Highlights of the Week

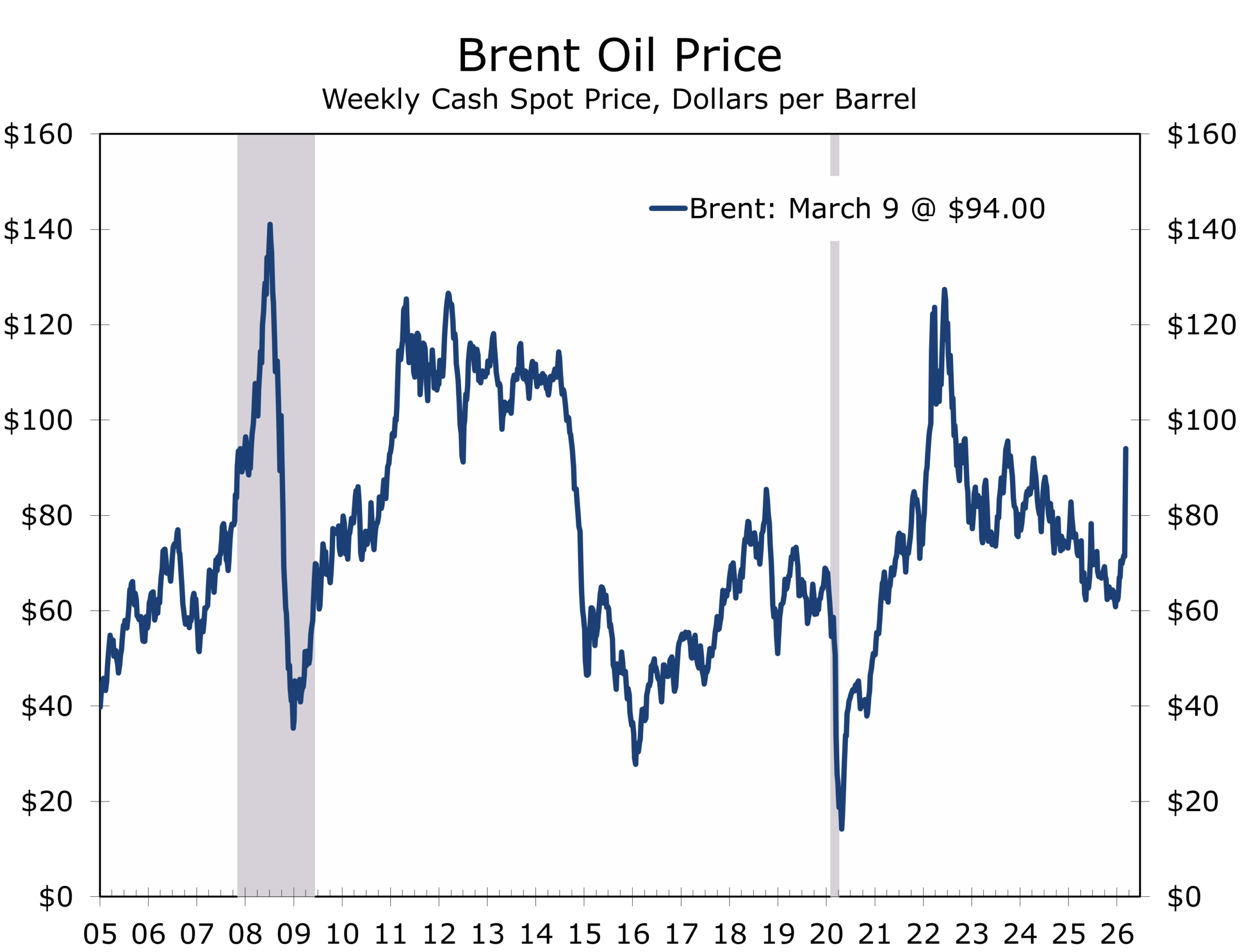

- Brent and WTI briefly traded near $120 on Monday as the Hormuz disruption deepened and Gulf producers began trimming output. Markets are now pricing a genuine supply shock, not merely shipping friction.

- February payrolls were soft, but the details were firmer than the headline. Wage growth stayed solid, the unemployment rate was unchanged, and strike distortions likely exaggerated the weakness in the establishment survey.

- Europe is emerging as one of the clearest economic pressure points. Qatar’s LNG shutdown and low regional gas storage leave Europe exposed to another power-price squeeze just as growth was trying to stabilize.

- The dollar has firmed, equities have wobbled, and break-evens have moved higher. The first market response has been inflation repricing and selective de-risking rather than a full-blown growth panic.

- The Federal Reserve’s room to ease has narrowed materially. Energy shocks only become persistently inflationary if validated by monetary accommodation, but the policy margin for error is now much thinner.

From Tail Risk to Market Reality

The war with Iran moved from tail risk to market fact pattern over the past ten days, and the economic conversation changed with it. What began as a geopolitical shock is now an inflation, funding, and confidence shock as well. Our thoughts remain first with those in harm’s way, especially U.S. personnel and allies operating in an increasingly fluid theater.

Markets are no longer pricing a modest disruption. They are pricing a serious supply shock with an uncertain self-life. Reuters reported Monday that crude briefly traded near $119.50 per barrel, Gulf producers have begun cutting output as shipments stall, and G7 governments are weighing emergency stock releases. Wall Street sold off early, the dollar strengthened, and bond markets repriced inflation risk faster than growth risk. Attitudes improved in the afternoon as President Trump signaled that the conflict is closer to an end than it appears.

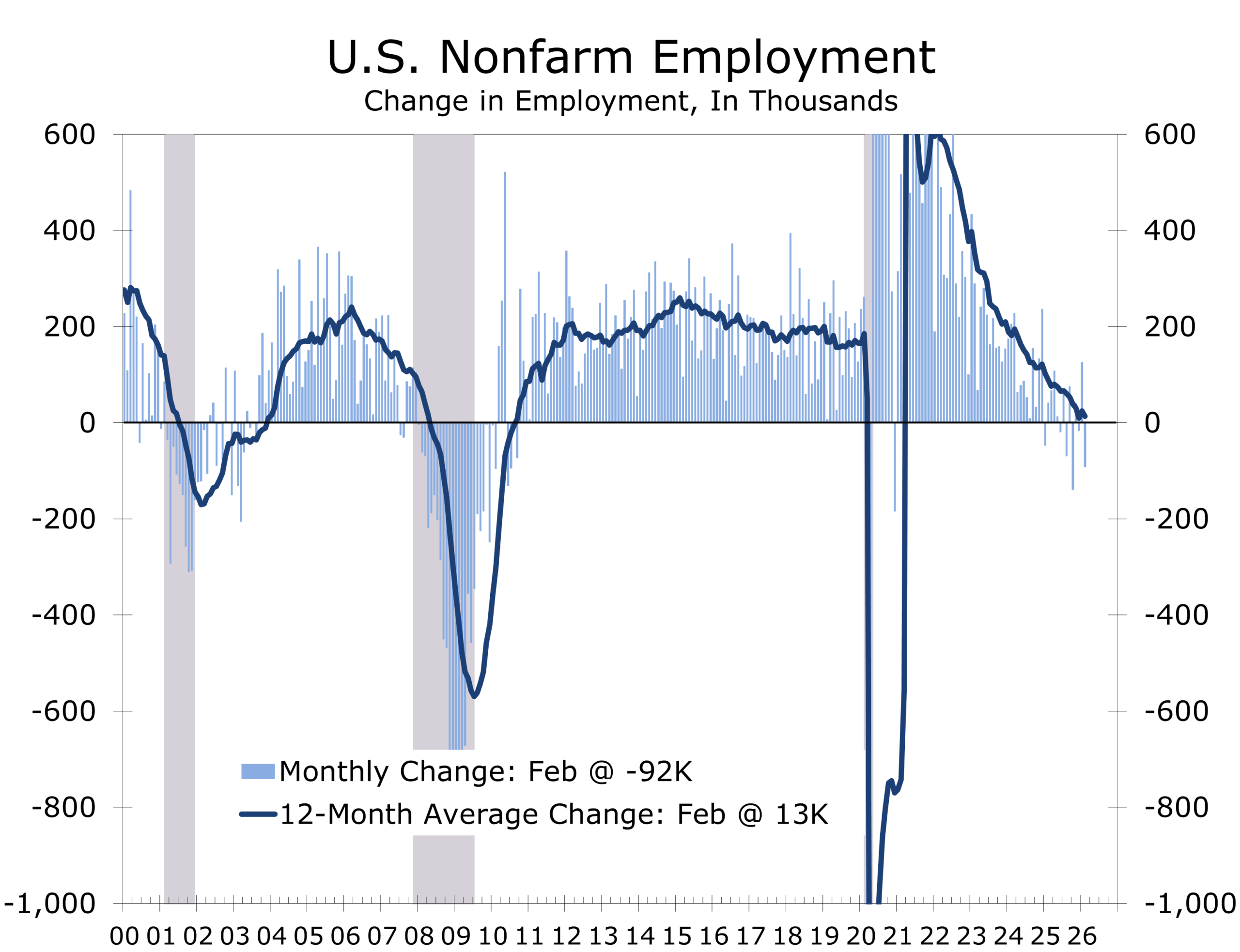

The U.S. economy entered this episode in better shape than many feared. Friday’s February employment report was weaker on the surface but less alarming underneath. Nonfarm payrolls fell 92,000, the unemployment rate held at 4.4%, average hourly earnings rose 0.4% on the month and 3.8% from a year earlier, and participation held at 62.0%. Healthcare strike effects, federal cutbacks, and prior downward revisions made the headline softer, but the labor market still looks more cooled than cracked.

Hormuz: From Friction to Shock

The situation in the Strait of Hormuz increasingly resembles the central tension in the George Clooney film The Peacemaker: preventing a crisis before it becomes irreversible. As Clooney’s character notes, if you want to stop catastrophe, you cannot wait for the mushroom cloud. Markets are now grappling with that same question of timing and duration.

The Strait of Hormuz has moved well beyond a friction story. Ship traffic remains nearly paralyzed, hundreds of tankers are idle, and Saudi Arabia has begun diverting exports toward Red Sea routes. Iraq, Kuwait, Qatar, and the UAE have also curtailed output as storage fills and logistics snarl. Brent briefly touched $119.50 and WTI traded near similar levels. That is no longer low-to-mid-$80s disruption pricing. It is the market’s way of signaling that duration now matters as much as magnitude.

Prices stabilized near $90 per barrel late Monday afternoon after President Trump suggested the United States might move to secure the Strait of Hormuz, easing fears of a prolonged shipping shutdown.

The volatility reflects uncertainty more than a definitive loss of supply. The key distinction is between temporary seizure and structural destruction. Strategic petroleum reserves, spare production capacity, elevated inventories, and the flexibility of U.S. shale still provide a substantial cushion. But once physical flows are impaired and major producers begin cutting output, the path to normalization becomes longer and more uncertain.

Eighty-dollar oil signals volatility. One-hundred-twenty-dollar oil signals that markets are beginning to price regime change and the possibility of a longer disruption to global energy supply chains.

The psychological dimension should not be underestimated. Videos circulating over the weekend showing burning oil storage facilities outside Tehran carried an unmistakably apocalyptic tone. In the absence of hard information about how long shipping through the Strait of Hormuz might be disrupted, those images likely amplified investor anxiety and helped fuel the earlier spike in oil prices.

Labor Market: Softer Headline, Firmer Core

Friday’s employment report looked alarmingly weak at first glance, but the internals argue for moderation rather than collapse. Payrolls fell 92,000 in February after a downwardly revised 126,000 gain in January, with healthcare employment dragged down by strike activity and federal government payrolls continuing to trend lower. Revisions lowered December and January payrolls by a combined 69,000. Even so, the unemployment rate edged up only to 4.4%, participation held at 62.0%, average hourly earnings rose 0.4% on the month, and aggregate hours worked increased modestly.

One factor largely overlooked over the weekend is that January and February payroll data are often highly volatile due to swings in holiday-related hiring. In the past those swings were concentrated among retailers. Today they are more often found among restaurants, delivery services, and couriers. The return of winter weather also reversed earlier gains in construction payrolls that had benefited from relatively mild conditions in December and early January. Annual updates to the methodology BLS uses to compile the monthly data further complicates monthly comparisons and this year also has the added burden of government shutdowns and outsized reductions in the federal workforce.

As we cautioned last month, the January payroll numbers were ultimately not likely to be as strong as the headlines suggested. Even so, the three-month trend, which smooths many of these distortions, suggests hiring has slowed to a crawl. The ADP data point to a slightly firmer underlying trend, and we remain encouraged by the improvement in the employment diffusion index, which shows a broader array of industries adding jobs. That improvement is echoed in both the ISM Manufacturing and Services surveys, which have also shown gradual improvement in recent months. Given current conditions, we feel the best measure of underlying job growth is provided by measures of private sector growth from the BLS and ADP.

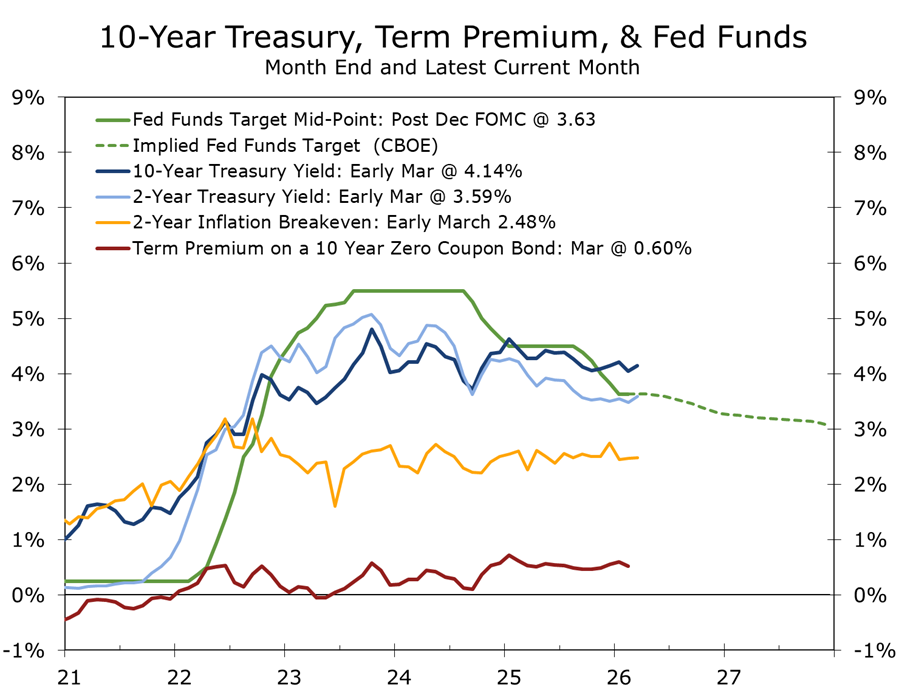

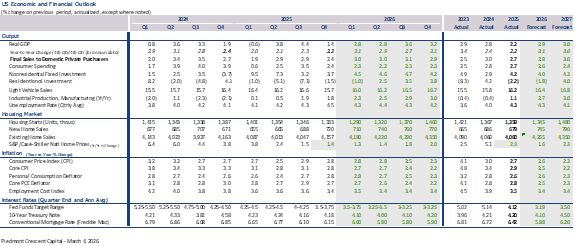

For the Federal Reserve, the result is an awkward combination: labor market conditions are soft enough to invite discussion of easing, but wage growth remains firm enough to complicate any response to an energy-driven inflation impulse. For now, the Fed likely has time to let the data clarify the underlying trend. Aggregate hours and productivity trends suggest real GDP is still expanding at roughly a 2.5% pace in the first quarter.

Europe: Energy Shock, Strategic Squeeze

Europe looks especially exposed. Qatar’s production halt has intensified competition for LNG cargoes, European benchmark gas prices jumped more than 30% after the attack on Qatar’s LNG facilities, and major gas storage levels across Europe are near 30% full versus roughly 54% typical for early March. Germany’s inventories are only about 27% full and the Netherlands is near 10%. Statkraft also warned that higher gas prices are already pushing up power costs in Germany, France, and the U.K.

That leaves Europe squeezed from both directions. It remains strategically dependent on the United States for security while once again confronting an imported energy shock that threatens industrial competitiveness. The old continent spent the better part of three years learning that energy dependence is destiny. Iran has now handed it a refresher course.

Markets: Inflation Repricing, Growth Questions Next

Financial markets are behaving as one would expect in the early stages of an oil shock. Wall Street fell Monday before paring losses, the dollar strengthened as a source of liquidity, and Treasury yields jumped and then partially retraced as investors debated whether higher energy prices mean tighter financial conditions or simply more inflation. Gold even fell on Monday as the stronger dollar and reduced expectations for near-term easing overwhelmed the usual haven bid.

ISM and Cyclicals: Still Expanding, Less Comfortable

The ISM surveys remain among the cleanest read-throughs on cyclical momentum, and they continue to point to expansion. Manufacturing has held above 50 for a second consecutive month, with new orders and backlogs improving from previously depressed levels. The Services survey has also remained comfortably in growth territory. That is the good news.

The less comforting news lies in costs. Tariffs, metals prices, AI-related equipment demand, and now energy are all pushing input costs higher at the same time. Firms can manage one cost shock. Several arriving simultaneously begin to squeeze margins, slow hiring, and delay discretionary spending. The industrial upswing remains intact, but it is now running into a much harsher cost backdrop.

Regular readers know we place substantial weight on manufacturing because it provides the cyclical impulse for the broader economy. The recent improvement in factory activity, defense production, aerospace output, data-center construction, and reshoring still argues for solid underlying growth later this year. The latest data show a clear improvement, with orders up sharply. The risk is that oil and LNG could do to 2026 what tariffs alone could not: turn what had been shaping up as a classic cyclical rebound story into a much messier inflation story.

Piedmont Perspective: Deterrence, Duration, and Europe’s Dilemma

Much of the public discussion still treats the current conflict as a sudden rupture. Strategically, it is better understood as a continuation of a long-running confrontation that prior administrations were often reluctant to fully acknowledge. Since 1979, Iran’s regime has defined the United States as its principal adversary and has pursued that objective through both direct actions and a network of regional proxies. For markets, the key issue is not rhetoric but duration. Temporary conflicts can be traded around. Prolonged wars reshape inflation psychology, investment timelines, supply chains, and alliance structures.

Israel has long been Iran’s second primary adversary. Tehran has waged a sustained campaign against the Jewish state through regional proxies, including Hamas, Hezbollah, elements of the Muslim Brotherhood network, and the Houthis, as well as through covert operations. Iran has provided funding, training, and strategic support to these groups, and U.S. and Israeli intelligence assessments indicate Iranian backing for the October 7 attacks on Israel. From Israel’s perspective, that attack fundamentally altered the strategic calculus, strengthening the case for dismantling the regional architecture that Iran has built under the leadership of Supreme Leader Ali Khamenei.

It is worth remembering that relations between Israel and Iran were not always hostile. Prior to the 1979 revolution, the Persian monarchy maintained quiet but meaningful ties with Israel. A resolution that ultimately replaces the current theocratic regime with a government willing to normalize relations with its neighbors would significantly alter the Middle East’s economic trajectory, opening the door to broader regional integration and growth.

Europe now finds itself in a familiar and uncomfortable position. It speaks with moral clarity but possesses limited hard power while remaining heavily exposed to global energy markets. A prolonged Middle East disruption would indirectly strengthen Russia through higher energy prices, complicate Europe’s support for Ukraine, and remind investors that the continent has yet to close the gap between its geopolitical ambitions and its strategic capabilities. History has a habit of sending the bill twice.

Looking Ahead

This week’s calendar arrives at an awkward moment. On Tuesday, investors will parse the New York Fed’s Survey of Consumer Expectations, the rescheduled January Existing Home Sales report, and the delayed fourth-quarter retail e-commerce release. Wednesday brings the February CPI report, the week’s key macro event. Thursday includes initial claims and the February PPI. Friday is crowded: the second estimate of fourth-quarter GDP, personal income and the PCE deflator, JOLTS, and the preliminary March University of Michigan consumer sentiment survey.

Under ordinary circumstances the CPI would dominate. This week it shares the stage with oil, gasoline, shipping disruptions, and consumer psychology. If inflation data run hot while gasoline prices keep climbing, markets will further reduce the odds of near-term Fed easing. If sentiment sours sharply, growth fears will move up the list.

Funding Fundamentals

Front-end relief can no longer be assumed. Oil in the $90 range, firmer wage growth, and a still-expanding services economy complicate the path to easier policy. Funding windows may remain open, but they are likely to be more episodic and more dependent on intraday market tone. Refresh liquidity forecasts, revisit commodity and transport exposures, and be realistic about working-capital pressure if energy and freight costs remain elevated. Opportunistic issuance on rallies still makes sense, but the comfort of a steadily declining rate path has faded.

Bottom Line

The U.S. economy entered the Iran shock with more resilience than the headlines suggest, but resilience is not immunity. As Clooney’s character observes in The Peacemaker, “Once it starts, you don’t control it.” Markets are hoping that deterrence still works before the current conflict reaches that stage. Friday’s employment report reiterates that the labor market has limited room for error, but it is not collapsing either.

Monday morning’s oil market initially signaled that the geopolitical shock was intensifying, before reconsidering that view by mid-afternoon. The oil market remains well supplied overall, but a prolonged disruption could easily see those earlier price highs revisited. Europe’s renewed energy vulnerability raises the global stakes, and this week’s inflation and activity data will help determine whether the macro backdrop can absorb another oil spike.

Economic growth remains solid, even if it is moderating somewhat. Real GDP appears to be tracking near a 2.4% annualized pace in the first quarter, reflecting the combined effects of winter weather and the early stages of geopolitical uncertainty weighing on consumer spending and capital investment.

Markets began the year expecting a friendlier mix of moderating inflation, modest policy easing, and steady growth. They are now being asked to contemplate something less comfortable: respectable growth, stubborn inflation, and a war whose duration may matter almost as much as its outcome.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 9, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000