Key Takeaways

-

- Home price appreciation continued to decelerate in early 2026, with both S&P CoreLogic Case-Shiller Home Price Index and FHFA House Price Index showing low-year-to-year single-digit gains.

- Monthly momentum is soft. Prices are drifting higher on a seasonally adjusted basis but slipping slightly on an unadjusted basis.

- Regional divergence has widened. The Midwest and Northeast are now leading, while several Sun Belt markets are flat to declining. Florida is a notable soft spot.

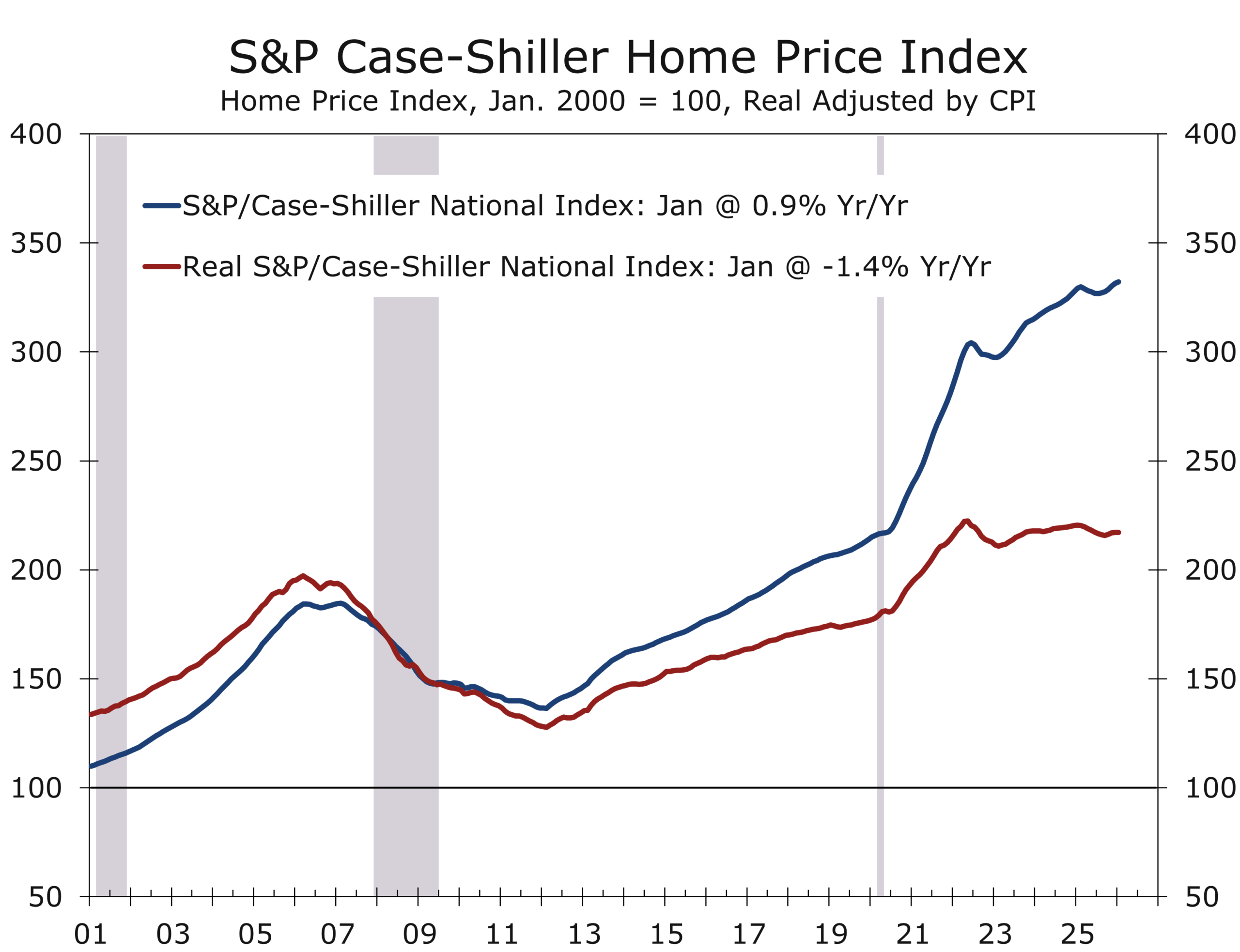

- Real home prices are falling modestly as inflation runs ahead of nominal appreciation.

- The housing market remains constrained by affordability. Higher mortgage rates are offsetting any benefit from slower price growth.

Price Growth Is Positive, But Fading

January’s data reinforces a theme that has been building for several quarters: the housing market has cooled but the overall supply of homes for sale remains tight, which is supporting home prices.

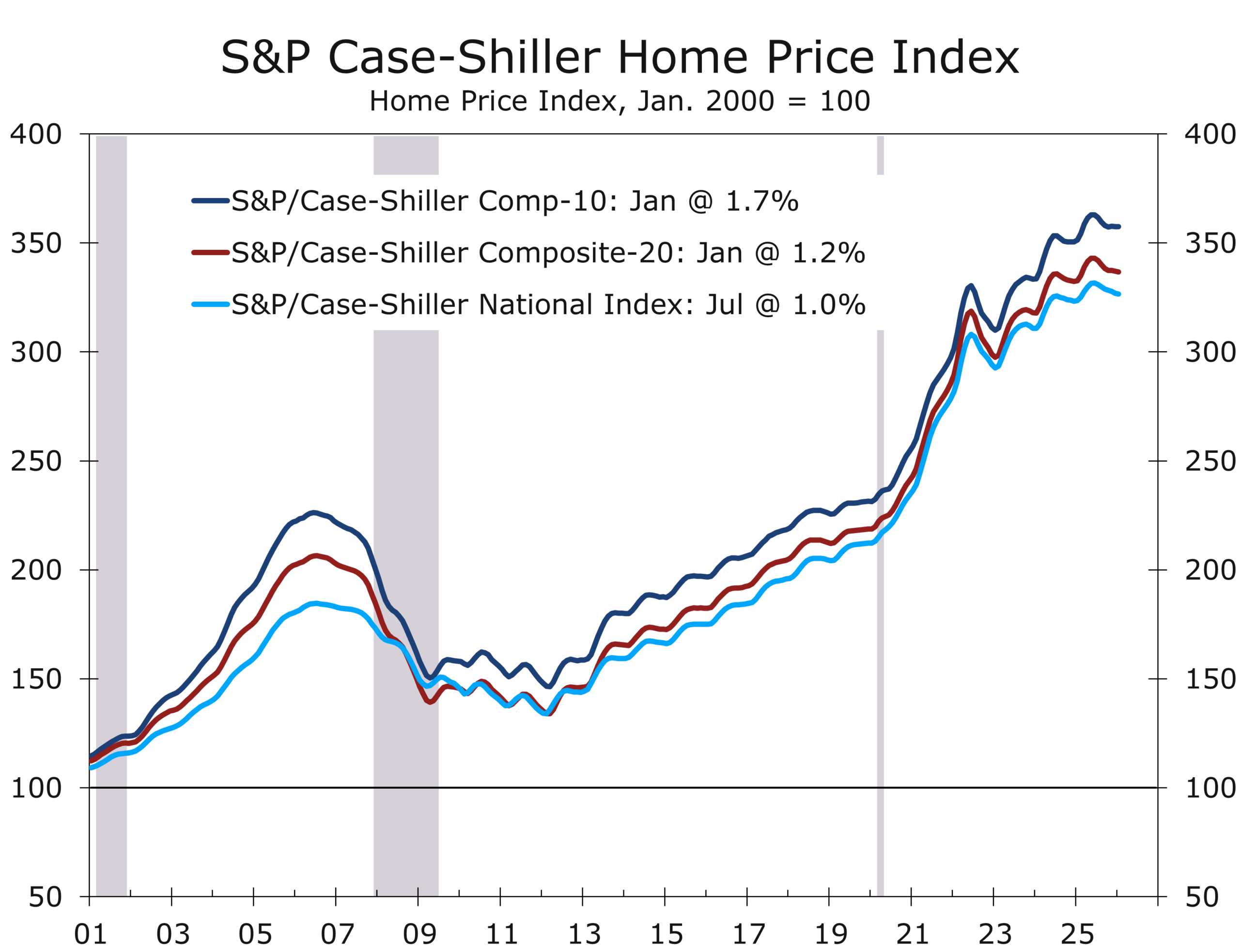

The S&P CoreLogic Case-Shiller Home Price Index rose 0.9% year over year in January, down from 1.1% in December. The 10-city and 20-city composites slowed to 1.7% and 1.2%, respectively. The FHFA House Price Index showed a similar pattern, rising 1.6% year over year, with a modest 0.1% monthly gain.

The signal is clear. Home prices are still rising, but only marginally. The market has shifted from strong price appreciation to something closer to stall speed as demand remains constrained by affordability constraints and a weaker job market

Nominal home price appreciation has slowed enough that inflation is now outpacing home prices.

On a monthly basis, the Case-Shiller national index declined slightly on a non-seasonally adjusted basis and rose just 0.2% after seasonal adjustment. FHFA reported a similarly modest 0.1% increase.

This is not the profile of a market under stress. It is the profile of a market constrained to the point that it is stalling. Buyers are sensitive to monthly payments, not just prices, and the recent back up in mortgage rates has likely caused many would-be buyers to pause.

The result is a low-velocity market. Transactions are limited, inventories are gradually rising off historically low levels, and prices are drifting rather than moving decisively in either direction.

Regional Divergence Is Now the Defining Feature

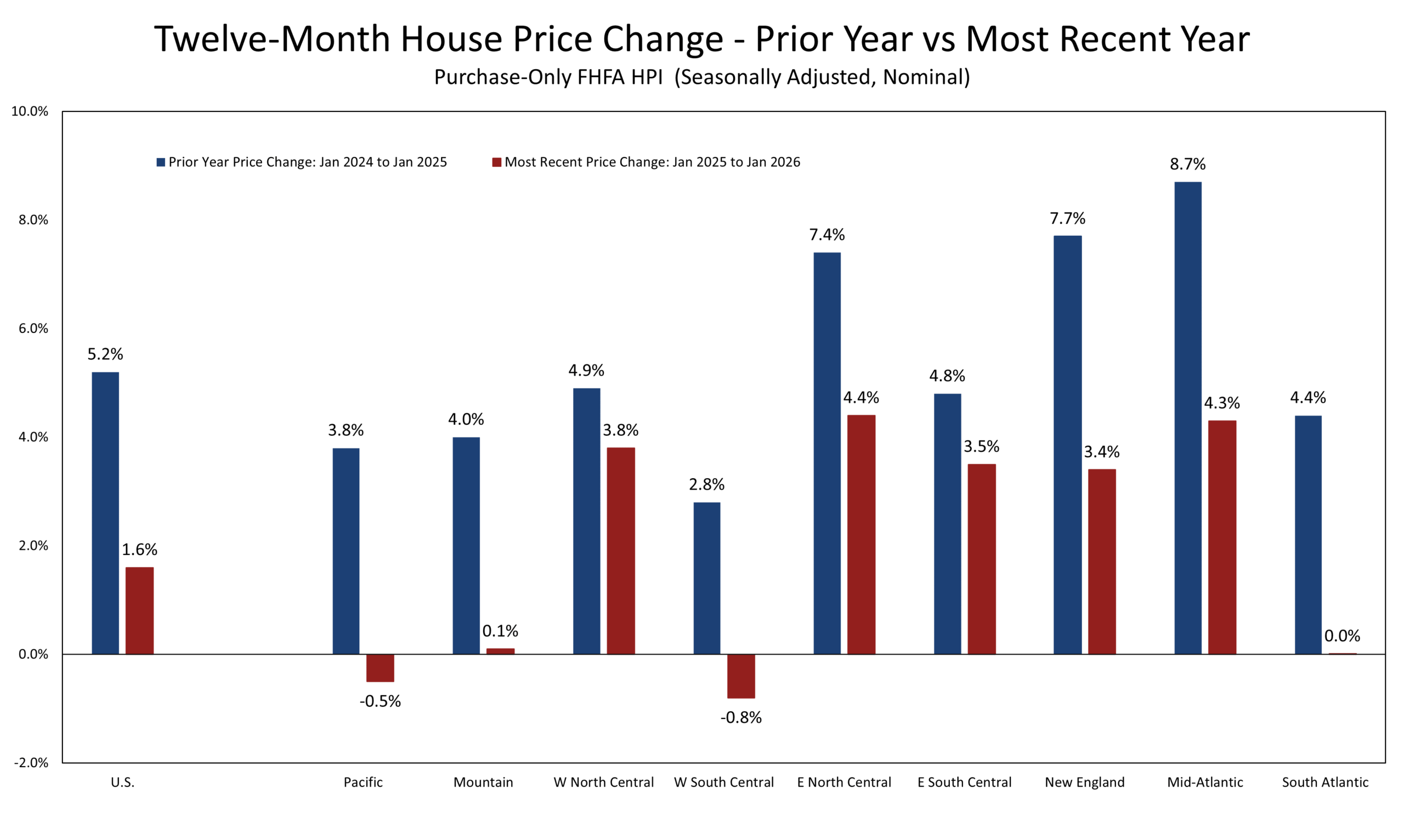

Variations in regional price performance offer confirming evidence on the most recent Census data, which should population growth remaining strong Texas, the Mountain West and the Southeast, with the exception of Florida. The Midwest is showing more resilience, as housing is relatively more affordable compared to other regions. New York’s prices reflect the full return to the office amid a scarcity of homes available for sale.

In the Case-Shiller 20-city index, New York, Chicago, and Cleveland posted the strongest gains, while Tampa remained firmly negative year-over-year. Prices were flat or down in several formerly high-flying Sun Belt markets, including Phoenix, Dallas, and Seattle.

Leadership has shifted from Sun Belt hot spots to the Midwest, Northeast, and more affordable parts of the South.

FHFA’s regional data tell the same story. The East North Central division posted the strongest annual gains, while West South Central, which includes Texas, was negative. The East South Central, which includes Tennessee and Alabama, shows more resilience, however.

The pandemic-era leaders are no longer carrying the market. Instead, price growth has rotated toward regions where affordability remains less strained, and valuations did not overshoot as dramatically.

Real Prices Are Quietly Declining

With the CPI running above the pace of home price appreciation, inflation-adjusted values have edged lower over the past year. This marks a notable shift from the prior two years, when housing was a primary driver of household wealth gains.

Real home prices are declining modestly, even as nominal prices remain positive.

This adjustment is doing some of the work that outright nominal declines would otherwise accomplish. It is easing valuation pressures, albeit slowly and unevenly.

Despite the moderation in price growth, affordability has not meaningfully improved. Mortgage rates remain elevated, and in recent weeks have moved higher alongside Treasury yields. That keeps monthly payments high and limits the pool of qualified buyers.

This dynamic explains why slower price growth has not translated into stronger activity. The constraint is not price levels alone, but the cost of financing those prices. The market is caught between two forces: limited supply from rate-locked homeowners and constrained demand from payment-sensitive buyers.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 31, 2026

Mark Vitner, Chief Economist

(704) 458-4000