The Weakest Job Growth Since the Pandemic

- Employers added just 114,000 jobs in July, marking the smallest hiring gain since …

- Revisions were modest but most negative, subtracting a combined 29,000 jobs from the previously reported May and June data.

- Health care and social assistance, leisure and hospitality and government continue to account for the bulk of net new jobs (90%+ of the total). Hiring elsewhere was sparce.

- There were a few other notable bright spots. Construction added 25,000 jobs and hiring rose solidly in transportation & warehousing and wholesale trade.

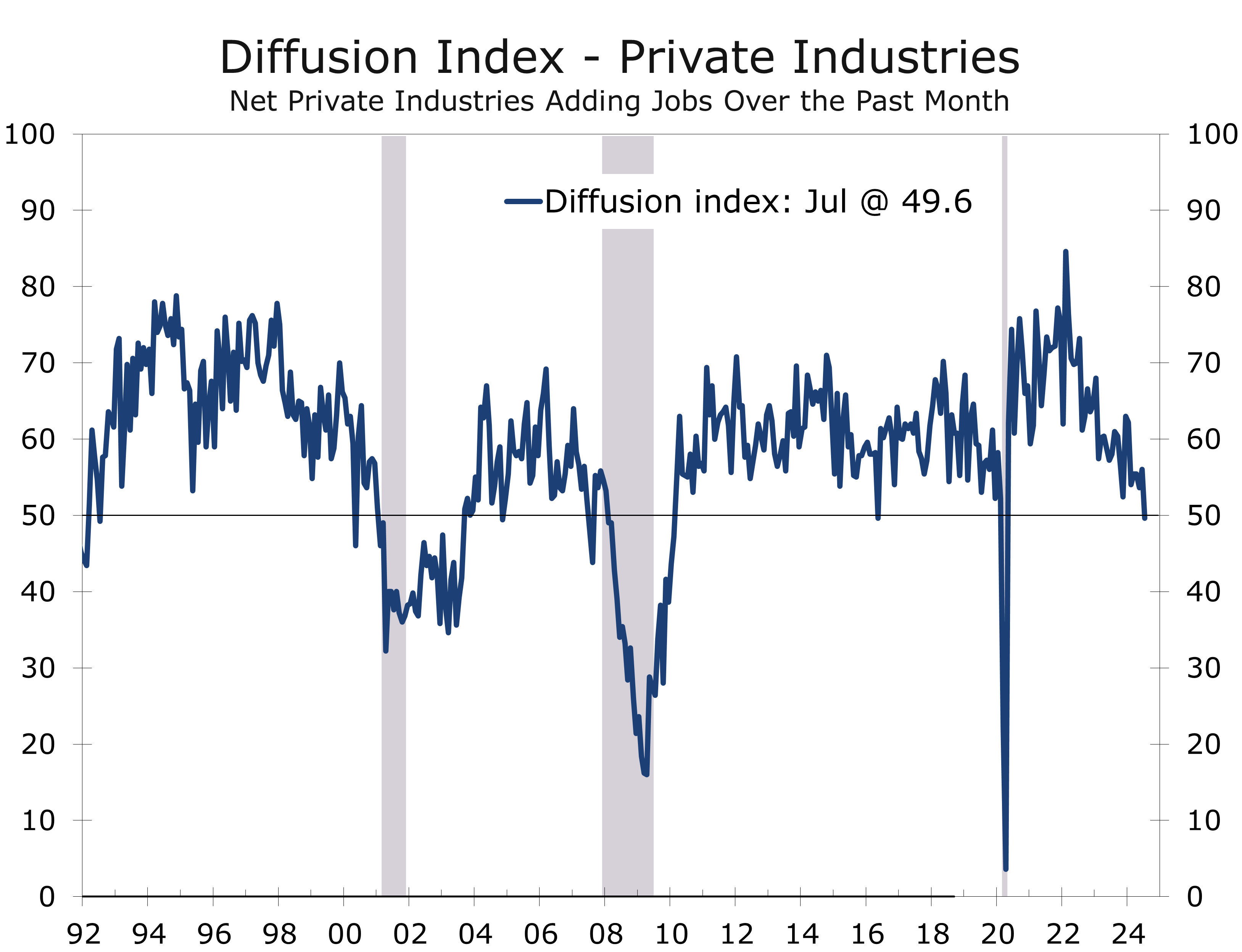

- The diffusion index fell 6.4 point to 49.6 and average workweek fell, both are reliable precursors for slower nonfarm job growth.

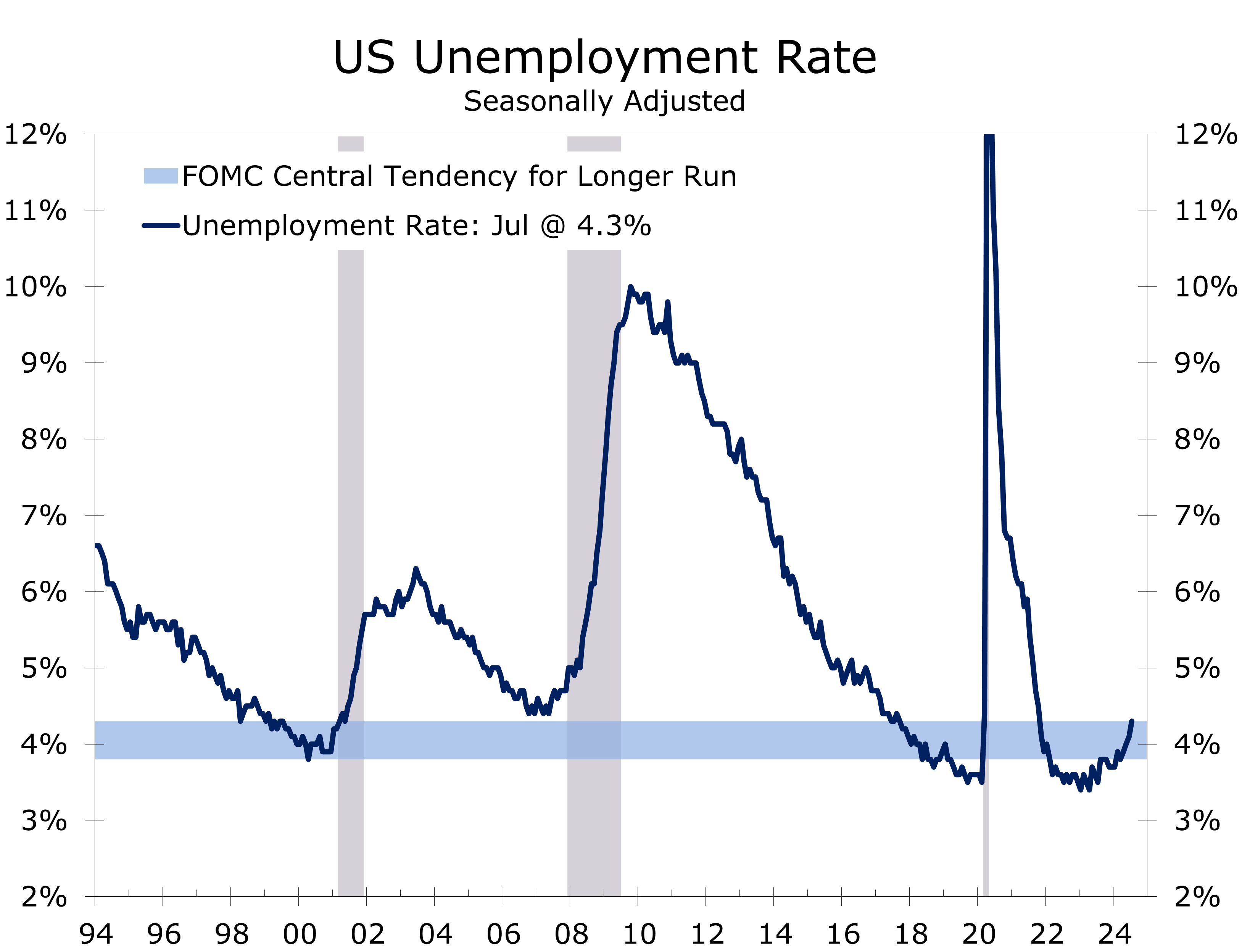

- The unemployment rate rose 0.2 percentage points higher to 4.3%, hitting its highest level since October 2021.

- July’s weaker employment numbers and higher unemployment rate will fuel the discussion of whether the Fed is waiting too long to begin to cut interest rates. A recession on top of the transitory inflation fiasco would be disastrous for the Fed. The economy is still growing, however, and the summertime data is often quite volatile.

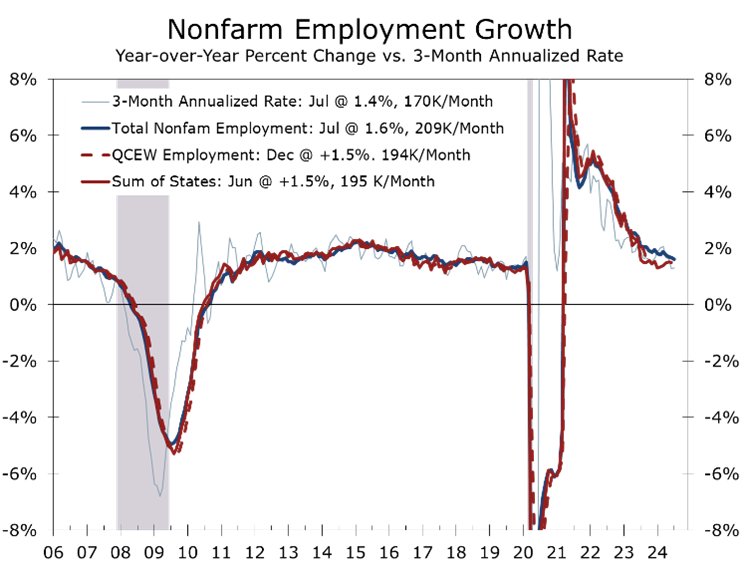

Employers added just 114,000 nonfarm jobs in July, which was well below consensus expectations. Moreover, job gains May and June were revised lower by a combined 29,000 jobs. Employers have added an average of 170,000 jobs a month over the past three months, down from an average of 209,000 a month over the past year.

Hiring continues to decelerate and is now more closely in line with the QCEW data.

Hiring has slowed significantly, aligning with our long-held forecast for payroll growth to moderate to around 170,000 jobs per month by mid-2024. This forecast is based on the latest data from the Quarterly Census of Employment and Wages (QCEW), which is the source data for the annual revisions. The BLS is set to release preliminary estimates through March 2024 on August 21, which we expect to show weaker job growth for the six months ended March 2024 than currently reported.

Not only has job growth slowed, but gains are now much more narrowly based. The diffusion index, measuring the share of industry sectors adding jobs, fell 6.4 points in July to 49.6. This indicates that more industries reduced rather than increased employment in July, marking the first reading below the key 50 break-even level since April 2020 during the pandemic.

Job growth remains highly concentrated in just a handful of key industries. Health care and social assistance added 64,000 jobs, with most gains occurring in lower-paying segments like home health care (+21,600), hospitals (+19,500), nursing homes (+9,200), and social assistance (+9,000).

Excluding health care, the largest payroll gains were in construction (+25,000), leisure and hospitality (+23,000), government (+17,000), and transportation and warehousing (+14,000). Conversely, the information sector (-20,000), education (-7,000), other services (-5,000), and financial services (-4,000) saw job losses. Manufacturers added 1,000 jobs in July, despite July’s surprisingly weak ISM report.

Some of the air may be coming out of the AI boom, with notable job losses in the tech sector.

The information sector experienced unusually large losses in July. Job declines were widespread, with publishing (-5,900), telecommunications (-4,500), and motion picture and sound recording (-3,500) posting the largest drops. The tech subcategories, including computing infrastructure providers, data processing, web hosting, and web search, lost 2,600 and 2,500 jobs respectively. The decline may reflect a recalibration of investment in the AI boom as firms adjust to a slower-than-anticipated uptake in user demand.

The July employment report underscores the need for a shift in monetary policy. The unemployment rate increased by 0.2 percentage points to 4.3%, technically activating the Sahm recession warning rule. This rise was largely driven by a surge of 249,000 unemployed workers on temporary layoff, which accounted for 70% of the overall increase in unemployment. Additionally, an influx of 420,000 new job seekers pushed the unemployment rate higher. The unemployment rate now sits slightly above the upper range of the Fed’s long-run view of full employment.

A surge of temporary layoffs and stronger labor force growth lifted the unemployment rate.

While the jump in the unemployment rate looks a little suspicious, there is no doubt the labor market has moved into balance or beyond. Hours worked fell by 0.3% in July, and our income proxy has risen at under a 0.1% annual rate over the past three months. The data indicates the economy is slowing more than expected, possibly moving beyond a soft landing. Q3 GDP is currently on track to grow at just a 1.8% pace. We still anticipate two quarter-point rate cuts this fall, but the Fed may act more aggressively if upcoming reports and the August jobs data also show significant weakness.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 2, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

704-458-4000