Highlights of the Week

- The Fed continues to hold steady, but mounting political pressure—most notably from Trump’s critique of Powell as “too late”—is raising the stakes.

- FOMC minutes reveal a growing internal divide: while most members remain focused on tariff-driven inflation risks, a vocal minority warn that delaying cuts could jeopardize the recovery.

- NFIB Small Business Optimism edged lower in June, reflecting excess inventories, weak demand, and a growing reluctance to purchase new equipment or hire staff.

- Continuing claims climbed to a post-COVID high, signaling an increasingly stagnant labor market, with little hiring or firing.

- Real yields remain anchored near 2%, driving volatility and justifying a long-duration, defensive portfolio stance, while larger deficit projections and a weaker dollar make investors wary of being too exposed to the long end of the curve.

- The U.S. tariff regime is expanding, with a 50% tariff on copper and new tariffs proposed on Canada and Brazil.

- The latest barrage of tariffs follows a lull that allowed markets to rise back to record highs. Businesses and investors are likely to remain cautious this summer, as macro momentum remains soft, public and private valuations are rich, and the path to easing remains narrow.

Patience May be a Virtue but Often Comes at a Cost

The Federal Reserve’s cautious stance, reinforced by this week’s FOMC minutes, is increasingly at odds with an economy showing obvious signs of fatigue. While most Fed officials remain inclined to wait for more conclusive evidence that inflation is on a sustained path to 2%, labor market data looks softer beneath the surface, and renewed trade tensions suggest the window for a soft landing may be narrowing. President Trump’s critique of Jerome Powell—labeling him “too late”—may be political theater, but it underscores a growing concern: the longer the Fed waits, the greater the risk that it misses its opportunity to act.

The pressure on the Fed may make it tougher for Powell to cut rates earlier, even if he needs to.

Ironically, the pressure from President Trump may complicate the Fed’s ability to react. A rate cut in the near term could be perceived as a concession to political pressure—undermining the Fed’s independence, weakening the dollar, and unsettling bond markets. This political overhang makes it harder for policymakers to act decisively, even as economic momentum softens beneath the surface. We believe the July FOMC decision will be a closer call than the markets currently expect but still see the kickoff for the next round of rate cuts coming in September.

The June FOMC minutes confirmed that while a vocal minority supports earlier rate cuts, most committee members remain focused on the slow and uneven pass-through of tariffs into inflation. The stronger-than-expected June payrolls report provided cover to hold rates steady, but labor market fundamentals are clearly deteriorating. Hiring has slowed across most sectors, and job gains are increasingly concentrated in just a few industries. Alternative data—including the Bureau of Labor Statistics’ QCEW and ADP’s private payroll figures—suggest job growth has been overstated, with actual payroll gains running at least one-third below headline estimates over the past year.

Hiring has stalled, layoffs remain low, and the labor market is stuck in neutral.

High-frequency and survey data reinforce this softer assessment. Continuing unemployment claims have climbed to a post-pandemic high of 1.965 million, while initial claims have edged down to 227,000. This divergence points to a stagnant labor market marked by less hiring and less firing—a regime where laid-off workers, new entrants, and re-entrants struggle to find jobs as employers remain cautious amid soft demand and tariff uncertainty. The Conference Board’s Consumer Confidence Survey and the NFIB Small Business Optimism Index show that jobs are less plentiful and that hiring has slowed.

A stagnant labor market is not a healthy one. In a dynamic economy, workers leave jobs for better opportunities, and employers actively recruit to fill openings—supporting productivity, wage gains, and stronger growth. Today’s picture is more muted. Job growth has narrowed to pockets like healthcare, while cyclical industries are losing traction. Small businesses are at the center of the slowdown. The NFIB’s June survey showed optimism dipping to 98.6, driven by rising inventories, falling sales expectations, and weak hiring plans. Wage pressures are easing not because inflation expectations have normalized, but because labor demand is weakening.

The evolving tariff landscape adds another layer of complexity. This week, President Trump extended the July 9 tariff deadline to August 1 and proposed raising duties on 16 countries unless new deals are reached. While the new rates largely mirror those outlined in April and are unlikely to be fully implemented, they introduce a renewed layer of uncertainty into business planning—delaying capital expenditures, inventory restocking, and hiring decisions.

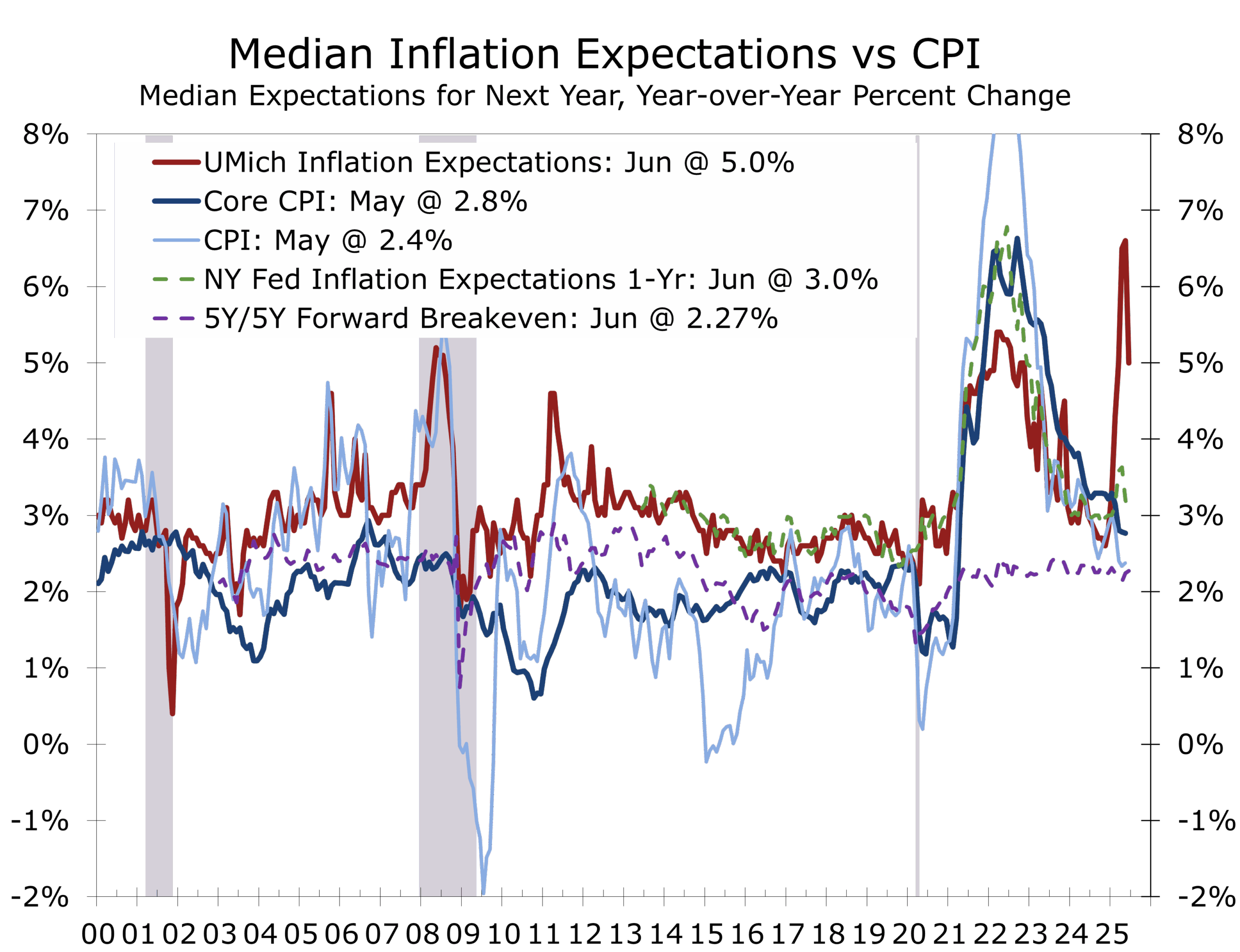

One lingering question is why this latest wave of tariffs has not shown up in consumer prices. The answer lies in delayed transmission, frontloading of imports, and absorption across the supply chain. Many of the goods hit by April’s tariffs did not arrive until May due to “on-the-water” exemptions. In addition, tariff payments can be deferred for up to six weeks, and many firms waited to raise prices until it became clear whether the tariffs would stick. Businesses also had some margin flexibility and ability to pressure suppliers, while consumers have shown strong resistance to price increases—especially with household budgets squeezed by housing, food, and transportation costs.

We estimate that roughly 35 percent of the current tariff burden has been absorbed by foreign producers, 40 percent by U.S. businesses, and just 25 percent by consumers. Alternative data and business surveys suggest the passthrough to consumer prices has been more limited than during the 2018–2019 tariff experience—likely due to more elastic supply chains and weaker household finances. If new tariffs take effect in August, consumer exposure may increase, but the broader inflationary impact remains constrained.

Our out-of-consensus view remains that fears of tariff-driven inflation are overstated. Roughly two-thirds of U.S. consumer spending is for services, which are unaffected by tariffs. Of the one-third spent on goods, only a portion is for imported goods. With consumer budgets already strained—particularly for households earning under $100,000—businesses are finding it difficult to pass on cost increases. In fact, the overall effect may prove disinflationary, as tariffs function more like a consumption tax and reduce spending for other goods and services. Soaring tariff revenues at the U.S. Treasury lend weight to that argument.

Despite rising risks, markets remain unusually calm—for now. Implied volatility across FX and fixed income has declined, anchored by steady inflation expectations and a lack of acute macro shocks. But realized volatility in equities and bonds continues to outpace implied levels, suggesting options markets may be underpricing near-term risks. With volatility risk premia compressed, investor complacency could set the stage for a sharp repricing—especially if trade tensions flare or policy credibility erodes. The month of August often brings big surprises.

Real yields near 2% signal a fragile equilibrium. The 10-year TIPS yield hovers near post-GFC highs, reflecting high nominal rates and subdued long-term inflation expectations. While that level aligns with estimates of trend growth, it also underscores growing fragility. Financialization, elevated leverage, and weak productivity have increased the economy’s sensitivity to shocks. As central banks transition from pandemic-era support to neutral or tighter policy, these real rates may begin to bite—tightening credit, curbing investment, and raising the odds of a hard landing.

Against that backdrop, a defensive stance remains prudent. Valuations are stretched, macro momentum is fading, and the outlook for a broad equity rally in the second half is weak—despite enthusiasm around AI and the emerging defense-tech buildout. July’s fiscal stimulus may offer support in 2026, but for now, a rebound in small business sentiment, capital spending, and hiring appears remote—particularly with a new round of tariffs in play.

The latest tariff announcements are puzzling in tone but fairly clear in intent: contain China, support strategic industries, and monetize access to the U.S. consumer market. Rhetoric aside, the message is simple—foreign firms will pay to play. The Trump administration is also taking a harder line on transshipping and fentanyl, where China remains the primary bad actor, but close allies—including Canada and Mexico—play supporting roles. While most fentanyl intercepted at the border enters via Mexico, Canada is a known source of key precursor chemicals. China has agreed to ban production of several precursors effective July 20, and the U.S. and Canada are scheduled to meet on July 21, with a potential agreement expected to follow.

The 35% tariff on Canadian goods announced July 10 would raise duties from 25% on targeted items such as non-USMCA-compliant lumber and dairy, while exempting compliant products—which account for 40% of bilateral trade—as well as steel, aluminum, autos, copper, and energy goods including oil and potash. These issues are also expected to be addressed during upcoming talks.

Asymmetric Pressure: Fentanyl and Rare Earths

The flurry of tariffs and trade deals reflects President Trump’s effort to boost federal revenues in exchange for access to the U.S. market, correct longstanding trade imbalances, support the reshoring of critical manufacturing, and counter China’s systematic exploitation of asymmetric vulnerabilities in the U.S. economy. Two recent developments illustrate the stakes: the rise of fentanyl as a tool of destabilization and the weaponization of rare earth supply chains.

China’s role in the fentanyl crisis aligns with its doctrine of “unrestricted warfare.” By enabling transnational criminal networks and shielding fentanyl producers behind state-controlled pharmaceutical infrastructure, the CCP has built an “unassailable base” for synthetic drug manufacturing. The result: over 100,000 annual U.S. overdose deaths, rising health costs, and hollowed-out communities—all while remaining below the threshold of conventional conflict.

China’s rare earth chokehold threatens U.S. military strength and industrial competitiveness.

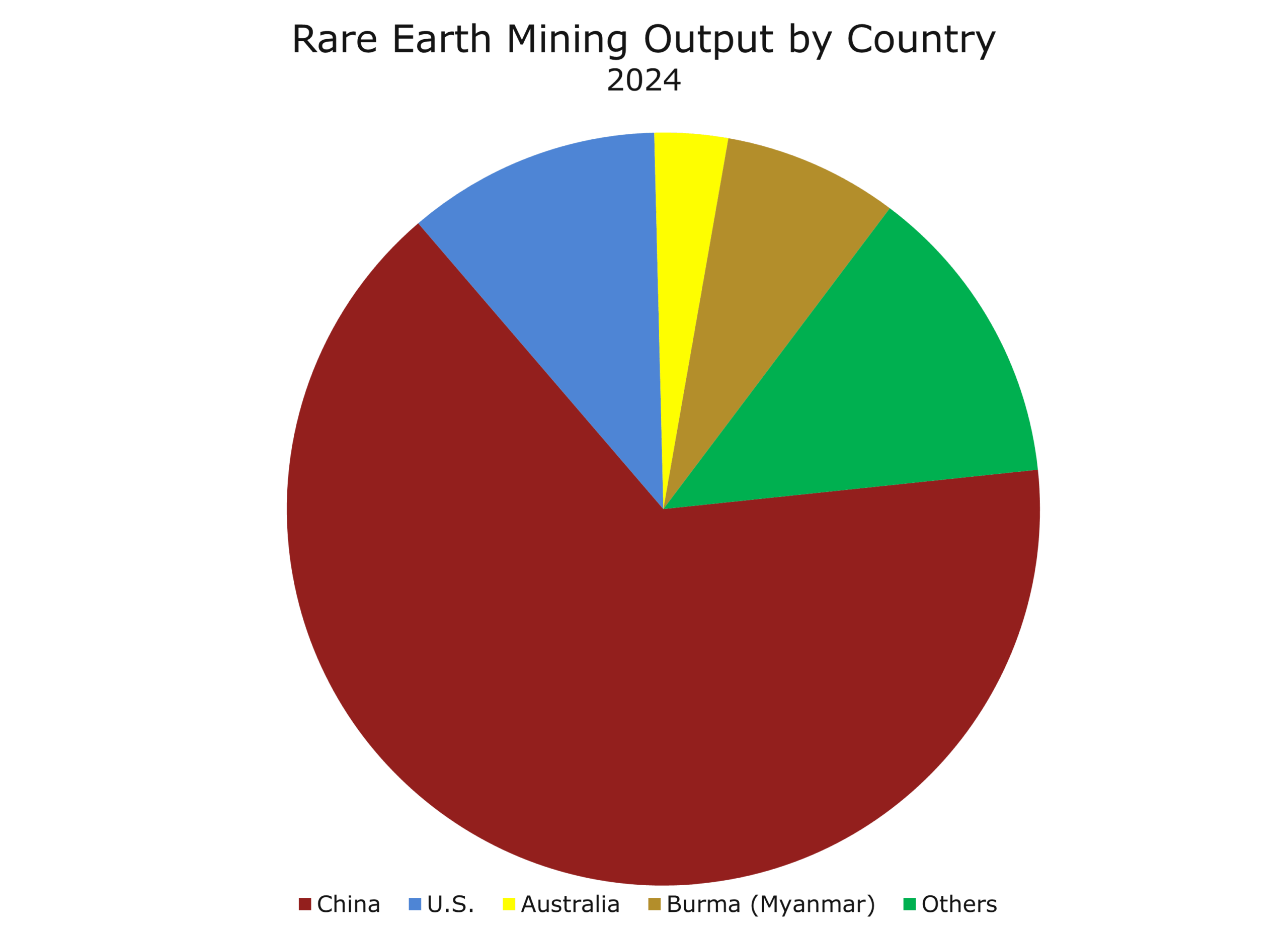

At the same time, China’s April 2025 decision to restrict exports of seven rare earth elements sent shockwaves through the U.S. defense and manufacturing sectors. China mines over 65% of the world’s rare earths and controls more than 85% of global refining capacity. By dominating nearly 90% of high-performance magnet production, China maintains a chokehold on critical supply chains for missiles, fighter jets, satellites, and electric vehicles. These latest restrictions follow earlier bans on gallium and germanium—materials essential to radar, infrared systems, and semiconductors. This is not merely economic leverage; it is a direct challenge to U.S. military readiness. A true Sputnik moment.

A $3 billion public-private partnership between the Pentagon and MP Materials marks progress toward magnet independence, but full production likely will not begin until 2027 or later. Without stronger incentives and binding agreements with allies, the U.S. remains dangerously exposed. Fentanyl and minerals are not separate challenges—they are part of a coordinated asymmetric strategy aimed at weakening U.S. power and resilience.[1]

Next week, senior U.S. officials will participate in a series of high-level talks across sub-Saharan Africa, including bilateral meetings in Kenya and mineral security discussions with Angola and South Africa. These meetings come at a pivotal time, as the U.S. seeks to counter China’s growing economic and strategic footprint on the continent and reinforce ties with nations critical to global supply chain resilience.

[1] Macdonald Amoah, Morgan Bazilian, and Jahara Matisek, Minerals, Magnets, and Military Capability: China’s Rare Earth Weaponization Should Be a Wake-Up Call, Modern Warfare Institute. July 10, 2025.

Inflation, Inventories, and the August 1 Tariff Clock

The week ahead will test whether the Fed can afford to continue sitting on the sidelines. The data slate includes June CPI and PPI, retail sales, industrial production, housing starts, and the Fed’s Beige Book—each offering critical insight into whether the balance of risks is weighted toward higher inflation or slumping economic growth.

We expect CPI to come in slightly below expectations, with the headline rising 0.3% but the core CPI rising just 0.2%. The recent slide in energy prices should slightly reverse in June. Food prices may also surprise to the upside, led by beef. Core goods prices continue to post modest increases, although we expect some snapback in airline fares and used car prices. Residential rent should moderate further. Producer prices are expected to match or slightly exceed the CPI—reinforcing our view that margins are absorbing much of the hit from higher tariffs.

Look for another flat industrial production reading, with most cyclical sectors down slightly and gains in defense, aerospace, and technology sectors. Retail sales are expected to rise a modest 0.3%, with weak auto sales offset by gains in building materials and restaurant spending. The control group should rise 0.4%. Inventory accumulation remains soft.

And then there’s trade. Unless negotiations succeed by August 1, U.S. tariff rates will rise across a wide range of imports. We expect to see a few more deals signed, but countries are increasingly concerned that early concessions will only invite greater demands later. We see the tariff endgame as a 10% universal rate, paired with elevated duties on goods originating in China—regardless of final assembly location. Higher rates will likely apply even to trade with Canada and Mexico.

The Fed’s Beige Book will be watched for anecdotal insights on hiring, pricing (tariff pass-through?), and investment sentiment—qualitative signals that may shape the tone of the July and September FOMC meetings, especially given ongoing data volatility, low confidence, and still high inflation expectations.

Looking Ahead: Week of July 14–18

- CPI (Tuesday, July 15): Headline (+0.3%, 2.7% yr/yr). Core (+0.2%, 2.9% yr/yr).

- PPI (Wednesday, July 16): PPI Final Demand (+0.2%). Core PPI (+0.2%).

- Industrial Production (Wednesday, July 16): Overall (+0.2%), Manufacturing (0.1%). Gains in aerospace offset minor declines elsewhere.

- Retail Sales (Thursday, July 17): Overall retail sales (+0.1%). Ex-Autos (+0.3%). Core (+0.4%).

- Import Prices, Initial Claims and Business Inventories (Thursday, July 18): The torrent of data will lead to some final tweaks in Q2 GDP forecasts. We are currently at 2.9%.

- Housing Starts (Friday, July 18): Look for a slight rebound following last month’s 9.8% plunge. Overall Starts (+2.5%). Building Permits (-2.0%).

Final Thought: Timing is Everything

The Fed’s patience is understandable, but the risks of delay are growing. A stagnant labor market, weak small business sentiment, and tariff-driven uncertainty are tightening the noose around the recovery. The central bank still has time—but not much. In a cycle increasingly defined by policy lag and global volatility, timing is not just everything—it is the only thing.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 13, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000