Highlights of the Week

- The U.S. economy is settling into a two-speed pattern—services expanding, manufacturing contracting—keeping growth positive but slowing.

- Labor softening is broadening, and with BLS data delayed, survey-based indicators now carry outsized influence for the Fed.

- A December rate cut is widely expected, but the internal dispersion among FOMC members increases the odds of a hawkish cut.

- Treasury markets signal a narrowing easing path for 2026, making optionality critical for financial decision-makers.

- Geopolitical risks remain elevated but contained: Ukraine’s attrition, Middle East fragility, and persistent PLA pressure on Taiwan.

- The new U.S. National Security Strategy frames Europe’s challenges in civilizational terms, signaling a more conditional American posture.

- The coming weeks will test the Fed’s ability to manage a slowing labor market via actions and statements without reigniting inflation expectations, setting the tone for the 2026 policy path and setting the stage for a second half rebound.

A Two-Speed Expansion Enters a Cooling Phase

Financial markets ended the week with a calm that felt slightly at odds with the underlying economic tone. Equity indices hovered near all-time highs, volatility receded, and modestly stronger data from Europe and China offered reassurance that the global soft landing remains intact. Yet beneath the surface, the internal gears of the U.S. economy are turning more slowly. The labor market is softening more sharply and more broadly, the services sector is shedding some of its earlier momentum, and manufacturing remains modestly but firmly in contraction. Stability persists, but with diminishing buffers and a steeper glide path than markets appreciated a few weeks ago.

The soft landing remains alive, but the labor market is cooling in breadth, not just in pockets.

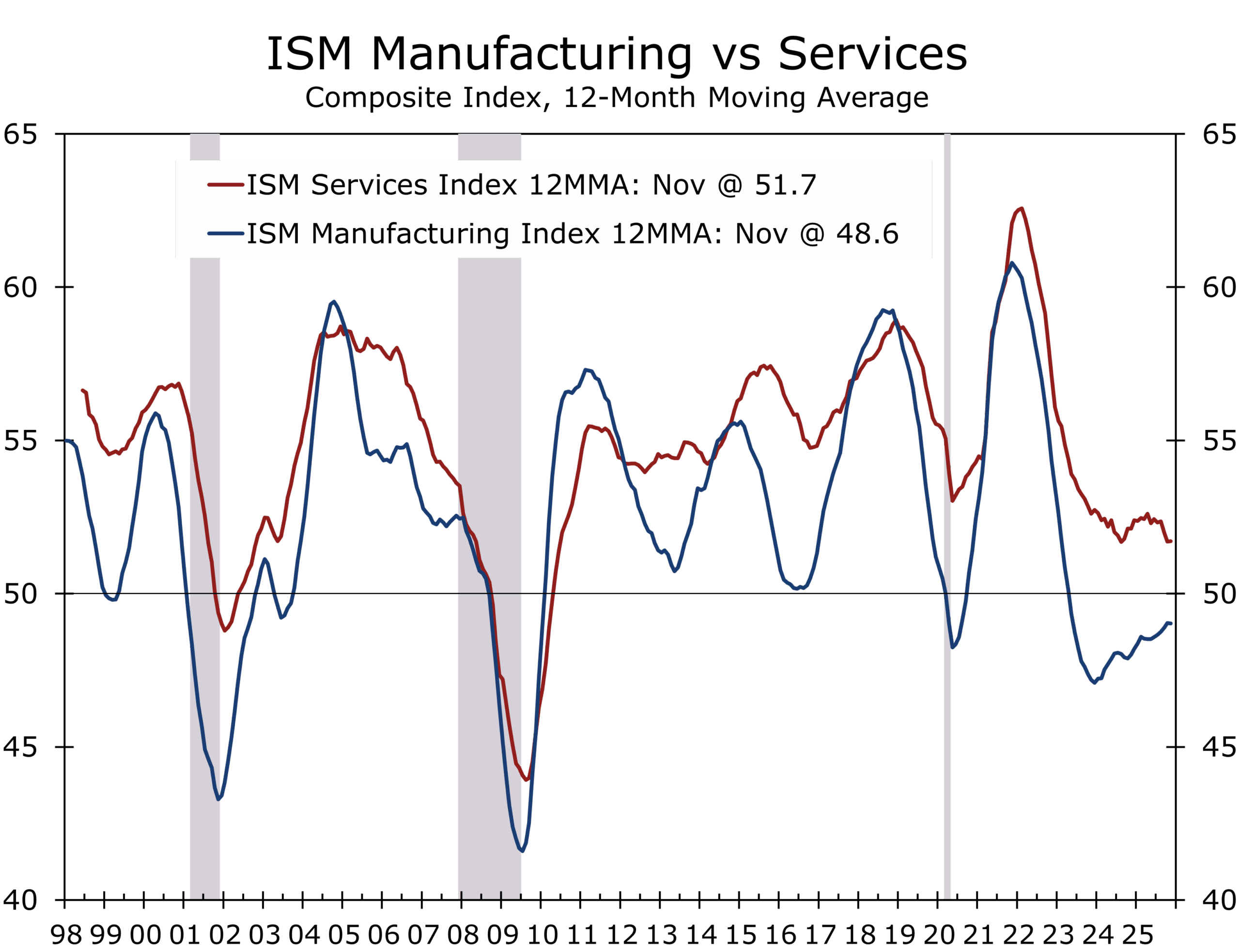

The two-speed economy is now unmistakable. Services remain the dominant engine of the post-pandemic period and continued to expand. The ISM Services PMI rose to 52.6 in November. Business Activity held at 54.5, and backlogs surged to their highest level since early 2025. These indicators collectively point to an economy growing at roughly a 1.3% annualized pace. Yet the deeper trend is drifting downward: the 12-month average of the Services PMI sits at its lowest reading since 2010, evidence of a maturing cycle rather than an accelerating one.

The ISM Survey is consistent with our key call for 2026, which sees the economy getting off to a sluggish start in the New Year but catching its second wind by mid-year.

Manufacturing, meanwhile, is charting a different trajectory. The ISM Manufacturing PMI contracted for the ninth consecutive month, slipping to 48.2, with new orders, backlogs, and export demand all under pressure. Producers are not signaling collapse, but rather caution—rooted in tariff volatility, compliance frictions, and lingering effects of the government shutdown. Customer inventories remain unusually lean, a condition that typically precedes a restocking cycle. But managers remain hesitant, preferring liquidity and flexibility over scale until policy uncertainty clears.

Weakness that began in goods production is now visible across the labor landscape.

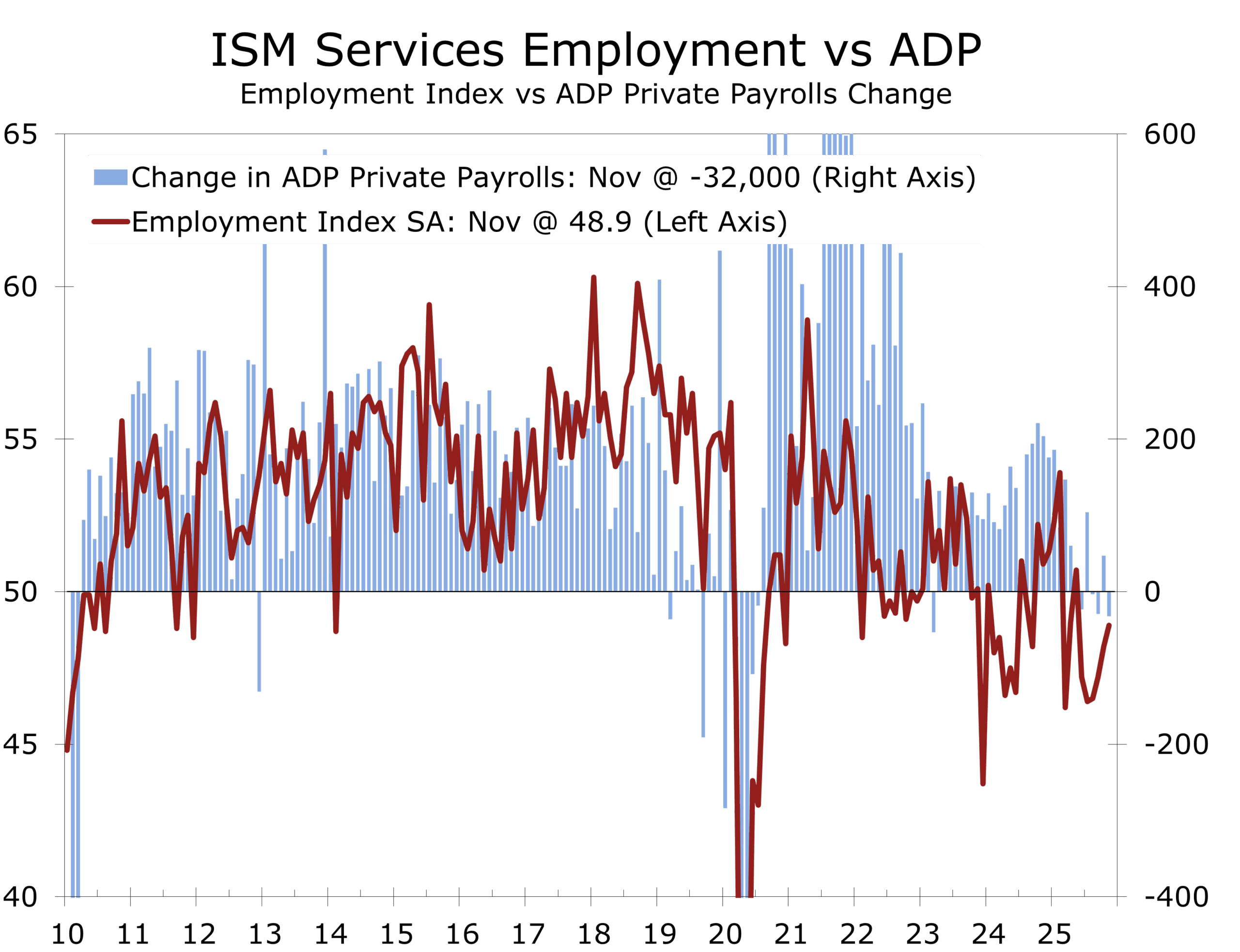

The labor market delivered the most consequential signals of the week. ADP reported a 32,000 decline in private payrolls; Challenger layoffs softened slightly from October’s spike but remain 24% above year-ago levels; and both ISM employment readings remained in contraction—Services at 48.9, Manufacturing at 44.0. Until recently, hiring weakness had been concentrated in rate-sensitive pockets of the economy. Now it is broadening across middle-skill service industries and goods-producing sectors. With the federal shutdown delaying fresh BLS payroll and CPI releases, the Fed must rely more heavily on these forward-looking indicators, which carry decisive weight heading into the December FOMC meeting.

A Hawkish Cut Comes into View

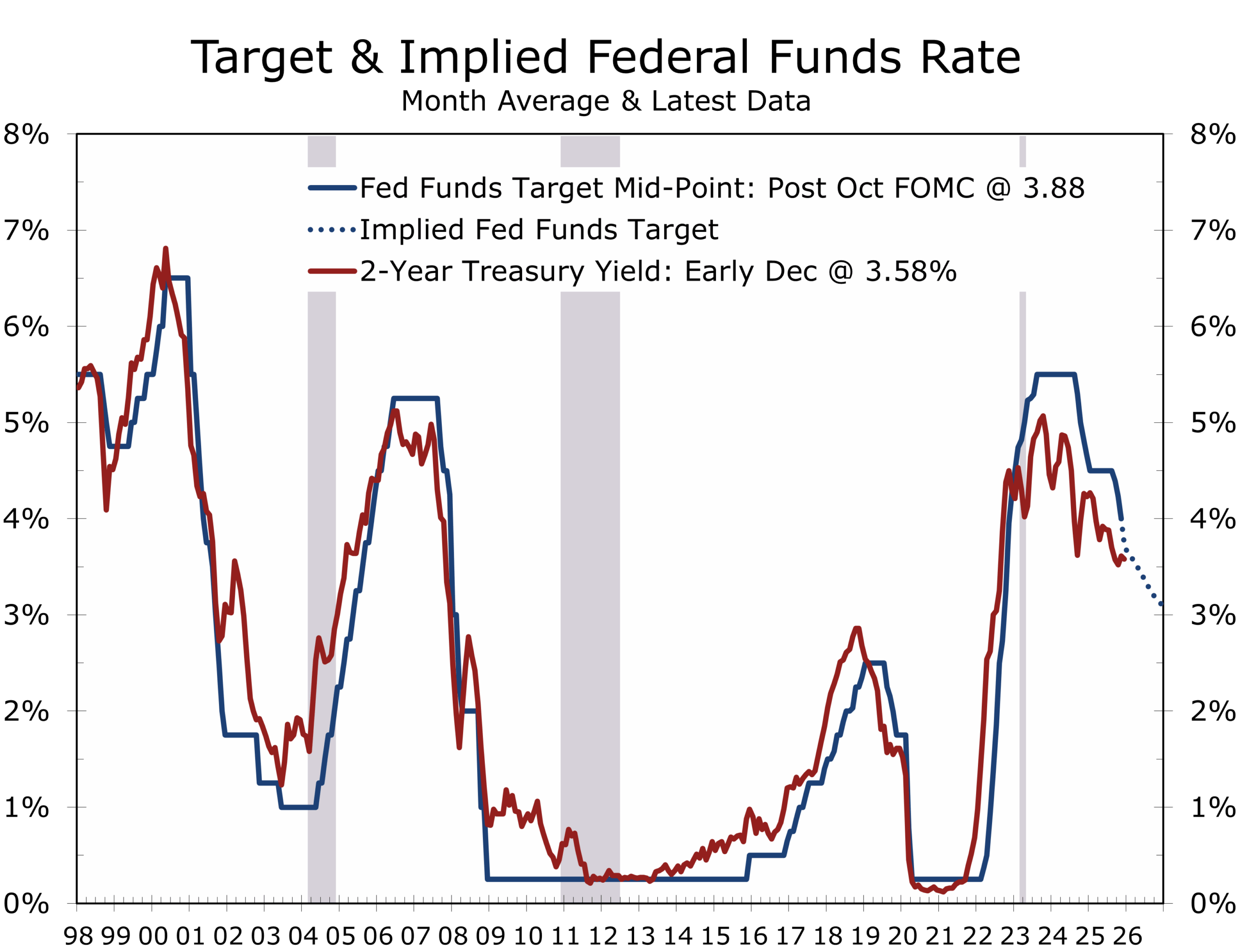

The policy implications are significant. The Fed is almost certain to cut rates this week, but the broader narrative remains unsettled. The dove bloc argues that risks to employment now outweigh risks of lingering inflation and that tariffs represent a one-time shift in price levels rather than a persistent inflationary force. Centrists emphasize careful progress toward the neutral rate. The hawks warn that financial conditions have eased too quickly and that another cut risks weakening the Fed’s credibility. Powell’s challenge is to deliver an easing step that arrests the downward drift in the labor market without signaling a broad pivot.

The Fed must cut to steady hiring but must do so without undermining inflation credibility.

What the market increasingly anticipates is a hawkish cut: one that acknowledges the labor softening while clearly conveying that the Committee is not embarking on a rapid or extended easing cycle.

From a financial management standpoint, this environment requires a more tactical interpretation of the yield curve. The front end remains anchored to the near-certain December cut, but expectations for additional easing have thinned. The long end continues to face upward pressure from Japanese yield dynamics and heavy Treasury issuance. Funding markets remain stable, with abundant liquidity, and tight credit spreads—but duration volatility is still elevated.

This is a moment to preserve optionality: maintain staggered maturity ladders, extend duration opportunistically, and consider timely pre-funding of 2026 obligations. The December cut should be viewed as a calibration of policy, not the beginning of a deeper easing sequence.

Global Dispersion and the Strategic Backdrop

Globally, monetary dispersion has returned. Japan’s upward pressure on yields remains a key undercurrent in global fixed income. Switzerland has not ruled out unconventional measures if the franc strengthens excessively. Australia, Brazil, Canada, and Türkiye all continue to move in divergent directions. The post-tightening era is not synchronized easing but a landscape of increasingly differentiated monetary paths and heightened FX sensitivity.

Geopolitically, the global map remains tense but contained. Ukraine enters winter under considerable strain as Russia employs more sophisticated drone and artillery tactics. The Gaza ceasefire remains fragile but holds for now, with particularly intense fighting around tunnel networks. PLA air and naval activity around Taiwan remains elevated, reinforcing long-term strategic risk in the Indo-Pacific. Markets have absorbed these developments with guarded calm, but that calm depends heavily on diplomatic bandwidth.

A two-speed economy narrows the margin of policy error, particularly in early 2026.

This backdrop echoes in the administration’s newly released National Security Strategy, which employs unusually stark language about Europe’s future. It warns that demographic decline, institutional fragmentation, migration pressures, and insufficient defense investment could leave parts of the continent “unrecognizable in 20 years.” The Strategy reframes Europe less as a postwar project and more as a civilization confronting internal drift. The United States signals continued engagement—but on more conditional terms, emphasizing burden-sharing, energy security, and renewed strategic coherence.

Our view is that the soft landing remains achievable but increasingly delicate. Services continue to provide lift, but with diminishing thrust. Manufacturing remains cautious. Labor is softening more broadly. Inflation continues to ease, but not uniformly. And the Fed must execute a careful recalibration: supportive enough to prevent unnecessary labor weakness, firm enough to preserve credibility, and clear enough to avoid sending markets sprinting ahead of policy.

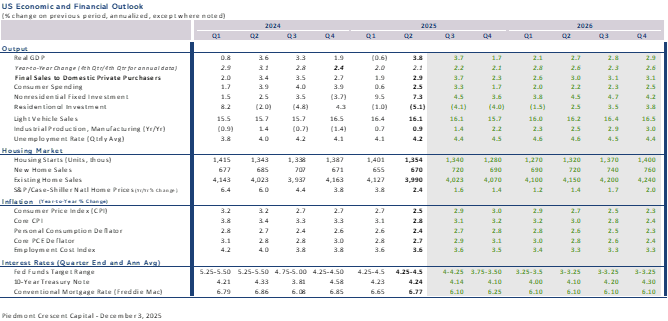

Private Final Domestic Demand is likely to be weakest at the tail end of 2025 and early 2026. We look for interest-rate-sensitive sectors (housing and consumer durables) to begin to improve by summer and look for inventory rebuilding to add modestly to overall growth.

The economy retains its resilience. But resilience requires continuous adjustment—small corrections made at the right moments to keep the wings level as the air grows thinner. Over the weeks ahead, the skill with which policymakers navigate this narrowing runway will determine whether the economy glides its way into a soft landing or stalls out.

The Week Ahead: December 8-12

The government’s statistical agencies continue to play catch up but the Fed will have to make its decision relying on a mix of private, government and anecdotal reports. The Fed has enough information to make an informed decision.

Tuesday, December 9

NFIB Small Business Optimism (Nov): We are looking for a modest decline in Small Business Optimism, reflecting slowing and uncertain sales and stubborn cost pressures.

JOLTS Job Openings (Sep & Oct): The JOLTS report will provide a much needed update on the labor market. Look for a decline in job openings.

Wednesday, December 10

Employment Cost Index (Q3): We may see slightly more easing on wages, but benefits will likely hold firm. Overall, we look for the ECI to be up 3.6% year-to-year.

FOMC Statement & Powell Press Conference: We are looking for a hawkish quarter point cut, with three and possibly four dissents (one favoring a larger cut and two against any cut at all). Dissents mean less at this time, as a new Fed Chair will likely be announced ahead of the next FOMC meeting in January.

Thursday, December 11

Initial Jobless Claims (week ended Dec 6): Look for a rebound from last week’s holiday-shortened week decline.

Trade Balance (Sep): we are due for a widening in the trade deficit and look for imports to surge on inventory rebuilding and slightly more clarity on tariffs.

Friday, December 12

Fed Speakers: Philadelphia Fed President Paulson (2026 FOMC Voter), Cleveland Fed President Hammack (2026 FOMC Voter), Chicago Fed President Goolsbee (2025 FOMC voter).

Note: while regional Federal Reserve Bank presidents rotate voting roles by year, all members have a voice at every FOMC meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 8, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000