Hurricanes Held Back Starts in the South

- Housing starts came in slightly short of expectations in October, falling 3.1% to a 1.311-million-unit annual rate.

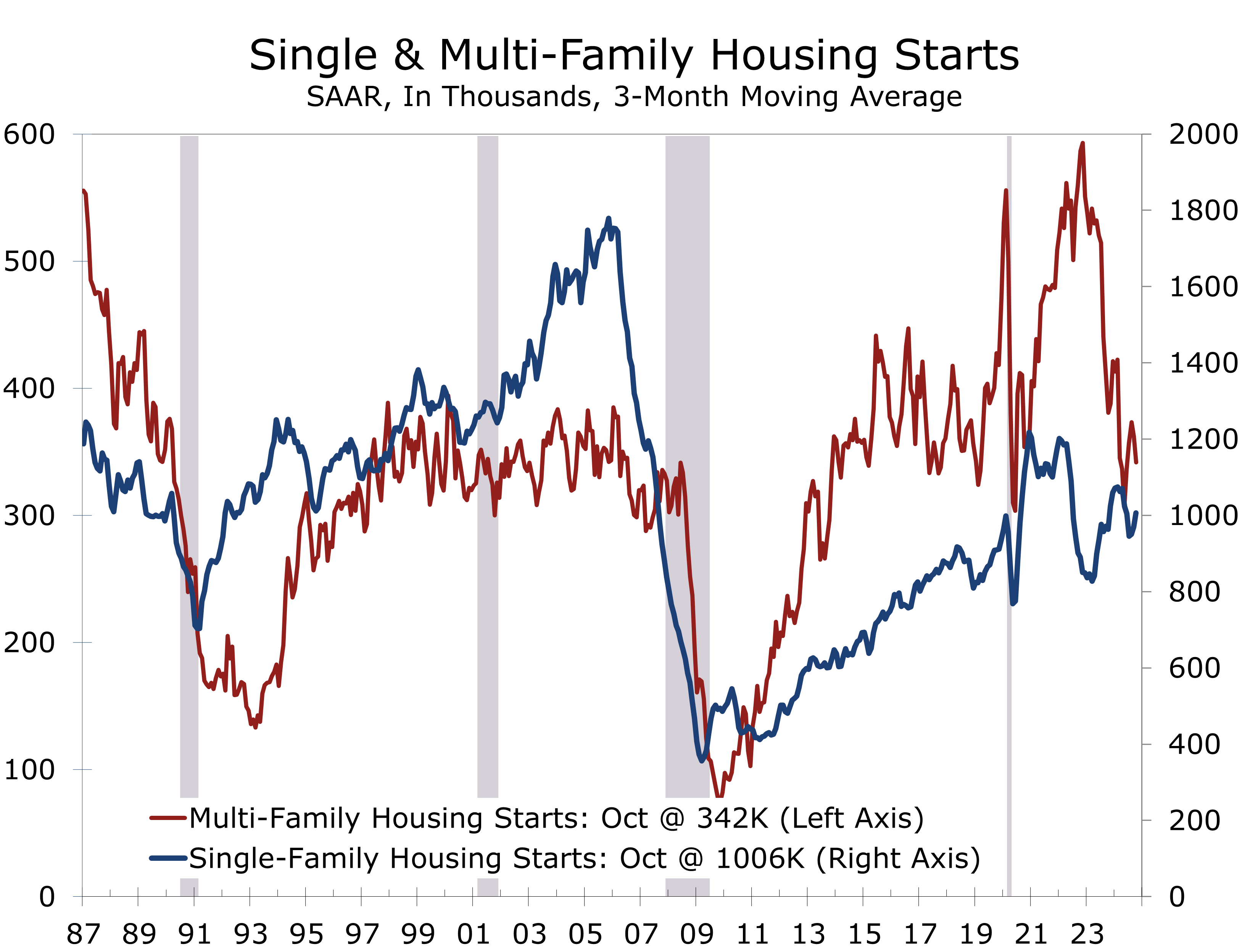

- Single-family starts fell 6.9% in October, while multi-family starts rose 9.7%.

- Despite falling back below a 1 million unit pace, single-family construction remains resilient at a 970,000-unit annual rate.

- Year-to-date, single-family starts are up 9.3%, fueled by strong pent-up demand and limited resale inventory, while multi-family starts are down 29.3%, pressured by higher vacancies, falling rents, and tighter credit.

- The West (+21.1%) and Midwest (+9.4%) saw strong gains, while the South (-8.8%) and Northeast (-32.9%) faced disruptions from hurricanes and affordability hurdles.

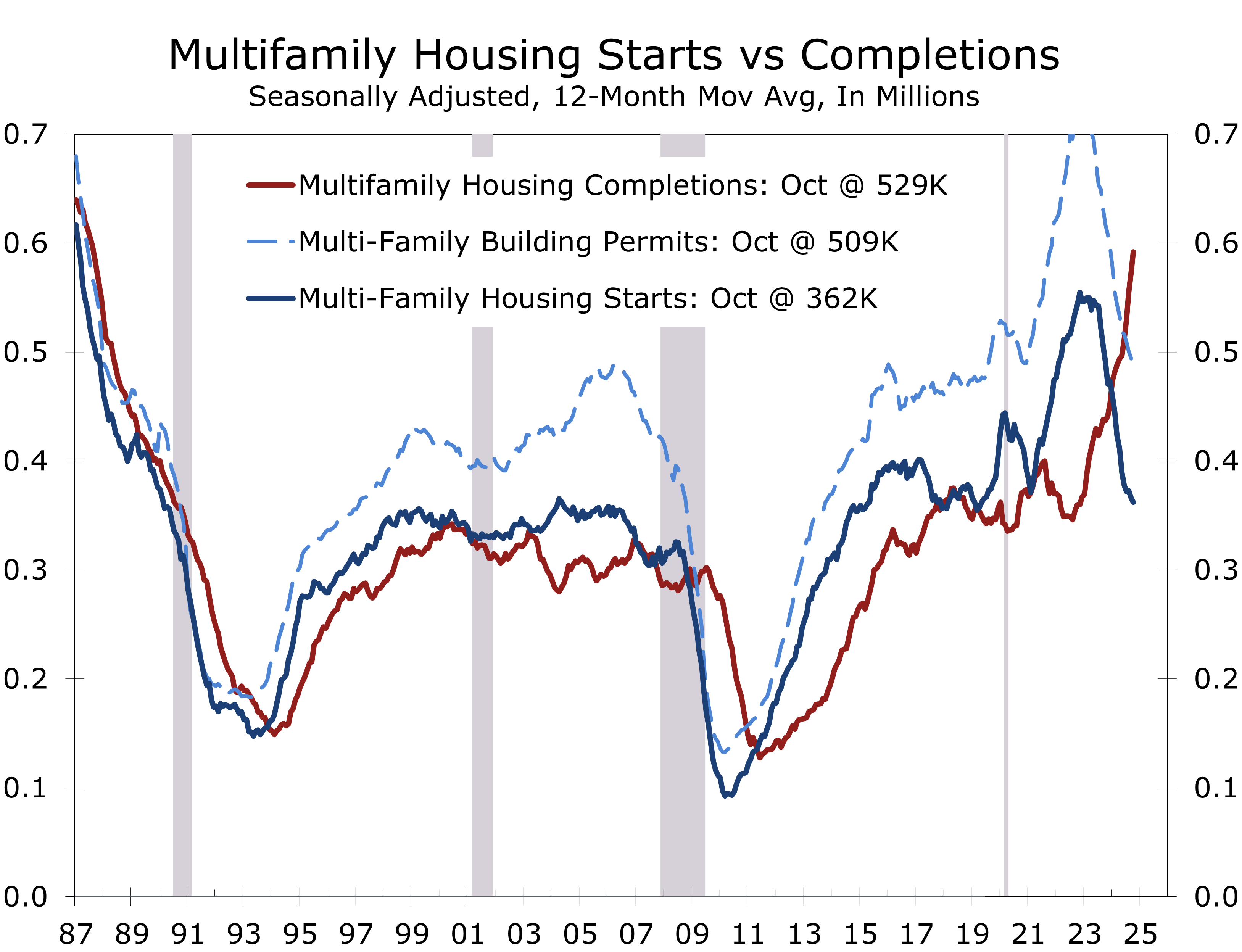

- Overall housing completions rose 16.8% year-over-year, driven by a wave of multi-family completions, addressing the supply overhang from the 2022-2023 boom.

- Housing starts fell short of expectations, as back-to-back hurricanes hindered activity in the South. In contrast, milder-than-usual fall weather in the West and Midwest bolstered starts. Builder confidence has improved, driven by lower short-term rates and continued hopes for lower mortgage rates.

Housing starts declined 3.1% in October to a 1.31-million-unit seasonally adjusted annual rate (SAAR), a slightly slower than expected pace. Starts are down 4.0% year-to-year, with a notable split between the relatively resilient single-family starts and the ongoing challenges in the multi-family segment. The shortfall in starts also reflects the impacts from back-to-back hurricanes, which cut starts in the South, which is by far the largest region for new home building.

Single-family housing starts fell 6.9% in October to a 970,000-unit pace. Despite this decline, single-family activity remains robust on a year-to-date (YTD) basis, rising 9.3% compared to the prior year. Strong pent-up demand for new homes, coupled with historically low levels of resale inventory, continues to provide a potent tailwind for single-family construction, even amid affordability concerns and higher mortgage rates.

October’s rise in multi-family starts suggests the apartment market is finding its footing.

Multi-family starts rose 9.7% to a 326,000-unit pace but remained down a sharp 29.3% YTD. While tighter credit, rising vacancies, and slower rent growth weigh on development, stronger-than-expected apartment demand has allowed more projects to move forward. The October increase suggests near-term stabilization, though the sector remains in correction.

Building permits, which are less impacted by weather distortions, edged 0.6% lower to a 1.416-million-unit SAAR in October. This modest decline reflects a 3.0% drop in multi-family permits, counterbalanced by a 0.5% rise in single-family permits, reflecting some tentative stability in single-family construction activity.

The apartment boom continues to wind down, with the backlog of projects gradually declining.

Housing completions paint a more dynamic picture. Overall completions fell 4.4% in October, possibly reflecting some impact from Hurricanes Helene and Milton. Completions have surged 16.8% over the past year, however, driven by a wave of apartment completions. That onslaught of supply has pushed vacancy rates higher and weakened asking rents. Fortunately, the sector’s backlog is finally clearing, which is allowing a handful of projects in faster growing market to move forward.

Regionally, housing starts rose in the West (+21.1%) and Midwest (+9.4%) due to strong single-family demand and a rebound in multi-family activity. The Northeast (-32.9%) and South (-8.8%) saw declines. The South, which generates 55% of U.S. housing starts, was hit by hurricanes and waning affordability migration as rising home prices diminished the appeal of relocating from higher-cost parts of the country.

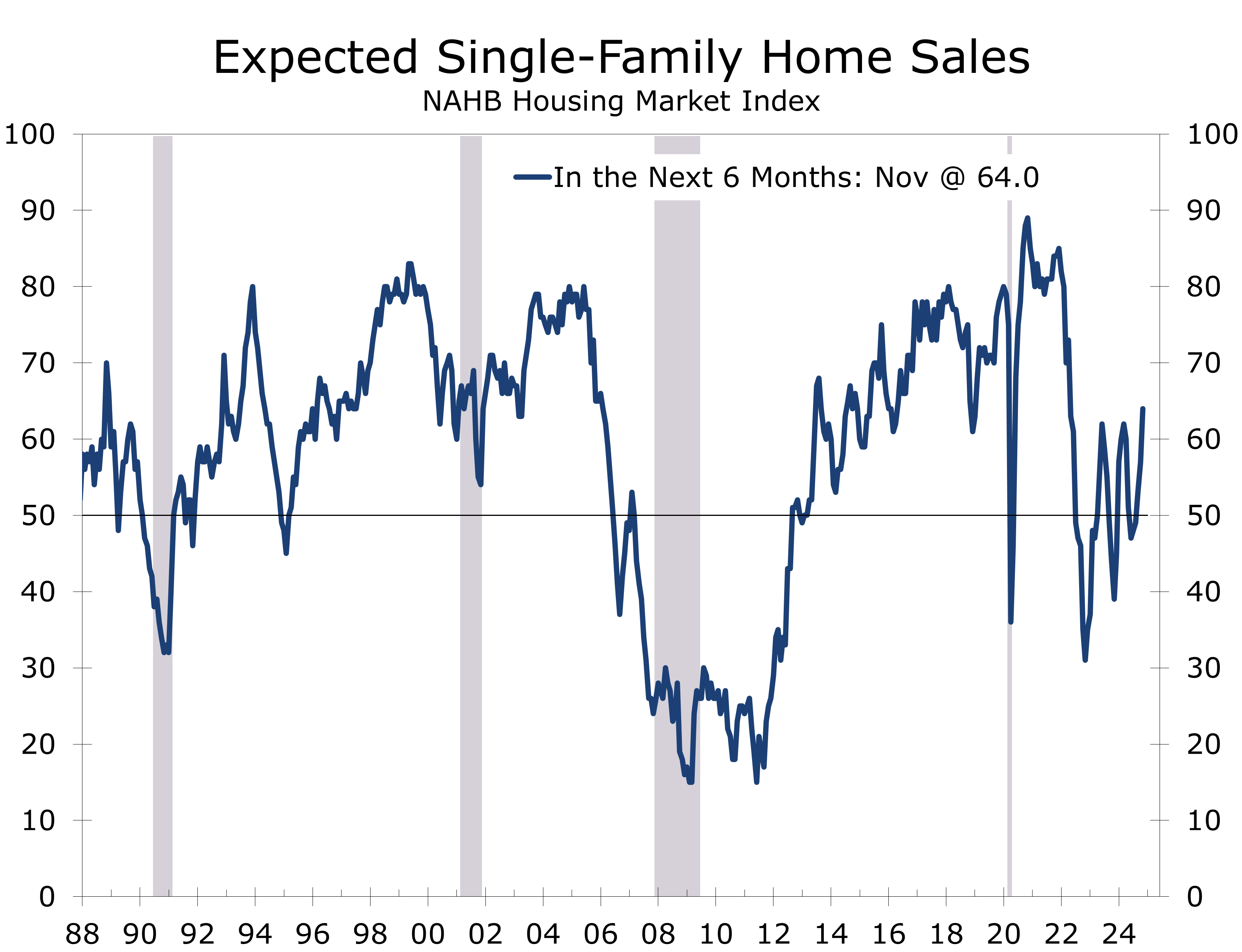

Builder sentiment improved for the third consecutive month in November, with the NAHB/Wells Fargo Housing Market Index (HMI) rising 3 points to 46. Optimism was likely driven by the Republican sweep of the presidency, House, and Senate, which is expected to ease regulations and open more land for development. Expectations for sales over the next six months surged, likely at least partly because of this.

Despite rising confidence, builders face persistent challenges, including labor shortages, a shortage of buildable lots, and high building material costs. Moreover, mortgage rates surpassing 7% have further strained affordability. In November, 31% of builders reduced home prices, with average price cuts easing slightly to 5%, while the share of builders offering sales incentives dipped from 62% to 60%.

All three HMI sub-indices improved in November: current sales conditions rose 2 points to 49, sales expectations jumped 7 points to 64, and buyer traffic increased 3 points to 32. Regionally, the Northeast gained 4 points to 55, the Midwest rose 3 points to 44, the South edged up to 42, and the West held steady at 41. Single-family construction is expected to strengthen this spring as mortgage rates dip below 7%.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 19, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

(704) 458-4000