A 21st-Century Energy Shock: A Stress Test for the West

- The joint U.S.–Israeli strikes against Iran and the expanding conflict involving Hezbollah in Lebanon have introduced a new geopolitical shock to the global economy. The principal transmission channels are higher energy prices, tighter financial conditions, weaker consumer confidence, larger budget deficits, and greater uncertainty around capital investment.

- The confrontation stems from a long-running regional conflict that intensified following the October 7 attacks on Israel. Iran’s support for militant proxy networks across the Middle East and its direct role in planning and training the October 7 attacks made a direct confrontation inevitable, particularly after Israel systematically dismantled Iran’s key proxies: Hamas and Hezbollah.

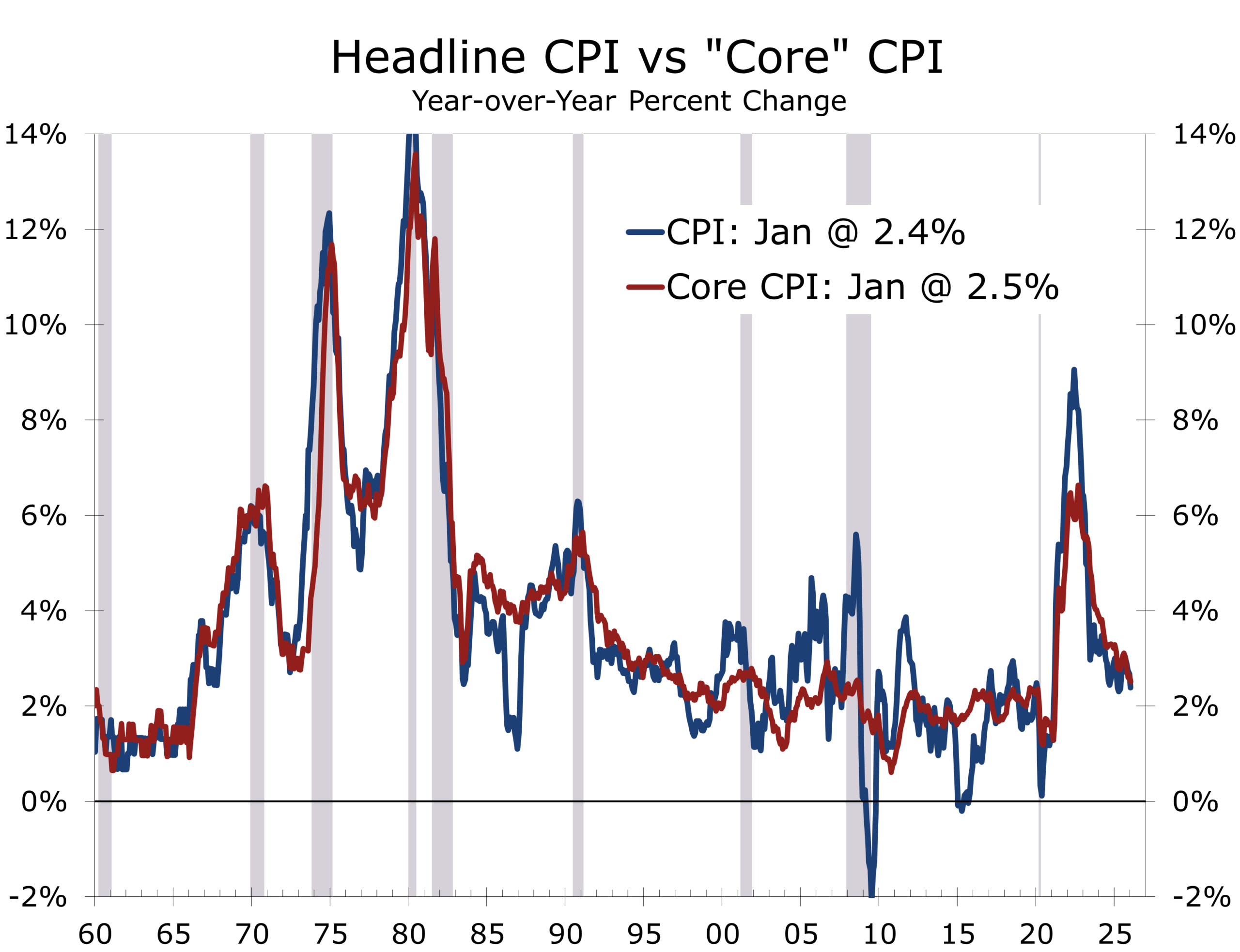

- The shock remains largely concentrated in energy markets. Higher oil prices will likely lift headline inflation during the first half of the year while slowing economic growth modestly.

- Headline PCE inflation could run roughly 5 percentage point higher than previously expected, while core PCE may rise about 0.2 to 0.3 percentage points more than earlier thought. The increase is meaningful but not transformative, particularly since most of the adjustment occurs early in the year.

- Economic growth is likely to slow modestly, reflecting softer consumer spending on durable goods and some delays in capital investment.

- Structural changes in the global economy should limit the risk of a sustained inflation spiral. The U.S. economy is far less energy-intensive than in the 1970s and domestic energy production is far higher. Moreover, today’s modern monetary policy framework emphasizes maintaining inflation credibility.

- One secondary risk lies in credit markets. Elevated energy prices and tighter financial conditions amplify the ripples with private credit and modestly restrain capital investment.

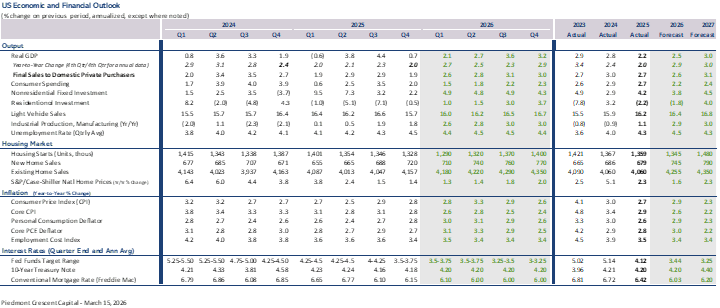

- Our baseline outlook remains one of continued expansion, though with slower growth, fewer near-term rate cuts, and greater financial market volatility. Real GDP is expected to rise 2.9% in 2026, while the headline PCE deflator rises 2.6% and the core PCE deflator rises 2.5% (all Q4/Q4 basis).

The Geopolitical Shockwave

The joint U.S.–Israeli military campaign against Iran and the widening conflict involving Hezbollah in Lebanon have introduced a new layer of uncertainty into the global economic outlook. The macroeconomic consequences are being transmitted primarily through higher energy prices, tighter financial conditions, declining consumer confidence, increased budget deficits and Treasury issuance, and greater uncertainty surrounding business investment decisions.

The risk is not today’s oil spike, but tomorrow’s supply disruption

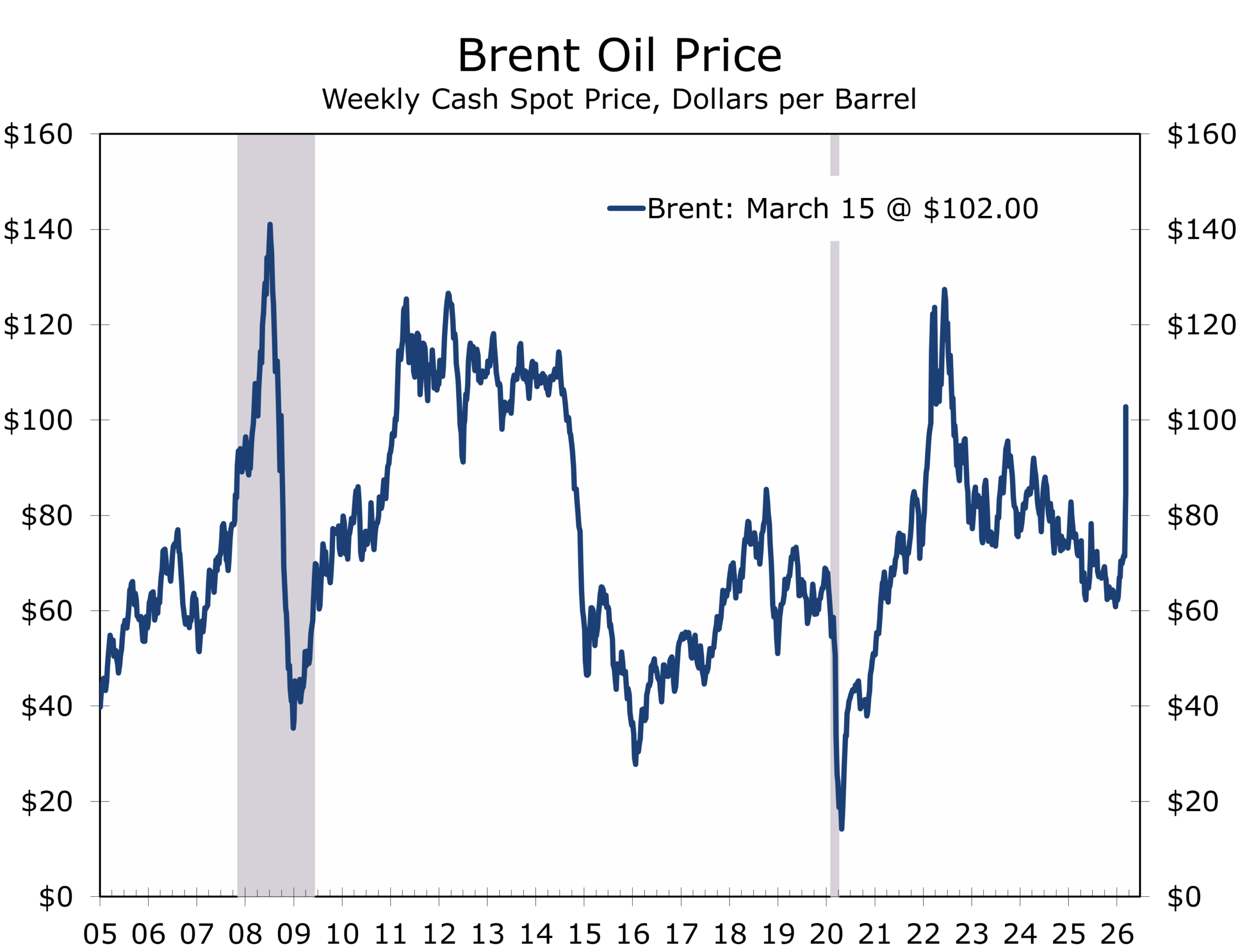

The key question is not whether the shock will affect the global economy but whether it remains contained within energy markets. Financial markets have spent the past few weeks debating whether the conflict could evolve into a broader disruption to global supply chains and financial conditions. Those concerns appear overstated for now. Energy markets entered the crisis oversupplied, a factor that has kept oil prices from surging beyond roughly $120 per barrel.

The conflict itself has deep roots. Iran has spent decades cultivating proxy forces throughout the region, including Hezbollah in Lebanon and Hamas in Gaza. Regular readers of our publications will note that we have long warned that a direct conflict between the U.S. and Iran was a virtual certainty. The October 7 attacks crossed many lines, dramatically escalating tensions and accelerating a trajectory toward direct confrontation that had been building for years. While Israel is the primary target today, a similar attack in the U.S. is a key Iranian objective.

The regional dimension of the conflict is already evident. Hezbollah has launched rockets into northern Israel from Lebanon, while Israeli forces have conducted retaliatory strikes against Hezbollah positions across southern Lebanon and areas surrounding Beirut. The conflict now effectively spans multiple fronts across the region.

The economic implications extend far beyond the battlefield. The Middle East remains central to global energy markets and international shipping routes. Roughly one-fifth of global oil flows pass through the Strait of Hormuz, making it one of the most strategically significant energy chokepoints in the world. A durable resolution to the conflict will ultimately require removing this threat permanently.

For now, spillovers beyond energy markets remain limited. Oil prices have risen sharply, but the broader global supply chain disruptions seen during the pandemic have not reappeared and are unlikely to do so. Shipping costs outside tanker markets remain relatively stable, and industrial supply chains remain largely intact.

Energy shocks tend to lift headline inflation quickly but fade over time. The expected increase in inflation this year appears meaningful but temporary, concentrated primarily in the first half of the year.

Even so, higher energy prices will push inflation somewhat higher and slow growth modestly. Headline PCE inflation may run roughly half a percentage point higher than previously expected, while core inflation may rise about 0.2–0.3 percentage points faster than previously expected. Most of the adjustment is likely to occur during the first half of the year.

The U.S. economy entered this episode with more underlying momentum than recent headline data suggest. Real incomes continue to rise, the labor market remains stable, and layoffs remain historically low. The January data might overstate the economy’s resilience, however. Personal income has a tendency to rise solidly in January and give back most of those gains in following months. The seasonal quirk is likely a legacy of the Pandemic. Hence, recent after-tax income growth and saving rate may currently overstate the resilience of consumer spending.

Momentum remains intact, but seasonal noise and demographics are distorting the data

February’s payroll numbers nearly reversed all of January’s downwardly revised gain. Hiring was impacted by the return of winter weather, strikes in the healthcare sector, and some larger than expected reversals in sectors boosted by the holiday season, such as couriers and delivery workers. The data are also being weighed down by federal retirements. We believe the ADP private sector payroll data, which rose by 63,000 in February and an average of 27,000 jobs per month over the past year and are less impacted by strikes and some season distortions, currently provide a better read on the state of the labor market.

While hiring has slowed, Demographic forces are reshaping the labor market. Slower population growth and reduced immigration have reduced the supply of labor, lowering the pace of payroll gains required to maintain a stable unemployment rate. In this environment, slower job growth does not necessarily signal economic weakness. A low unemployment rate, however, does not necessarily signal a strong labor market.

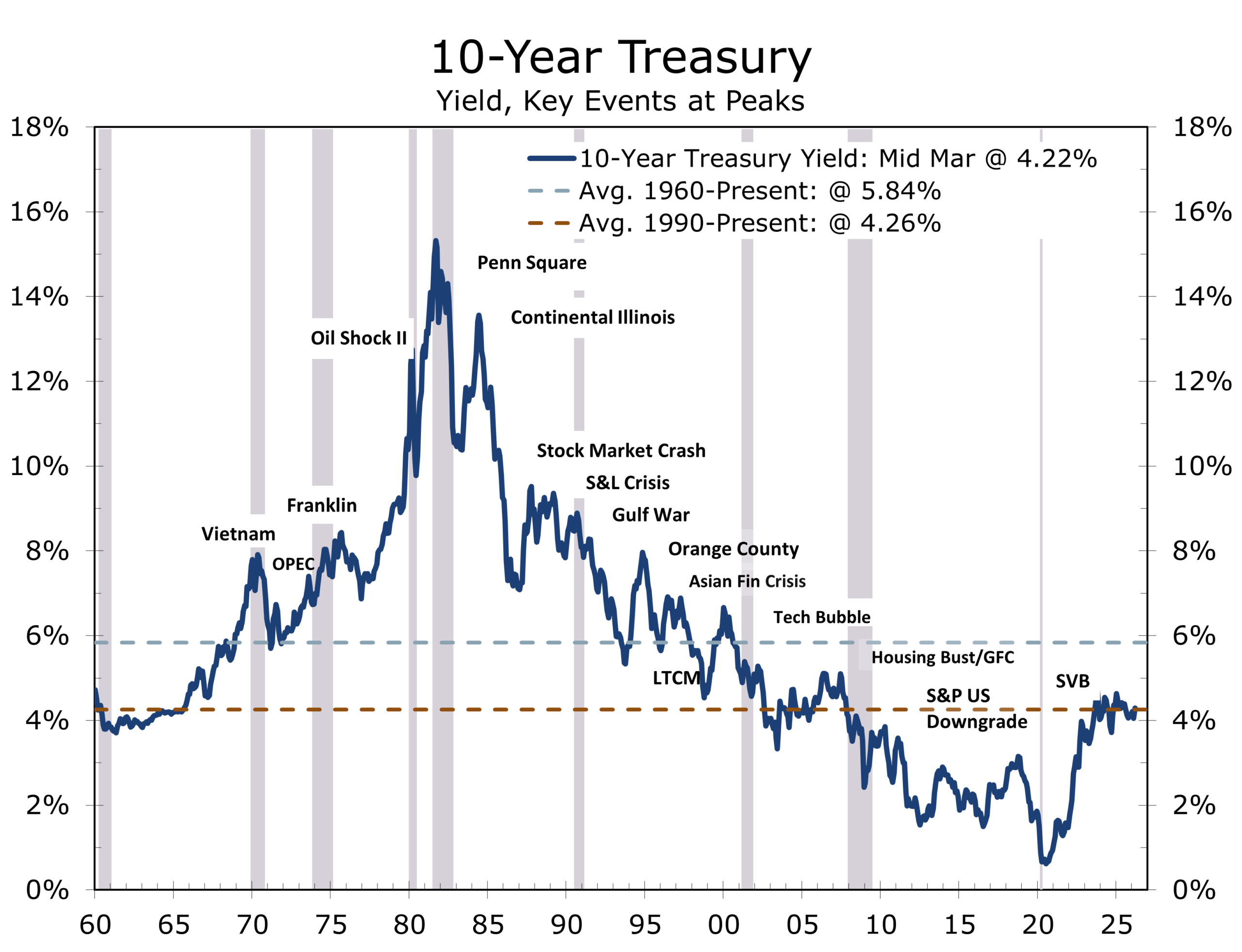

The bottom line for consumers and the broader economy is that higher energy prices reduce real purchasing power (income effect) and complicate the task facing central banks. Monetary policymakers must balance the inflation impulse from energy prices against the risk that tighter financial conditions slow economic activity. We feel the Fed is still likely to ease, with its primarily motivation being to return monetary policy to neutral. Right now, the next Fed rate cut looks like it will be in September, but an earlier cut is possible if the job growth begins to lose significant momentum.

Transmission Channels

Energy shocks affect the economy through several key mechanisms. In economics the key terms are the income effect and substitution effect.

The most immediate transmission channel is oil prices. Energy markets responded quickly to the escalation of hostilities, reflecting both supply risks and concerns about shipping through the Strait of Hormuz. Even with ample current supplies, markets are forward-looking, effectively pricing the next marginal barrel of oil or shipment of natural gas.

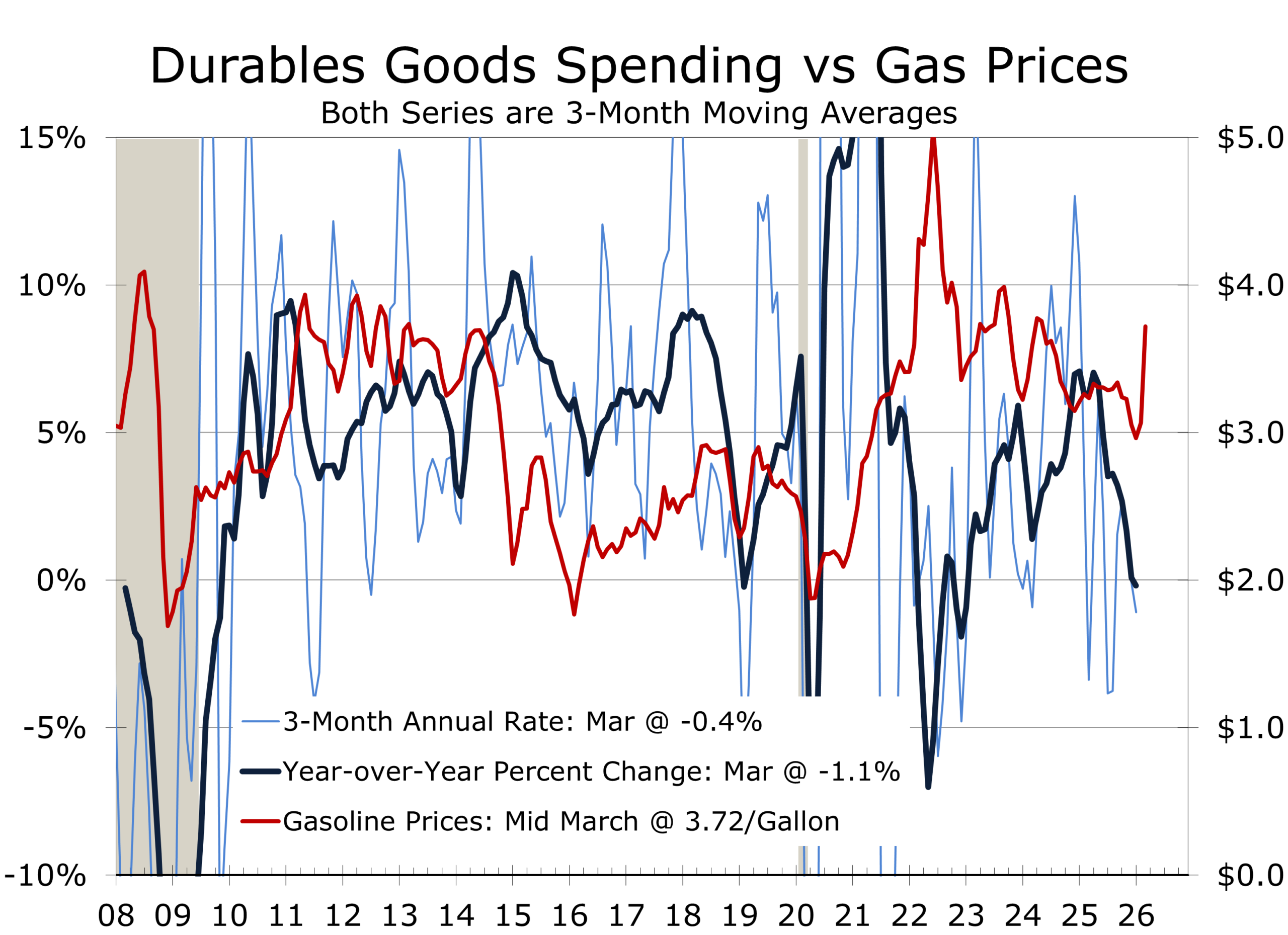

Energy shocks historically weaken durable goods demand first, as households postpone large purchases such as vehicles, furniture and appliances.

Higher gasoline and utility cost’s function much like a tax on economic activity. They reduce household purchasing power and shift spending away from discretionary categories (Income effect).

Durable goods spending is particularly sensitive to these shifts. Purchases of vehicles, appliances, and other large-ticket items often weaken when energy prices rise (Substitution effect).

A second transmission channel is consumer confidence. Energy prices are highly visible and often shape household perceptions of the broader economy.

A third channel involves business investment. Firms frequently delay or stage large capital expenditures during periods of geopolitical uncertainty.

Finally, financial conditions can tighten as investors reassess risk and Treasury issuance increases to finance to war, pushing borrowing costs higher across credit markets.

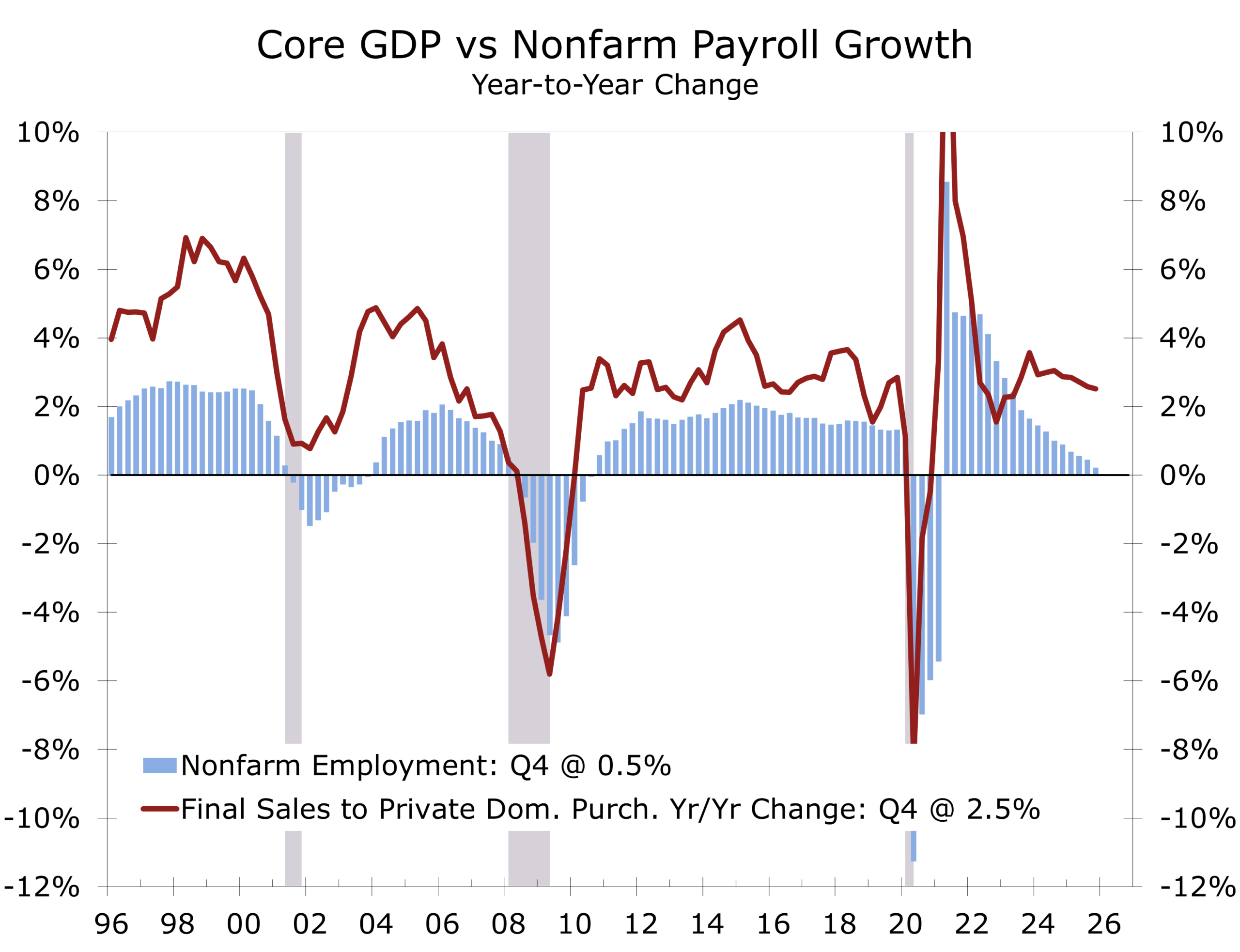

Private domestic final sales rose at a 1.9% annual rate in Q4 and are up 2.5% year-to-year, only modestly below the pace in the third quarter. Consumer spending slowed but remained positive. Business fixed investment increased at a solid clip, led by intellectual property and equipment. Residential investment continued to contract, underscoring that housing remains a lagging sector in this cycle. The composition of growth matters more than the disappointing 1.4% headline Q4 real GDP growth print.

Capital deepening is the primary growth engine, resulting in a capital-led, job-light expansion

This is increasingly a capital-heavy, job-light expansion. Equipment, software, and R&D spending remain firm, particularly in AI-linked sectors. Hiring, by contrast, has moderated materially. Job growth in 2025 was the weakest of any non-pandemic year since 2009, yet output continues to expand near trend. That divergence is the defining feature of this cycle and, in part, reflects payback from the post-pandemic labor surge.

Productivity gains are allowing firms to generate higher output without proportional increases in headcount. Returns to physical capital, intellectual property, and specialized skills are rising faster than aggregate wage income. Higher-income households, which disproportionately own financial assets and benefit from equity market strength tied to AI investment, are capturing a larger share of income growth. Meanwhile, lower- and middle-income households, which are more dependent on wage gains and more exposed to goods inflation, are experiencing less improvement in purchasing power.

This dynamic is often described as a K-shaped economy: aggregate growth continues, but the distribution of gains is uneven. This is not unusual during periods of structural transformation. As tariff distortions fade and fiscal incentives broaden equipment spending, capital deepening should remain a central theme in 2026. Lower interest rates should eventually support key cyclical sectors that have been lagging, particularly interest-sensitive areas such as housing, durable goods consumption, and capital spending by small and mid-sized businesses that have been constrained by many of the same forces weighing on consumers.

Capital Investment and Credit

Capital spending remains the key driver of the medium-term economic outlook.

Investment in artificial intelligence infrastructure, semiconductor manufacturing, energy systems, commercial aviation, and advanced manufacturing continues to reshape the global economy. Reshoring is also contributing more meaningfully to growth, with gains likely to become more visible over the coming year, particularly in pharmaceuticals, medical technology, and semiconductors.

Private credit has emerged as an important financing channel for capital investment as bank lending has become more constrained. Its expansion has supported investment momentum but has also increased sensitivity to financial conditions. Further tightening in credit markets could slow private credit growth and delay capital spending at the margin.

Geopolitical uncertainty is increasingly influencing the timing and composition of investment. Firms are staging or delaying projects until financing conditions stabilize and supply chains become more predictable. Uncertainty surrounding U.S.-China relations remains a key variable. A delay in high-level engagement, including a potential summit between Xi Jinping and Donald Trump, would likely postpone progress toward broader trade normalization.

At a structural level, U.S.-China tensions reflect a deeper strategic divide that extends beyond trade. China’s use of industrial policy, state support, and geopolitical alignment remains central to negotiations. The policy path will shape trade restrictions, capital flows, and supply chain realignment over the medium term.

Taken together, capital spending remains supported by strong structural demand tied to technology, infrastructure, and reshoring, but the pace is increasingly sensitive to financial conditions and geopolitics.

Inflation and Monetary Policy

Energy shocks present a complicated challenge for central banks.

Higher oil prices raise headline inflation while often weakening economic growth. Policymakers must therefore balance the risk of tightening policy too aggressively against the risk of allowing inflation expectations to drift higher. For the Federal Reserve, this currently implies a more cautious pace of easing than underlying demand conditions would otherwise warrant.

Importantly, energy price increases function more like a tax on economic activity than a traditional demand-driven inflation shock. Rising gasoline and utility costs reduce real purchasing power and tend to slow consumer spending.

While energy prices ripple through the economy, they primarily affect relative prices rather than the overall price level. Sustained inflation typically emerges only when monetary policy accommodates the shock.

The experience of the 1970s illustrates the risk. When monetary policy remained overly accommodative following oil shocks, inflation became entrenched. Modern policy frameworks were shaped by that episode, and today’s Federal Reserve is far less likely to repeat that mistake.

Oil shocks force central banks to choose between fighting inflation and protecting growth

The current energy shock appears more likely to produce a temporary increase in headline inflation than a sustained acceleration in core inflation. The key risk is not the initial price spike, but whether it begins to influence inflation expectations or wage-setting behavior.

Policy is therefore likely to remain data-dependent, with the timing and pace of easing driven more by core inflation and labor market conditions than by movements in headline inflation.

The Political Clock – Geopolitical Implications

The outcome of the Iran conflict will have implications far beyond the Middle East.

A decisive weakening of Iran’s ability to project power could reshape the regional balance and potentially accelerate diplomatic normalization between Israel and several Arab states under the framework established by the Abraham Accords. A less conclusive outcome, however, would risk slowing or reversing that momentum and prolonging regional instability.

The stakes extend far beyond Iran. The outcome will shape the global balance of power

The implications extend well beyond energy markets. The outcome may influence geopolitical alignments across multiple regions, from Eastern Europe to the Indo-Pacific.

The conflict also carries broader implications for the global balance of power. China and Russia are closely monitoring developments. In Asia, the outcome may influence perceptions of U.S. strategic credibility, particularly in the context of rising tensions surrounding Taiwan.

In Europe, the conflict intersects with the ongoing war in Ukraine. Higher energy prices and shifting strategic attention could influence the trajectory of that conflict, particularly if resource flows or policy priorities are redirected.

The geopolitical stakes therefore extend well beyond the immediate battlefield, with potential implications for global alliances, capital flows, and long-term investment decisions.

A prolonged or inconclusive outcome could also increase domestic policy uncertainty in the United States, potentially affecting fiscal priorities, regulatory direction, and the broader policy environment.

Review and Outlook

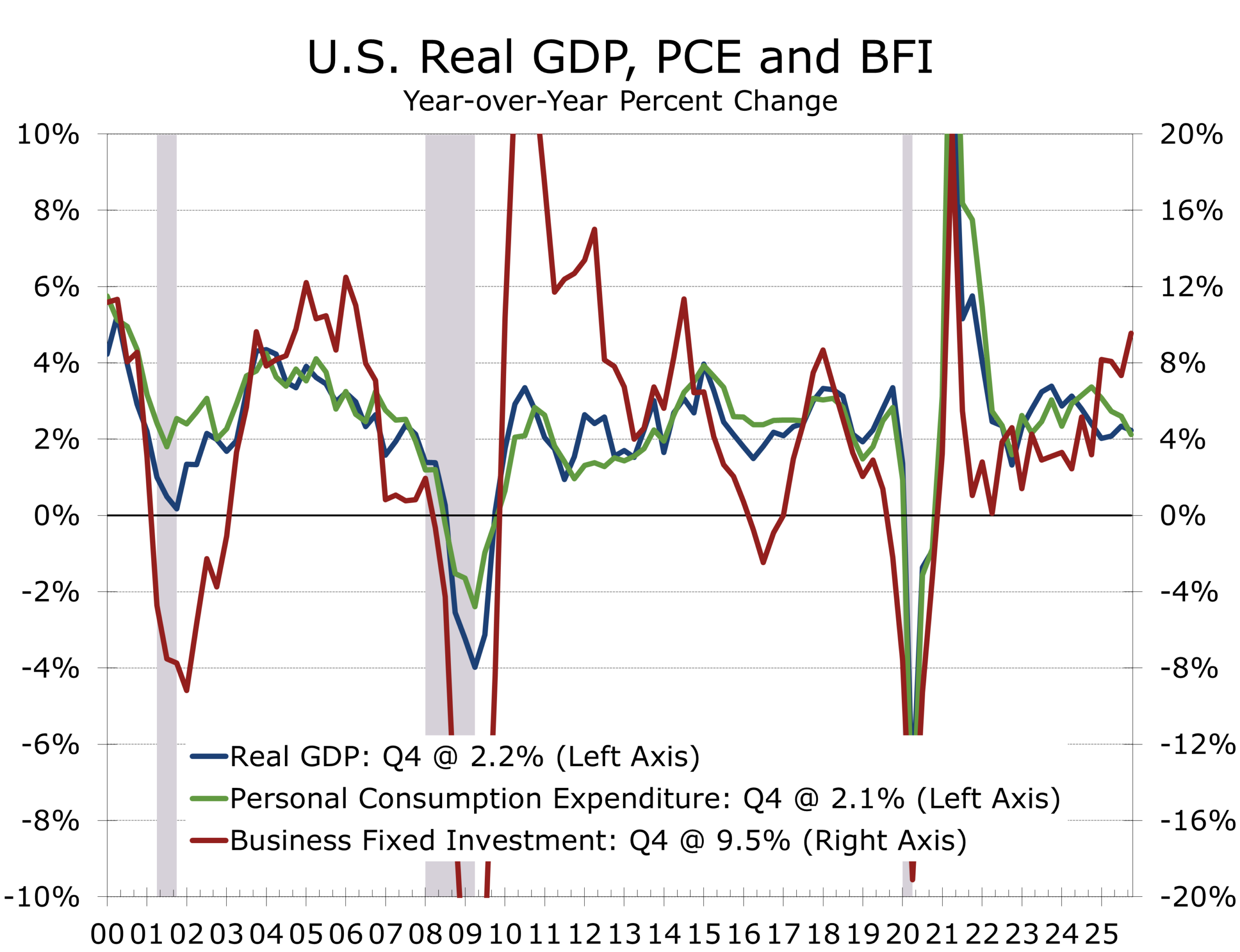

The baseline outlook remains one of continued economic expansion, though with slower growth and heightened volatility. First-quarter GDP has shown a recurring tendency to come in softer than underlying fundamentals would suggest, and that risk remains in place this year. Our 2.1% Q1 real GDP forecast is currently below consensus and below the latest point estimate from the Atlanta Fed GDPNow, which calls for 2.7% growth.

Markets are overpricing inflation risk and underpricing the durability of growth

Higher energy prices are likely to restrain consumer spending, particularly on durable goods, while geopolitical uncertainty may delay some capital investment. Even so, the expansion should remain intact and continue to be led by productivity-enhancing investment.

The U.S. economy retains important structural advantages, including deep capital markets, flexible labor markets, and sustained investment in advanced technologies, all of which should continue to attract global capital. The advantages reassert themselves in times of economic stress.

Monetary policy is likely to remain cautious as policymakers assess whether the energy shock generates more persistent inflation pressures. Our base case remains that the Federal Reserve will ease policy gradually, with scope for two 25 basis point rate cuts over the course of the year. We currently view September as the most likely timing for the next move, although an earlier adjustment is possible if geopolitical risks recede and labor market momentum softens more quickly or more dramatically.

Financial markets are likely to remain volatile as investors reassess the balance between inflation risks and slowing growth. In our view, markets are placing too much weight on inflation risks—which are likely to prove more contained than in prior energy shocks—and too little on the near-term implications for growth. While growth may soften in the near term, the drag is likely to be manageable and should ease as financial conditions stabilize and investment remains firm. This suggests that periods of market volatility may present opportunities as the underlying expansion remains supported by structural investment and resilient fundamentals.

Strategic Takeaway

The conflict with Iran represents more than a regional security event; it is a test of the geopolitical framework underpinning the global economy. It is also a test of strategic resolve among the United States and its allies, Iran’s regime, and key external actors, particularly Russia and China.

A decisive outcome stabilizes the outlook. An inconclusive one prolongs uncertainty

While Russia and China are less directly committed to Iran than the United States is to Israel, both are closely monitoring the conflict’s trajectory. The outcome will help shape perceptions of U.S. strategic credibility and influence broader geopolitical calculations, particularly in regions where deterrence and alliance structures are already under pressure.

Russia, in particular, has an interest in sustained geopolitical friction, as elevated instability in the Middle East can support energy revenues and divert Western attention. China’s posture is more complex, balancing its economic interests in stable energy markets with its longer-term objective of reshaping the global order. In both cases, the conflict’s outcome will inform how these countries assess the durability of U.S. leadership and the cohesion of Western alliances.

A decisive outcome that materially weakens Iran’s ability to project power could reshape the regional balance and reinforce broader deterrence. Such an outcome could reduce a persistent source of regional instability, support renewed diplomatic engagement, and improve the medium-term outlook for global energy markets and capital flows.

A more prolonged or inconclusive outcome, however, would likely have broader implications. Sustained uncertainty could weigh on investment, tighten financial conditions, and increase the risk of spillovers into other geopolitical theaters, including Eastern Europe and the Indo-Pacific. It could also contribute to a more fragmented global environment, with greater emphasis on security, supply chain realignment, and regional blocks.

If the conflict stabilizes and energy markets normalize, the global economy should be able to absorb the shock and continue expanding, supported by underlying strength in investment and productivity. If not, the interaction between geopolitical uncertainty, financial conditions, and policy constraints could become a more binding headwind for growth.

The expansion remains intact, but with a narrower margin for error and greater sensitivity to geopolitical outcomes. In that sense, the economic outlook will be shaped not only by traditional macroeconomic forces but also by the evolving structure of the global geopolitical landscape.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 18. 2026

Mark Vitner, Chief Economist

704-458-4000