Looking Ahead to 2025

- We have had a couple of weeks to adjust to the impact of the 2024 presidential election. As we expected, Trump won with a resounding electoral college majority and the republicans won control of the Senate and narrowly retained control of the House. We expect swift action with policies regarding border security, regulatory relief, extending the Trump tax cuts, land use, trade negotiations, and tariffs. The financial markets have priced in more persistent large budget deficits and modestly higher inflation, which is partly reflected in our own forecast.

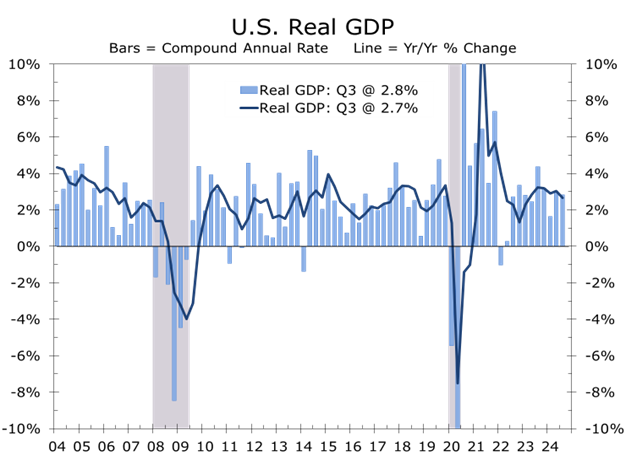

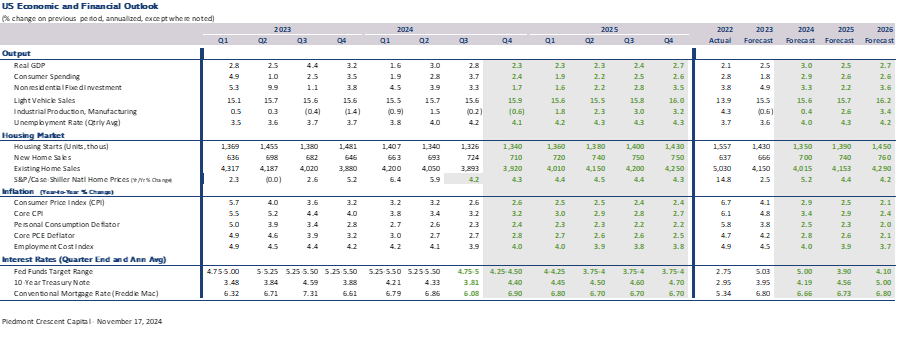

- The economy remains remarkably resilient, with revised real GDP growing at an annualized rate of 2.8% in the third quarter and 2.7% year-over-year. The economy has maintained a growth rate of approximately 3.0% in 7 of the past 8 quarters, marking a remarkable run. Despite this stronger headline growth, consumer sentiment has been uneasy throughout much of this period, casting doubt on the veracity of the GDP data.

- This divergence between robust GDP growth and uneasy consumers highlights the waning but notable impact of fiscal stimulus on capital spending, offset by frustration over high prices for essentials. Both business investment and consumer spending are expected to moderate in the coming quarters, as uncertainty surrounding the new administration delays capital spending. Fourth-quarter growth is projected at 2.3%, with solid consumer spending through the holidays.

- Inflation has eased this past year, providing some relief to household budgets. Further progress may prove challenging, however, as wages and core service prices are easing much more slowly. While concerns about tariffs, trade wars, and stricter immigration policies are fueling inflation fears, we believe these concerns are overstated and expect only a modest impact on inflation.

- The outcome of the U.S. presidential election will refocus attention on global hotspots, particularly Ukraine and the Middle East. The Trump Administration is likely to pursue a Ukraine peace deal with stronger guarantees than currently anticipated, while Iran may seek an exit from the conflict it initiated. The key question in both scenarios is whether any agreement is worthwhile if it merely postpones the conflict, giving Russia and Iran time to regain leverage.

The 2024 Presidential Election outcome will drive significant policy shifts in the coming year. The incoming Trump Administration aims to quickly appoint cabinet members focused on streamlining government, reducing regulation, expanding federal land use for energy and other resources, cutting taxes, reforming trade and immigration, and implementing tariffs. On foreign policy, Trump has pledged to quickly end Russia’s war in Ukraine and Iran’s conflict with Israel, as well as redouble efforts to expand the Abraham Accords. While new administrations often enter with ambitious plans, the first 100 days are critical and typically set the tone. Narrow congressional majorities mean the speed of cabinet confirmations will heavily influence the Administration’s success.

Trump’s initial cabinet choices, including Matt Gaetz for Attorney General, Robert F. Kennedy Jr. for Health and Human Services Secretary, and Pete Hegseth for Defense Secretary, have sparked controversy among mainstream political insiders. However, these selections are highly popular with Trump’s base and appear intended to maintain their support during the administration’s early months. While it remains uncertain whether the Senate will confirm all these controversial picks, Trump’s cabinet is expected to align closely with his populist agenda. Notably, he has yet to announce a Treasury Secretary, though the shortlist includes several credible candidates, and he has been relatively quiet about the Federal Reserve.

On foreign affairs, we do not expect Trump to end Russia’s war with Ukraine immediately upon taking office. Both Russia and Ukraine are likely to escalate their efforts before January 20 to strengthen their bargaining positions. For Russia, this likely involves attempting to push Ukrainian forces out of occupied areas near Kursk, bolstered by additional manpower from North Korean troops, and intensifying missile strikes on Kyiv. For Ukraine, the strategy will focus on holding these territories and inflicting significant casualties on Russian forces and military infrastructure. These actions would bolster Ukraine’s negotiating position should Putin accept Trump’s mediation offer. The Ukraine War has vastly exceeded Russia’s expectations in terms of lives lost, costs incurred, and its overall duration.

In the Middle East, Israel is expected to continue operations against Hamas, Hezbollah, and Iran. While there are signs that Iran may ask Hezbollah to pull back along the lines proposed by Israel, Hamas and the Houthis remain far apart with Israel on terms of a possible cease fire. The Biden administration may push for a settlement before Trump takes office, but Israel is likely to remain cautious, preferring guarantees Trump could more credibly provide for enforcing and maintaining a ceasefire.

Domestically, Trump is likely to prioritize swift implementation of his agenda during his first two years, as GOP control of the House may be difficult to maintain in the mid-term elections, and the next presidential race looms shortly thereafter. Reducing regulation, which was more impactful than tax reform during Trump’s first term, is an area where quick action is likely. We also expect the Trump tax cuts to be extended and anticipate Trump using tariff threats to secure stronger trade deals. While tariffs are unlikely to significantly impact inflation, an escalating trade war may lead to renewed supply shortages..

The incoming Trump Administration inherits an economy that, on the surface, appears firm but is significantly softer in the middle. The forces propelling economic growth have been narrowing, with health care and government accounting for a disproportionate share of job growth. Overall GDP growth has been bolstered by unprecedent fiscal stimulus, which has bolstered business fixed investment in EV-related and Chip-related ventures and boosted state and local government outlays. Growth in other areas of the economy has cooled and the pipeline of incentive-driven projects is winding down.

How much of the current slowdown is reflected in the data remains uncertain. Key indicators, such as employment figures, have been distorted by several significant exogenous events, including Hurricanes Helene and Milton, strikes at Boeing and East Coast ports, and the usual pullback in capital spending and hiring that precedes presidential elections. The Bureau of Labor Statistics (BLS) has already disclosed that nonfarm payrolls will see a substantial downward revision when the annual updates are released with the January payroll data. Preliminary figures indicate employers added 818,000 fewer jobs from March 2023 to March 2024 than initially reported, even before the recent hiring slowdown became apparent.

After adding just 12,000 jobs in October, we anticipate a partial rebound in November as workers return from temporary strikes and disruptions caused by back-to-back October hurricanes. However, recovery from Hurricane Helene is expected to be unusually slow due to extensive flood damage, which typically requires more time to repair, and delays in relief efforts reaching rural areas. These recovery efforts are likely to boost construction payrolls as cleanup crews are mobilized. Conversely, the leisure and hospitality sectors, along with retail trade, may experience a more gradual recovery. Additionally, this year’s late Thanksgiving could shift holiday-related hiring into December, potentially resulting in another weak month for November data.

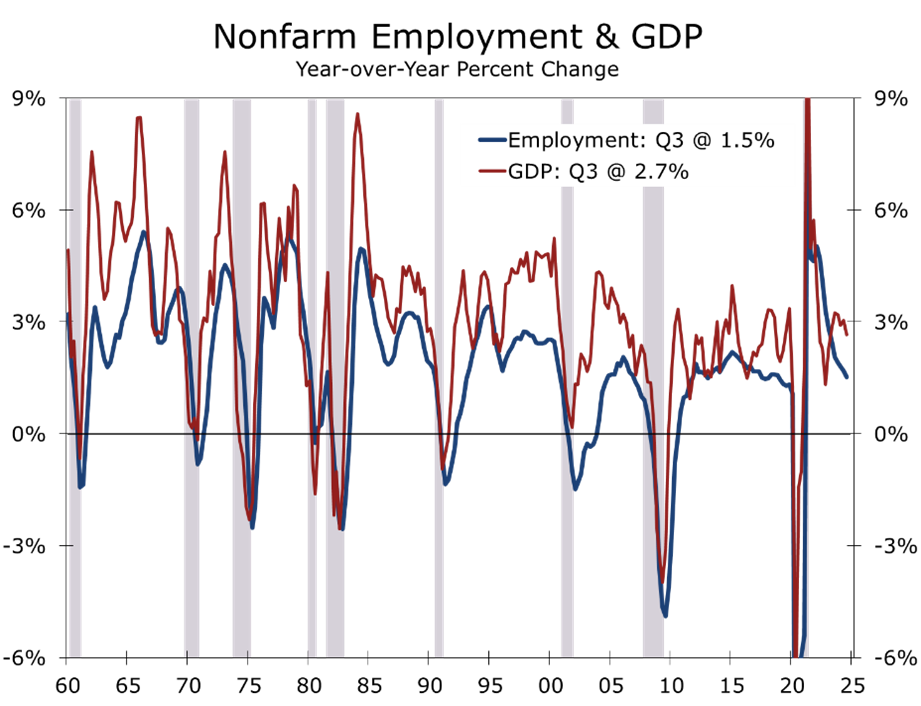

This past year’s slowdown in job growth is not fully reflected in the GDP data. Real GDP grew by 2.7% over the past year, compared to 3.2% in the previous year, while job growth slowed to 1.5% from 2.1% a year earlier. The implication is that productivity growth and the economy’s potential growth rate are somewhat stronger than previously estimated. As a result, inflation should continue to decelerate, albeit at a much slower pace than seen over the past two years.

.

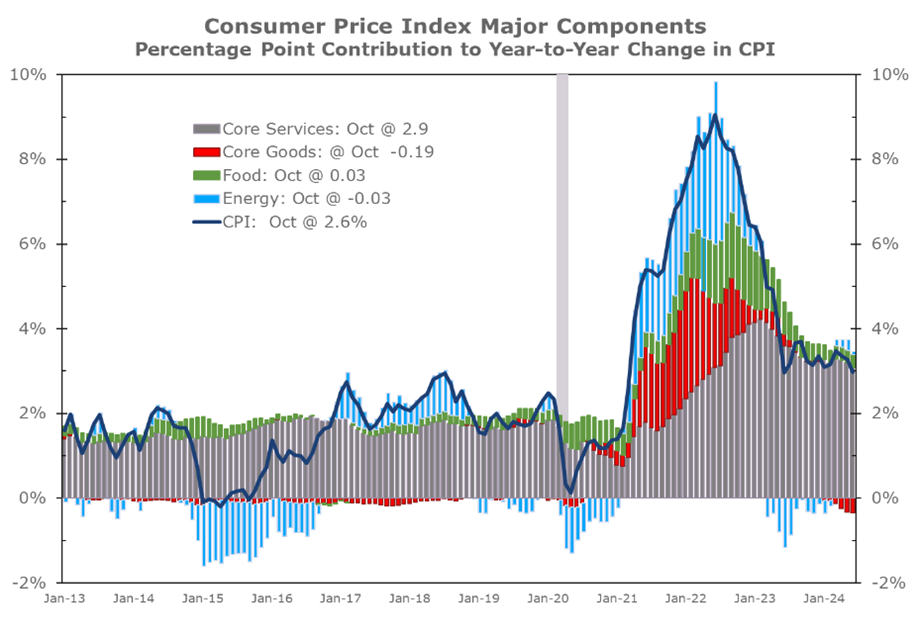

The path back to the Fed’s 2% inflation target appears increasingly challenging, as recent reports highlight persistent price increases in key areas of the economy, particularly in the service sector, where labor costs heavily influence pricing. The easiest phase of disinflation now appears to be behind us, with energy prices declining and food prices largely stabilizing. Core goods prices have also fallen, driven by slower global economic growth—particularly in China—which has led to a surge in exports to the U.S., exerting downward pressure on final core goods prices.

The relief from inflation has been insufficient for many consumers, as voters cited higher grocery bills and housing costs as key factors for choosing Trump over Kamala Harris. Overall, prices are roughly 20% higher than when the Biden-Harris administration took office, with grocery store prices and residential rents both up by 26%. Inflation expectations have risen since the election, driven in part by recent firmer inflation data and concerns over potential tariffs and large-scale deportations

We believe concerns about tariffs are overstated. While Trump has announced plans for significant tariff increases—proposing a 10% across-the-board tariff and a 60% tariff on Chinese imports—we view these proposals as largely a negotiating tactic. We anticipate tariffs, currently averaging around 3%, to rise modestly to approximately 6%, with Chinese goods facing somewhat steeper increases. One key objective is to curtail transshipments of steel, light vehicles, and other goods through free-trade partners. This practice circumvents tariffs by routing shipments of high-value-added products from China though Mexico or Canada or other nations under U.S. free trade agreements, where some light assembly or processing is completed.

The link between tariffs and consumer prices is less direct than commonly assumed. Tariffs are applied to the customs value of imports, but the landed cost—what wholesalers and distributors pay—includes tariffs, transportation, and insurance costs. Landed costs account for only a fraction of final retail prices: roughly one-third for furniture and clothing, and as little as 10% for high-end luxury goods such as jewelry and perfume. To mitigate tariff impacts, importers can ship less-assembled goods and complete assembly in the U.S., a long-standing practice for products like light trucks and furniture.

We estimate tariffs will ultimately add about 0.3 percentage points to the Consumer Price Index (CPI), modestly extending the path back to the Fed’s 2% inflation target. The primary risk lies in the potential for a broader trade war, which could lead to shortages of key inputs in the U.S. and dampen global economic growth.

.

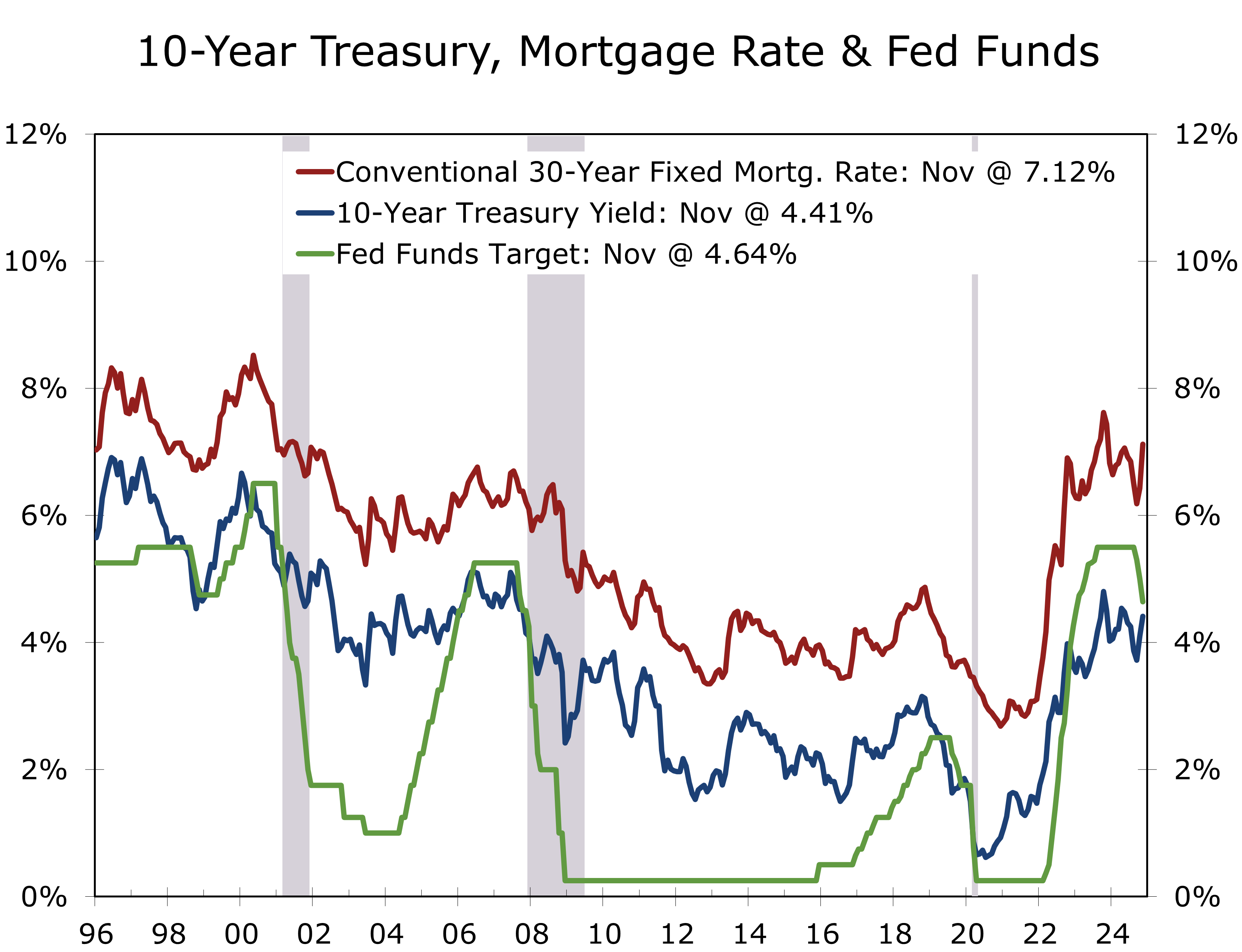

Bond yields have risen sharply in the weeks leading up to and following the presidential election, driven by a few disappointing inflation reports, a less optimistic inflation outlook in general, expectations for fewer Federal Reserve rate cuts, and growing concerns about persistent large federal budget deficits. We now anticipate the Fed will cut the federal funds rate by a quarter percentage point just three more times, with reductions at successive FOMC meetings in December and January, followed by a pause in March and another cut in May. The yield on the 10-Year Treasury Note has climbed from 3.80% in late September to around 4.40%, while the 2-Year Note has risen to 4.29%, aligning with this outlook.

Inflation concerns and worries about larger budget deficits are not the only drivers of rising interest rates. Annual benchmark revisions revealed stronger-than-expected economic growth, particularly in Gross National Income, which saw significant upward adjustments in real after-tax income and corporate profits. Stronger income growth means the economy is more resilient to outside shocks and rising interest rates. Strong growth also reflects stronger productivity growth which supports the argument that potential GDP growth and the neutral federal funds rate are higher than the Fed’s long-term estimates in its Summary of Economic Projections. Productivity growth has averaged 1.9% over the past five years, compared to 1.3% in the five preceding years. Coupled with 0.6% labor force growth, potential real GDP growth now stands at approximately 2.5%.

We estimate the neutral federal funds rate to be between 3.50% and 4%. Consequently, we expect the Fed to pause once the federal funds rate reaches the 3.75%-4% range. Lower short-term rates should steepen the yield curve, boosting banks’ interest rate margins and encouraging more lending. While mortgage rates are tied to the 10-Year Treasury yield, the spread between the two has been unusually wide due to elevated funding costs for lenders. As funding costs decline, we anticipate lenders will adopt more aggressive pricing, gradually narrowing the spread between 30-Year mortgage rates and the 10-Year Treasury yield toward its long-run average of 170 basis points. As a result, mortgage rates could fall from current levels even if the 10-Year Treasury yield rises further. Similarly, lower funding costs should enable banks to price auto loans more competitively, which we feel will become apparent this spring.

We have raised our Q4 real GDP growth estimate to 2.3%, reflecting stronger core retail sales and continued support from business fixed investment. Holiday retail sales should see solid gains, though the unusually late Thanksgiving may shift more activity into December. We have also increased our growth estimate for the first half of 2025, as businesses are likely to accelerate exports and imports ahead of a potential tariff hike. While inventory building should boost growth early in the year, homebuilding and consumer durable goods purchases are expected to drive growth in the second half.

The policy mix is expected to become more favorable, with an extension of the Trump tax cuts and modest expansions to current law, including partial relief on the cap for state and local tax deductions and tax breaks on tip income. Regulatory relief and land-use reform are poised to provide an immediate supply-side boost, enabling faster growth without increasing inflation. Risks remain from tariffs and potential deportations, though administrative solutions allowing working immigrants to remain could mitigate disruption.

Internationally, the Trump Administration has an opportunity to reset relations strained by Russia’s invasion of Ukraine and Hamas’s attack on Israel. Geopolitical maneuvering is likely as all parties jockey for position ahead of U.S. leadership changes. A preliminary peace outline for Russia and Ukraine has been circulating by will likely require stronger guarantees for Ukraine, such as limited EU and NATO observer status. In the Middle East, while lasting peace remains elusive, a ceasefire returning hostages and advancing the Abraham Accords offers the best path to stability and hope for the region.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice. Any forward-looking statements or forecasts are not guaranteed and are subject to change at any time. Information from external sources have not been verified but are generally considered reliable.

© 2024 CAVU Securities, LLC

November 21, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000