Anecdotes Provide Some Guidance

-

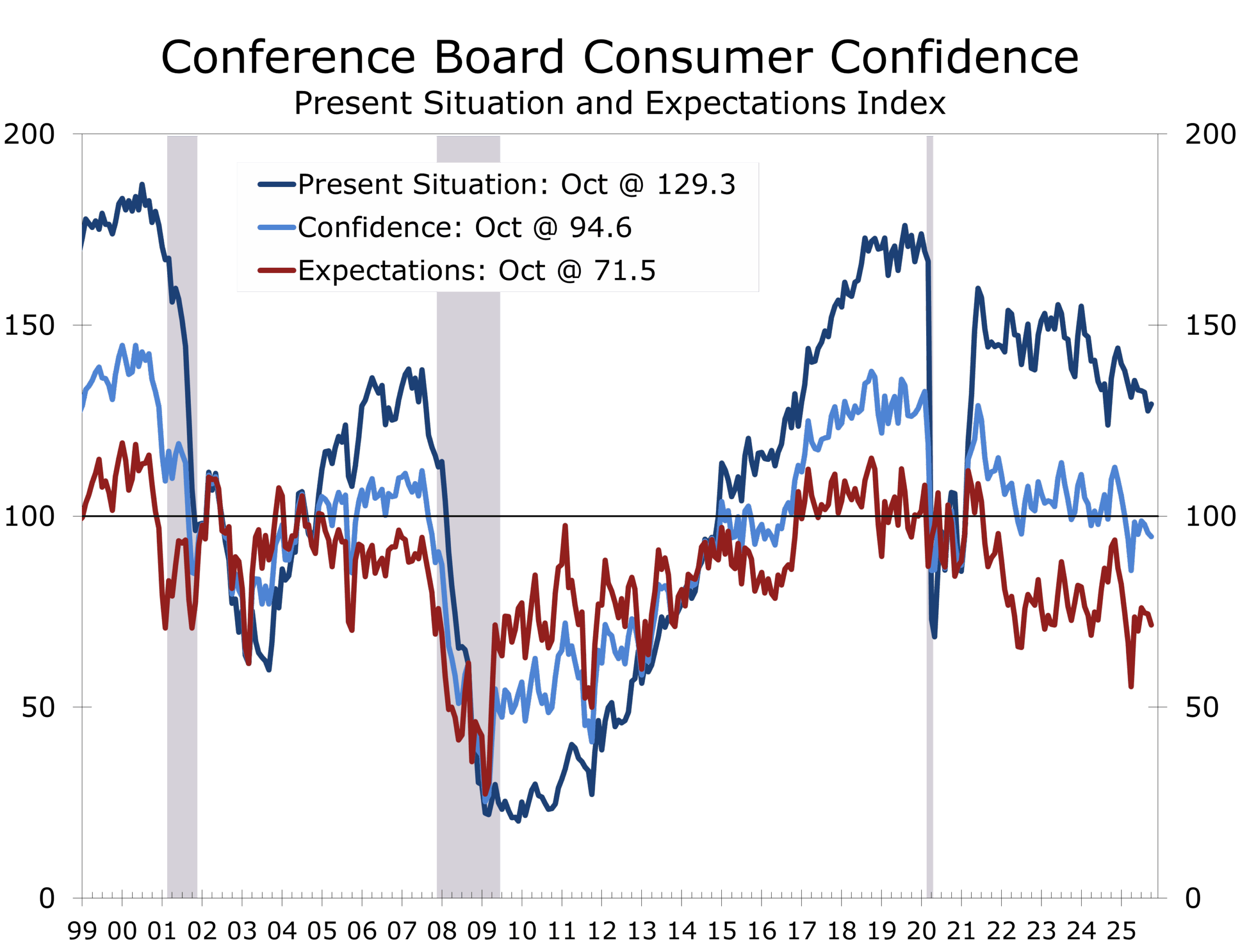

- The Conference Board’s Consumer Confidence Index® slipped 1.0 point in October to 94.6 (1985=100), essentially unchanged from September’s upwardly revised 95.6.

- The Present Situation Index rose 1.8 points to 129.3, while the Expectations Index declined 2.9 points to 71.5 — remaining below the key 80 threshold that historically signals recession risk.

- With most federal data releases delayed by the government shutdown, the Consumer Confidence report provides one of the few real-time signals on household sentiment and labor trends.

- Write-in comments continue to focus on prices, inflation, and the shutdown itself — though mentions of tariffs declined further.

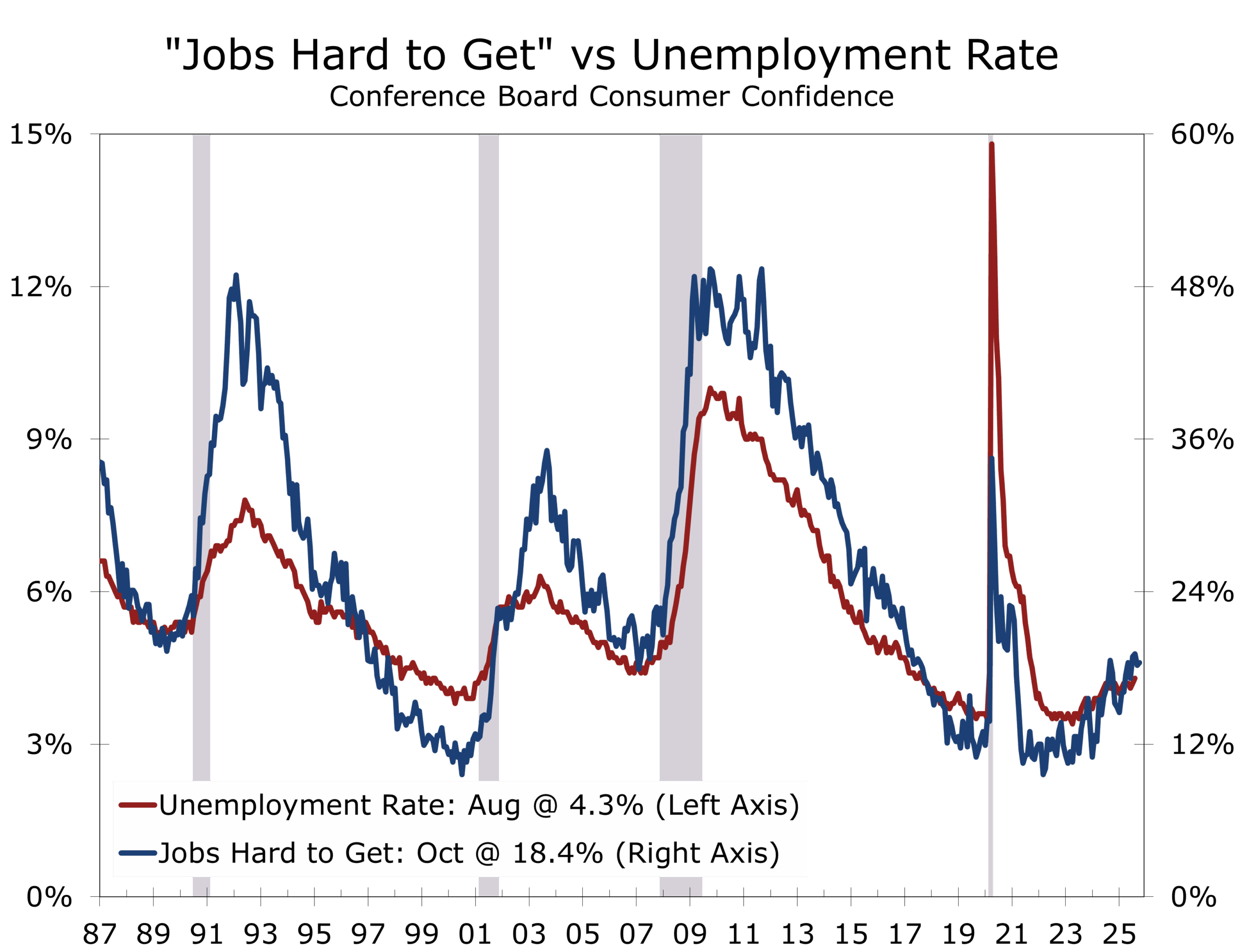

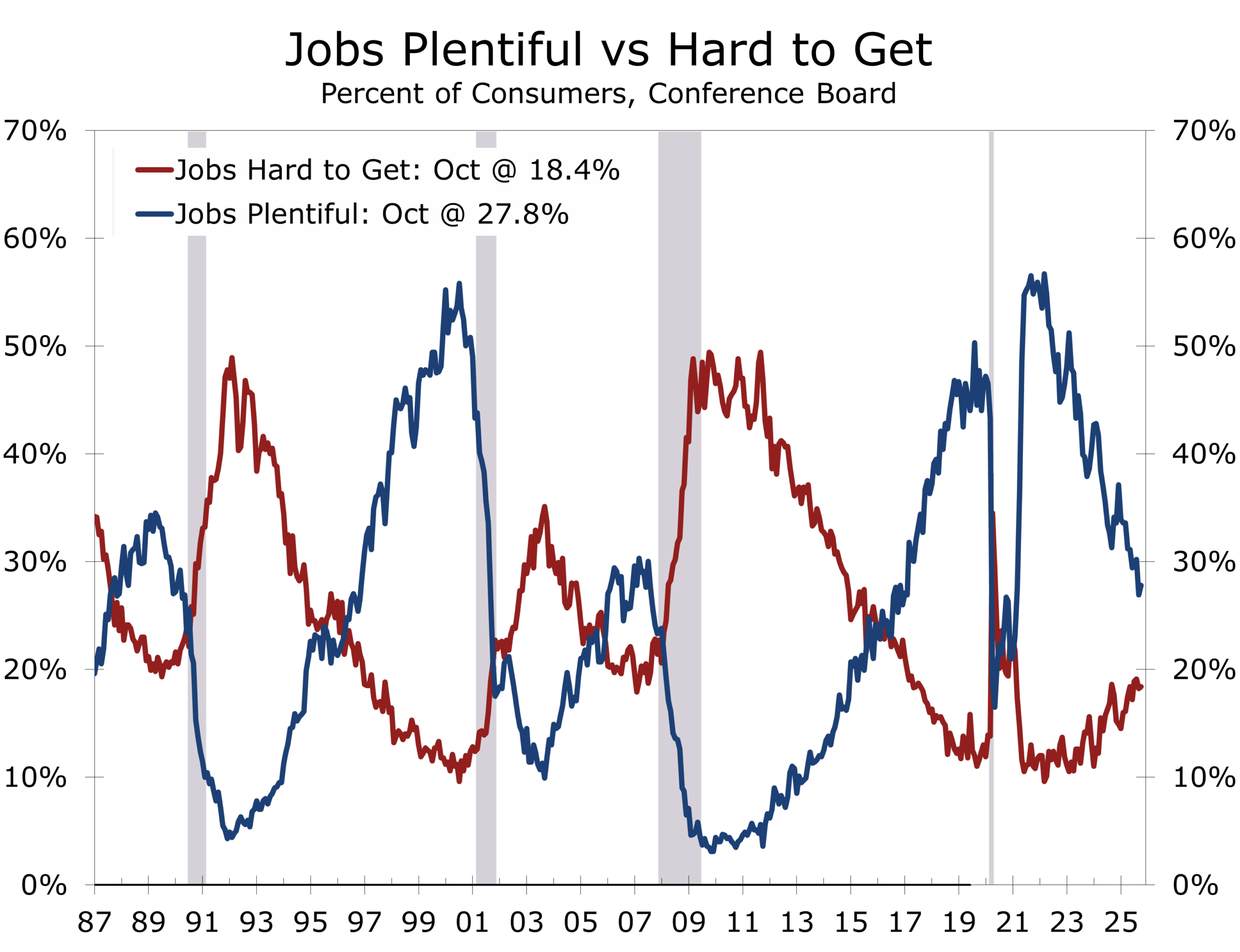

- Views of the job market improved slightly: 27.8% of consumers said jobs were “plentiful,” up from 26.9% in September.

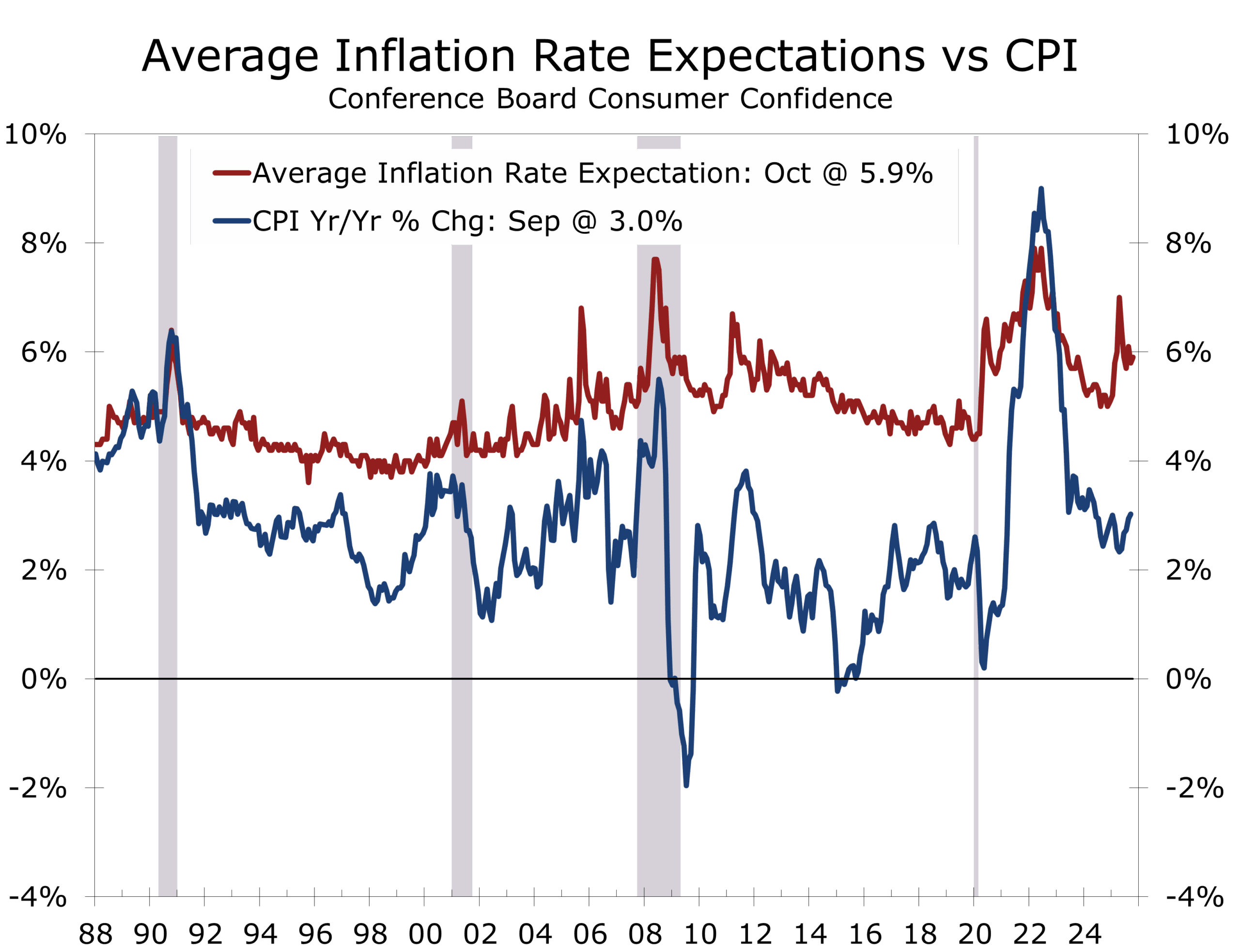

- Inflation expectations edged up to 5.9%, while the share expecting higher interest rates rose to 52.8%.

- October’s confidence readings are consistent with other private data (including this morning’s new weekly ADP report) showing modest payroll growth and a gradual rise in the unemployment rate. The Chicago Fed’s labor market indicator pegs October’s unemployment rate at 4.35%.

Confidence Holds Ground as Data Remains Scarce

With much of the federal statistical system offline during the ongoing government shutdown, this month’s Consumer Confidence report carries unusual weight. In the absence of payroll, retail sales, and inflation updates, the Conference Board survey offers rare, consistent insight into how households perceive current and future conditions. Historically, shifts in its labor market components — particularly the “jobs plentiful” and “hard to get” series — have led changes in nonfarm payrolls by one to two months.

Confidence edged lower, but revisions point to stronger underlying sentiment.

In October, confidence effectively moved sideways. The headline index dipped just one point to 94.6, from an upwardly revised September reading, with stronger views of current conditions offset by weaker expectations. The Present Situation Index gained 1.8 points to 129.3, while the Expectations Index fell nearly three points to 71.5. That measure has now been below 80 since February — a duration consistent with past pre-recession readings. On net, Consumer Confidence was slightly higher than was previously reported for September, despite falling 1 point from the revised reading.

Labor Sentiment Offers Early Clues

Consumers’ appraisal of the job market improved slightly for the first time since December 2024. The share calling jobs “plentiful” rose to 27.8%, while those calling jobs “hard to get” edged up to 18.4%. The resulting labor differential remains near 9 points — a level consistent with below-trend hiring and a modest uptick in unemployment.

Given the survey’s track record as a leading indicator, the October readings reinforce expectations that the labor market continues to cool, especially in lower-wage and entry-level positions. The latest official unemployment rate for the U.S. is 4.3% for August 2025.

Rising jobless expectations signal a softer market for lower-wage and entry-level workers.

Due to the ongoing government shutdown, however, more recent official data are unavailable. A model from the Federal Reserve Bank of Chicago estimates the jobless rate at around 4.35% for October 2025 and we see the jobless rate eventually rising to 4.5%.

Prices, Shutdown, and Political Fatigue

Consumers’ write-in responses again centered on inflation, which remains the most frequently mentioned concern, followed by the government shutdown and political uncertainty. References to tariffs declined further but remain elevated. Average 12-month inflation expectations edged up to 5.9%, and more than half of respondents expect higher interest rates ahead.

Confidence fell among younger consumers and lower-income households but improved for middle-aged respondents and those earning above $75,000, especially at the top end of the income spectrum. By political affiliation, the Conference Board noted that confidence increased among Independents but slipped among Democrats and Republicans alike.

Spending Signals Mixed but Holding Up

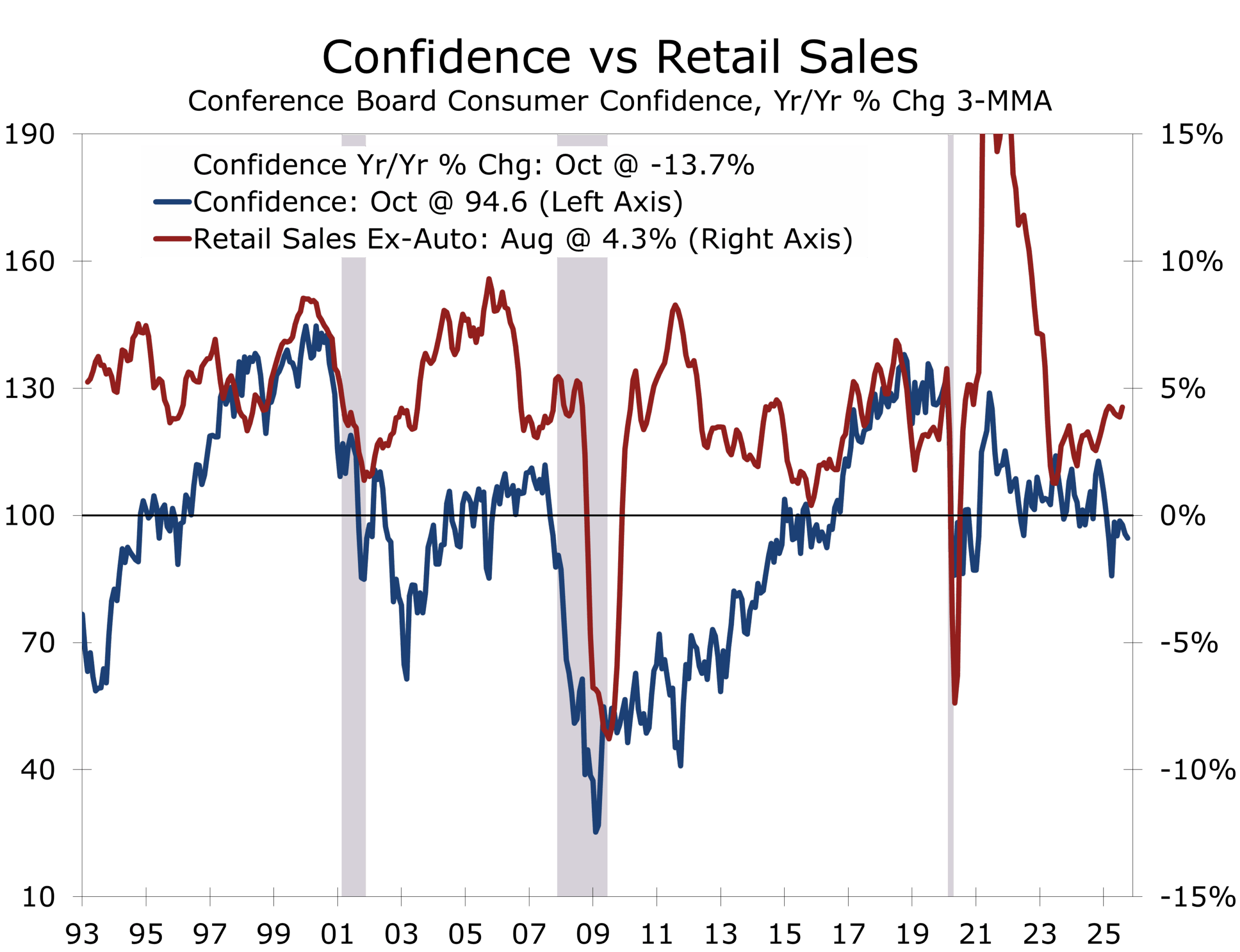

Despite downbeat expectations, spending behavior continues to outperform confidence measures. Purchasing plans for cars rose in October, driven by used vehicles, while home-buying plans weakened but remain higher on a six-month trend basis. Intentions to purchase big-ticket items were steady overall, and spending on services — particularly pet care, streaming, and vehicle maintenance — showed renewed strength.

Consumers remain cautious—but they’re still spending, prioritizing value and essentials.

We are looking for a 4.8% rise in holiday-related spending this year. Consumers cited promotions and “getting the most out of every dollar” as their main motivators — an early sign that value and price sensitivity will dominate this holiday season. That said, higher-end retailers will likely do best this season, given stronger income growth and asset appreciation among high-earning households.

Interpreting the Disconnect

The Consumer Confidence Index remains a critical real-time gauge as official data flow stalls. While the survey has reliably led turning points in hiring and unemployment, its correlation with near-term spending has weakened. Elevated asset prices, pent-up savings among higher-income households, and the resilience of service spending continue to prop up consumption even as confidence drifts sideways. Moreover, expectations for future economic conditions have a stronger correlation with actual spending and remain historically low.

Consumers’ views of job availability continue to erode—often a leading signal for slower payroll growth

This divergence underscores that consumers are adapting, not retreating—trading down, delaying major purchases, yet still finding ways to meet everyday needs. Much of this resilience has been financed through rising credit card balances, a strategy that may prove short-lived as delinquency rates climb. For policymakers, the picture is mixed: inflation expectations remain stubbornly high, but overall spending has yet to crack, even as middle- and lower-income households scale back. For now, the labor market remains the key to watch. Most indicators—including consumers’ own perceptions of job availability—suggest that conditions are continuing to soften, a trend that will eventually weigh on spending. The Fed will weigh these crosscurrents carefully as it considers a possible December rate cut.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 28, 2025

Mark Vitner, Chief Economist

(704) 458-4000