Highlights of the Week

- The economy ended Q3 with modest but stable growth, though momentum has softened as hiring slows and confidence slips.

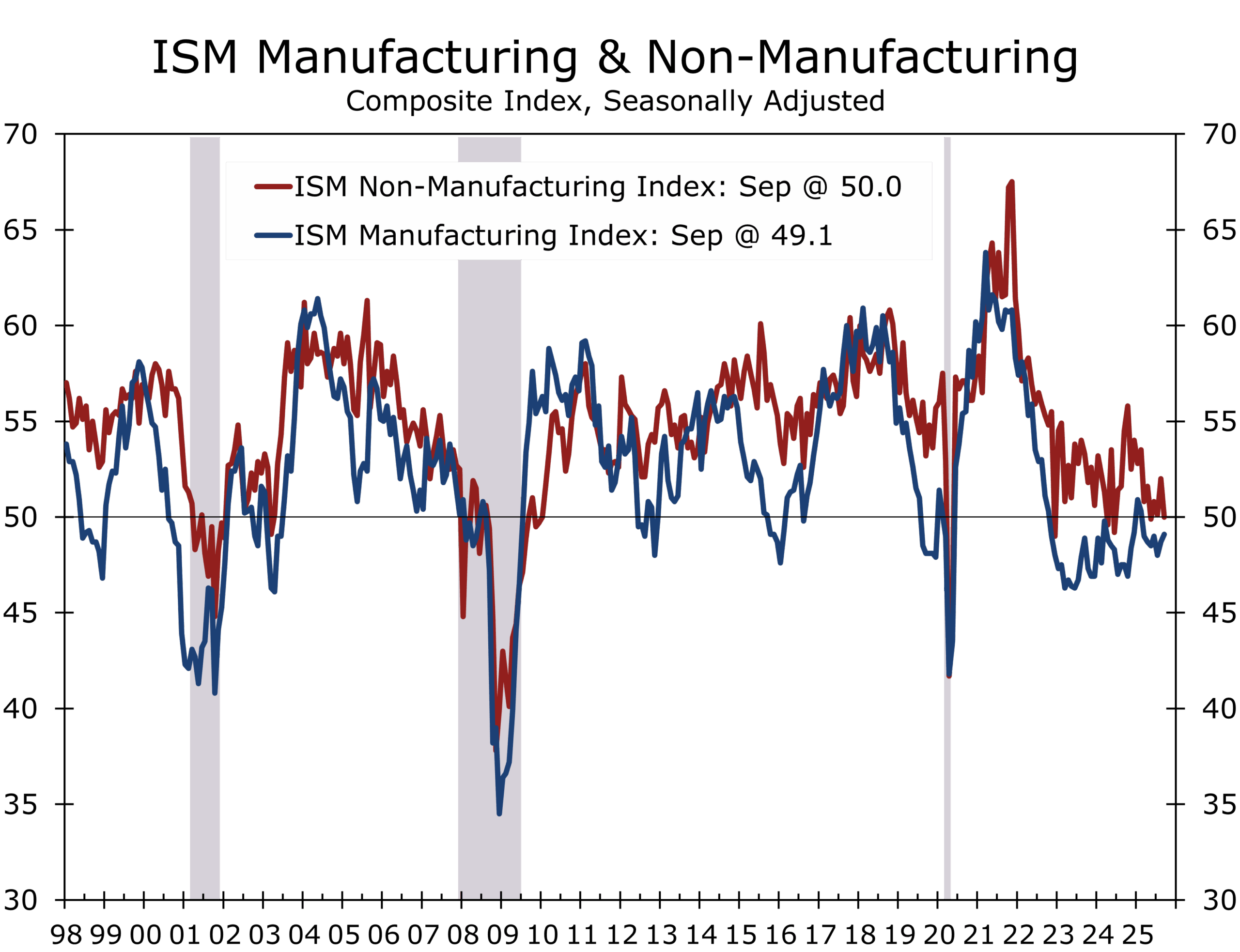

- ISM Manufacturing rose to 49.1 while ISM Nonmanufacturing fell sharply to 50.0 — both employment subindexes contracted, pointing to weaker labor demand.

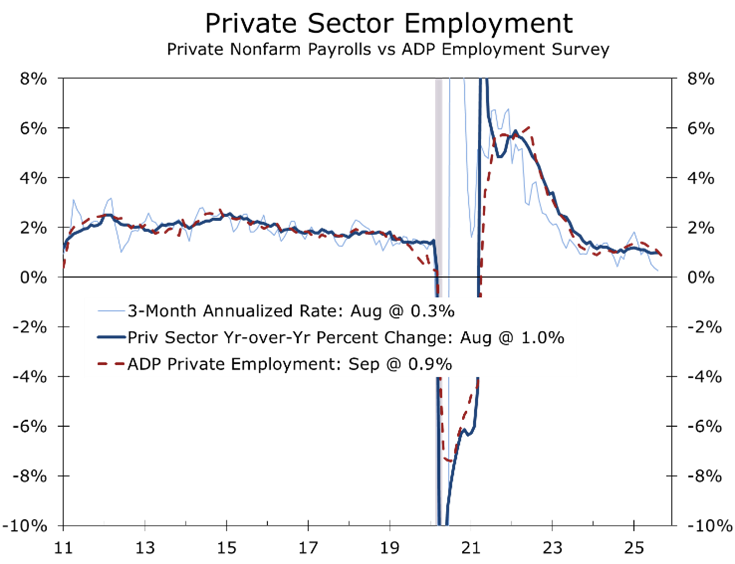

- The ADP report showed a 32,000-job decline, concentrated in small firms, and NFIB data confirm hiring plans remain strong but hard to execute amid skill mismatches.

- Private consumption finished Q3 on a high note as vehicle sales surged 2% before the expiration of EV tax credits; that strength will fade in Q4.

- The government shutdown has suspended key data releases, creating a “data fog” that may push the Fed toward an October rate cut, already priced into markets.

- Treasury yields declined 5–8 basis points as the curve steepened, equities gained, and investors stayed positioned for a soft-landing.

- Housing shows early signs of stabilization as mortgage rates approach 6%, while home price growth continues to cool without collapsing.

- Geopolitical tensions intensified with renewed ceasefire pressure on Israel, Moldova’s pro-EU election, Japan’s new conservative leadership, and protests across Europe supporting Hamas.

Macro Update: Private Data, Public Impasse

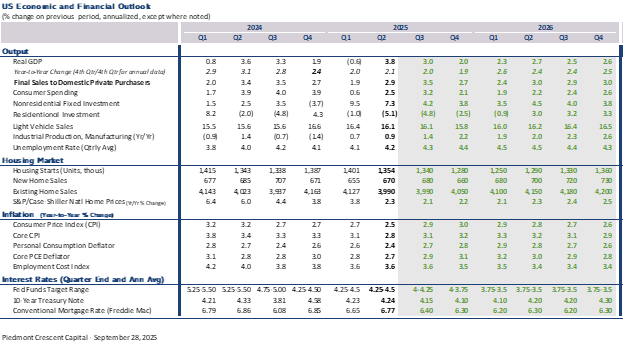

The early weeks of October find the economy balancing steady private-sector momentum against fiscal and geopolitical uncertainty. With the government shutdown delaying key official releases, investors have turned to private surveys, diffusion indexes, and real-time models as proxies. Together, these data suggest the economy remains resilient but is losing a little altitude, with hiring softening and confidence fraying at the margins. Our forecast now pegs Q3 growth at 3 %, reflecting the inertia of consumer spending and business investment even under constrained policy conditions.

Even amid gridlock, the private economy kept its footing, with Q3 growth likely near a 3% pace.

The September ISM manufacturing and services reports suggest the economy ended the third quarter with modest but stable forward motion. The manufacturing PMI edged up to 49.1 from 48.7 in August, alleviating some weakness while remaining in contraction territory but still well above levels typical of recession. New orders softened, inventories continued to shrink, input costs remained elevated, and employment showed tentative signs of stabilization.

On the services side, the ISM nonmanufacturing PMI fell to 50.0 from 52.0, the lowest reading since early 2023, indicating near-stagnation in service-sector output. The employment component weakened further to 47.2, confirming slower hiring momentum even as demand steadied.

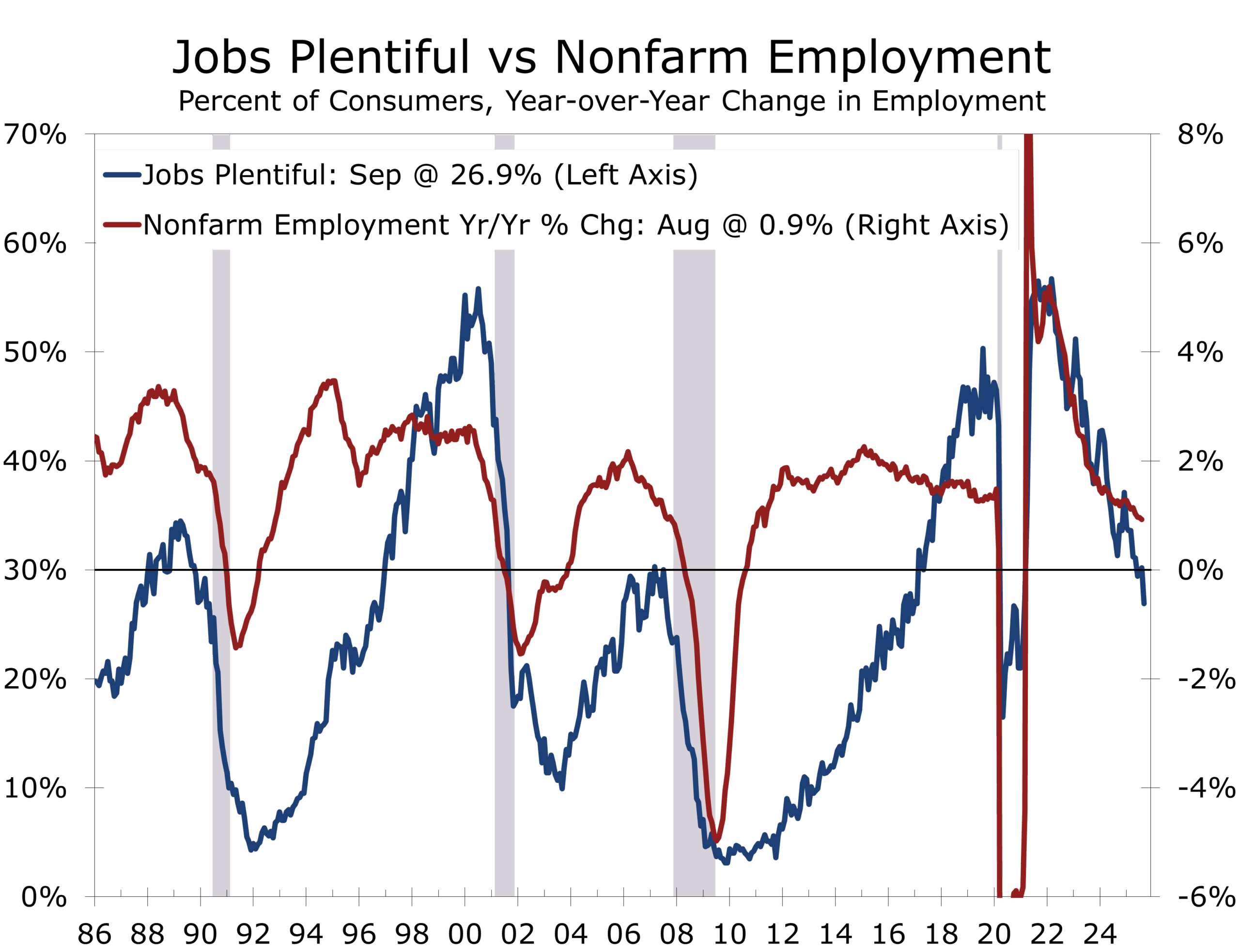

With the shutdown suspending the release of BLS employment and initial claims data, markets have leaned heavily on alternative signals. The Challenger report again showed hiring extremely slow and layoffs steady—an extension of the “low hiring, low firing” regime. The Chicago Fed’s real-time model estimates unemployment ticked up to 4.34 % from 4.32 %.

The ADP private payrolls release revealed a 32,000 decline, with significant downward revisions to past months, pointing to a weaker private employment trend. Regional Fed manufacturing surveys signaled mild job cuts across districts, and consumer surveys showed a rising share of respondents describing jobs as hard to get—a signal that labor demand is softening faster than supply. August JOLTS data also revealed continued loosening in cyclical industries, while Indeed job ads fell.

Adding further nuance, the NFIB small-business survey showed that net hiring plans rose to 16%, the highest since January, suggesting firms still intend to expand. Yet that intention exists amid constraints: 32% reported unfilled job openings, and, among those hiring, 50% said they had few or no qualified applicants. Labor quality remains the top constraint, while labor costs as a top operating concern edged up to 11 %. A net 31 % of firms said they raised compensation in September, and 19 % planned pay increases in the next quarter.

Data delays leave markets flying blind; private reports keep an October cut on the radar.

Taken together, these indicators point to a labor market that is cooling rather than collapsing. Market consensus remains that the Fed cut at each of the next three meetings, banking on further softening. Still, the risk asymmetry is clear: sharper-than-expected labor weakness could pressure earnings, while a resurgence in inflation would constrain policy flexibility. Our base case remains a soft landing, but we remain cognizant of both tail risks. We would prefer the Fed alternate meetings for rate cuts, which would extend the cycle. That looks unrealistic today, however.

The Atlanta Fed’s GDPNow model, prior to the shutdown, placed Q3 growth at 3.8%; private data since then have largely upheld that estimate. The rush to lock in EV incentives creates some upside risk to Q3 GDP. While a short-lived shutdown will likely have muted effects on Q4 growth, extended paralysis could erode confidence, disrupt capital spending, and slow government-driven flows—risks that would erode the momentum that private activity has carried thus far. We expect the shutdown to be resolved by mid-October. The House will be back in session on October 13 and military members need to be paid on the 15th.

.

Israel Under Pressure—and Shifting Global Currents

For nearly two years, Israel has fought the multi-front war that began with the October 7 attacks. Prime Minister Benjamin Netanyahu’s government expanded operations from Gaza to the northern frontier with Hezbollah while carrying out precision strikes across the West Bank and Syria. That strategy—focused on threat eradication—now faces increasing constraints: diplomatic pressure for a ceasefire, internal political fractures, and rising risk of regional escalation.

Following Israel’s strike on Hamas leadership in Qatar, the U.S. has quietly shifted toward diplomacy, working with Egypt, Qatar, and other intermediaries to explore phased ceasefire arrangements tied to the release of all hostages and security assurances. Iran continues to press via proxies in Lebanon, Iraq, and Yemen, as well as stoking resistance in Europe through intermediaries (both knowing and unknowing) complicating Israel’s margin for maneuver. U.S. military posture in the region has been adjusted to deter escalation, but domestic fiscal and institutional stress may limit strategic flexibility.

The region is tired or war and we expect the U.S.-brokered peace deal to take hold. The ever-elusive perfect peace deal will not get in the way of a very good settlement.

In Europe, Moldova’s pro-European Party of Action and Solidarity, led by Maia Sandu, secured a clear parliamentary majority, reinforcing a westward orientation and delivering a political setback to Kremlin influence. Moscow has already challenged the result, citing limitations in expatriate polling access, and may deploy disinformation or economic pressure tactics to destabilize the new government. The victory will force the new administration to balance reliance on EU leverage with the latent risks surrounding Transnistria, where Russian military presence endures.

In Asia, Japan’s Liberal Democratic Party elected Sanae Takaichi as leader, making her the country’s first woman to become prime minister. A long-time conservative figure and confidant of the Abe era, she signals a more assertive security posture and renewed emphasis on defense cooperation with the U.S. Economically, she favors fiscal stimulus over monetary tightening, likely delaying any aggressive BOJ normalization. Regionally, her style could revive disputes with China and Korea if nationalistic signals intensify, even as she seeks to consolidate power within the fractious LDP.

Across Europe, sustained protests in support of Hamas and against Israel’s Gaza campaign have mobilized hundreds of thousands in capitals from Rome to London, Berlin to Paris. In Italy, protests extended over several days, with parts of the movement targeting ports and arms shipments. In London, police made nearly 500 arrests during Palestine Action demonstrations. European governments are now confronted with the challenge of reconciling domestic pressure with their diplomatic commitments to Israel. At the same time, the protests energize fringe movements across the political spectrum, raising broader security and stability risks in a continent already grappling with inflation, energy stress, and slow growth.

Taken together, these dynamics underscore the fracturing of the post-war global consensus. Leadership transitions, social unrest, and cross-pressured alliances are accelerating realignments. The global economy may still be holding up, but the buffer zone in which policymakers can absorb shocks is narrowing fast—and missteps will carry greater consequences.

Looking Ahead

In the week ahead, markets will look for high-frequency proxies for labor market, consumer spending, economic activity and capital spending and, assuming the government reopens, the CPI and PPI prints. The consensus still leans toward cuts in October and December, and more likely January as well, but geopolitical volatility and legislative risks in Washington could derail that script. The economy is managing by momentum—for now—but the durability of that run rate is becoming more fragile. The real test in coming months will be whether markets and governance can absorb noise without breaking down.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 6, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000