Kevin Warsh as Fed Chair: Key Takeaways

-

- Credible nomination: Kevin Warsh is a serious, market-literate choice with a clear framework focused on restoring Federal Reserve credibility.

- Targeted hawkishness: Warsh is hawkish on balance-sheet expansion and QE, not reflexively hawkish on growth or rate cuts.

- Misread by markets: The initial market reaction priced Warsh as a broad tightening signal, pushing long yields higher and pressuring risk assets, but that interpretation overlooks his distinction between rate policy and asset reflation.

- Inflation context matters: Inflation has eased toward its long-run trend, but today’s PPI release underscores uneven upstream pressures, reinforcing the need for vigilance.

- Capital-driven economy: The expansion is increasingly powered by capital deepening and productivity rather than consumption leverage, reducing overheating risk.

- Warsh fits this phase of the cycle, inflation vigilant, credibility focused, and increasingly optimistic about capital-led growth. The central risk is not excessive tightening but rather underestimating how much credibility itself has become policy.

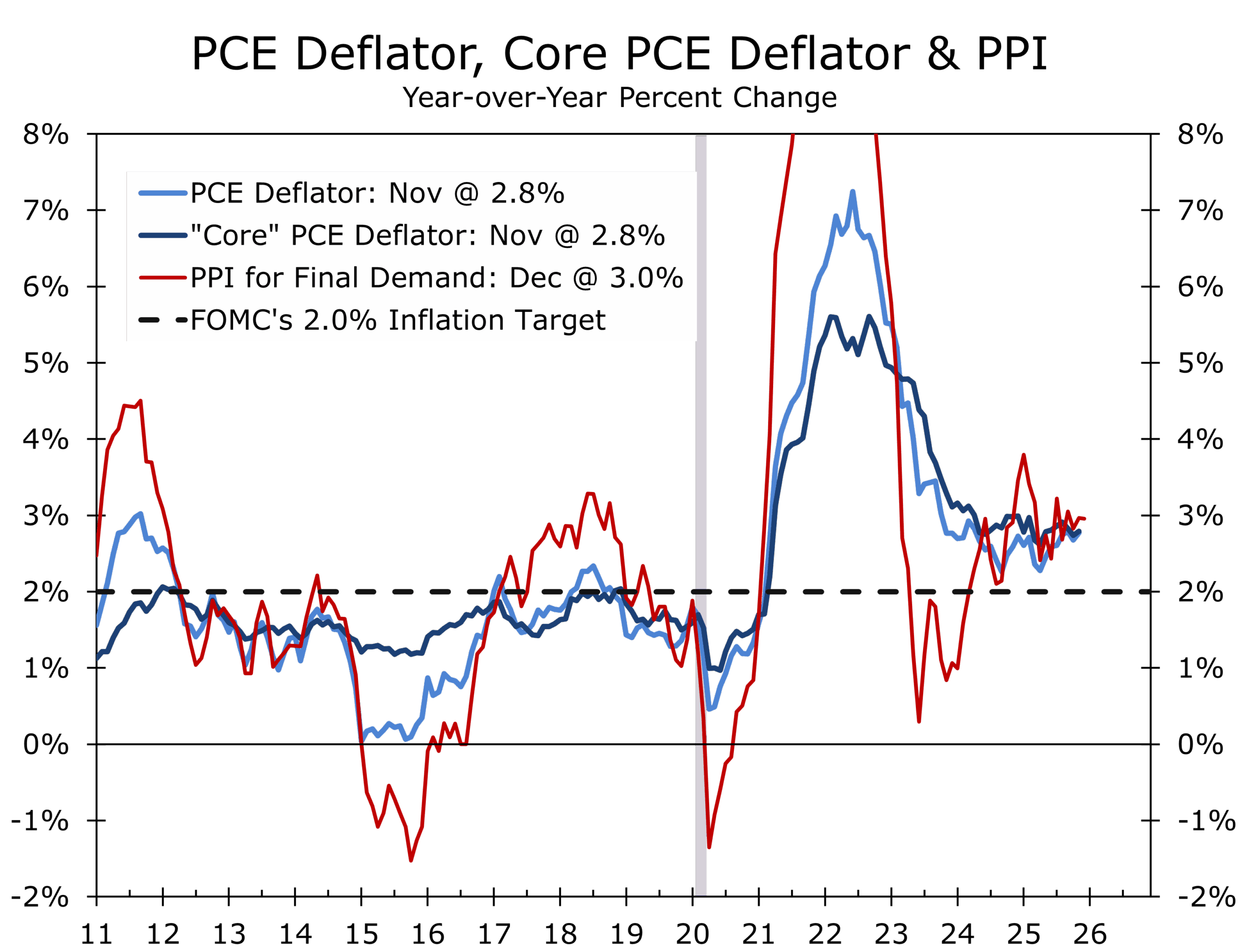

Headline Inflation: A Firm Finish to the Year

President Trump’s nomination of Kevin Warsh as Federal Reserve Chair is a strong and credible choice. From a short list of qualified candidates, this outcome appeared increasingly likely. Warsh’s hawkish reputation is well earned, rooted in his focus on inflation credibility and long-standing criticism of the Federal Reserve’s oversized balance sheet. At a time when institutional credibility itself has become a market variable, that focus matters.

Importantly, Warsh’s hawkishness is targeted rather than ideological. He has consistently drawn a line between interest rate policy, which can support real economic activity as inflation cools, and balance-sheet expansion, which he believes blurred the Fed’s mission, distorted capital allocation, and weakened public confidence. That distinction was largely missed in the initial market reaction, which treated the nomination as a signal of across-the-board tightening.

Warsh is hawkish when it comes to the Fed balance sheet but pragmatic about growth.

Today’s Producer Price Index release reinforces why inflation vigilance remains essential. While the broader disinflation trend continues, upstream price pressures remain uneven, particularly in services and categories tied to energy, logistics, and geopolitics. In that context, Warsh’s emphasis on discipline and credibility is less a brake on growth than a necessary guardrail.

The Market’s Initial Read

The immediate market response reflected a shallow interpretation of Warsh as a pure hawk. Long-term Treasury yields moved higher, equities sold off with rate-sensitive sectors leading the decline, and precious metals retraced sharply as the dollar firmed. Crypto assets traded heavy, as liquidity assumptions were reset.

The markets heard “hawk.’ Warsh’s record points to credibility first and flexibility second.

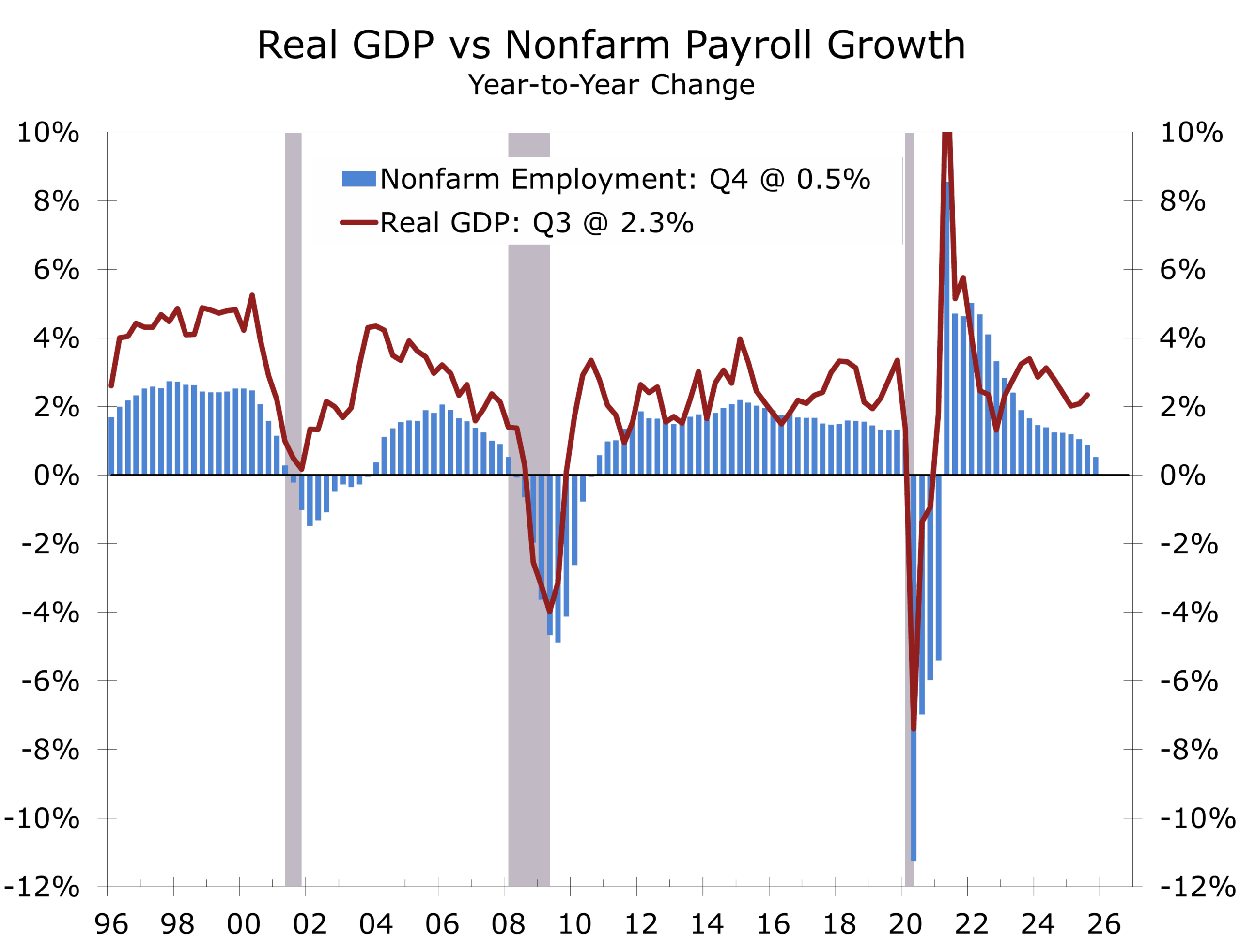

The economy continues to confound late-cycle pessimism. Growth is shifting away from consumption-led sugar highs toward capital-intensive, productivity-driven endeavors. Capital spending is adding meaningfully to growth. Our baseline outlook assumes productivity growth near 2.7 percent, with headline inflation approaching 2 percent by year-end even as real GDP growth runs at around a 3 percent pace.

Several forces support that view. Capital deepening is expanding supply capacity faster than demand, which is disinflationary and margin supportive. Inventory rebuilding and a gradual thaw in housing activity are stabilizing demand without recreating excess. Fiscal policy remains supportive, with the first-quarter FY2026 deficit near $600 billion, cushioning private-sector softness. Labor markets remain in a low-hire, low-fire regime, with jobless claims near cycle lows and participation stabilizing.

The PPI data highlights the tension in this environment. Consumer-level inflation is cooling, but pockets of upstream pressure remain. That combination argues for a Fed chair who is neither complacent nor reactive.

Warsh’s Stance: Hawkish Roots, Productive Optimism

Warsh’s path to the Fed runs through Wall Street, public service, and his tenure as a Fed Governor from 2006 to 2011. Like Chair Powell, he is not a PhD economist, but he brings deep market awareness and institutional memory. His hawkish instincts were evident during the post-crisis period, particularly in his skepticism toward inflation risks and large-scale asset purchases.

More recently, his thinking has evolved without abandoning discipline. Warsh has acknowledged that rates should be lower in a world where artificial intelligence and capital deepening raise productive capacity. At the same time, he has remained firm in his view that an expansive balance sheet and repeated QE undermine the Fed’s credibility and misallocate capital. He has also criticized regulatory burdens on smaller banks, aligning with a more pragmatic supervisory approach.

This is where the caricature breaks down. Warsh is not hostile to easing in principle. In a capital-driven economy, he recognizes that growth can remain strong without running hot. That view fits squarely with our protein-over-sugar thesis.

The Balance Sheet Reality

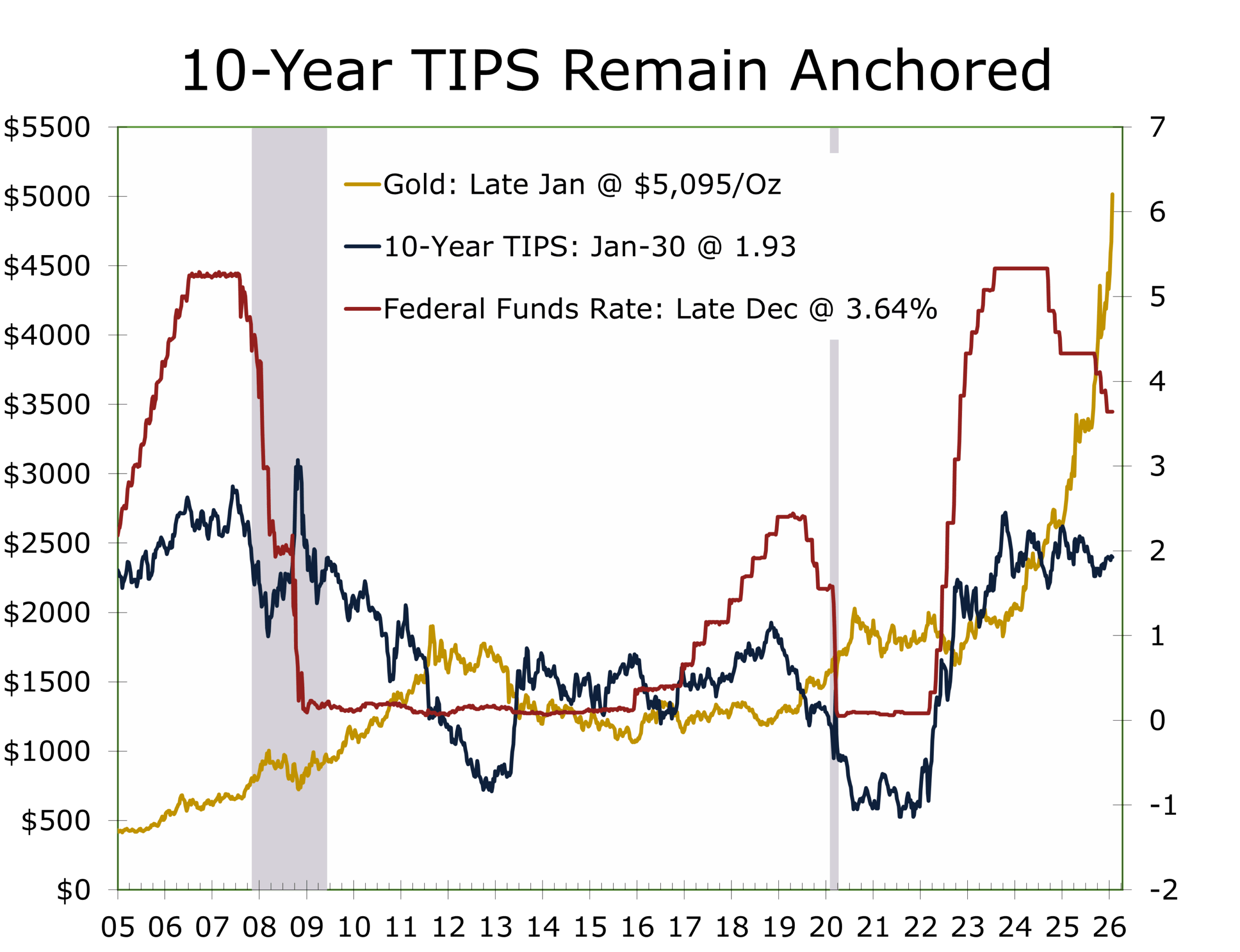

Warsh’s critique of the Fed’s balance sheet is well documented. The Fed still holds roughly 14 percent of outstanding Treasuries and about 25 percent of agency mortgage-backed securities, amounting to more than 20 percent of GDP. Structural constraints make rapid shrinkage unlikely. The more realistic outcome is a shift in emphasis, away from balance-sheet tools and toward clearer separation between monetary policy and asset-price management.

Warsh’s hawkishness targets QE and reflects openness to a productivity-led expansion.

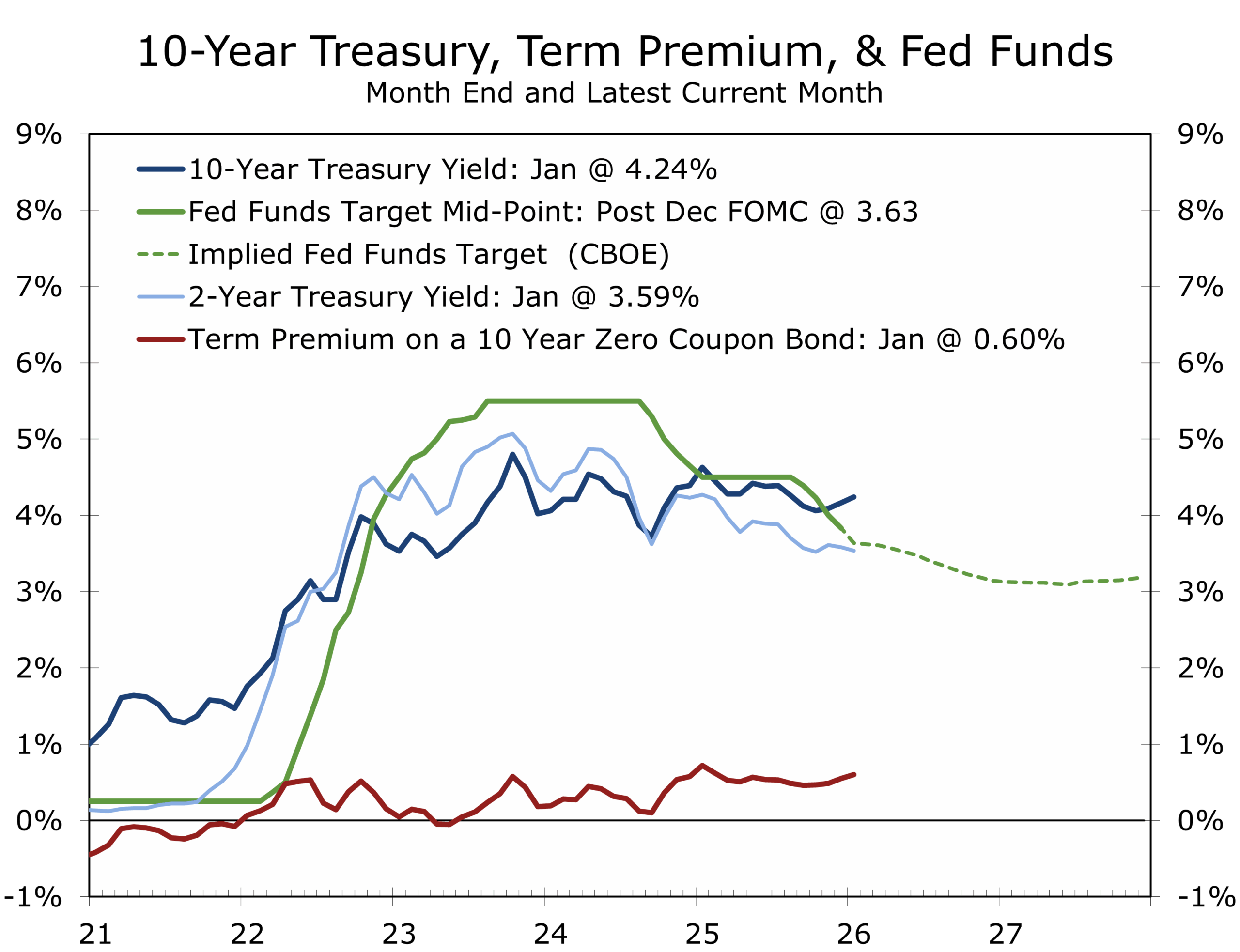

Confirmation should be achievable but not automatic. Political friction around Fed leadership and independence remains a live issue, and even the perception of interference feeds directly into term premia, currency markets, and real-asset hedging. For markets and corporate decision-makers alike, Fed optics now matter almost as much as the policy path.

That backdrop includes the unresolved legal dispute involving Federal Reserve Governor Lisa Cook, whom the Administration sought to remove in August 2025 over mortgage-fraud allegations, which Cook denies. Courts blocked the removal under the Federal Reserve Act’s “for cause” standard, and the case is now before the Supreme Court, raising broader questions about presidential authority and central bank independence.

We expect the Administration to shift toward a more neutral posture during Warsh’s confirmation. The emphasis is likely to move toward governance and institutional stability rather than confrontation, providing him a clear runway into hearings and tenure while also building constructive momentum ahead of the State of the Union.

Implications for Market Participants

Policy continuity at the FOMC limits abrupt change, but Warsh may be more willing to cut rates ahead of the dots if inflation continues to cool. Bond markets remain vulnerable to credibility and fiscal risk, particularly at the long end. Equity valuations depend more on profit execution than multiple expansion. Energy markets continue to emphasize reliability over direction, with recent natural gas volatility reinforcing that lesson. Precious metals remain hedges against policy and governance risk rather than inflation plays.

Kevin Warsh is well suited to this phase of the cycle. He is inflation vigilant, credibility focused, and increasingly confident that a capital-driven economy can grow without overheating. The divergence between real GDP growth and employment is likely to persist, keeping pressure on the Fed to ease. The central risk is not reflexive tightening, but markets underestimating how much credibility itself has become policy.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 30, 2026

Mark Vitner, Chief Economist

(704) 458-4000