Improving Affordability is Bringing Buyers Back

-

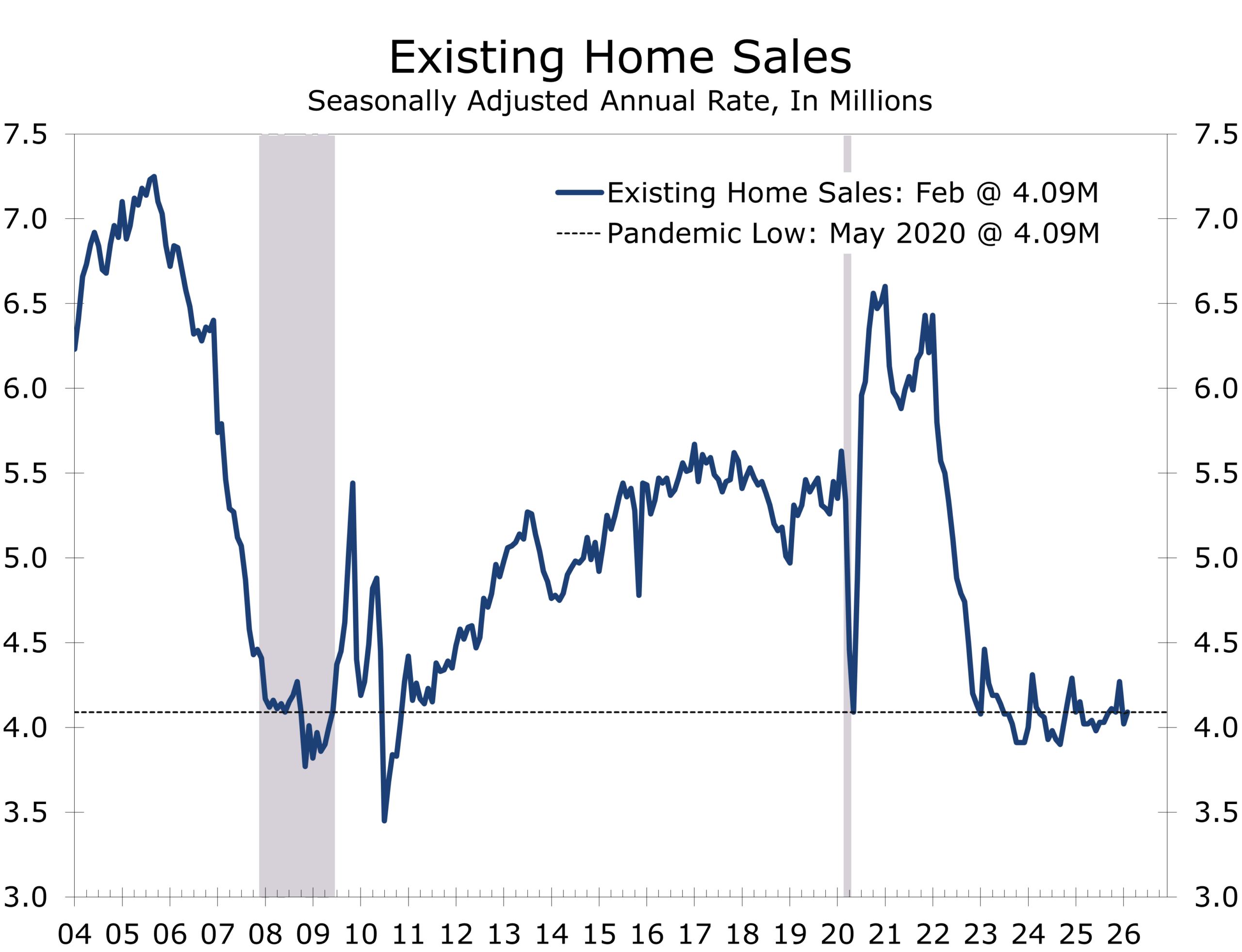

- Existing-home sales rose 1.7% in February to a 4.09-million-unit annual rate

- Sales remain 1.4% below year-ago levels, reflecting still-muted housing turnover.

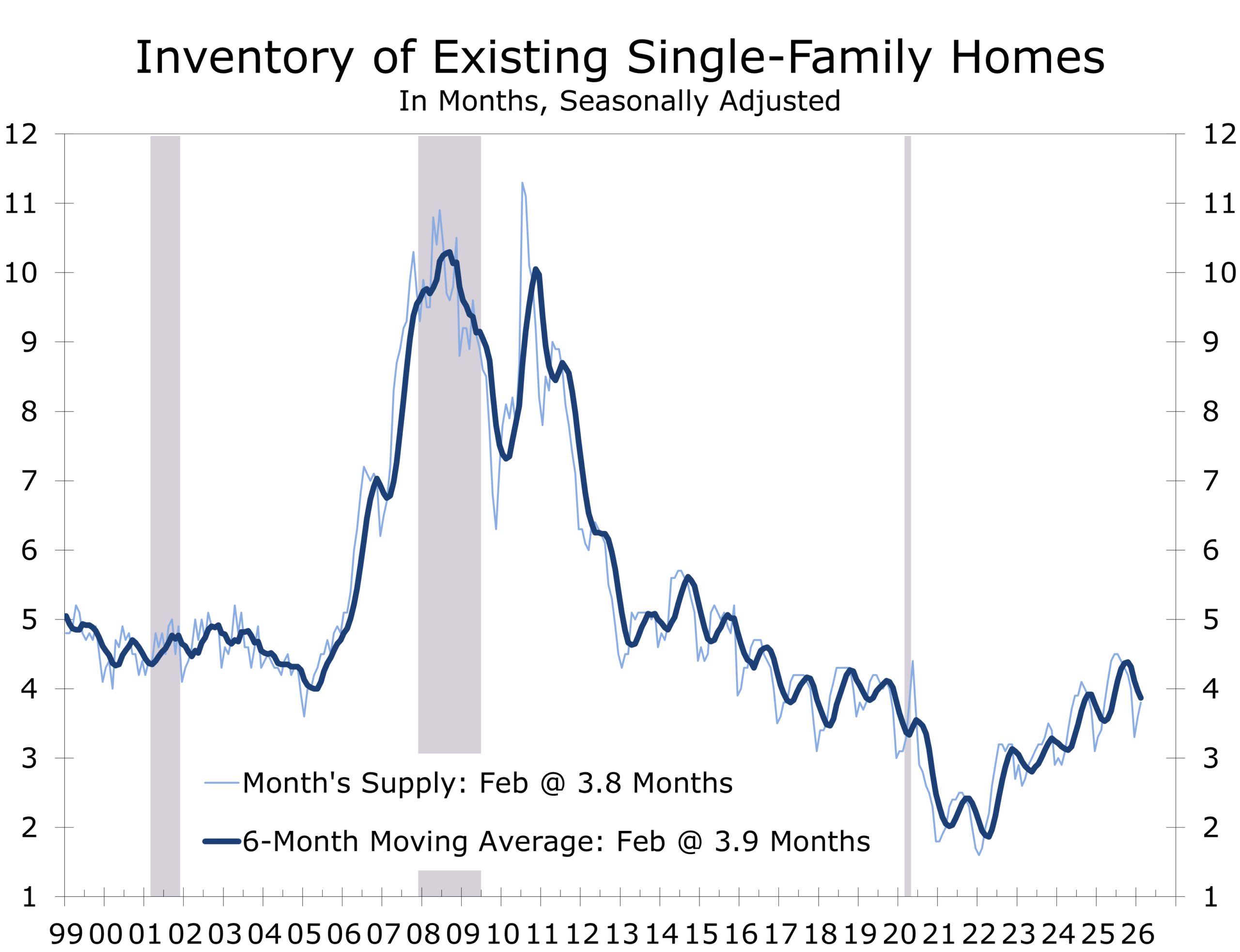

- Inventory increased 2.4% to 1.29 million units, equal to a 3.8-month supply. A 4.5 to 5-month supply would be more normal.

- The median existing-home price rose 0.3% year-over-year to $398,000, marking the 32nd consecutive year-over-year increase.

- Single-family sales increased 2.5%, while condo and co-op sales fell 5.3%.

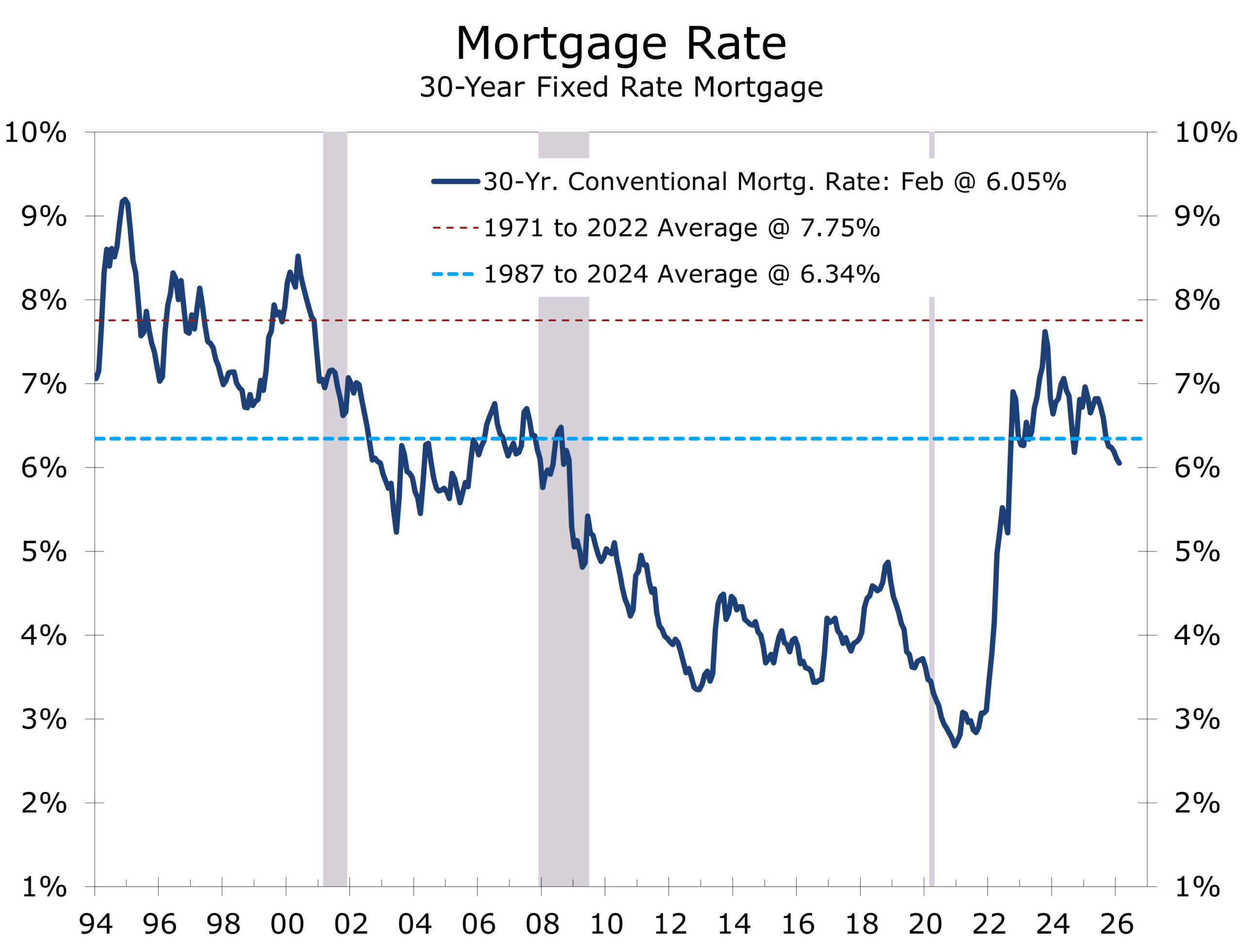

- Housing affordability improved for the eighth straight month, reaching its highest level since early 2022.

- Despite February’s rebound, sales remain well below pre-pandemic norms due to limited inventory and the mortgage-rate lock-in effect.

Harsh Winter Weather Had Little Impact on Closings

The housing market may finally be stirring from its winter lull. Existing home sales rose 1.7% in February to a 4.09-million-unit annual rate, a modest but encouraging gain following two years of unusually weak housing turnover. The increase came despite harsh winter weather in parts of the country and slightly exceeded expectations, suggesting that underlying demand remains stronger than the recent pace of sales might imply.

Existing home sales reflect closings on contracts that were signed several weeks earlier, meaning the severe January weather likely has had less impact than feared. January sales were also revised higher to 4.02 million units, lifting the combined January–February pace to roughly 4.06 million units, slightly stronger than expected for the first quarter.

Improving affordability is bringing buyers back, but millions of homeowners remain reluctant to part with their ultra-low mortgage rates.

Even so, the housing market remains constrained. The U.S. economy now supports more than six million additional jobs than it did in 2019, yet annual home sales remain roughly one million units below pre-pandemic norms. The primary culprit remains the mortgage-rate lock-in effect, which continues to discourage homeowners with sub-4% mortgages from selling and taking on higher borrowing costs.

Affordability is gradually improving, offering some hope that activity may begin to recover. The Housing Affordability Index rose to 117.6 in February, the eighth consecutive monthly increase and the highest reading since early 2022. Mortgage rates averaged 6.05% in February, down from 6.84% a year earlier, while wage growth has recently begun to outpace home price appreciation. These shifts have modestly improved purchasing power, although affordability remains far from pre-pandemic levels. We expect this improvement to continue and help resurrect home sales this spring and summer.

Affordability is improving, but existing home sales remain constrained by limited inventory.

Home price growth has cooled but remains positive. The median existing home price rose 0.3% yr/yr to $398,000, extending the streak of yr/yr gains to 32 consecutive months. Price trends, however, are diverging across regions. The Northeast and Midwest continue to see modest gains, while price growth in the South has flattened and prices in the West have edged lower, reflecting the larger pandemic-era price surge in those markets. Sellers in the South face competition from new homes, with many builders slashing prices to clear new home inventories.

Existing home inventories remain too low but are beginning to recover, albeit gradually. The number of homes available for sale rose 2.4% in February to 1.29 million units, translating to a 3.8-month supply at the current sales pace. Inventory is now 4.9% higher than a year ago, suggesting supply constraints are easing modestly as the spring selling season approaches.

Some homeowners who previously pulled their listings appear to be returning to the market. Roughly 45,000 sellers who delisted their homes last year re-listed in January, an unusually large number and a potential sign that supply could increase further.

Regional trends were mixed. Sales rose 8.2% in the West, reflecting a rebound in the most rate-sensitive region. Sales increased 1.6% in the South and 1.1% in the Midwest, while sales in the Northeast fell 6.0%, likely reflecting the greater impact of winter weather.

First-time buyers accounted for 34% of purchases, up from 31% in January, while cash sales represented 31% of transactions. Investors and second-home buyers accounted for 16% of sales. Homes remained on the market for 47 days, up slightly from a year ago, likely signaling less competition among buyers.

Looking ahead, existing home sales are expected to gradually improve through the end of this year, assuming mortgage rates remain near current levels, and the broader economy remains resilient. However, the outlook is not without risks. The past couple of days have seen a great deal of volatility in energy prices and the financial markets more broadly. We feel the worst of this has now passed and look for mortgage rates to remain near 6% going into the key Spring Selling Season.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 10, 2026

Mark Vitner, Chief Economist

(704) 458-4000