Early Signals of a Spring Rebound

-

- January payrolls surprised to the upside, rising 130,000 — roughly two and a half times consensus expectations.

- Private-sector payrolls jumped 172,000, signaling firmer underlying momentum.

- The unemployment rate edged down 0.1 percentage point to 4.3%, with declines among reentrants and new entrants.

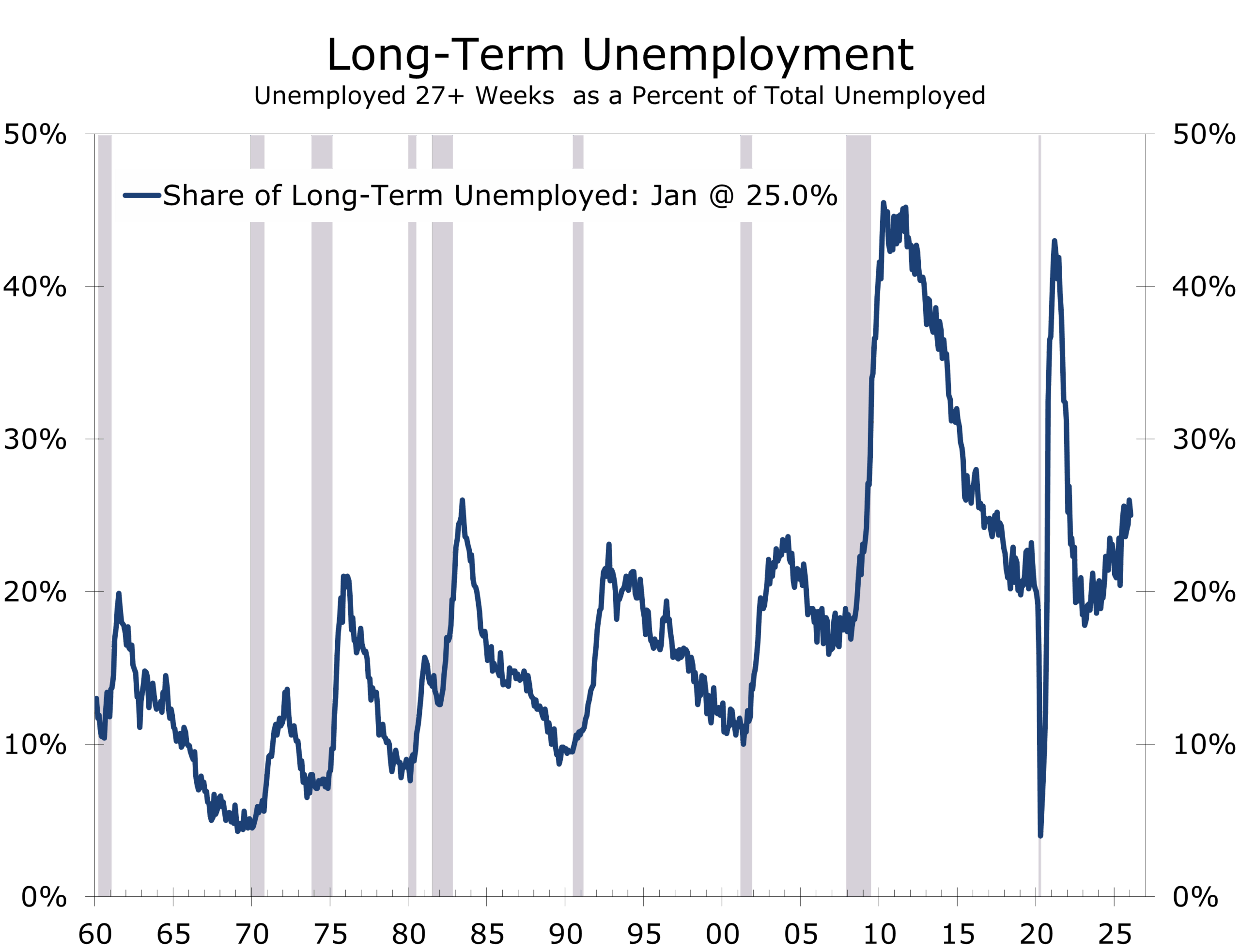

- We see several early signs of a cyclical rebound including a modest drop in the number of long-term unemployed.

- Manufacturing employment rose by 5,000, ending a multi-month stretch of softness.

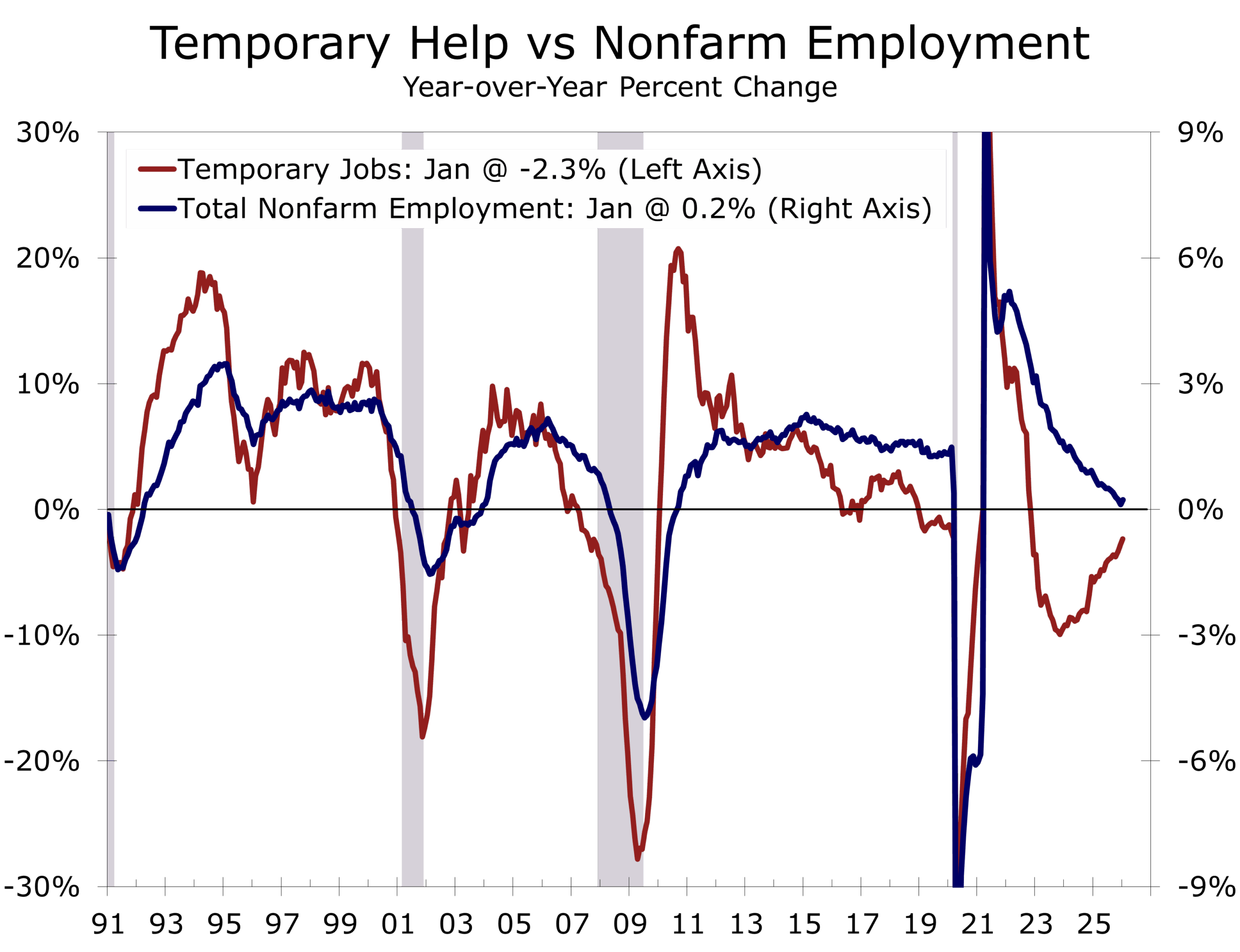

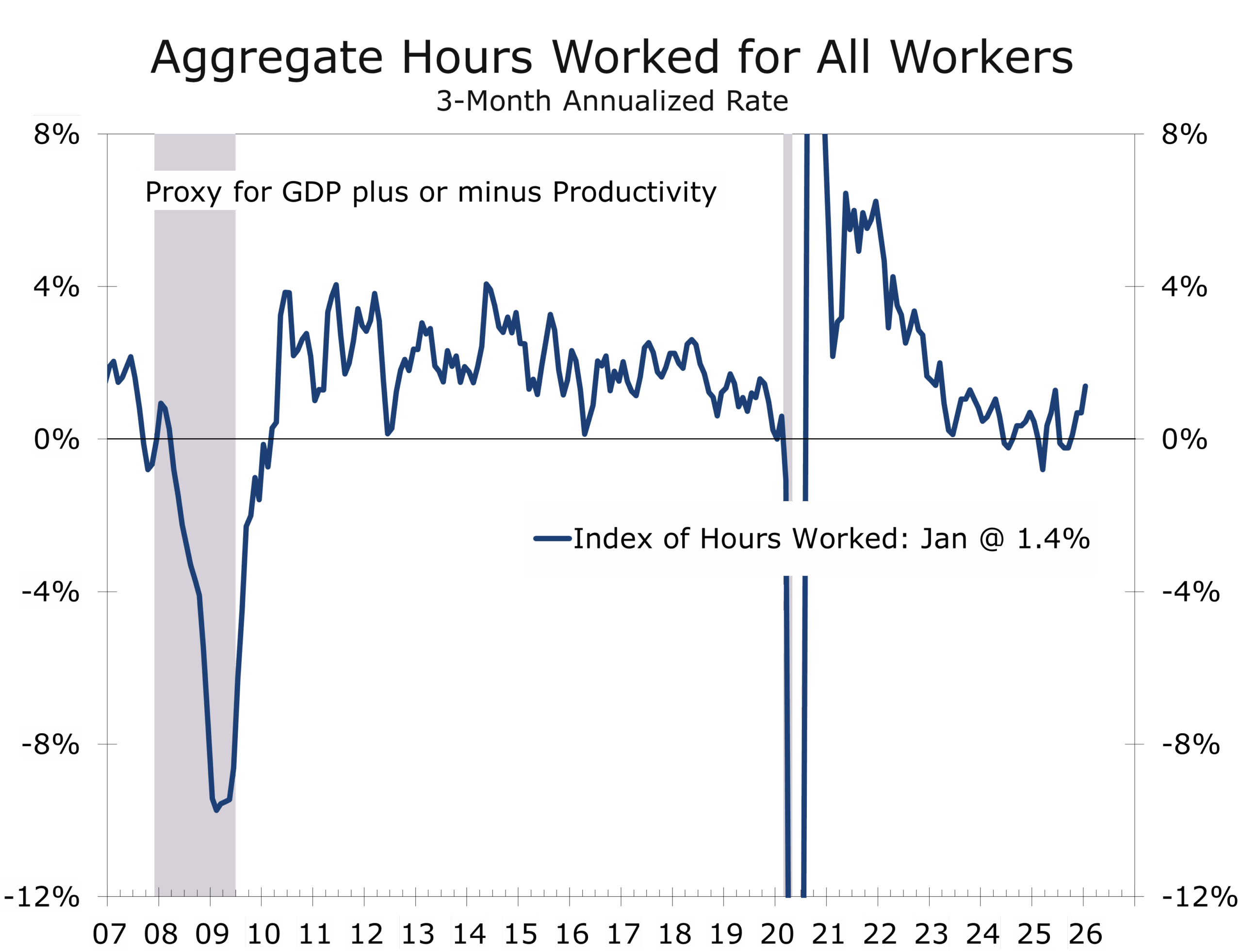

- Temporary staffing employment and average weekly hours improved, both consistent with a cyclical bounce.

- Hiring remains concentrated but may be beginning to broaden.

- We see emerging Green Shoots supplementing what has been a structural, capital-intensive expansion this past year. We expect to see more compelling evidence of this later this year.

January Payrolls: A Firmer Start Than Anticipated

January payroll growth handily exceeded expectations, with employers adding 130,000 net new jobs — roughly twice consensus expectations and materially stronger than our 50,000-job increase forecast.

More notably, private-sector payrolls rose 172,000. The divergence from the headline reflects declines in government employment and underscores firmer hiring within the private economy.

Gains remain concentrated in health care, social assistance, and construction — sectors that have carried much of the employment load over the past year. Demographic trends, infrastructure spending, and reshoring-related activity continue to support hiring in these areas.

Manufacturing employment rose by 5,000 in January, ending a multi-month stretch of weakness. While modest, the increase is notable given the sector’s earlier softness and aligns with improving manufacturing survey data.

Temporary staffing, the sector that predicted the slowdown, is now hinting at stabilization.

Temporary help employment has improved over the past several months. This sector weakened well ahead of the broader slowdown in nonfarm payrolls and often serves as a leading indicator. Its recent firming suggests that hiring may begin to perk up as we move into the spring and summer.

Breadth is not yet robust. But directionally, several indicators are turning less negative.

Subtle but Constructive Improvement

The unemployment rate edged down 0.1 percentage point to 4.3% in January.

The number of unemployed declined modestly, with the reduction occurring primarily among reentrants and new entrants into the labor force. That detail matters. It suggests that job seekers are being absorbed rather than discouraged.

January household data are inherently volatile due to seasonal adjustments and annual updates. Still, the direction of change aligns with other cyclical indicators.

Long-term unemployment declined slightly as well, reinforcing the notion that labor market slack is not building in a meaningful way.

Stability is giving way to incremental improvement.

Taken together with better-than-expected ISM Manufacturing report, these data point toward early cyclical improvement in 2026 — supplementing the structural capital-intensive growth that has defined the past several quarters. We expect these Green Shoots to become more prominent this spring and summer, producing a more durable and more highly visible expansion.

Hours Worked: An Early Signal

Average weekly hours improved in January, and aggregate hours worked rose as well.

Employers typically increase hours before expanding payrolls. When demand begins to firm, firms stretch existing labor first. The improvement in hours reinforces the view that labor demand may be stabilizing beneath the surface.

If sustained, rising aggregate hours support income growth and help stabilize consumption without requiring rapid payroll acceleration.

Hours tend to turn before headcount.

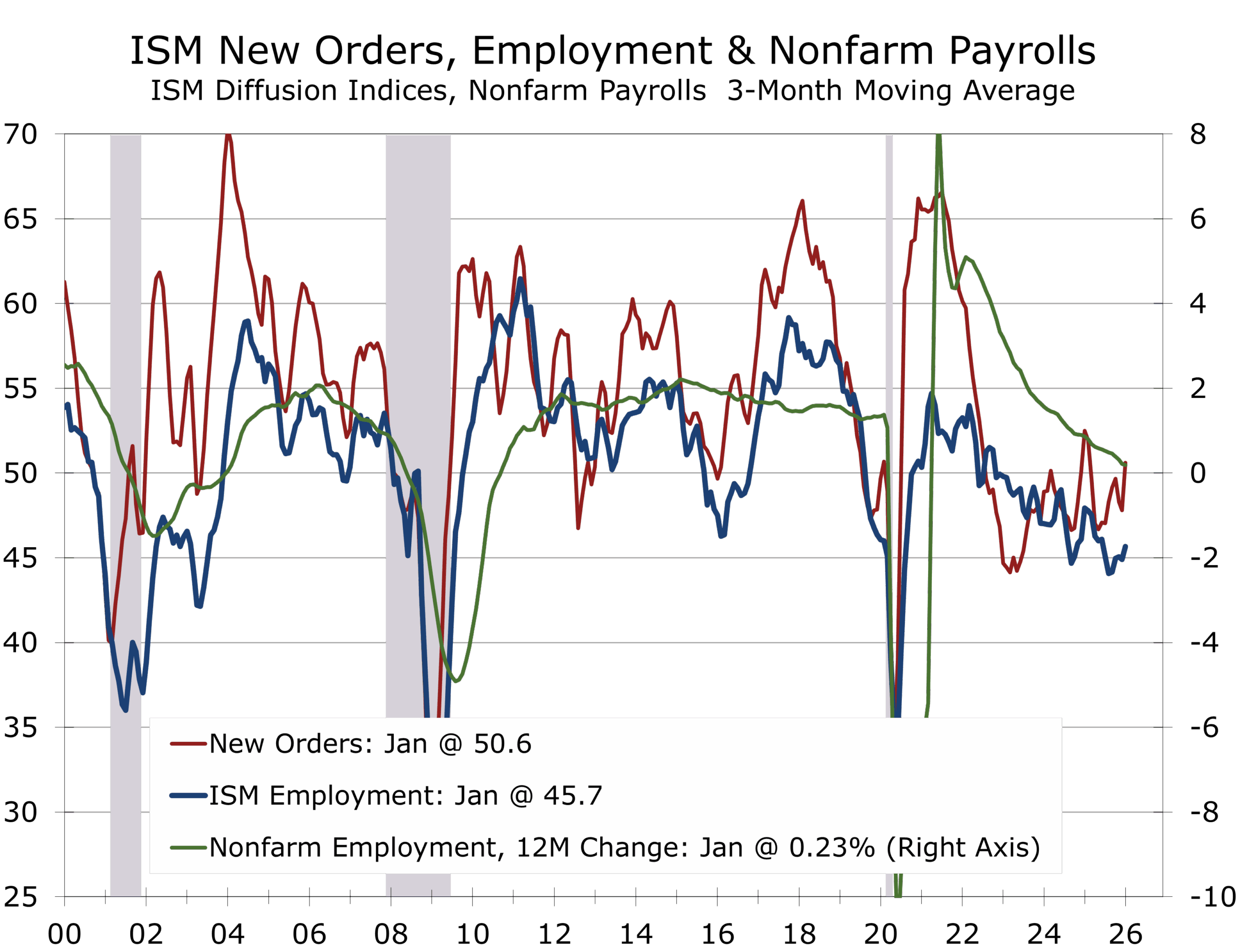

Recent ISM readings surprised to the upside, particularly in the new orders and employment components.

Historically, payroll growth follows sustained improvement in ISM components with a lag of one to three months. The emerging pattern is consistent with that sequence:

- Surveys stabilize

- Hours improve

- Temporary staffing firms

- Payroll growth firms

January’s report suggests that sequence may now be underway.

Structural Protein Meets Cyclical Lift

The broader economy continues to benefit from structural, capital-intensive investment in AI infrastructure, advanced manufacturing, reshoring, grid modernization, and defense-related activity. That investment wave has been productivity enhancing but labor light. January’s data suggests cyclical forces may now begin to supplement that structural base.

Stabilization gives the Fed room to normalize policy and re-energize the expansion.Bottom of Form

Even with the recent eye-popping GDP growth, we are not describing a boom. We are observing Green Shoots emerging within a labor market that cooled but never contracted meaningfully.

Wages and Inflation Context

Average hourly earnings rose 0.4 percent in January, bringing year-over-year wage growth to 3.7 percent. While the monthly increase was firm, the broader trend remains consistent with gradual disinflation and well below peak inflation-era levels.

The improvement in hours worked amplifies aggregate income growth without signaling renewed wage acceleration. The combination of firmer hours, stable unemployment at 4.3 percent, and wage growth holding in the upper 3 percent range supports real income gains while keeping inflation pressures contained. When combined with recent productivity trends, aggregate hours worked imply Q1 real GDP is on pace to grow at 3% pace.

For policymakers, this is a constructive mix. Wage growth is no longer the primary source of inflation concern, and income gains are increasingly supported by productivity and improved labor utilization rather than accelerating compensation.

January’s report reduces the urgency for immediate policy easing but does not eliminate the case for further normalization later this year. Modestly firmer hiring, improving hours, contained wage growth, and declining long-term unemployment point to a labor market that is stabilizing rather than overheating.

That distinction matters.

If cyclical indicators continue to firm while wage pressures remain contained, the Federal Reserve gains flexibility to deliver two or even three additional rate cuts over the course of the year. Such moves would not signal weakness. They would reflect confidence that inflation is on a sustainable path lower and that real rates no longer need to remain deeply restrictive.

The current configuration of steady job growth, improving labor utilization, and moderating wage pressures is precisely the environment in which policymakers can ease gradually without reigniting inflation.

Protein built the floor. Cyclical lift may now be adding incremental momentum.

If rate cuts unfold as we expect, the result should be a classic cyclical recovery in interest-rate-sensitive sectors this spring and summer. Lower borrowing costs would likely improve housing affordability and unlock pent-up demand, support light vehicle sales that remain below long-term replacement needs, reinforce spending on household durables and home improvement, and encourage a modest reacceleration in residential construction activity.

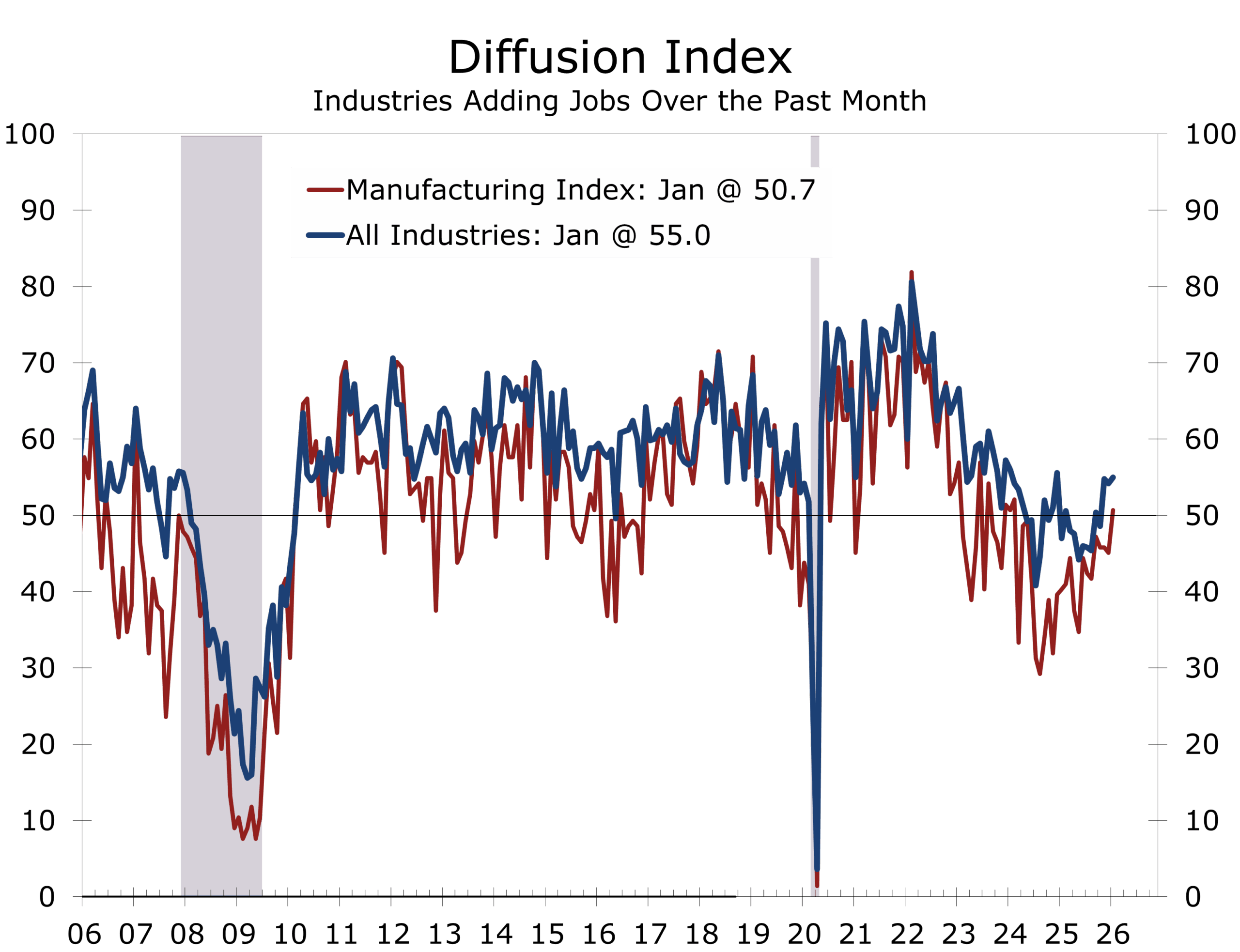

The labor market is not signaling boom conditions. It is signaling that downside risks have diminished and that cyclical momentum may begin to complement the structural, capital-intensive expansion already in place. If hiring breadth expands — the 1-month diffusion index rose back above 50 in January — and hours continue to improve, markets may reassess second-half growth expectations. Longer-term yields could stabilize, and credit conditions may ease further as recession concerns fade.

For now, the message is balance. Not overheating. Not contraction. And balance is precisely what sets up a classic cyclical recovery.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 11, 2026

Mark Vitner, Chief Economist

(704) 458-4000