| PIEDMONT CRESCENT CAPITAL | May 10, 2026 |

|

Highlights of the Week

• Economic Pulse: Capital cycle is real. Labor market softening at the margin. War remains the dominant risk. • ISM Manufacturing: Held at 52.7 in April, fourth straight month of expansion. Prices surged on the oil shock; employment fell to 46.4. • ISM Services: Rose to 53.6, the 22nd consecutive month in expansion. • Employment: April payrolls +115K, beating the 55K consensus; unemployment held at 4.3%. ADP at +109K corroborated the BLS read. Low-hire, low-fire continues. • NY Fed Survey: One-year inflation expectations rose to 3.6%; longer-run remained anchored at 3.0–3.1%. • GDPNow: Atlanta Fed Q2 nowcast at 3.7% as of May 8 — driven by investment, not consumption. • Markets: 10-year near 4.41%. Brent ~$101 after touching $119. FOMC held 8-4, the most dissents since 1992. • Geopolitics: Ceasefire on “massive life support” after Trump rejects Iran proposal. Trump-Xi summit May 14–15. Market Snapshot

Brent Crude: ~$101 / bbl WTI: ~$95 / bbl 10-Yr Treasury: 4.41% 2-Yr Treasury: 3.81% Yield Curve (2s10s): +60 bps Fed Funds Target: 3.50–3.75% Atlanta GDPNow Q2: 3.7% |

Capital Cycle Carries the Day,

|

The Macro Backdrop

The period since our last weekly report has been unusually rich in key economic data. The April employment report, ADP, both ISM surveys, the New York Fed Survey of Consumer Expectations, the UMich survey, and the latest Atlanta Fed GDPNow nowcast all landed in close succession. Taken together, they sketch a clearer picture than any single release. The capital cycle is real and is driving topline growth. The labor market is cooling gradually but is not breaking. Underlying inflation is contained, though headline measures are being pushed around by the oil shock. And the war with Iran remains the central risk to the expansion.

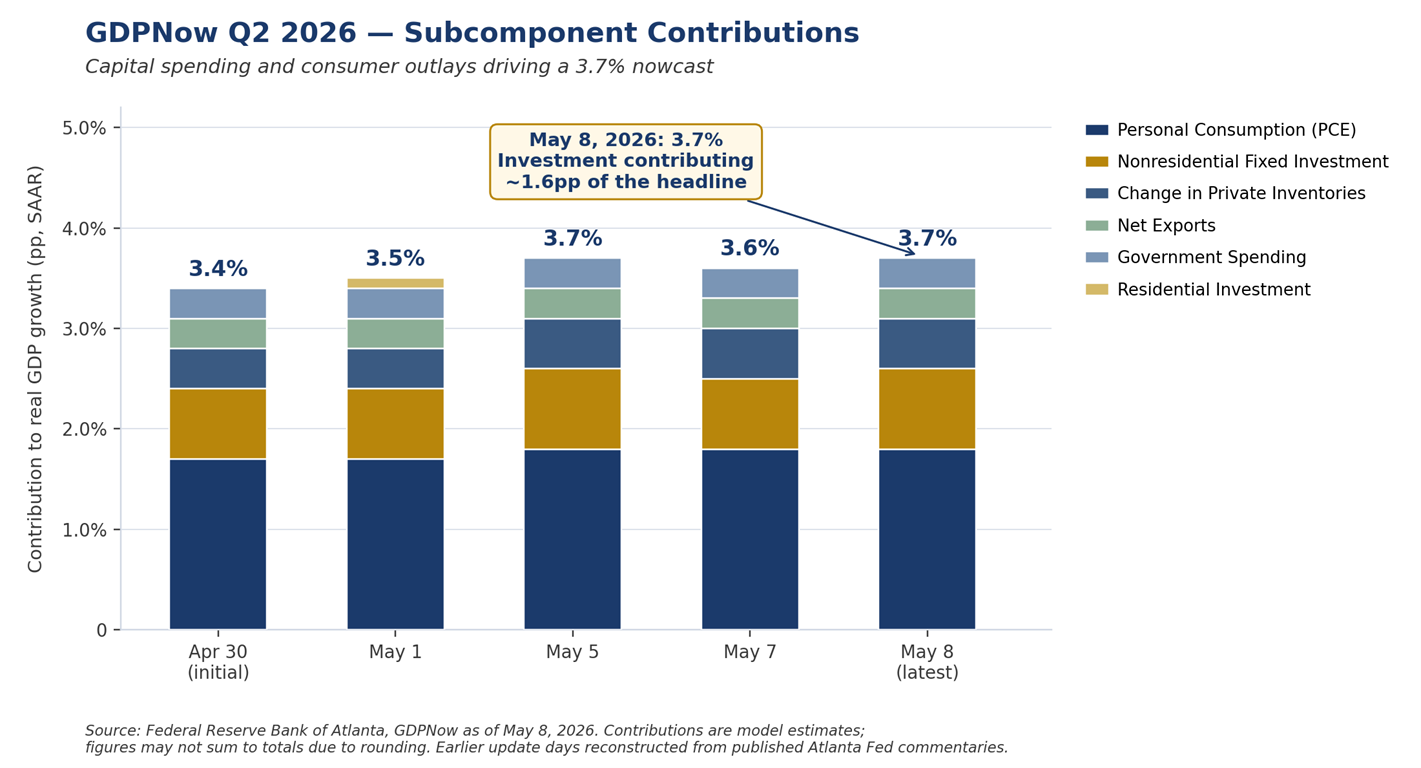

Begin with growth. After rising at a solid 2% pace in Q1, the Atlanta Fed's GDPNow projects real GDP to rise at a 3.7% pace during the current quarter, up from 3.5% a week earlier. Nonresidential fixed investment is expected to contribute roughly 0.8 percentage points to headline growth and real personal consumption another 1.8 points. Government spending, trade, and inventory building account for another 0.8. This is a capital-led expansion of a sort the post-2008 economy rarely produced. AI infrastructure, power generation, grid expansion, reshoring, and defense investment are no longer talking points; they are pushing measured growth into territory we have not seen in any meaningful stretch since the late 1990s. The war is a real drag, but business investment is more than offsetting it, pulling the headline higher rather than letting it slip. AI is also beginning to deliver productivity gains, modest this year and likely to compound in future years. The economy is being fueled more by protein, that is, capital investment and intellectual capital, than by carbohydrates.

The ISM surveys reinforced the same picture. Manufacturing held at 52.7 in April, a fourth consecutive month of expansion. New orders, the most forward-looking component of the survey, strengthened to 54.1. Production decelerated but stayed in expansion at 53.4. Two warning lights flashed. The Prices Index surged at the fastest pace since April 2022, driven by oil and diesel costs, and the Employment Index fell to 46.4, the sharpest contraction in four months and a rare countersignal in an otherwise firming jobs picture. Services rose to 53.6, the 22nd consecutive month in expansion. Demand is holding up, but costs are climbing — a strain that became increasingly visible in Q1 earnings commentary. Where the surveys go from here depends largely on how the Iran conflict plays out. Most business owners we hear from are not expecting the disruption to drag into the summer; if it does, the softer-tier data will likely give way first, and firms whose margins have been squeezed for any sustained period will need to begin cutting costs in earnest.

Labor Market: Low-Hire, Low-Fire Continues

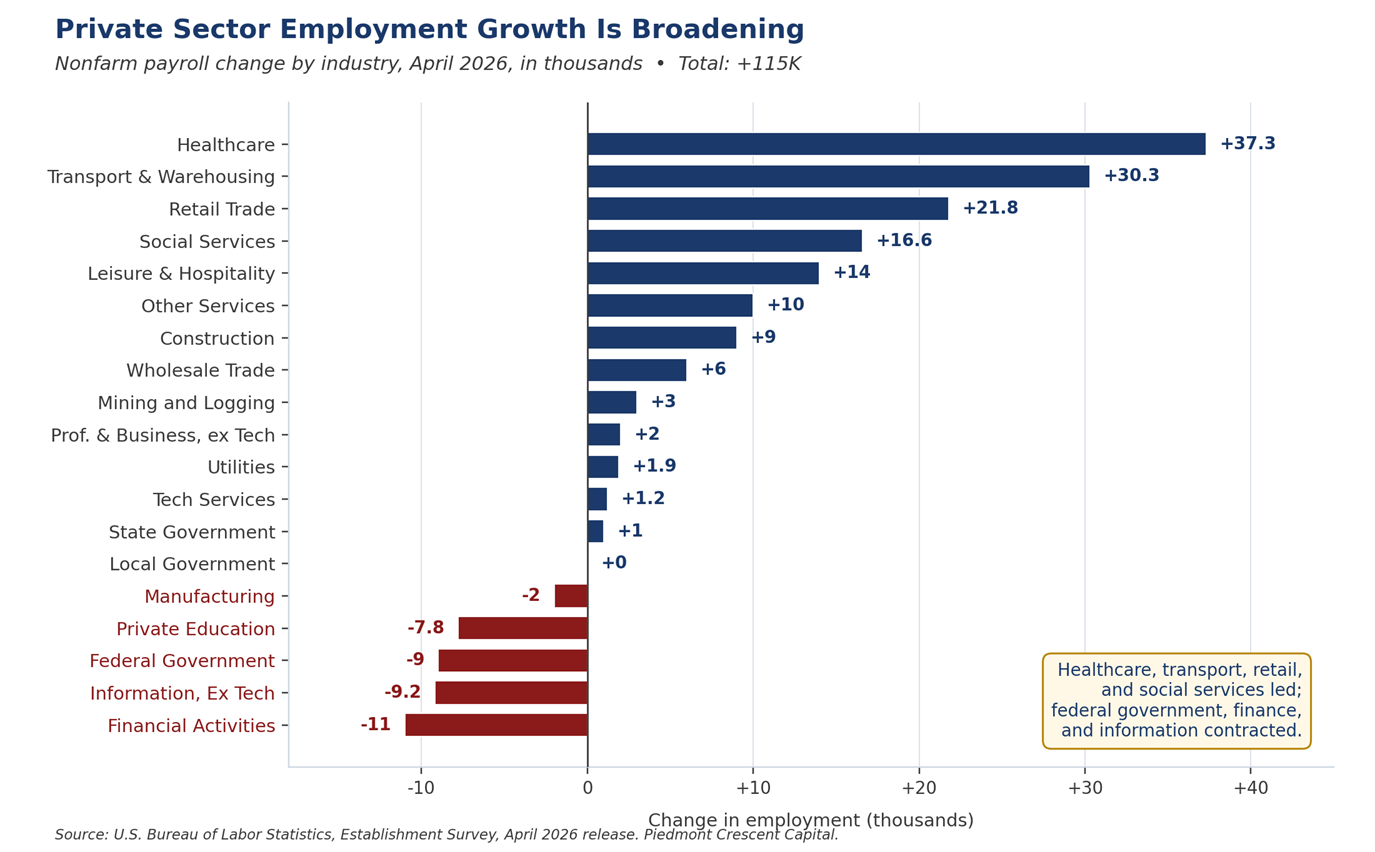

Friday's employment report did not change the labor market story so much as confirm it. Nonfarm payrolls rose 115,000 in April, well above the 55,000-consensus estimate, although February was revised sharply lower by another 23,000 to a net loss of 156,000. The gains were concentrated in healthcare (+37,000), transportation and warehousing (+30,000), and retail trade (+22,000). Federal government employment continued to contract, falling another 9,000 in the month and roughly 348,000 since October 2024. Manufacturing payrolls edged down 2,000, consistent with the ongoing weakness signaled by the ISM employment index. The unemployment rate ticked up modestly, but the rounded figure held at 4.3%.

What growth there has been in the manufacturing sector remains concentrated in the capital-intensive industries — semiconductors, machinery, chemicals, and related high-tech durables — where surging fixed investment in equipment, automation, and AI-related infrastructure is driving robust output and value-added gains but delivering only modest net employment increases. That mix tells us most of what we need to know about why nominal payrolls and the underlying productive economy can diverge for an extended period.

Questions about the quality of April's payroll gain persist, as the BLS birth-death model added 386,000 jobs in the unadjusted data — more than accounting for the entire reported increase. ADP's independent read should largely put those concerns to rest. The ADP National Employment Report, which covers a much larger sample of private payrolls and has historically aligned closely with BLS annual revisions, showed a solid +109,000 private-sector gain in April, the strongest reading since January 2025. Education and health services again led the way. Wage growth for job-stayers remained steady at 4.4% year-over-year.

Average hourly earnings in the BLS report rose a modest 0.2% month-over-month and 3.6% year-over-year, below the pace of inflation. This is the texture of a labor market that has settled into the “stable but not strong” equilibrium Chair Powell, Governor Waller, and Chicago Fed President Goolsbee have been describing for some months. Hiring is slow, layoffs are limited, and the gains continue to skew toward lower-paying service sectors, weighing on the average hourly earnings figure. At the same time, voluntary attrition has slowed to unprecedented lows across most industries — reducing training and onboarding costs but pushing up wage and benefit expenses, as annual increases are now applied across a more experienced and higher-paid workforce.

The New York Fed's April Survey of Consumer Expectations added important context. One-year inflation expectations rose to 3.6%, but the three-year and five-year measures held steady at 3.1% and 3.0%. Longer-run expectations remain well anchored even as headline inflation gets pushed around by gasoline, which is a quietly encouraging signal that household psychology has not yet shifted. The mean perceived probability of a higher unemployment rate one year out — the other side of the Fed's dual mandate — rose to 43.9%, the highest reading since April 2025. Households are uneasy about jobs but have not yet adjusted their spending plans materially.

By contrast, the University of Michigan preliminary May reading plunged to a record low of 48.2, far more pessimistic than the New York Fed survey and driven heavily by gasoline prices and tariff concerns. The divergence reflects the Michigan survey's greater sensitivity to immediate pocketbook and political strains. The New York Fed data are reassuring in that longer-term inflation expectations remain contained. We put more weight on the New York Fed series, as longer-run expectations are what matter most for the Fed's policy calculus.

The Capital Cycle in the Numbers: Milken and Earnings Season

First-quarter earnings continued to validate the capital-intensity story that permeated the Milken Institute Global Conference in Beverly Hills this past week. The 29th annual conference made one thing clear: the largest pools of capital in the world are leaning into this cycle rather than stepping back from it. Blackstone President Jon Gray captured the prevailing sentiment when he reminded the audience that the U.S. economy and global markets have powered through pandemic, inflation, regional conflict, and now the war with Iran, and he saw no reason to expect anything different this time. Most of the panel speakers we heard echoed that view. The mood was constructive in a way it has not been at Milken in some time.

A few of the more substantive themes from this year's panels we feel deserve emphasis. AI has moved decisively from a software story to an industrial buildout, and the financing is following suit. Panels featuring Macquarie, Actis, ECP, and DataVolt discussed how institutional capital is being deployed across power generation, grid, storage, and data centers, increasingly through private credit and insurance balance sheets rather than traditional bank channels. The AI–energy backbone in particular is shaping up as the dominant new driver of infrastructure capital formation, with reliability, duration, and regulatory constraints, and importantly not capital availability, emerging as the binding constraints on the pace of deployment.

Private credit got plenty of attention as well, both as an enabler of the cycle and as a source of nascent concern. The stress signals at Tricolor and First Brands came up repeatedly in hallway conversations, but the largest sponsors — Apollo, Ares, Blackstone, Blue Owl, and Golub — sounded notably constructive on direct lending volumes overall, while acknowledging that the easy returns of 2022 to 2024 are behind us. The asset class continues to grow, but selectivity is back.

The earnings data backed up the conference rhetoric. With 89% of the S&P 500 having reported, blended Q1 earnings growth stands at 15.1% year-over-year, the sixth consecutive quarter of double-digit growth. Eighty-four percent of companies beat EPS estimates, the highest beat rate since Q2 2021, and in aggregate companies are reporting earnings 18.2% above estimates against a five-year average of 7.3%. By any conventional measure these are exceptional numbers.

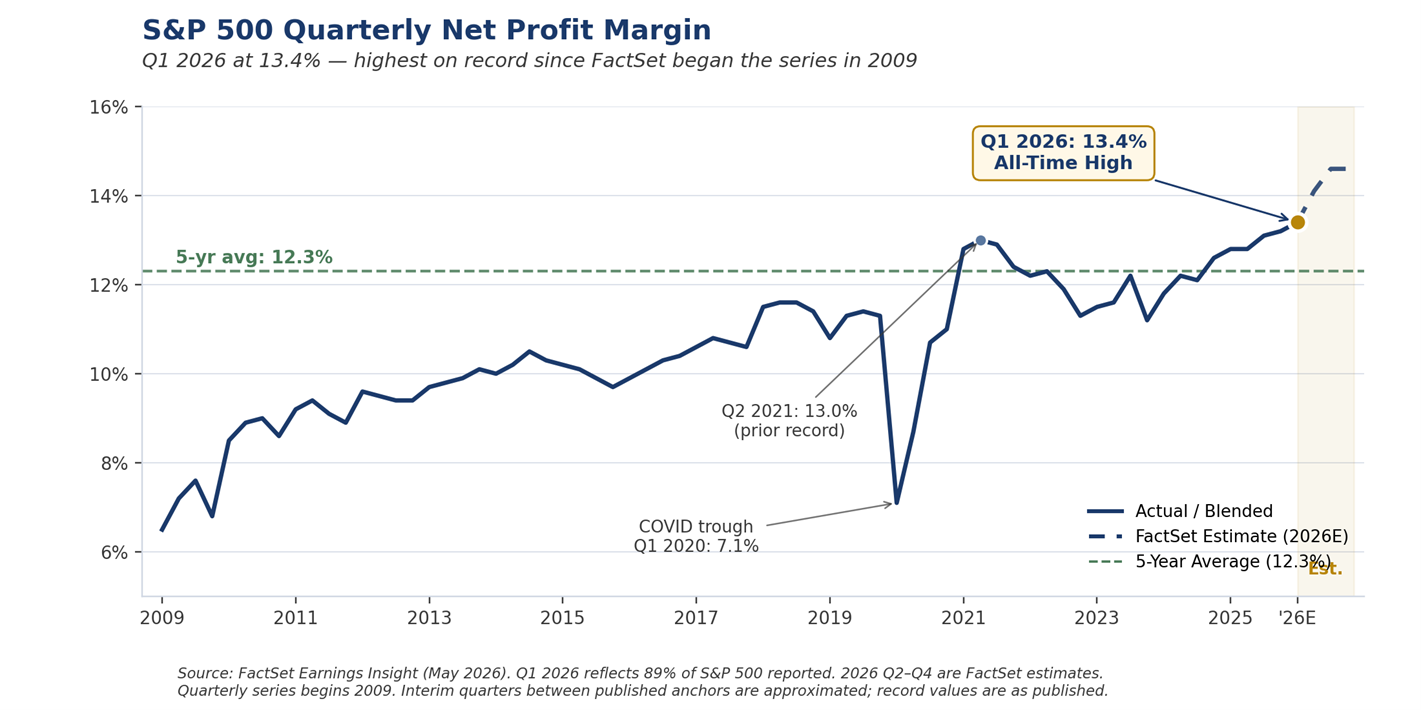

The single most striking data point is the blended net profit margin of 13.4% for Q1 2026, the highest reading on record since FactSet began tracking the metric in 2009 and a step up from the prior record of 13.2% set just one quarter ago. Information Technology led at 29.1%, up from 25.4% a year earlier. The capital-intensity thesis is showing up where it ultimately matters most — in the bottom line. Firms that allocated capital toward automation, productivity, and AI-enabled process redesign during the post-pandemic period are now translating modest revenue growth into outsized earnings growth, and the operating leverage runs throughout the income statement.

A genuinely new differentiation emerged within the Mega-cap technology complex this earnings season. Alphabet rose roughly 34% in April, its strongest monthly gain since 2004, after a Q1 beat across cloud, advertising, and Waymo. Meta Platforms fell roughly 9% despite beating earnings, after raising their 2026 capex guidance to a range of $125 to $145 billion. The market is no longer rewarding the scale of AI commitment alone; it has begun demanding evidence of returns, or at least a credible path to wider margins. This is a healthy development for the cycle, and it distinguishes the current capex boom from earlier ones in which spending itself was treated as a positive signal regardless of the back-end economics.

Two caveats are worth highlighting alongside the strength. AI-related capex is beginning to crowd out other investment categories in certain segments, a shift that bears watching even as aggregate investment continues to rise. And the private credit stress signals are real, even if overall flows remain ample. Tricolor and First Brands have generated headlines, and we expect more idiosyncratic accidents in the asset class in coming quarters. Neither caveat undermines the broader thesis. Both argue for selectivity. Pricing power has narrowed but not disappeared. Firms with genuine productivity gains can still hold price; firms without them cannot.

The composition of growth has lasting benefits beyond the immediate cycle. The most important implication is that it supports stronger potential GDP. It raises long-run electricity demand in ways that will require sustained investment for a decade or more. It rewards firms that allocate capital well. And it likely contributes to the upward drift in long-term interest rates. The transmission mechanism to higher rates is the competition for capital, not higher underlying inflation. The economy should be capable of growing more rapidly than it has during the bulk of the post-2008 period, to something closer to what occurred in the late 1990s.

Markets & Financial Conditions

Bonds and equities remain at odds with one another. The 10-year Treasury yield held near 4.41% this week, the 2-year near 3.81%, and the curve sits positively sloped by roughly 60 basis points. The long end is being pushed higher by three forces working in the same direction: oil-driven inflation expectations, persistent term premium rebuilding on heavy Treasury issuance, and a structural growth rate that may be meaningfully higher than the post-2008 framework assumed. The bond market is pricing the war as a duration risk rather than a flight-to-quality story, which is unusual and worth flagging.

Equities continue to take the constructive view. The Q1 earnings strength has broadened beyond a handful of mega-cap names, and the capital-cycle theme is supporting cyclicals tied to power, grid, defense, and reshoring. Higher rates that reflect stronger growth are very different from higher rates that reflect inflation worries, and we read the current move as much closer to the former. That said, the gap between equity and bond pricing is wider than the underlying data justify in both directions. The bond market's caution looks well grounded.

Brent settled near $101 after touching $119 earlier in the week on fresh clashes between U.S. and Iranian forces in the Strait. WTI sat near $95. The Strait of Hormuz remains effectively closed, and the IEA continues to characterize the disruption as removing roughly 14 million barrels per day from global supply. U.S. retail gasoline is over $4 per gallon. Refined product stocks have drawn for twelve consecutive weeks for gasoline and nine for distillates. The supply-side math is considerably starker than the headline crude price would suggest.

Piedmont Perspective: A Divided Fed and the Warsh Transition

The April 29 FOMC meeting was Chair Powell's last and one of the most consequential in years. The Committee held the federal funds target at 3.50 to 3.75% on an 8-4 vote, the most dissents the Committee has recorded since 1992. Unsurprisingly, Governor Miran preferred a 25 basis-point cut. Cleveland's Hammack, Minneapolis's Kashkari, and Dallas's Logan all supported holding rates steady but objected to including an easing bias in the statement. The split is real and reflects a growing concern among the hawks that the easing cycle may already be over and that the next move, if there is one, could just as plausibly be a hike as a cut. The path to consensus inside the Committee has narrowed considerably.

Kevin Warsh's nomination cleared the Senate Banking Committee on Wednesday, with final Senate confirmation now imminent. Warsh is on track to chair the June 17 FOMC meeting. Futures markets are pricing roughly a 93% probability of a hold in June, and we agree with that probability. Warsh's framework, as he laid it out in his confirmation testimony and in his subsequent commentary, rests on a handful of core ideas. Policy should remain restrictive until inflation is fully anchored. Balance sheet normalization should continue. Markets need stronger price discovery. And the Treasury and the Fed must acknowledge their growing interdependence, particularly with fiscal deficits running at the current scale.

The most underappreciated element of the Warsh framework is his structural optimism about productivity. He has argued that AI is materially boosting the supply side of the economy and that the Fed needs to do considerable additional work to assess the productivity boom in real time. A central banker who believes potential output is rising should, in principle, tolerate higher measured growth without raising rates. The implication is that the gap between Warsh's stance and Powell's may be narrower than markets are currently pricing, particularly if the labor market stays in its current low-hire, low-fire equilibrium.

Our base case is a patient Warsh Fed through the June meeting, followed by a 25 basis-point cut in September if the war risk subsides and the underlying inflation trend continues to drift lower. We see a possible second cut at the December meeting, but only if the labor market weakens meaningfully. The first real test arrives once the economy moves past the Iran-related distractions and growth firms as inflation moderates. If growth firms more decisively than we expect, the second cut becomes considerably less likely.

Geopolitics: Iran Hits a Wall as Trump Heads to Beijing

The Iran picture has deteriorated meaningfully in the last several days. President Trump rejected Tehran's most recent counterproposal as “totally unacceptable” and declared on Monday that the conditional ceasefire is on “massive life support.” The administration has accused Iran of reneging on commitments around the disposition of its enriched uranium stockpile, and Trump aides have been describing the President as more seriously considering a resumption of major combat operations than at any point in recent weeks. The Strait of Hormuz remains effectively closed. The U.S. naval blockade of Iranian ports is in its fourth week. Operation Project Freedom, the Navy escort mission for outbound merchant ships that Trump launched on May 4 and paused two days later on reports of progress, may not stay paused much longer but would provide only minimal relief. Brent traded as high as $119 earlier in the week before settling back near $101 as the diplomatic temperature kept changing.

Our reading is that further military action is now more likely than not, simply because there is no other way to bridge the gulf between what each side currently views as an acceptable outcome. Tehran wants compensation for war damage, the release of frozen assets, and the lifting of sanctions before yielding control of nuclear material. Washington wants the uranium out, the Strait fully open, and a binding curtailment of Iran's ballistic and missile programs before serious sanctions relief is on the table. Beyond these specifics, Washington would also like to see an Iranian regime less openly hostile to the West.

The Iranian negotiating position has hardened further in recent weeks under pressure from hardliners critical of Parliamentary Speaker Ghalibaf's lead role. A short, sharp escalation aimed at infrastructure rather than population centers may be the only mechanism available to the administration to reset expectations and unstick the talks. The risk is that even a calibrated escalation could trigger a less calibrated response, particularly from elements of the Iranian Revolutionary Guard with their own incentives. For the IRGC, a deal along U.S. guidelines is an unacceptable existential risk.

That backdrop frames the Trump-Xi summit on May 14 and 15 in Beijing, the first state visit to China by a sitting U.S. president since Trump's own visit in 2017. The summit was originally scheduled for March and pushed back after the Israeli and U.S. strikes on Iran. The principal agenda items are trade, rare earths, semiconductors, AI, Taiwan, and Iran. Treasury Secretary Bessent and Vice Premier He Lifeng meet in Seoul on Wednesday to finalize the trade groundwork. Trump is traveling with a large delegation of U.S. CEOs including Musk, Cook, Fink, Schwarzman, Solomon, Mehrotra, and Amon, signaling that the administration wants tangible purchase commitments to point to ahead of the November midterms. The new “Board of Trade” mechanism, intended to police follow-through on Chinese purchase commitments, will be the centerpiece of any announcement.

Iran is the wild card in Beijing. China is Iran's largest crude buyer, and the U.S. Navy is currently intercepting tankers bound for Chinese ports. Beijing hosted Iranian Foreign Minister Araghchi last week and is publicly positioning itself as a potential broker on Hormuz, an awkward but useful role given how few governments have working relationships with both Tehran and the Gulf states. Concrete progress on Iran at the summit is unlikely. The optics matter regardless. If the two leaders signal even modest alignment on freedom of navigation through Hormuz, oil markets could give back $10 to $15 a barrel of crisis premium very quickly. If the summit produces nothing on Iran, or if it coincides with renewed U.S. strikes, oil will move sharply the other way.

Our base case remains that an outline agreement on Iran comes together by late May or early June, with the political pressure of Memorial Day and the summer driving season weighing on both sides. We have moved the downside probability up to 35% from 30%, reflecting both the deterioration in the negotiating tone over the past several days and the increased likelihood of additional U.S. military action. Markets remain priced considerably closer to the base case than the risk case, particularly in equities. The supply-chain consequences of the conflict continue to extend well beyond crude. Fertilizers, industrial gases, ammonia, and freight insurance are all exposed. Disruptions of this kind typically appear first in corporate margins and only later in consumer prices, with a one to two quarter lag. The April surge in the ISM Manufacturing Prices Index is the leading edge of that adjustment.

CFO & Treasurer Corner

What This Means for Corporate Finance

Funding & Issuance: The fixed-rate window remains open but is no longer improving. Term premium continues to build as markets digest the war, the deficits, and the structural growth picture. Borrowers should lock in fixed-rate funding opportunistically and pull forward 2027 and 2028 maturities where the trade-off allows. Floating-rate borrowers should stress-test interest coverage assuming the 10-year remains at or above 4.40% through year-end.

Energy & Input Costs: Brent has settled near $101 after touching $119 mid-week. The April ISM Manufacturing Prices Index surged at its fastest pace since 2022, and diesel and middle distillates remain the choke point. Firms exposed to freight, logistics, or petrochemical inputs should be stress-testing 2026 cost assumptions now, and the hedging window may be shorter than usual.

Capital Allocation: Capex guidance from Q1 earnings has continued to rise. The cycle is being driven by AI infrastructure, power generation, grid expansion, and reshoring, and it is showing up in the early Q2 GDP forecasts. AI is delivering measurable productivity gains today, with the bigger payoff likely to compound over the coming years. Firms with credible productivity stories are being rewarded; those without are not. This is a moment to commit, not to wait.

Planning Assumption: Our base case has the Strait of Hormuz reopening by mid-summer, Brent retracing toward $80 by year-end, GDP growing around 2.5% driven by capital spending, and the Warsh Fed delivering one cut in September. With the downside probability now at 35% and rising, we recommend explicitly building the war-escalation case into Q2 board discussions and ensuring liquidity buffers can withstand a 60-day run at $130 Brent alongside materially slower global growth.

Looking Ahead

| Day | Release / Event | Why It Matters for CFOs & Markets |

|---|---|---|

| Tuesday | CPI (April); NFIB Small Business Optimism | Headline CPI is the cleanest read on how much of the oil shock is flowing into the broader price basket. The Cleveland Fed median and trimmed-mean prints embedded in this report will tell us whether the underlying trend is still drifting lower or has stalled. |

| Wednesday | PPI (April); Senate floor vote on Warsh confirmation expected; Bessent meets Vice Premier He Lifeng in Seoul | PPI will speak to margin pressure for goods producers. The Warsh confirmation vote could come this week, with markets attentive to any commentary on the timing of the first Warsh Fed meeting in June. The Seoul meeting between Treasury and China's economic czar sets the table for the Trump-Xi summit later in the week. |

| Thursday | Retail Sales (April); Initial Claims; Industrial Production; Trump-Xi summit (Day 1, Beijing) | First read on whether the consumer is responding to higher gasoline prices. Claims continue as the highest-frequency labor signal. IP will track manufacturing momentum after the soft ISM employment print. The summit's opening session is the most consequential event of the week for trade, technology, and the path of the Iran negotiations. |

| Friday | Housing Starts & Permits (April); UMich Sentiment (preliminary, May); Trump-Xi summit (Day 2, joint readout) | Starts will signal whether higher long rates are weighing on residential investment. UMich sentiment has run well below the hard data; convergence in either direction is the question. The summit's joint readout and any commitments on rare earths, technology, agriculture, and Iran will close out the week. |

Markets will focus on next week's CPI and PPI as the cleanest read on how much of the oil shock is flowing through to the broader price basket, on Thursday's retail sales as a real-time check on consumer behavior, on the Senate confirmation vote for Kevin Warsh, and on the Trump-Xi summit. The interpretation of these prints will matter more than the headline numbers themselves. The unsettled questions are whether the better measures of underlying inflation continue drifting lower despite headline pressure, whether the Powell-to-Warsh transition introduces fresh volatility at the long end, whether Beijing offers anything meaningful on Hormuz, and whether the Iran negotiations require another round of military action to get unstuck.

Scenario Framework

| Scenario | Macro & Market Implications | Corporate Finance Action |

|---|---|---|

| Base Case (50%) | Outline agreement on Iran by late May or early June; Hormuz reopens by mid-summer with U.S. military reinforcement of the timetable; Brent retraces toward $80 by year-end. Capital cycle continues to drive Q2/Q3 GDP at 2.5–3.0%. Labor market stays in low-hire, low-fire equilibrium with unemployment at 4.3–4.5%. Warsh Fed delivers a 25 bps cut in September, holds in November and December. 10-year holds a 4.30–4.60% range. | Lock fixed-rate funding opportunistically; long end no longer improving. Continue capex investment in productivity-enhancing projects. Use any back-up in long rates above 4.60% as an issuance window. Build moderate inventory buffers on energy-sensitive inputs. |

| Upside Case (15%) | Trump-Xi summit produces meaningful alignment on Hormuz; Iran agrees to verifiable nuclear concessions by early June; Hormuz reopens faster than expected. Brent returns to a $75–80 range by Q3. Capital cycle accelerates as input cost pressure recedes. Equity earnings broaden further. Warsh Fed cuts 50 bps over H2. | Step up productivity-led capex. Reassess working capital toward growth. Communicate margin trajectory clearly. Refinancing window opens further. |

| Downside Case (35%) | Negotiations collapse or escalate through Q3; Brent moves to $130+. Headline CPI re-accelerates above 4%. Consumer cracks visibly in lower-income segments. Fed paused indefinitely. Credit spreads widen 50–100 bps. GDP slows to 1.0–1.5% in H2. | Stress-test floating-rate exposure. Build liquidity buffers. Defer non-essential capex. Hedge energy and freight inputs aggressively. Review covenant headroom on leveraged credits. Lengthen working-capital cycles. |

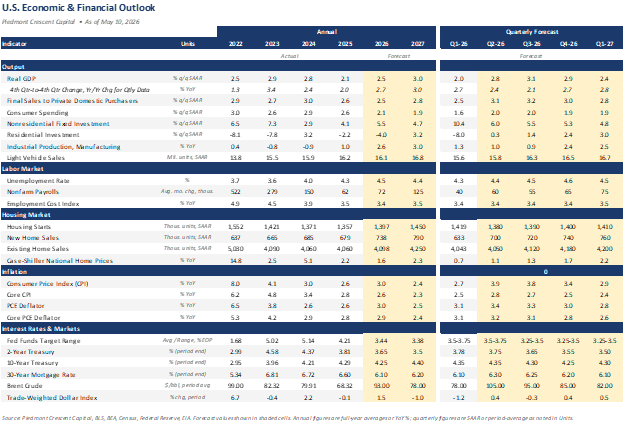

Forecast Update

Disclaimer

This commentary reflects the views of the author as of the date noted and is provided for informational purposes only. It does not constitute investment advice or a recommendation to buy or sell any security. Information has been obtained from sources believed to be reliable, but accuracy and completeness are not guaranteed. Past performance is not indicative of future results. © 2026 Piedmont Crescent Capital.