A VIEW FROM THE PIEDMONT

Hot Headline, Patient Core, and a Cleared Runway at the Fed

Highlights of the Week

- Economic Pulse: Strong consumer in the data, weakening confidence in the surveys. The expansion is holding even as the war embeds itself in headline prices.

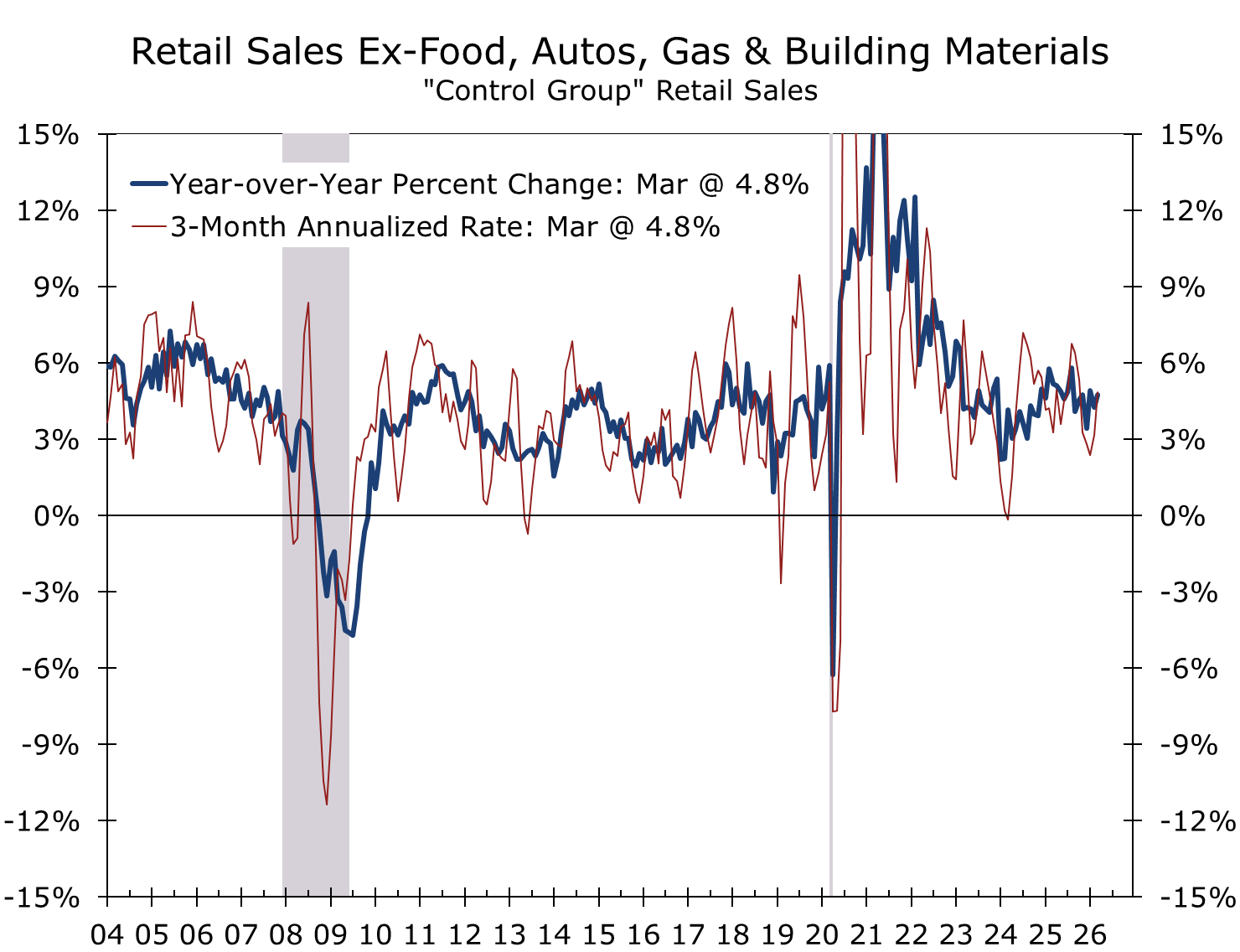

- Consumer: March retail sales beat expectations at +1.7% headline and +0.7% control group, the strongest since August. Tax refunds are doing real work.

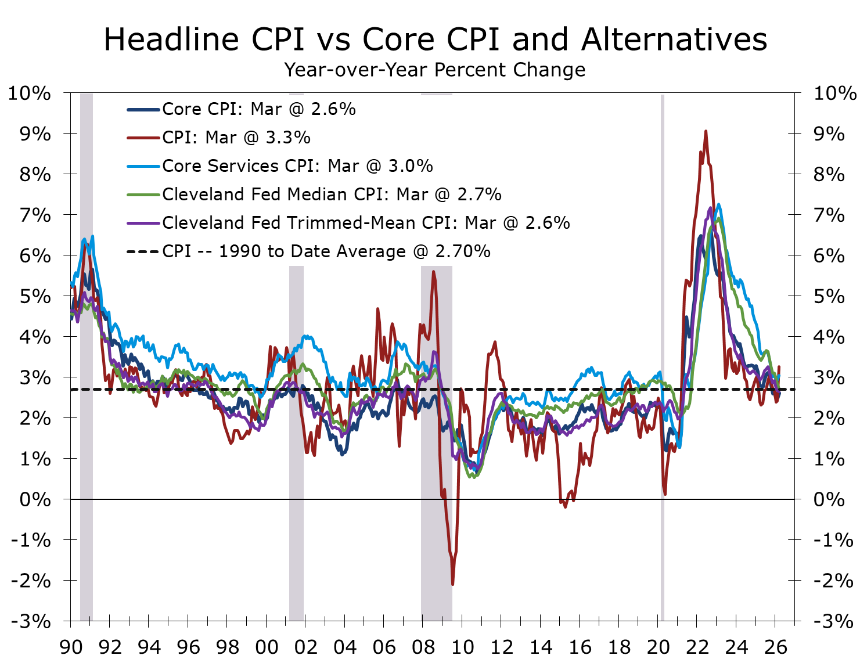

- Inflation: Headline CPI jumped to 3.3% YoY on a 21% gasoline surge, but core CPI was 0.2% m/m and Cleveland median and trimmed-mean both ran 0.2%. The trend signal is intact.

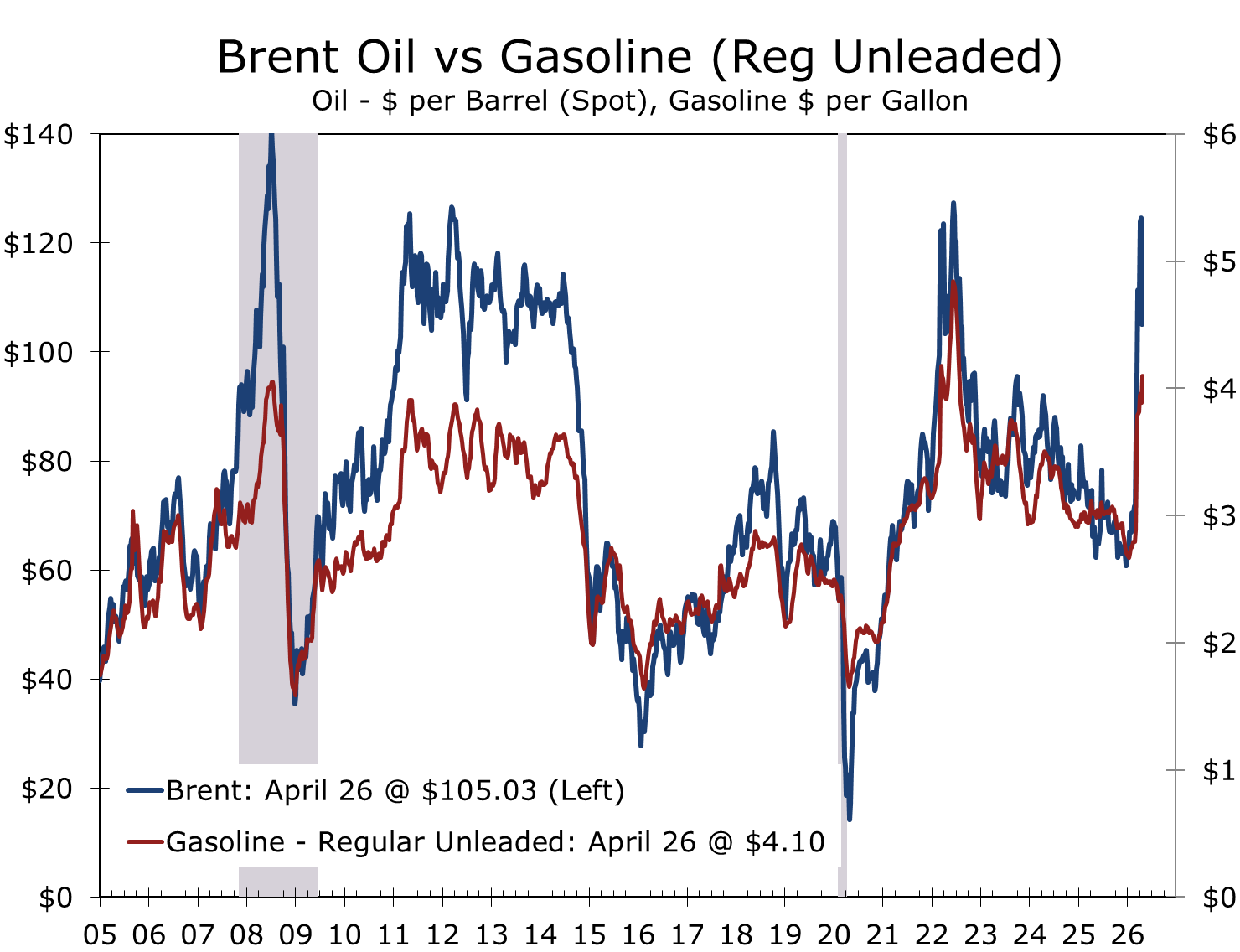

- Markets: 10-yr at 4.31%, equities at all-time highs, Brent ~$104. Risk and rate markets disagree on the war's trajectory. Bonds look right.

- Geopolitics: Strait of Hormuz remains effectively closed. U.S. naval blockade of Iranian ports enters its third week. Talks collapsed Saturday after Iran's foreign minister left Islamabad; the ceasefire holds in name but both sides are still seizing vessels.

- Fed: DOJ dropped the Powell probe Friday; Tillis ended his block on Warsh Sunday. Senate Banking Committee votes Wednesday. Markets price ~8 bps of cuts through year-end. FOMC meets next week.

- CFO/Treasurer: Fixed-rate issuance window remains open but is no longer improving. Stress-test floating-rate exposure for a 10-year sustained at or above 4.30%.

Market Snapshot

- Brent Crude:

- ~$104 / bbl

- WTI:

- ~$95 / bbl

- 10-Yr Treasury:

- 4.31%

- 2-Yr Treasury:

- 3.78%

- Yield Curve (2s10s):

- +53 bps

- Gold:

- ~$4,722 / oz

- Fed Funds Target:

- 3.50–3.75%

- Next cut priced:

- ~8 bps priced through year-end

Hot Headline, Patient Core, and a Cleared Runway

"The spike in headline inflation is the noise. The underlying trend is the signal. The hard part is determining which price measure best reflects the trend." — Reflecting on Warsh's Senate testimony

This past week was light on key economic data but heavier on geopolitics and policy shifts. March retail sales surprised to the upside. Gasoline station receipts rose with pump prices, the same 21% gasoline surge captured in the March CPI report. Core retail sales jumped 0.7%, showing more resilience than expected and sending Q1 GDP forecasts higher. After testing lower levels, long-end Treasury yields held at 4.31%. On the policy front, the Justice Department dropped its criminal probe of Chair Powell, and the Strait of Hormuz remains effectively shut. The story is no longer about a Fed easing cycle. It is about whether the United States can keep its economy steady through an oil shock, an active naval blockade, and a leadership transition at the central bank.

Equities finished the week at record highs while bonds priced essentially no Fed cuts through year-end. The two markets are looking at the same set of inputs and arriving at materially different conclusions. Brent settled near $104 after touching highs above $109. Gold ended near $4,722, off about 3% on the week as the indefinite ceasefire extension softened the safe-haven bid. Retail gasoline is over $4 per gallon. Consumer sentiment hovers near record lows even as the hard data is coming in well ahead of expectations.

Source: BLS and Federal Reserve Bank of Cleveland

The Macro Backdrop

Retail sales for March came in well above expectations. Headline rose 1.7% versus the 1.4% consensus, and the control-group measure that feeds GDP rose 0.7%, the strongest since August. Tax refunds running roughly 17% above last year are doing meaningful work, offsetting the initial bite from higher gasoline prices. Nonstore retailers led the gain. Restaurants and bars eked out a small increase but have been roughly flat for the quarter, which bears watching as a discretionary-spending bellwether. The composite picture is a capital-led expansion with a steady consumer, slower hiring, and output that has held up better than sentiment.

The labor market has normalized rather than weakening further. The Beige Book described employment as flat to slightly up across most districts, with wages still in the modest-to-moderate range. Balance sheets are thinner than a year ago but not stretched. The forward question is whether the war-related inflation impulse begins to flow through to discretionary categories in Q2. So far, it has not. The University of Michigan sentiment index sits near a record low at 49.8, but the hard data has yet to roll over. That divergence is the central tension going into next week's Q1 GDP and PCE prints.

Source: U.S. Census Bureau

Geopolitics & Energy Markets

The geopolitical backdrop is no longer fluid. It is structurally hostile. Following the February 28 air war and the death of Supreme Leader Khamenei, Iran closed the Strait of Hormuz. The U.S. responded with a naval blockade of Iranian ports beginning April 13, now entering its third week. President Trump extended a fragile ceasefire on April 21 but talks collapsed Saturday when he called off sending Witkoff and Kushner to Pakistan after Iran's foreign minister left Islamabad. On Monday, Iran offered through Pakistani mediators to reopen the strait in exchange for the U.S. lifting its blockade and ending the war, with nuclear talks deferred to a later phase; Trump signaled the offer was unlikely to be accepted, telling Fox News "we have all the cards." The dueling blockades remain in place. Both sides are seizing commercial vessels. President Trump last week ordered the Navy to "shoot and kill" any Iranian boat caught laying mines in the strait. The IEA this week characterized the disruption as the largest energy supply shock on record.

Roughly 20% of seaborne crude and LNG normally moves through Hormuz; current traffic is near zero. Brent traded near $104 by Friday on cautious ceasefire optimism but pushed back above $108 in Monday trading after the weekend talks collapsed, nearly 50% above pre-war levels. U.S. retail gasoline, which had been falling slightly, is back over $4 per gallon, compared to roughly $3 before the conflict. Consultancy and trader estimates put cumulative global oil draws since the start of the shock at 500 to 700 million barrels. Aviation reroutes have lengthened journey times across Europe-Asia corridors. Gulf Cooperation Council economies are under acute pressure, with Bahrain having required emergency UAE central-bank support earlier this month.

Supply-chain consequences extend beyond oil. Fertilizers, industrial gases, ammonia, and freight insurance are all exposed. War-risk premiums for Hormuz transits jumped from 0.125% to 0.2 to 0.4% of insured value before traffic stopped entirely. These pressures typically appear first in margins, then in prices, with a one-to-two quarter lag. The composition of the inventory picture matters more than the total. The U.S. is not short of crude in storage; it is increasingly tight in refined products, particularly diesel and middle distillates. Those are the bloodstream of freight, industry, agriculture, and aviation.

The supply-side math is starker than the headline price suggests. Consensus estimates put April global oil inventory draws at 11 to 12 million barrels per day, a record pace by a wide margin. Persian Gulf production losses are running near 14 to 15 million barrels per day. Most forecasters now project the global market swings from a small surplus in 2025 to a deficit of 8 to 10 million barrels per day in Q2, before any meaningful recovery in Gulf flows. Even in the most benign scenarios where the strait reopens by mid-June, global visible inventories are expected to reach the lowest level on record since satellite tracking began in 2018. The price one sees is the price after policy responses, sanctioned-oil releases, SPR draws, and demand destruction. Without those buffers, the price would be substantially higher.

The base case is that the ceasefire holds and a negotiated reopening of the strait eventually occurs. The risk case is escalation through miscalculation in a contested waterway with active blockades on both sides. Markets are priced closer to the base case than the risk case, particularly in equities. The Trump administration's incentive to lower energy costs ahead of the midterms argues for a path to de-escalation, but Iran's leverage from holding Hormuz is greatest precisely now. The window for a negotiated arrangement is real, but it is not wide. We expect the outlines of an agreement to come together by late May. The Memorial Day weekend marks the kickoff of the summer driving season and the unofficial start of summer in the U.S., and political pressure to ease retail gasoline prices will be at its peak. Nailing down the specifics will likely carry into June.

Europe remains the most exposed downstream economy. Qatar's LNG disruption has driven European benchmark gas prices sharply higher and regional storage remains critically low. A prolonged disruption strengthens Russia through higher energy revenues, complicates European support for Ukraine, and reminds investors that the continent's strategic ambitions remain well ahead of its energy security. History has a habit of sending the bill twice.

Source: Energy Information Administration (EIA)

Markets & Financial Conditions

Stocks and bonds rarely agree, but they rarely disagree by this much. The S&P 500 and Nasdaq closed Friday at record highs while the 10-year Treasury sat at 4.31%, near a one-week high. Both markets are looking at the same set of inputs and pricing them in fundamentally different ways. The list is familiar by now: the war, the inflation impulse, the Fed transition, the consumer, and the AI capex cycle. The equity bull case rests on three assumptions: that the ceasefire holds, that energy stabilizes, and that AI proves a net stimulus to growth rather than a near-term disruption to labor markets and capital allocation. Bonds are not convinced on any of the three. The divergence itself is unremarkable. The size of it is.

The 10-year ended the week at 4.31%, the 2-year at 3.78%, the 30-year at 4.91%. The curve is positively sloped by 53 basis points. Three forces are pushing long-end yields. First, energy prices are keeping inflation expectations sticky; the Michigan one-year measure sits at 4.7%. Second, term premium continues to rebuild on persistent deficits and heavy issuance. Third, geopolitical risk is being priced as a duration risk, not a flight-to-quality story, which is unusual and worth noting.

The bond market's caution looks well-grounded. Even forecasters most concerned about the war's persistent effects expect Brent to ease toward roughly $90 by year-end as Gulf flows recover, with risks tilted to the upside. That is below current spot but well above the long-run average, and it is consistent with sticky inflation expectations and a Fed that cannot ease quickly without losing credibility. The shape of the curve fits that path. Equity index pricing assumes a smoother return to normal.

The Justice Department's Friday decision to drop its criminal probe of Chair Powell removes the principal hurdle to Warsh's confirmation. Senator Tillis announced Sunday he will end his block on the nomination, and the Senate Banking Committee is scheduled to vote on Wednesday at 10 a.m. ET. With Republican Banking Committee members outnumbering Democrats 13 to 11, Warsh is expected to advance to the full Senate, with confirmation likely in time to chair the June FOMC meeting. Powell's term as Chair ends May 15. Markets read Warsh's confirmation testimony as more hawkish than expected. Fed-funds futures price roughly 8 basis points of cuts through year-end. The probability of a move at the April 28–29 FOMC meeting is effectively zero.

Gold finished the week near $4,722 per ounce, down roughly 3% on the week as the indefinite ceasefire extension softened the safe-haven bid. The metal has now given back about 10% from its post-war peak, which is itself a useful signal. The market is not pricing the war as a regime change. It is pricing it as a fat-tailed but bounded disruption.

The funding-side conclusion is straightforward. The opportunity to lock in fixed rates remains, but conditions are no longer improving. Firms with floating-rate exposure should reassess downside scenarios where the 10-year remains at or above 4.30% through year-end. The market is demanding more compensation for duration, and that tends to persist.

Source: Bureau of Economic Analysis (BEA) and Federal Reserve Bank of Dallas

Piedmont Perspective: Warsh, Measurement, and the Stance of Policy

It is worth pausing on inflation this week, because the conversation about it has become muddled. Headline CPI is being pushed around by an oil shock. Core CPI is doing what it has done for the better part of a year, drifting slowly in the right direction. The Cleveland Fed's median CPI and 16% trimmed-mean CPI each rose 0.2% month-over-month in March, the same as core, suggesting the underlying signal is unchanged by the war.

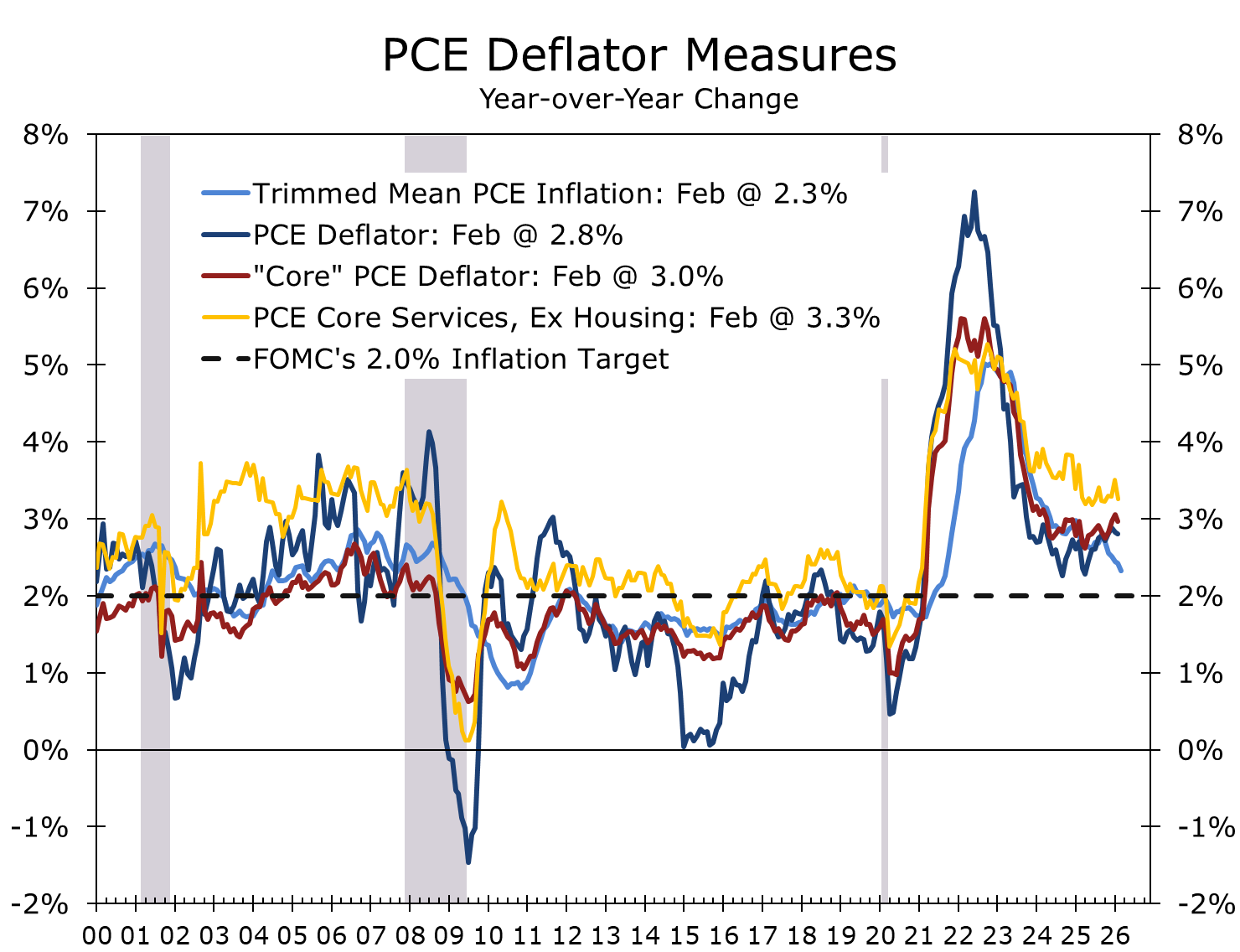

The Dallas Fed's trimmed-mean PCE, the cleanest filter on the FOMC's preferred index, ran at 2.3% year-over-year through February, against a 2.8% headline PCE and a 3.0% core PCE. Strip out the energy distortion and a single core read carrying more noise than signal, and the trend is reasonably benign.

Three points are worth making, each tied to themes Kevin Warsh laid out in his Senate testimony this week. First, the 2% target may be more aspirational than descriptive. CPI inflation has averaged roughly 2.7% per year from 1990 through today — the disinflationary era, the period most often invoked as the proof of concept for inflation targeting. Even with all of that pulling the average down, the long-run number sits well above 2%. The Fed has not spent nearly as much time at target as the casual narrative suggests.

Second, what the Fed measures matters as much as what it targets. Warsh dismissed core PCE as "a rough swag" and called for newer methodologies. The work has been there for two decades: the Cleveland Fed's median and trimmed-mean CPI and the Dallas Fed's trimmed-mean PCE. Cleveland's own research has shown median CPI to be a better forecaster of future PCE inflation than core PCE itself. Third, policy is restrictive but only modestly so. With funds at 3.50–3.75% and the better trend measures of inflation running between 2.3% and 2.6%, the implied real rate sits roughly 1.0 to 1.4 percentage points above zero. That is restrictive, but not punishingly so. The room for cuts is narrower than markets have been hoping for but in line with our expectations.

Fourth, Warsh's framework includes a structural optimism that has not received enough attention. He has argued that AI is boosting the economy's supply side and will deliver large productivity gains and called for the Fed to do considerable additional work to assess the productivity boom. This view could hardly be labeled hawkish. It connects directly to the equity bull case discussed above and complicates a simple read of Warsh as restrictive. A central banker who believes the economy's potential is rising should, all else equal, tolerate higher actual growth without pulling rates higher. The implication is that the gap between Warsh's framework and Powell's may be narrower than markets are pricing, particularly if the labor market remains close to full employment, as Warsh characterized it in his testimony. Warsh has room to cut rates. The real test will come once the economy moves past the Iran War distractions and growth firms as inflation moderates. We expect a Warsh Fed to let the economy run hot a bit, particularly if growth is being driven by capital spending, which raises the speed limit for potential growth.

CFO & Treasurer Corner

What This Means for Corporate Finance

Funding & Liquidity: The fixed-rate issuance window remains open. The trajectory is no longer improving. Markets price almost no Fed cuts through year-end and term premium continues to rebuild. The case for locking in fixed-rate financing is strengthening. Floating-rate borrowers should review covenant headroom and stress-test interest coverage if the 10-year holds above 4.30% through year-end.

Energy & Input Costs: Brent has settled near $104 after briefly touching highs above $109. Diesel and middle distillates remain the choke point. Firms with exposure to freight, logistics, or petrochemical inputs should stress-test 2026 cost assumptions now. The window to pre-buy or hedge inputs may be short. Fertilizer and LNG-linked supply chains require immediate review.

Working Capital: Higher energy and freight costs are creating a slow-moving squeeze on working capital. Transportation and warehousing firms absorbed the first wave. Consumer goods and industrial firms are next. Just-in-time supply chains with limited inventory buffers face the greatest risk. Margin pressure is likely to build in Q2 and Q3, even as headline retail spending holds up.

Planning Assumption: Base case. Ceasefire holds and a negotiated path eventually reopens Hormuz. Brent stabilizes in a $95 to $110 range by June and then eases over the summer. The market generally begins to build in rate cuts over the summer, and the Fed follows through with a quarter point cut in September, followed by another quarter-point cut at the December FOMC meeting. GDP growth runs around 2.5%, driven largely by capital spending, stabilization in residential investment, inventory building, and a resilient consumer. Stress case. Blockade persists or escalates through Q3. Brent rises to $120 to $140. Headline CPI re-accelerates above 4%. Credit spreads widen 50 to 75 basis points. Build both scenarios into Q2 board discussions.

Looking Ahead

| Day | Release / Event | Why It Matters for CFOs & Markets |

|---|---|---|

| Monday | Dallas Fed Manufacturing Activity (April); Treasury QRA preview | Regional Fed surveys are the cleanest read on whether the war's cost impulse is showing up in firms' prices and capex plans. Treasury's quarterly refunding announcement will set issuance tone for Q2. |

| Tuesday | S&P CoreLogic Case-Shiller home prices (Feb); JOLTS (March); Conference Board Consumer Confidence | JOLTS will inform the labor-market normalization story. Confidence has lagged the hard data badly; convergence in either direction is the question. Case-Shiller will speak to shelter inflation, which has been the dominant disinflationary force in core CPI. |

| Wednesday | FOMC Day 1; ADP Employment; Q1 GDP advance estimate; Treasury Refunding Announcement | Q1 GDP is the consumer story rendered as one number. Nowcasts have diverged: Atlanta GDPNow sits at 1.2% as of April 21 while the St. Louis Fed and Survey of Professional Forecasters cluster nearer 2.3 to 2.6%. Energy-shock effects on Q1 are limited because the bulk of the price impulse hits in Q2; the surprise risk lies in revisions and inventories rather than the consumer headline. Treasury issuance composition matters as much as the totals; longer duration in the issuance mix would add term-premium pressure. |

| Thursday | FOMC Decision and Powell Press Conference; ECI (Q1); Initial Claims | This may be Powell's last meeting as Chair. Watch for tone on inflation measurement, the war, and any signal on his future on the Board of Governors. ECI is the cleanest read on labor cost pressures and matters to the underlying inflation story. Q1 often is the highest print of the year. |

| Friday | PCE & Personal Income/Spending (March); ISM Manufacturing (April) | Friday's PCE is the most important data point of the week. The Dallas Fed trimmed-mean PCE update will arrive with it; a stable trend reading near 2.3% would reinforce the case that underlying inflation is contained even as headline runs hot. ISM provides the other side of the picture. Look for evidence of growing supply chain strains and margin pressure. |

The interpretation of next week's data will matter more than the numbers themselves. The headline narrative — strong consumer, hot inflation, Fed on hold — is largely settled. The unsettled questions are whether the labor market continues to normalize without breaking, whether the better measures of underlying inflation continue to drift lower, and whether the Powell-to-Warsh transition introduces volatility into long-end pricing. The shoals are visible. The task ahead is to navigate them.

Scenario Framework

| Scenario | Macro & Market Implications | Corporate Finance Action |

|---|---|---|

| Base Case (50%) | Sloppy ceasefire holds; phased Gulf reopening from mid-May through end-June; Brent settles near $90 by Q4 with risks skewed higher; Fed on hold through summer with one to two cuts likely in H2 if underlying inflation cooperates; GDP near 2.5%; headline CPI peaks above 3.5% in Q2, then moderates toward 3% by year-end. | Lock in fixed-rate maturities now. Stress-test energy and freight in 2026 budgets. Maintain liquidity buffers above minimums. Use this period of relative calm to prepare for the alternatives. |

| Downside (30%) | Blockade persists or escalates through Q3; Brent $120–130; headline CPI re-accelerates above 4% with stickiness in core; credit spreads widen 50–75 bps; Fed pinned with no cut path. | Accelerate issuance ahead of wider spreads. Model demand destruction in revenue forecasts. Limit new floating-rate exposure. Revisit dividend and buyback assumptions. |

| Tail Risk (20%) | Direct strike on Gulf energy infrastructure or full Hormuz closure into Q4; Brent $140+; global recession risk rises sharply; dollar surges; EM stress; equity drawdown of 15–20%+. | Maximize liquidity; draw revolvers preemptively; halt discretionary capex; model severe demand contraction; review counterparty exposure in EM and energy-importing economies. |

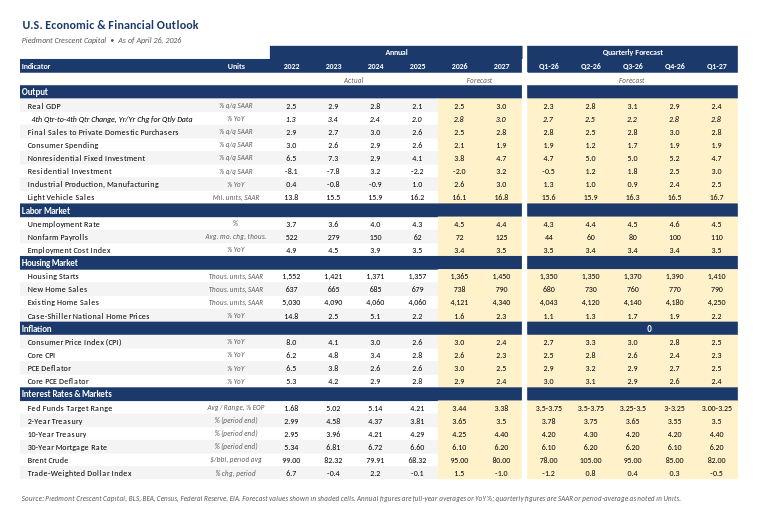

US Economic & Financial Outlook

Source: Piedmont Crescent Capital, BLS, BEA, Census, Federal Reserve, EIA. Forecast values shown in shaded cells. Annual figures are full-year averages or YoY %; quarterly figures are SAAR or period-average as noted in Units.

Piedmont Crescent Capital · April 26, 2026 · For informational purposes only. Not investment advice.