Manufacturing Shows Tentative Signs of Stability

- The ISM Manufacturing PMI slipped 0.2 points to 48.5 in May, its third straight sub-50 reading, though underlying data showed signs of resilience.

- New orders rose 0.4 points to 47.6—the most forward-looking component of the survey—suggesting early signs of a demand rebound.

- Production ticked up 1.4 points to 45.4, still in contraction but supported by easing backlogs and improving inventory alignment.

- The employment index edged up to 46.8, reflecting fewer layoffs, though hiring remains restrained.

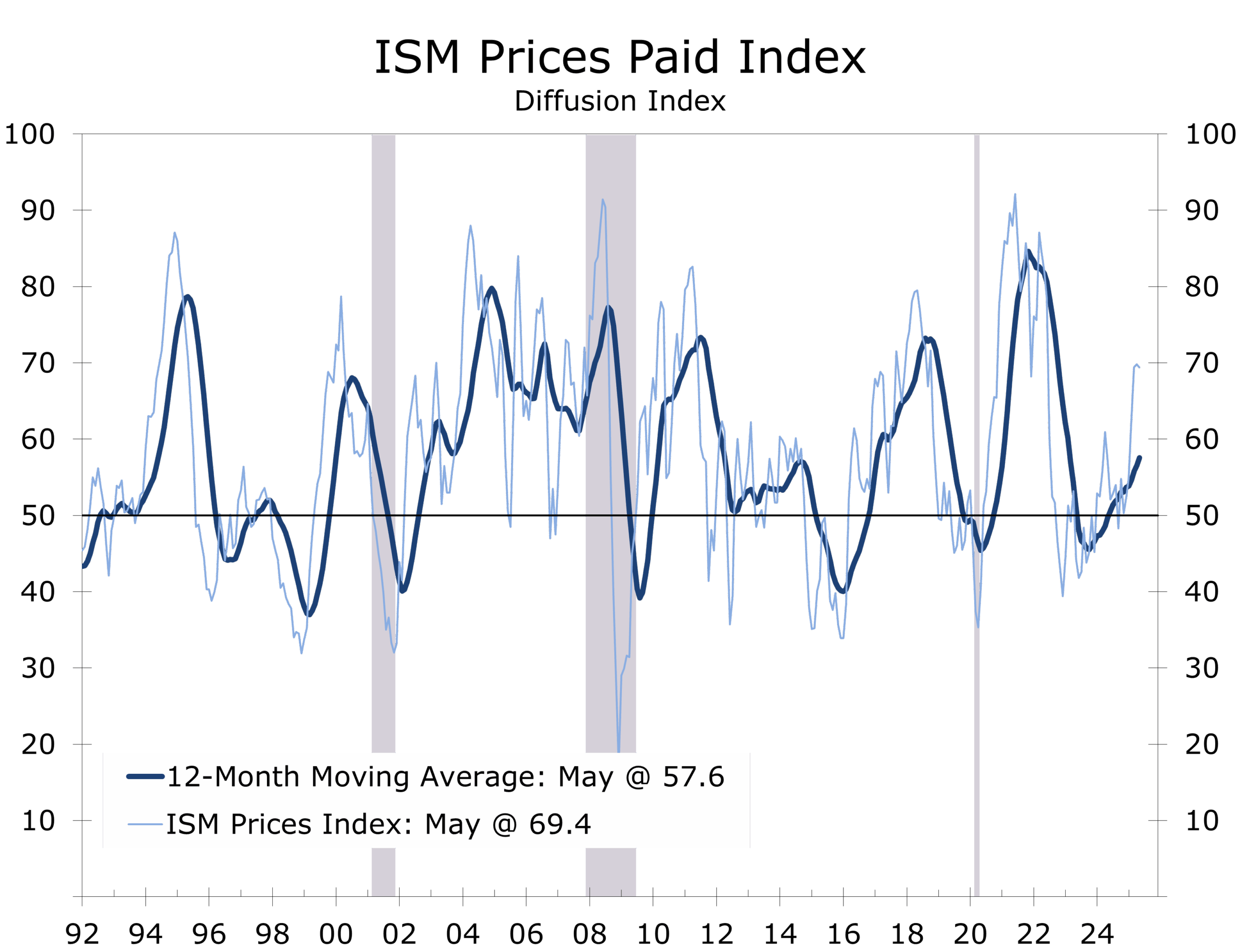

- Prices paid dipped slightly to 69.4 but remain elevated, as tariff pass-throughs continue to compress margins.

- Backlogs rose 3.4 points to 47.1, their highest since January, signaling tentative supply chain normalization and more stable factory schedules.

- Trade turmoil remains a major challenge for supply chain managers, who must navigate inbound material sourcing and outbound logistics amid heightened uncertainty. The fact that the headline index has held near 50 is encouraging and suggest that the recent turmoil has not been enough to derail growth.

While the ISM Manufacturing PMI edged down 0.2 points to 48.5 in May—its third consecutive sub-50 reading—the report offered several signs of underlying resilience. After a brief winter rebound, manufacturing remains in contraction, but forward-looking components suggest the sector may be approaching a turning point.

The New Orders Index rose 0.4 points to 47.6, offering a tentative sign that demand may be stabilizing. Several respondents cautioned that overseas orders remain weak, contributing to ongoing customer hesitation. While buyers are still wary amid pricing volatility and policy uncertainty, the modest improvement in the survey’s most forward-looking component is a welcome development.

The ISM Manufacturing Index remains near 50, highlighting the factory sector’s resilience.

Production rose 1.4 points to 45.4, remaining below the key 50 breakeven threshold, which signals more manufacturers cutting output than increasing it. Firms cited improving customer inventories and selective strength in machinery and electronics, though food processing and transportation continue to lag.

The employment index edged up to 46.8—its second straight gain—suggesting the pace of layoffs is moderating, even as overall hiring remains cautious

Headcount reductions are ongoing but more targeted—some firms are relying on attrition and hiring freezes rather than outright cuts. This aligns with broader labor data showing a plateau in manufacturing payrolls through mid-Q2. Many manufacturers remain chronically short of workers, however, so even the extended lull in activity may not leave them overstaffed.

Input costs remain stubbornly high, with the Prices Paid Index falling just 0.4 points to a still elevated 69.4. The marginal decline reflects slight relief in diesel and natural gas prices, but tariffs continue to complicate cost planning. The index has risen 19.1 points over the past six months. Respondents were explicit: most suppliers are passing through the full burden of tariffs, treating them as taxes.

Most suppliers are passing through the full burden of tariffs, treating them as a tax hike.

Trade remains the weakest link. New export orders plunged to 40.1—the lowest reading outside of COVID since the Great Recession. Imports also cratered, falling to 39.9 amid softer domestic demand and intensifying tariff friction. Multiple panelists described the latest tariff rollouts as more disruptive than COVID, citing shipment delays, canceled orders, and rising customer skepticism around forward pricing.

Inventories contracted sharply, with the index falling 4.1 points to 46.7. The pull-forward strategy that dominated earlier in the year appears to have run its course. Companies are now focused on reducing exposure to policy risk and fortifying balance sheets.

Customer inventories are relatively low, which could drive orders higher in coming months.

The Customers’ Inventories Index fell 1.7 points to 44.5 in May, indicating inventories at the customer level remain too low. While not a direct measure of output, this continued drawdown is typically viewed as a positive signal for future production. Survey respondents noted that products are understocked among customers, suggesting restocking could provide a modest lift to demand in the months ahead.

While the PMI remains in contraction, the broader takeaway from the May report is that recent tariff turmoil is not enough to derail economic growth. At 48.5, the index is consistent with modest GDP expansion—likely near 2%. The underlying details were also constructive: four of the five subcomponents used to calculate the headline PMI improved, including new orders, the most forward-looking of the survey

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.