Key Takeaways from November’s ISM Report

-

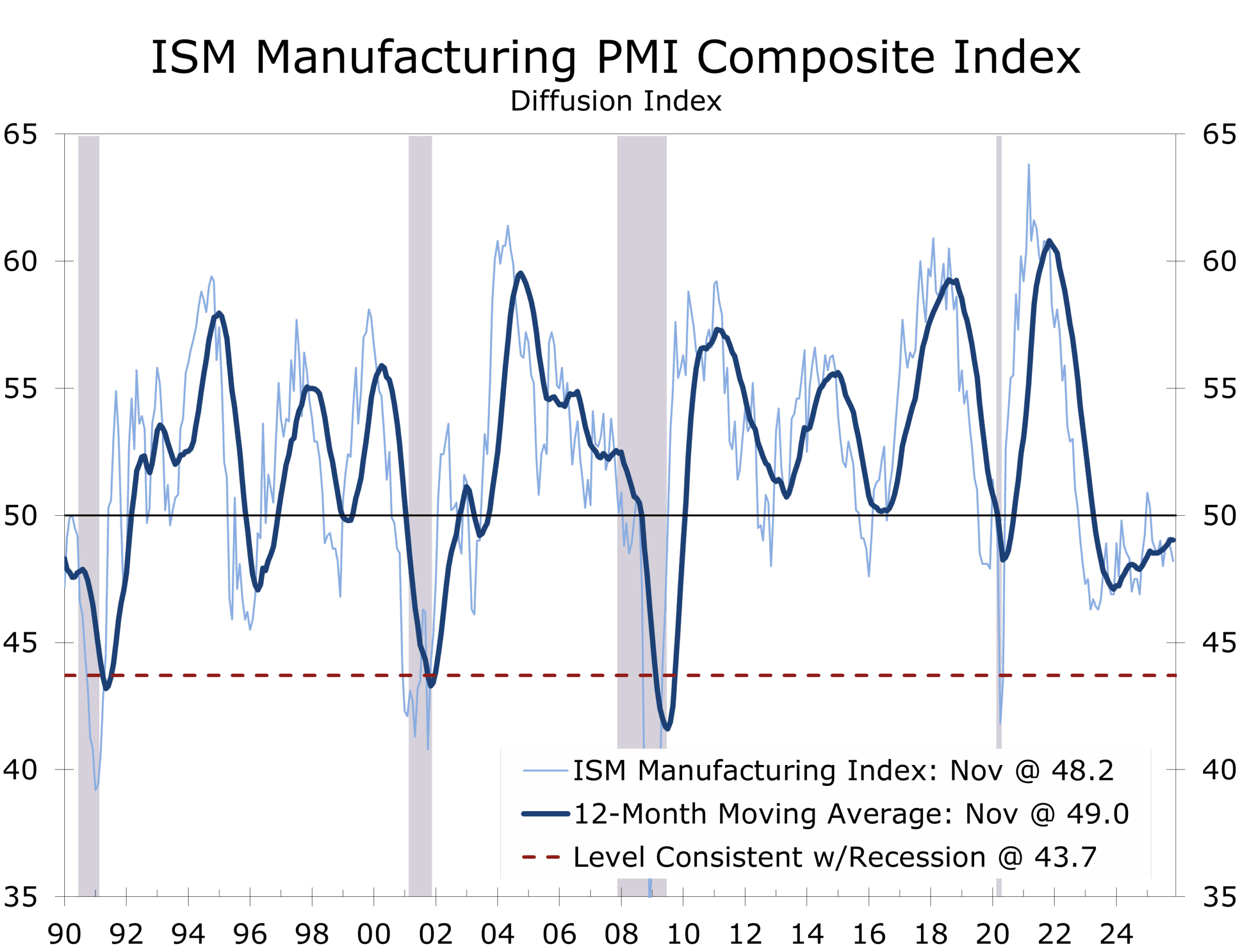

- Manufacturing PMI®: 48.2 (–0.5 pts) — ninth consecutive month of contraction; breadth of softness widened modestly.

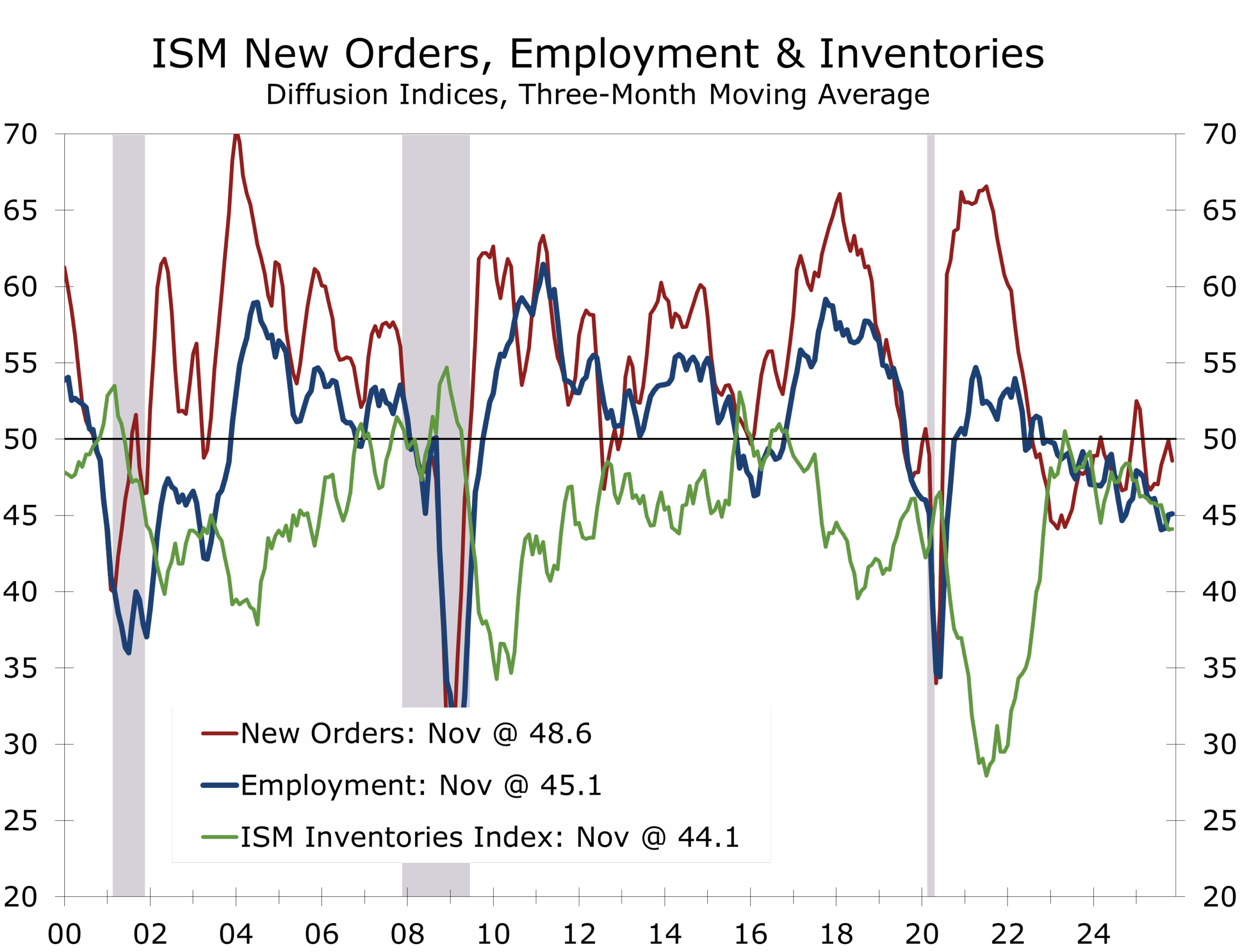

- New Orders: 47.4 (–2.0 pts) — third straight contraction as demand remains uneven.

- Production: 51.4 (+3.2 pts) — returned to expansion, supported by improved component flow and backlog conversion.

- Employment: 44.0 (–2.0 pts) — headcount reductions deepened amid ongoing caution.

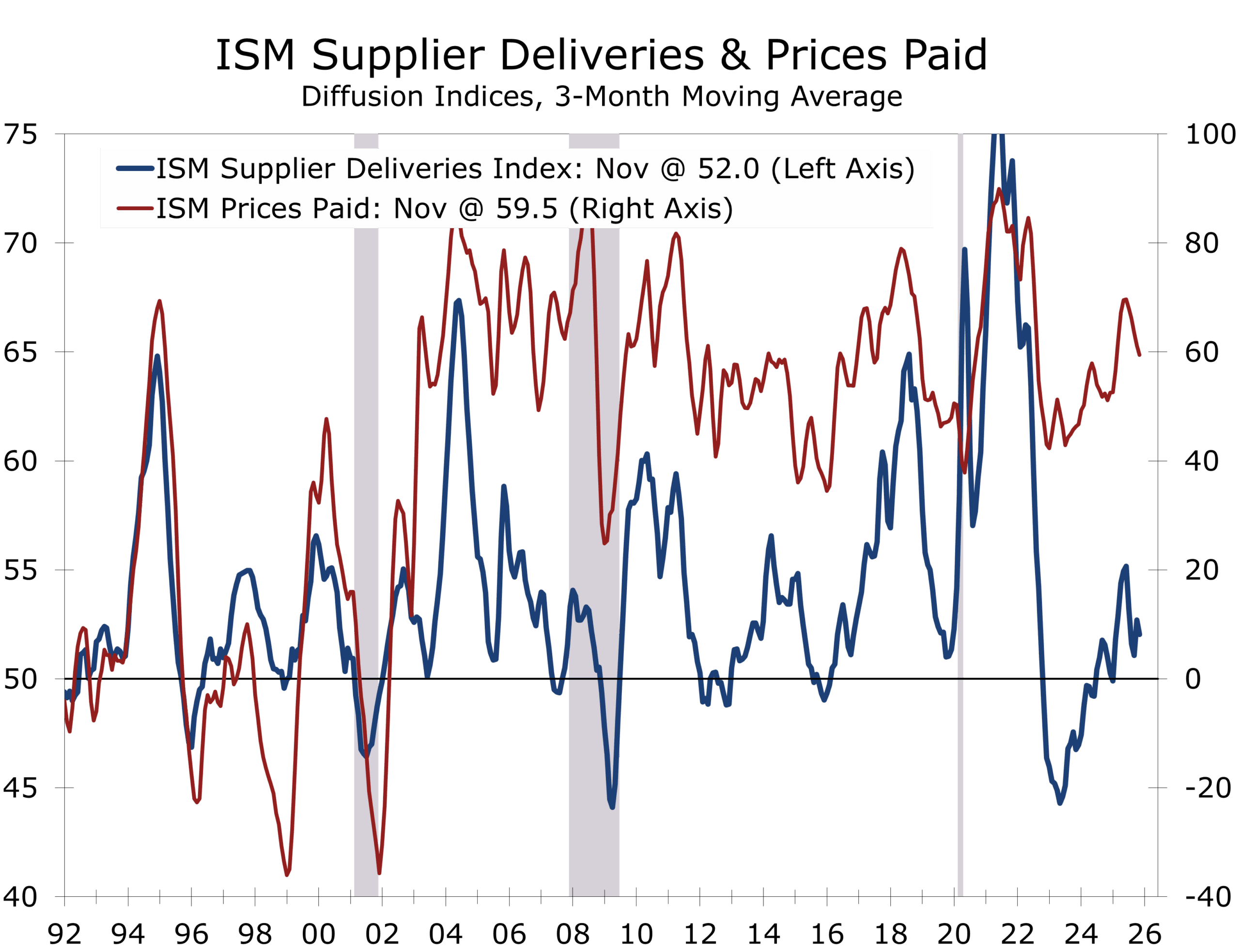

- Supplier Deliveries: 49.3 (–4.9 pts) — faster deliveries, signaling ample capacity and fewer supply chain constraints.

- Prices Paid: 58.5 (+0.5 pts) — input costs rose again, driven by metals and tariff-affected imports.

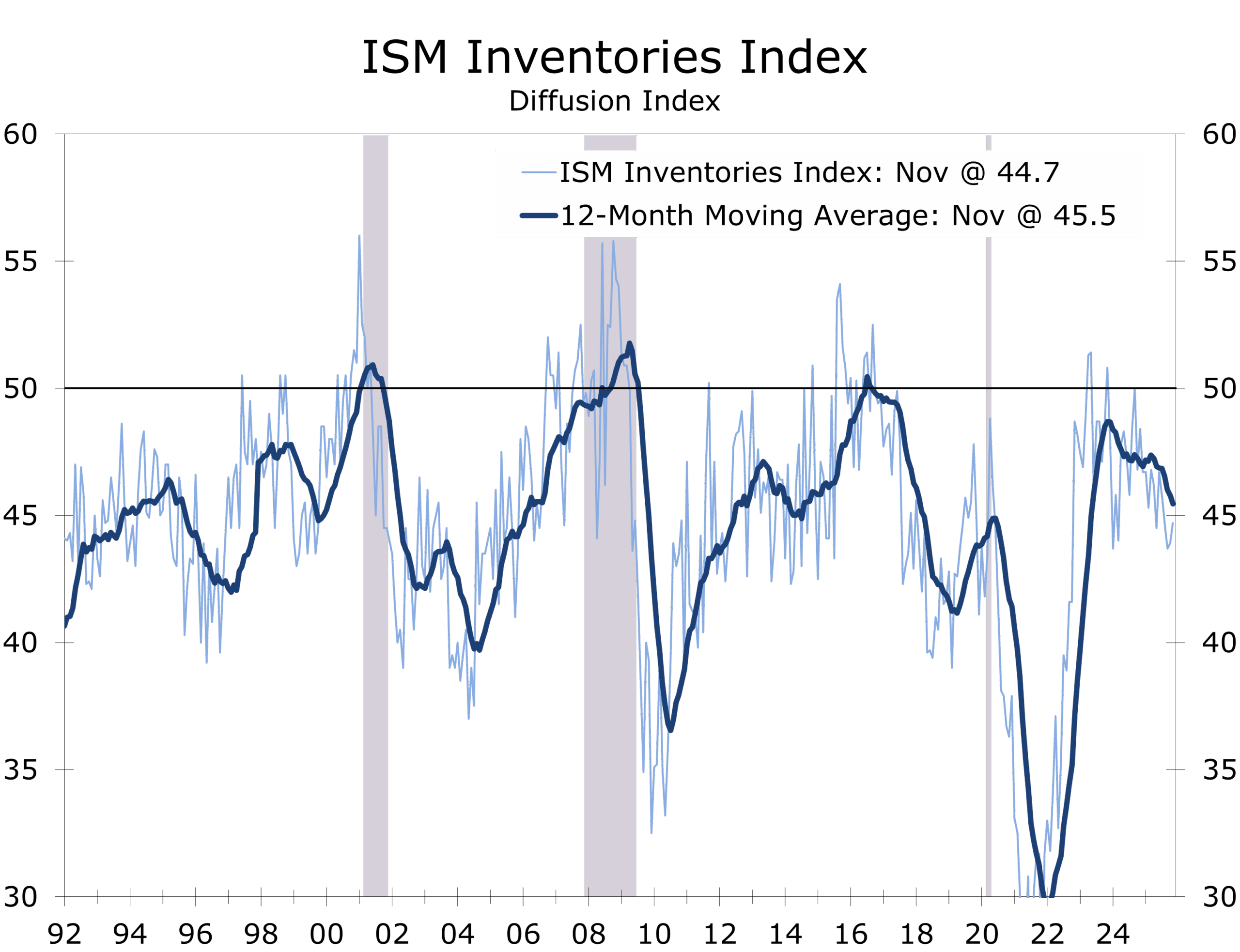

- Inventories: 48.9 (+3.1 pts) and Customers’ Inventories: 44.7 — both remain lean, but firms remain hesitant to rebuild.

- Order Backlogs: 44.0 (–3.9 pts) — pipelines remain thin heading into year-end.

- November’s PMI® corresponds with roughly +1.7% annualized real GDP, consistent with continued overall economic expansion.

Supply Chains Steady, Demand Slips, and Managers Remain Guarded

The ISM Manufacturing PMI® slipped to 48.2 in November, marking a ninth month of contraction and reinforcing the sector’s struggle to regain traction. Readings below 50 reflect breadth of deterioration, not magnitude, and the latest figure remains consistent with a manufacturing sector treading water while the broader economy continues to expand.

November’s report once again displayed the now-familiar pattern: demand softened, production improved, employment contracted, and supplier deliveries accelerated, suggesting that capacity is more than adequate. Input costs remain elevated, with Prices Paid rising to 58.5%, though the tariff-driven run-up appears to be losing momentum, and respondents signaled that cost pressures are starting to ease around the edges.

Production Rebounds, but Orders Slide as Uncertainty Keeps Managers Cautious.

New Orders fell 2 points to 47.4, contracting for a third straight month, while Employment dropped to 44.0, its lowest level since August. Production, however, bounced back into expansion at 51.4, reflecting improved parts availability and execution of previously delayed orders. Inventories rose modestly but remained in contraction, and Customers’ Inventories stayed at “too low” levels, a historically supportive signal once confidence improves.

Despite the weaker PMI, several regional Fed manufacturing surveys report a guarded optimism that 2026 may bring steadier demand and fewer tariff disruptions. For now, manufacturers remain cautious but not pessimistic.

Manufacturers Are Navigating a Two-Speed Cycle

- Demand for goods is weakening, with New Orders, Backlogs, and New Export Orders all in contraction.

- Production is expanding, helped by supply-chain stabilization and conversion of existing orders.

- Employment is contracting faster, as firms preserve liquidity and avoid adding capacity into an uncertain environment.

Panelists again cited tariff volatility, policy uncertainty, shifting international regulations, and inconsistent external demand as central challenges. Nearly two-thirds of manufacturers continue to manage headcount lower, relying on attrition, selective layoffs, and more disciplined labor deployment to boost productivity and protect margins.

Rising jobless expectations signal a softer market for lower-wage and entry-level workers.

Firms continue to operate in a defensive configuration — emphasizing cash-flow discipline, flexible staffing models, streamlined supplier portfolios, and reduced forward commitments. With backlogs thinning further, the sector lacks the “cushion” needed for a near-term snapback in production should orders remain soft.

The uncertainty that defined October became more visible in November. Respondents highlighted:

- Tariff-driven cost volatility in metals, electrical components, and engineered materials.

- Longer import transit times, even as aggregate supplier performance improved.

- Sourcing shifts and planning challenges tied to reciprocal trade actions and compliance changes.

- Lingering shutdown effects in agriculture, transportation equipment, and regulated industries.

- Offshore production adjustments, where firms sought ways to blunt tariff exposure.

The unifying theme: uncertainty, not collapsing demand, remains the dominant headwind and continues to reinforce a “wait-and-see” posture for inventories, hiring, and capital allocation.

Consumers remain cautious—but they’re still spending, prioritizing value and essentials.

The Prices Paid index increased to 58.5, marking the 14th consecutive month of rising costs. Metals (aluminum, copper, hot-rolled steel), critical minerals, and advanced electronics components continue to exert upward pressure. Top of Form

Respondents noted:

- Tighter supplier bases in some materials

- Longer lead times for specialized components

- Elevated landed costs due to tariff structures

- Limited availability of rare-earth magnets and electronic components

While the rate of increase has slowed relative to earlier spikes, cost stickiness remains a challenge, encouraging firms to maintain lean inventories and selective purchasing — a quiet signal to supply-chain teams that diversified sourcing and tighter contract windows may carry outsized strategic value.

Customers’ Inventories rose slightly to 44.7, still firmly in “too low” territory, a condition that historically precedes production upturns once sentiment turns. Inventories increased modestly to 48.9 but remain constrained by caution rather than capacity.

These dynamics mirror the backdrop from October: lean inventories could support a restocking cycle, but policy uncertainty — not supply chains issues — is keeping that demand on hold.

Backlog weakness reinforces that narrative. The Backlog of Orders Index fell to 44.0, its softest reading since spring, signaling minimal near-term lift for production.

Sector Breadth and Structural Takeaways

Four industries expanded in November:

Computer & Electronic Products; Food, Beverage & Tobacco; Miscellaneous Manufacturing; and Machinery.

Eleven contracted, including Apparel, Wood Products, Paper, Nonmetallic Minerals, Fabricated Metals, Chemicals, Petroleum & Coal, Transportation Equipment, and Plastics & Rubber.

The strongest sectors continue to reflect:

- Semiconductor and electronics ecosystems

- Food and beverage, supported by stable consumption

- Machinery and automation, driven by targeted investment in efficiency

Weaker sectors remain concentrated in:

- Construction-related inputs

- Tariff-affected intermediates

- Durables and transportation equipment, where planning visibility remains murky

The breadth of contraction is meaningful but not accelerating, aligning with a sector undergoing incremental adjustment rather than acute decline.

Inventories and Customers’ Inventories Signal Room for Restocking — When Confidence Returns

The November ISM report points to a manufacturing economy navigating a slow-moving adjustment, not a recession. The challenge remains the same as in October: low visibility, variable costs, and policy volatility are suppressing risk-taking at a time when inventories and customer stock levels would ordinarily support a modest rebuild.

The combination of thin backlogs, lean customer inventories, still-elevated input costs, and heightened geopolitical and trade friction, suggests that stabilization is possible in early 2026 if policy clarity improves. Until then, manufacturers are likely to remain defensive, focusing on flexibility over scale and liquidity over expansion.

Implications for the Federal Reserve

The ISM Manufacturing report neither accelerates nor derails the Fed’s path. While the factory sector is contracting at a slightly faster pace, the overall economy is still growing modestly, consistent with our Q4 real GDP forecast at 1.7%. This supports the view that near-term rate cuts should be approached cautiously, not urgently, and that manufacturing will not be a source of renewed inflation pressure without a significant shift in policy or trade conditions.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 1, 2025

Mark Vitner, Chief Economist

(704) 458-4000