost its footing, all this week. The week confirmed the hawkish hold and handed our framework two fresh supports. The Federal Reserve removed its 2026 cut, May inflation printed at a three-year high, and one more policymaker moved into the rate-hike camp. Energy worked the other way. Crude fell even after the Iran ceasefire was tested at the Strait of Hormuz, which tells us the market now expects the waterway to stay open. The wobble worth watching is in technology, where worries about the cost and financing of the artificial intelligence buildout pulled the largest names lower and revived comparisons to the late 1990s.

The Fed Got the Data It Wanted

The Federal Open Market Committee held the funds rate at 3.50 to 3.75 percent and erased the rate cut it had penciled in for this year at its June meeting. The dot plot did the talking. Nine of eighteen officials now see at least one increase in 2026, and only one still expects a cut, a sharp turn from the March projections. Chair Warsh used his first press conference to commit plainly to returning inflation to 2 percent. Markets heard the message and repriced the front end, sending the two-year note to a fresh high for the year before it eased back as oil fell. Our framework has held that the next move is more likely a hike than a cut, and nothing this week argued otherwise.

The Hawkish Camp Gains a Voice

The case for a hike is no longer confined to the dot plot. On Friday, Minneapolis Fed President Kashkari said he had changed his outlook and now expects one increase this year, arguing that the investment surge tied to artificial intelligence will add to price pressure. He joins Governor Waller, who has warned that the energy shock is working its way into other prices and that inflation is not moving in the right direction. We have made this argument for some time. When the doubts start migrating from the projections into the speeches, the committee is usually closer to acting than the market assumes.

A Three-Handle at the Headline

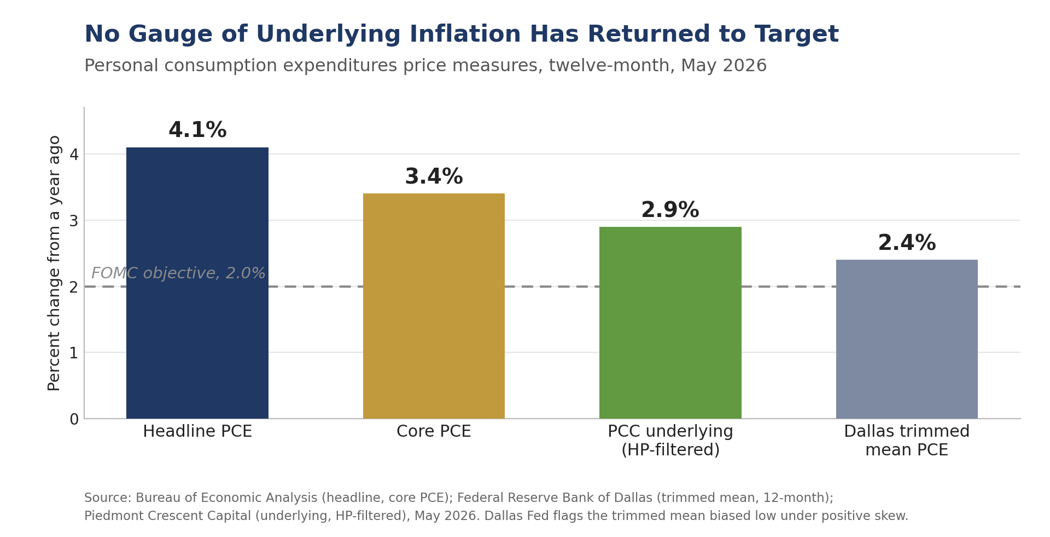

The Fed’s preferred gauge, the personal consumption expenditures price index, rose 4.1 percent from a year ago in May, the fastest pace in three years. Core prices, which strip out food and energy, climbed 3.4 percent, although the monthly increase was softer than feared. The energy shock from the conflict in the Gulf has been the main driver, and it has been seeping into services, where restaurant meals, lodging, auto repair, and medical care all firmed. We have long preferred trimmed-mean measures to the headline for reading the underlying trend, and even those sit above target today. The bottom line is that the underlying pace has not returned to 2 percent, a point we take apart in this week’s Perspective, summarized below.

Growth Is Not the Problem

The economy is not the soft spot in this picture. The third estimate of first-quarter output lifted growth to a 2.1 percent annual rate from 1.6 percent. Real consumer spending rose 0.3 percent in May, and real incomes turned higher for the first time in four months. Durable goods orders fell on a drop in transportation, but the core capital goods that feed business investment held firm, and new home sales slipped as housing stays pinched by rates. We would temper the income headline, since a one-time farm support payment flattered the May figure rather than broad wage growth, but the direction of travel on spending is intact. Firmer growth alongside above-target inflation is precisely the mix that keeps the Fed leaning toward restraint. We shaved our current read for Q2 real GDP growth by the same magnitude as the upward revision, 0.5 percentage point to 2.5 percent, and the wider-than-expected goods trade deficit in May adds further downside risk.

The Consumer’s Mood

Consumer sentiment fell to 44.8 in June, a reading we treat with more caution than usual. The University of Michigan index has dropped to a level the fundamentals do not explain, weaker than the troughs of 2008 and 2022 even as the labor market holds and households keep spending. We put less weight on the headline for that reason. The detail beneath it still earns its keep. The survey captures the frustration of families who have watched prices outrun paychecks through this expansion, and it tracks the long stretch of soft real income growth that has defined it. Real disposable income turned slightly positive in May for the first time in months, and the energy relief now coming through should lift it further in June. We would expect mood to firm as that improvement reaches household budgets, even if the gap between how consumers feel and how they spend remains one of the puzzles of this cycle.

The Tanker Turns

The most telling moment of the week came when the ceasefire was tested and oil fell anyway. An Iranian drone struck a Singapore-flagged cargo ship in the Strait of Hormuz on Thursday, and the United States answered on Friday with strikes on Iranian missile, drone, and radar sites, the first American strikes on Iran since the ceasefire was extended. Crude still declined roughly 3 percent on Friday, with Brent settling near 72 dollars and West Texas Intermediate near 69, the lowest since before the war began in February, because traffic kept moving and the market is pricing the waterway to stay open. The weekend complicated that read. Iran launched drones at Bahrain on Saturday, Hezbollah rejected the new Lebanon framework as a disgrace, and the basic terms of the memorandum, from control of the strait to the use of unfrozen funds, remain unsettled. Central Command still counted dozens of merchant ships transiting the strait on Saturday, so the disruption is contained for now. We attach two conditions to the peak-inflation call. The June price data, due in mid- and late July, has to confirm it, and the understanding has to hold. The weekend is a live test of the second, and oil could gap on Monday if the exchange widens.

The Lebanon Framework

The trilateral framework signed in Washington is best understood as a design to separate Hezbollah from Iran, not a peace deal. The United States, Israel, and Lebanon agreed to a sequenced process in which the Lebanese Armed Forces disarm Hezbollah and dismantle its infrastructure, after which the Israeli military progressively redeploys out of the territory it holds. Two pilot zones come first, with reconstruction money and the return of civilians promised once disarmament in those zones is verified. A trilateral military coordination group and a forthcoming security annex are meant to police the steps, and Washington put one hundred million dollars of humanitarian aid on the table to start. The Israeli delegation summarized the intent plainly, that Iran is out, Hezbollah is out, and a Lebanese state monopoly on force is in. The fact that Iran and Hezbollah both oppose the deal is itself a reason to think it could improve the region’s security.

The sequence is the whole argument, and it is the reason the framework will be hard to implement. Disarmament comes before withdrawal, with no fixed timetable, which lets Israel hold its buffer zone and its freedom to strike for as long as it judges a threat remains. Hezbollah, which was not at the table, has called the deal null and void and a humiliation, and one of its lawmakers warned that any attempt by the Lebanese army to enforce it would mean civil war. That is the trap. The framework asks the Lebanese army to accomplish by force what years of Lebanese politics could not, while Iran presses to fold the Lebanon question back into its own track, where it holds more cards. Reconstruction is the carrot, but it is withheld until the disarmament that Hezbollah refuses, which leaves the arrangement circling itself.

Our read is that this is a long and conditional process rather than a clean settlement, and the markets should treat it that way. The likely path is a slow, contested deployment into the two pilot zones, punctuated by Israeli strikes and Hezbollah harassment, with full peace a distant prospect. The Lebanon file and the Hormuz file move together, since Iran has shown it will use the strait as leverage whenever the regional picture turns against it, as the weekend made clear. The implication for our work is twofold. If the framework holds even loosely, it caps the escalation that drives the oil-risk premium and supports the case that May marked the inflation peak. If it breaks, it hands Iran a ready pretext to squeeze the strait again. We would keep a latent geopolitical premium in mind even as headline crude falls, because the arrangement pulling energy prices down is the same fragile one that could reverse them.

A K-Shaped Tape

The split inside the market widened into a fault line this week. Memory chipmaker Micron blew past expectations, yet the AI complex sold off anyway. A report that OpenAI may delay its public offering into next year, alongside the weak after-IPO performance of SpaceX, raised doubts about how the buildout will be financed, and trading desks flagged the risk to capital spending if the financing window stays shut. The selling went global. South Korea’s Kospi fell nearly 6 percent and tripped a circuit breaker, and the semiconductor index neared correction. Beneath it, the rotation we have flagged continued, with the Dow setting records midweek and the Russell 2000 holding near highs. The capital cycle we have likened to the late 1990s now carries the other half of that comparison. A rush of giant listings, from SpaceX to the coming OpenAI and Anthropic offerings, has drawn the same dot-com parallels we would expect this late in a capex boom. We read the pullback as a recalibration of expectations rather than the end of the investment wave, but the financing question is real and demands respect.

Across the Water

Britain is a useful reminder of what fiscal credibility is worth. Prime Minister Starmer has announced his resignation, with Andy Burnham the favorite to succeed him as soon as mid-July and the choice of Chancellor the next question. A Burnham government would likely lean on public investment and social care, which points to higher near-term borrowing and slower fiscal consolidation, and fits the premium the gilt market has been charging. Yields spiked toward levels last seen in the late 1990s as investors weighed the looser stance, then eased as the leadership picture cleared and soft activity data lowered the odds of further Bank of England tightening. The episode is a live demonstration of what markets demand when they doubt a government’s commitment to its own budget rules.

Geopolitical Watch

Two fronts moved this week, and a third opened on trade. In the Gulf, a single drone strike on a tanker escalated into American retaliation and an Iranian drone attack on Bahrain over the weekend. The skeptics who called the memorandum a pause rather than a peace look closer to right, and the nuclear and inspections questions remain open, with the IAEA still awaiting access. In Eastern Europe, Ukrainian strikes on Russian energy infrastructure are producing domestic fuel shortages inside Russia, a thread that could feed back into global product markets even as crude retreats. On trade, the administration said Europe had agreed to drop tariffs on a range of United States goods to zero, a development we will watch for its effect on industrial supply chains.

Our Call

We expect no rate cut in 2026, and we now count Minneapolis among the voices preparing for a hike. The risk around the Fed remains skewed toward tightening, and the hotter data have pulled that risk forward from the 2027 timing in our June base case, putting a September move on the table unless the energy-led decline in inflation arrives quickly and convincingly in the data. We stay cautious on duration, favor trimmed-mean gauges over the headline for reading the trend and continue to view this as a capital-led, K-shaped expansion, now with a financing question hanging over the AI buildout. May 2026 likely marks the inflation peak, conditional on an open Strait of Hormuz and a durable ceasefire, a condition the weekend’s renewed strikes have put back in play.

Key Takeaways

| Theme | Our read |

|---|---|

| Fed | Hawkish hold confirmed; Kashkari joins the hike camp; next move likely up |

| Inflation | Headline 4.1% is a three-year high; our underlying read near 2.9% is still a three-handle |

| Growth | Q1 revised up to 2.1% and spending resilient; housing still soft |

| Oil | Crude fell even as the ceasefire was tested; watch for a Monday gap on the weekend escalation |

| Consumer | Sentiment at 44.8 looks overdone; soft real incomes are the signal, and they are turning up |

| Markets | K-shaped tape; AI financing doubts pressure megacaps; Dow and small caps lead |

| Rates | Yields eased with oil, but we stay defensive on duration |

| Risks | Lebanon and Hormuz durability, June PCE confirmation, and AI capex financing |

Treasurers & CFO Corner

What this week means for corporate treasury and finance teams.

- Manage the front end actively. With the next move more likely a hike than a cut, revisit hedge ratios on floating-rate exposure, and keep operating cash in laddered Treasury bills and short corporates where front-end yields stay well-anchored.

- Pre-fund while the window is open. The cool reception for large AI-related debt sales and the reported delay in marquee listings show funding access can narrow fast. Term out maturities and bring issuance forward.

- Bank the energy relief, but hedge the tail. Brent near 72 dollars should ease fuel, freight, and input costs, yet the strait was tested this week. Lock in part of the savings with hedges rather than assuming the calm holds.

- Reassess FX into European flux. Sterling is soft on the UK transition and a move toward zero tariffs on United States goods is underway. Review euro and sterling hedges and counterparty exposure before they reprice.

THE PIEDMONT PERSPECTIVE · ABRIDGED

Left of the Decimal Point

Condensed from the Perspective published June 25, 2026. The full piece, with complete methodology and four exhibits, is available separately.

The debate over whether inflation carries a two-handle or a three-handle is not a rounding curiosity, it decides whether the Fed is near its goal or still distant from it. We ran a Hodrick-Prescott filter across a broad set of price series to separate the durable trend from monthly noise and the energy spike. The filtered measures put underlying inflation near 2.9 percent. That reading reaccelerated into the spring as the energy shock spread across the cross-section, but energy is the principal outlier and is now rolling over, leaving the durable trend firm relative to target rather than back at it.

Headline and core readings both distort the trend at a moment like this one. Headline at 4.1 percent overstates the persistent pace because it carries the full energy shock. Core at 3.4 percent removes food and energy but still reflects the pass-through of higher fuel costs into services. The filtered series cuts through both and lands near 2.9 percent. The Dallas trimmed mean reads lower, at 2.4 percent, though the Dallas Fed cautions the positive skew in the current shock is biasing that measure down, so we treat it as the floor of the range rather than its center.

Even under the most generous reading, the number does not round to target. A 2.9 percent underlying pace rounds to three, not to two. The Fed’s new leadership has signaled a willingness to interpret progress generously, yet generosity cannot turn a 2.9 into a 2.0. Only the trimmed mean slips to a two-handle, and the Dallas Fed itself says that reading is biased low today. The better-behaved gauges, and the more constructive forecasts across the Street, keep the trend on a three-handle through year end.

This is why we do not expect a cut. Underlying inflation sits closer to 3 percent than to 2 percent, in an economy still growing above 2 percent, leaving the Fed with no room to ease and a credible reason to consider tightening. The exhibit below shows where the major gauges stood in May.

Mark P. Vitner

President and Chief Economist, Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com | (704) 458-4000

A View from the Piedmont is published by Piedmont Crescent Capital for informational purposes only and does not constitute investment, legal, or tax advice. Views are as of the date of publication and are subject to change.