Modestly Better but Still Soft

- The ISM Manufacturing Index rose by 1.9 points to 48.4% but remained below the key 50 breakeven level, signaling contraction, for the 8th consecutive month.

- Manufacturing has been a persistent soft spot in what on appears to otherwise be a strong economy. The Manufacturing PMI® has been in contraction for 24 of the past 25 months.

- The overall PMI® has remained near its recent level for the past two years, consistent with a soft landing. The PMI® would need to fall below 42.5 to consistent with a recession.

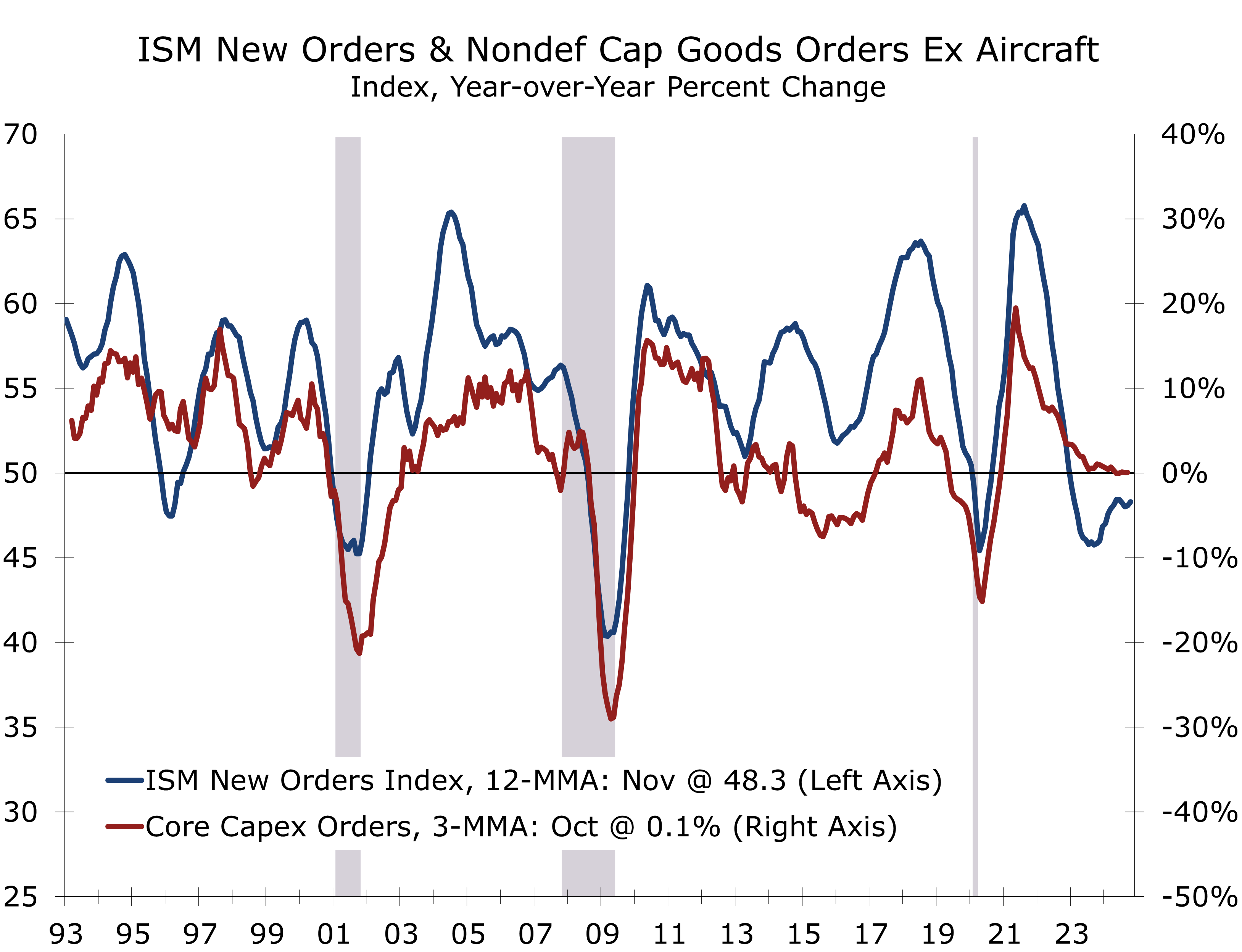

- The underlying details remain consistent with a soft landing, with new orders rising 3.3 points to 50.4, production climbing 0.6 to 46.8, and employment increasing 3.7 to 48.1.

- Supply chains also continue to normalize, with the suppliers’ delivery index declining 3.3 to 48.7, and the average lead time for production materials falling 2 days to 79 days.

- Persistent weakness in the factory sector has been a key reason for the Federal Reserve’s eagerness to cut interest rates, despite an otherwise healthy economy. While manufacturing represents a smaller share of overall output, it continues to drive much of the cyclical swing in GDP growth, signaling slower growth in coming quarters.

The ISM Manufacturing PMI® rose 1.9 percentage points to 48.4 in November, which topped expectations but remains well into contraction territory. The increase brought the index to its highest level since June, signaling some near-term stability.

The underlying details in the report were modestly positive. The New Orders component rose by 3.3 points to 50.4, while the Production and Employment indices also edged higher, increasing by 0.6 points and 3.7 points, respectively. However, both indices remain in contraction, with Production at 46.8 and Employment at 48.1, respectively.

Despite averaging 3.0% GDP growth over the past two years, manufacturing remains soft.

The ISM index and its subcomponents provide insight into the breadth of the manufacturing sector’s strength or weakness. The Pandemic distorted the index to a certain degree in that widespread shortages drove the supplier delivery index sharply higher and exaggerated the extent of improvement when the economy reopened. Part of the recent weakness may be a payback for this earlier strength. The PMI® has averaged 47.6 over the past 2 years, a level that would be consistent with just 1.5 percent real GDP growth, half of what BEA has reported for this period.

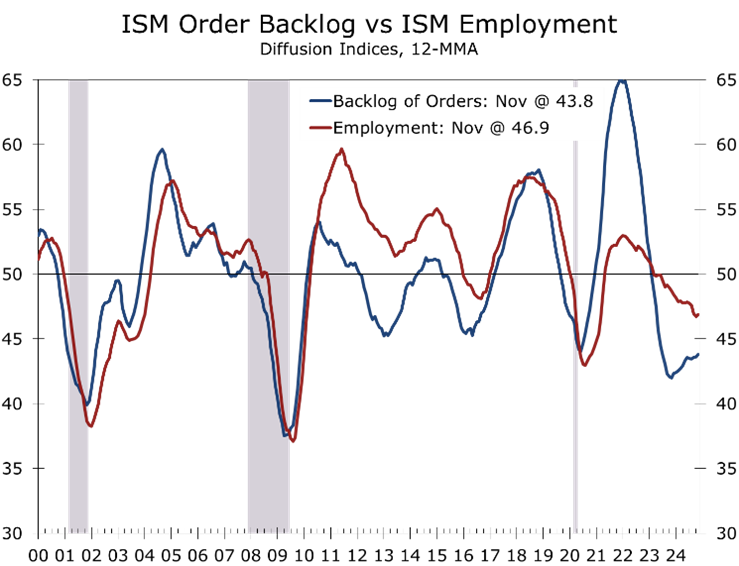

While several key components showed improvement, overall activity is expected to remain soft. Uncertainty has likely risen in the aftermath of the presidential election, with ongoing questions about taxes, tariffs, and regulations. Additionally, diminishing order backlogs—a typical precursor to hiring slowdowns—signal potential challenges ahead.

Manufacturers of building materials appear headed for a slowdown, particularly those tied to commercial construction. The construction backlog has thinned considerably, with fewer new projects starting and the previously record-high backlog of projects beginning to decline. This trend has notably impacted producers of wood products and fabricated metals.

The slowing pace of construction will likely weigh on factory output in the coming months.

Demand for big-ticket consumer goods, including motor vehicles and furniture, remains soft and is unlikely to recover meaningfully until job and income growth reaccelerate.

There are a few bright spots. Orders for capital equipment in the IT sector remain robust, driven by the ongoing impact of the CHIPS Act. Additionally, orders for industrial machinery have shown improvement. However, just five of the 15 sectors reported net growth during November, indicating that factory output will remain in low gear the next few months.

Manufacturing employment figures have been impacted by strikes in recent months and may see some near-term improvement. However, today’s ISM report indicates that any gains are likely to be short-lived. Manufacturers continue to grapple with elevated operating costs and heightened uncertainty, compounded by a consumer shift toward spending on services and experiences.

The manufacturing sector still provides the cyclical impulse to the broader economy.

The Prices Paid Index fell 4.5 points to 50.3 but has remained above 50 for the past two months, indicating that more manufacturers are reporting higher input costs. Aluminum, copper, and natural gas saw slight price increases, while prices for steel, plastic resins, and crude oil declined.

The Fed closely monitors manufacturing data and has historically relied heavily on the ISM surveys. The latest figures provide some reassurance that the economy continues to lose momentum, despite a resurgent stock market and strong GDP figures. We remain skeptical that economic growth will reaccelerate without better results from the ISM report.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.