Goldilocks Still Wants a Big Raise

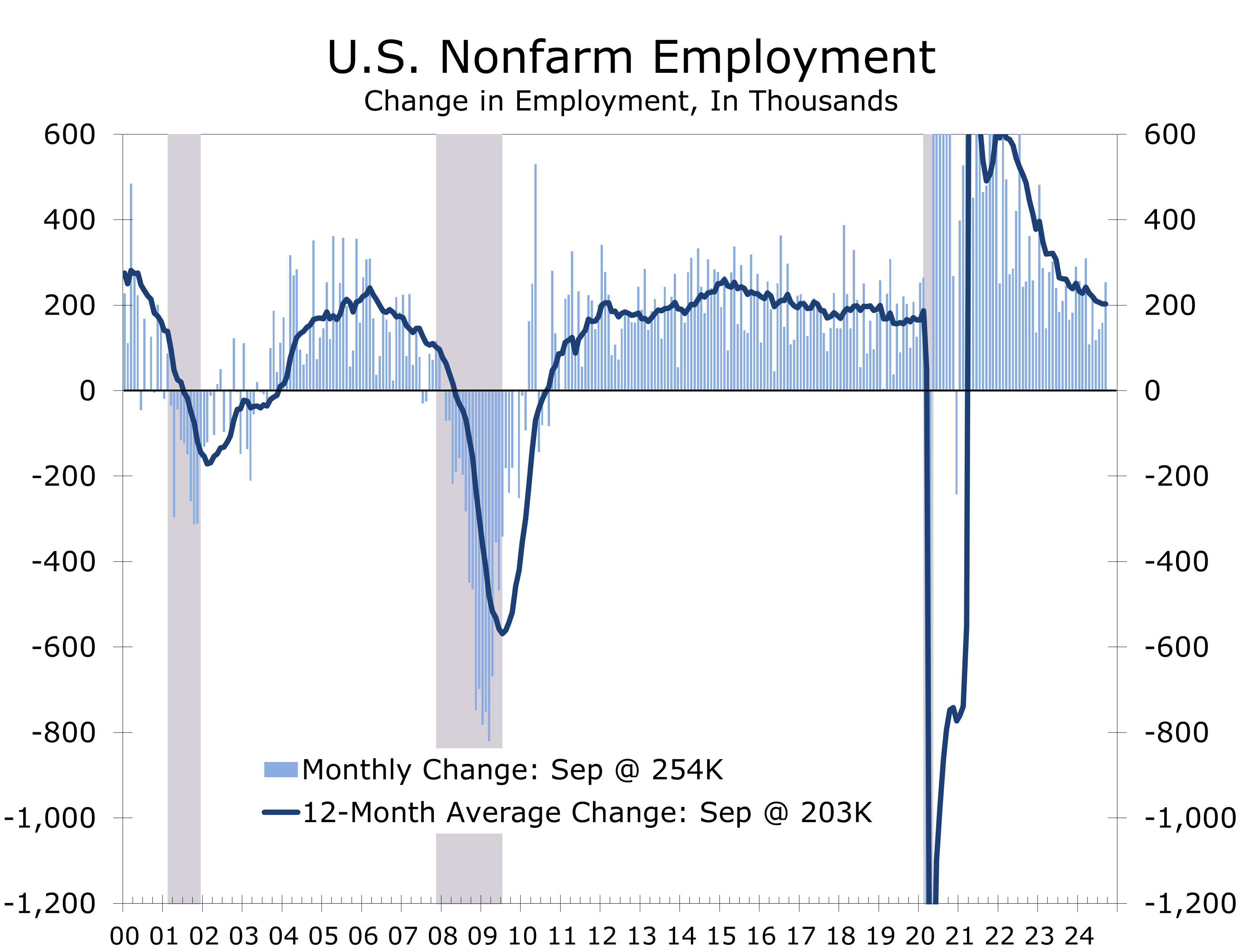

- Employers added 254,000 jobs in September, significantly exceeding the consensus estimate of 150,000.

- Revisions to the prior two months’ data added a combined 72,000 jobs, easing concerns that the labor market had cooled too much.

- The unemployment rate fell 0.1 percentage point to 4.1%, as the number of employed persons rose by 430,000 and far outstripped the 150,000-person rise in the labor force.

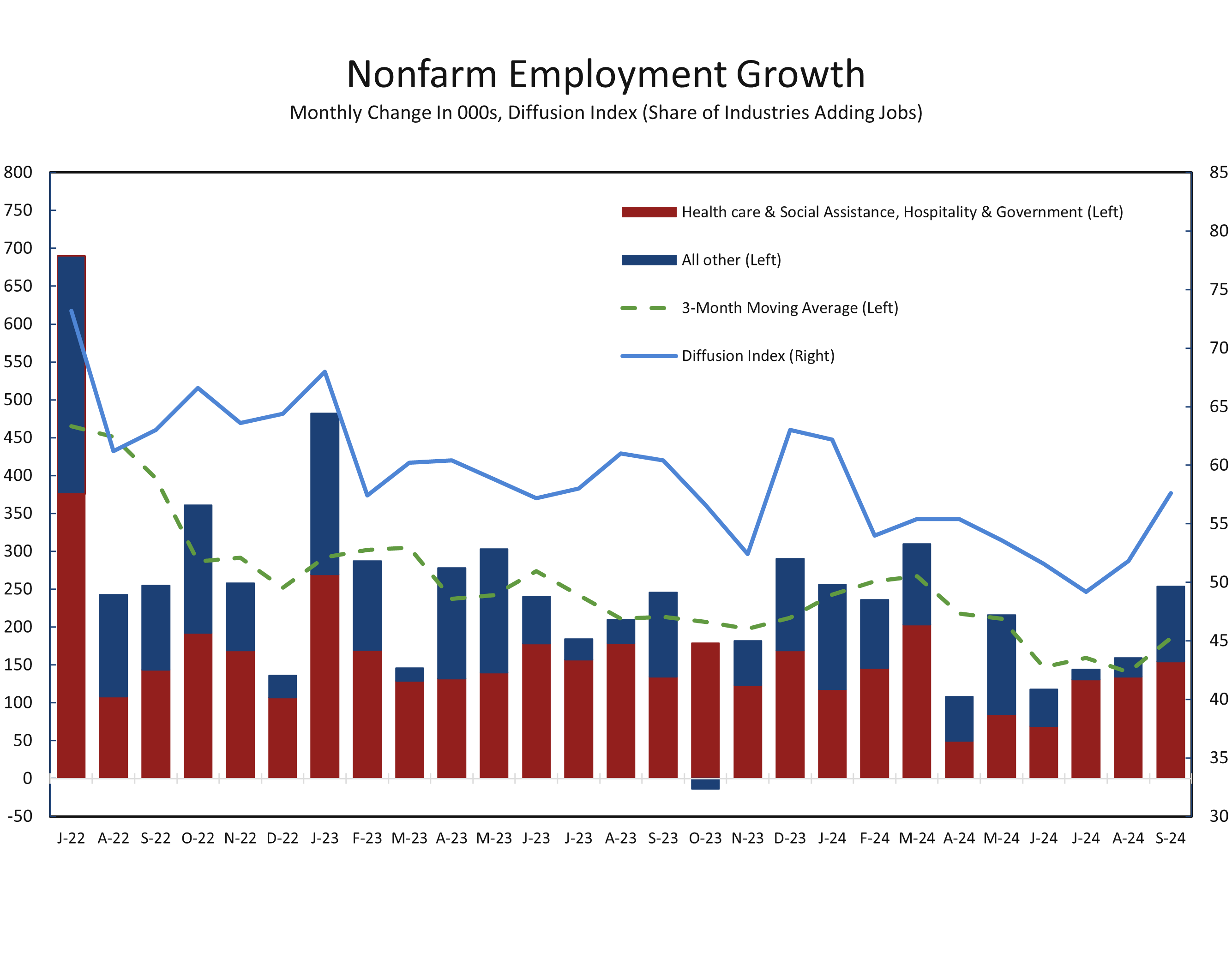

- Leisure and hospitality (+78K), health care and social assistance (+72K), government (+31K) and construction (+25K) continue to account for the bulk (80%+) of net new jobs.

- Job gains are more widespread, however, with the diffusion index rising to 57.6, up 8.4 points from its July low.

- Many pundits labeled September’s job report as a return to a Goldilocks economy—not too hot, not too cold. While some data supports this view, something is off. Labor unrest persists. The tentative port deal includes a 62.5% pay raise over five years and limits on productivity-enhancing investments. This hardly seems consistent with a cooling labor market.

The September employment report exceeded expectations, with employers adding 254,000 net new jobs—the most in six months. Revisions to July and August added another 72,000 jobs, suggesting the labor market was not as weak as the Fed feared at the September FOMC meeting. Job gains were also slightly more broad-based, and the strength in payrolls was confirmed by a 430,000-job gain in the household survey. The drop in the unemployment rate is actually larger than it appears. The unemployment rate fell by 0.17 percentage points to 4.1%. The August unemployment rate was rounded down to 4.2% and September’s rate is now being rounded up to 4.1%.

Job growth exceeded expectations, easing fears but dashing hopes for aggressive rate cuts.

The improved labor market assessment follows unexpectedly large upward revisions to the National Income and Product Accounts (NIPA) last week, which showed that growth, income, savings, and corporate profits are all in better shape than previously thought. This more robust economic backdrop was acknowledged by Fed Chair Jerome Powell earlier this week, signaling a cautious approach to further rate cuts. Powell noted that any further weakening of the labor market would be unwelcome. Those concerns now seem overblown, which may prompt some forecasters to lower expectations for rate cuts in 2025.

While job gains were broad-based, leisure and hospitality, healthcare, government, and construction made up the bulk of the increases. The diffusion index for private nonfarm payrolls, which tracks the percentage of industries adding staff, rose to 57.6% in September, up from 49.2% in July and marking the highest level since January. Job growth has slowed significantly across several sectors, including wholesale trade, retailing, transportation and warehousing, information, financial activities, professional and business services, and other services.

While more industries added jobs in September, job growth remained highly concentrated.

Manufacturing remains a weak spot, with payrolls declining over the past two months and down more than 40,000 this year. The Boeing strike, which began in September, may impact October’s data. More fundamentally, demand for goods has softened since the Fed began raising rates and will take time to recover. We expect lower interest rates to boost home buying and durable goods purchases by next spring.

Hours-worked are another weak spot. Average weekly hours declined slightly to 34.2. Total hours worked fell by 0.1% in September and rose at just a 0.2% annual rate in the third quarter. Changes in hours worked are closely watched because they often precede changes in employment.

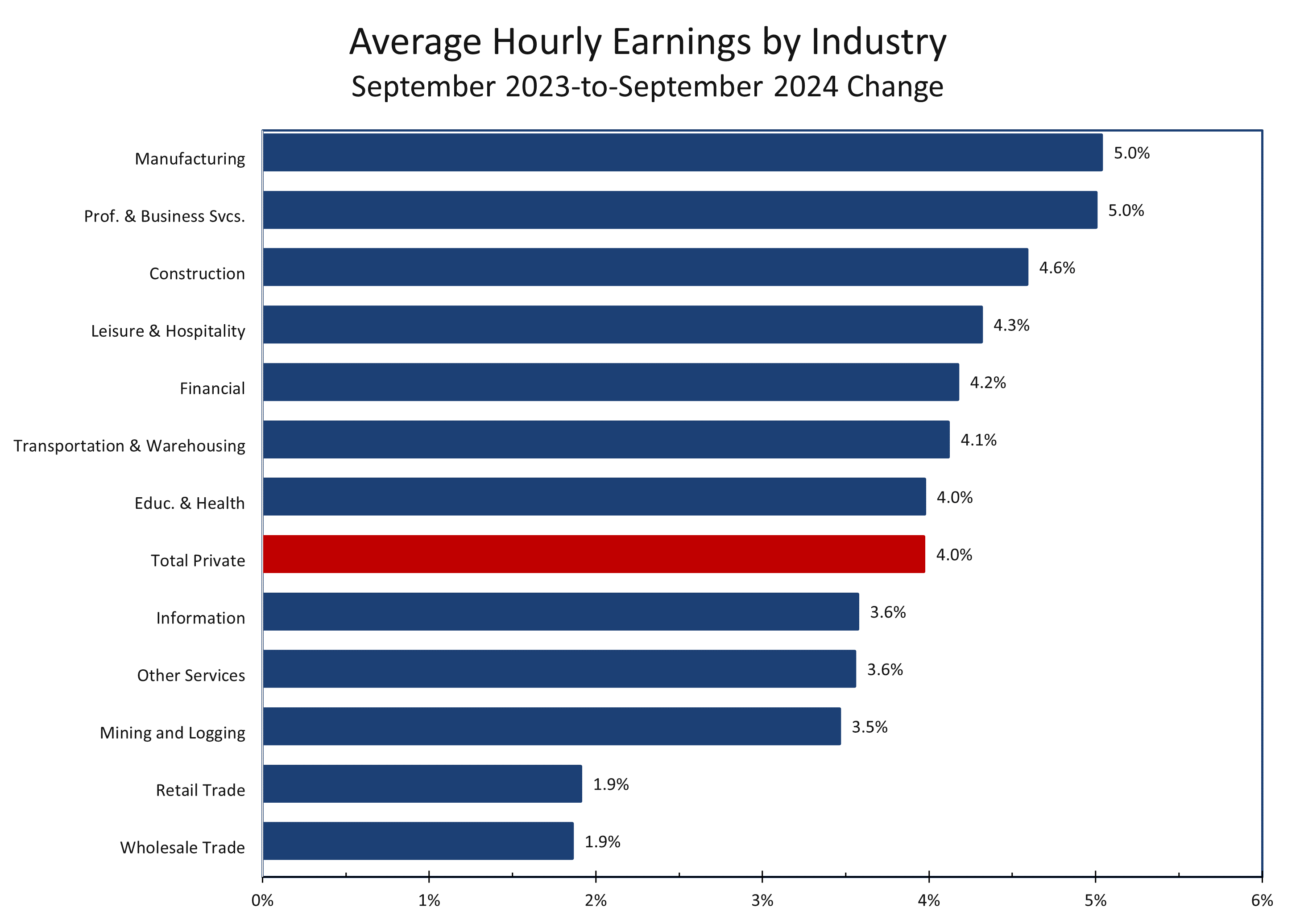

Average hourly earnings for private nonfarm employees rose by 13 cents (0.4%) to $35.36 in September, reflecting a 4.0% increase over the past year. Wages for private-sector production and nonsupervisory workers increased by 8 cents (0.3%) to $30.33. Despite recent productivity gains, these wage increases exceed the Fed’s preferences, particularly amid heightened strike activity and significant wage settlements. Even with improved productivity, annual wage gains of 4% or more are inconsistent with a sustained return to 2% inflation.

Overall, September’s employment report wasn’t as strong as the headlines suggest. While job growth rebounded, much of it came from just four sectors—restaurants, retail, healthcare, and government—all still working to restore staffing to pre-pandemic levels, with many of the jobs added being in lower-paying occupations.

Combined with stronger income and profits data, the economy appears less vulnerable than previously feared. The Fed is expected to proceed with a more measured pace of rate cuts, likely opting for 25 basis-point reductions in both November and December. We have also removed one of the rate cuts we had penciled in for 2025.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 4, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704)-458-4000