Finally, A Goldilocks-like Employment Report

- Employment growth kicked off the second quarter on a softer note, with employers adding 175k jobs in April, well below the first-quarter average of 270k.

- Job growth has averaged 242,000 the past 3 months, versus an earlier reported 276k.

- While gains remain broad based, health care, social assistance, logistics, and retailing accounted for the bulk of April’s job gains.

- The diffusion index, or share of industries adding staff, rose from 59.6 to 60.4 in April.

- Payrolls were revised 22k lower for the prior 2 months. Seasonal factors boosted reported April job growth by about 50k.

- The Household survey was soft, with the unemployment rate rising 0.1 pp to 3.9%.

- Average hourly earnings rose 0.2% in April, reflecting a heavier mix of lower-paying jobs added this past month.

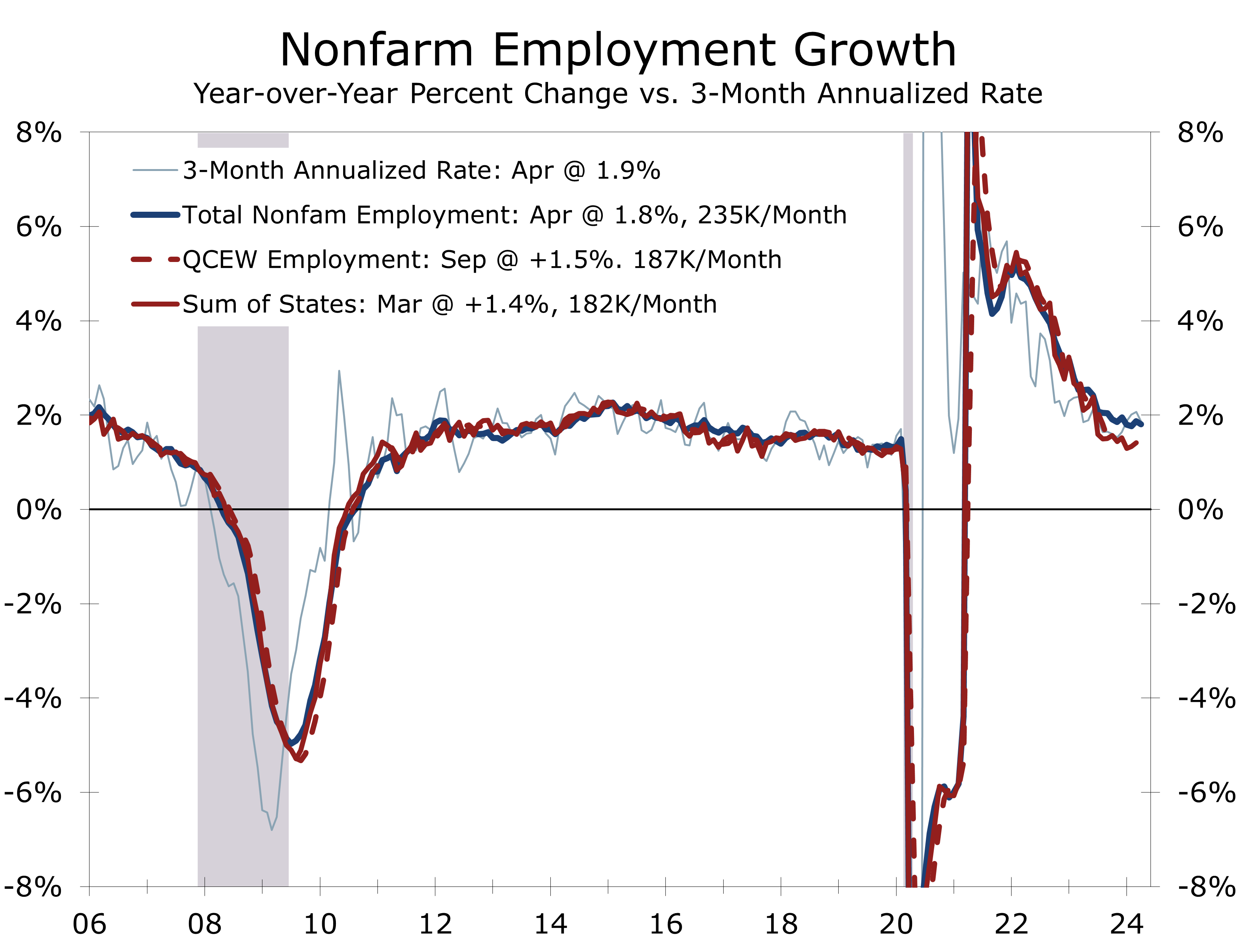

- After adding jobs at a torrid pace in the first quarter, hiring slowed more in line with our expectations. We look for job growth to slow to 170,000 jobs a month around the middle of this year, which would be consistent with the recent trend in the Quarterly Census of Employment and Wages and Sum of States employment.

Following a string of stronger than expected job gains in the first quarter, employers throttled back hiring in April. Nonfarm employers added 175,000 jobs and job growth for the prior 2 months was revised lower by a combined 22,000 jobs.

Employers have added an average of 234,600 jobs a month over the past year, and 242k a month over the past three months (down from 279k previously). April’s 175,000-job gain was the smallest in six months.

April’s moderation in hiring reflects the winding down of efforts to restaff in hard to hire sectors.

The moderation in job growth likely reflects the winding down of efforts to restaff in the leisure and hospitality industry and government. The more moderate pace is also closer to what we believe the underlying trend actually is.

We have highlighted the softer trend in the Quarterly Census of Employment and Wages, which is the most accurate measure of employment and the source of the annual revisions to the monthly payroll series. Data for the QCEW is available through September 2023 and has been running around a half percentage point below nonfarm payroll growth, which would reduce growth 71,000 jobs a month over the past year. QCEW data thru December will be released May 22nd.

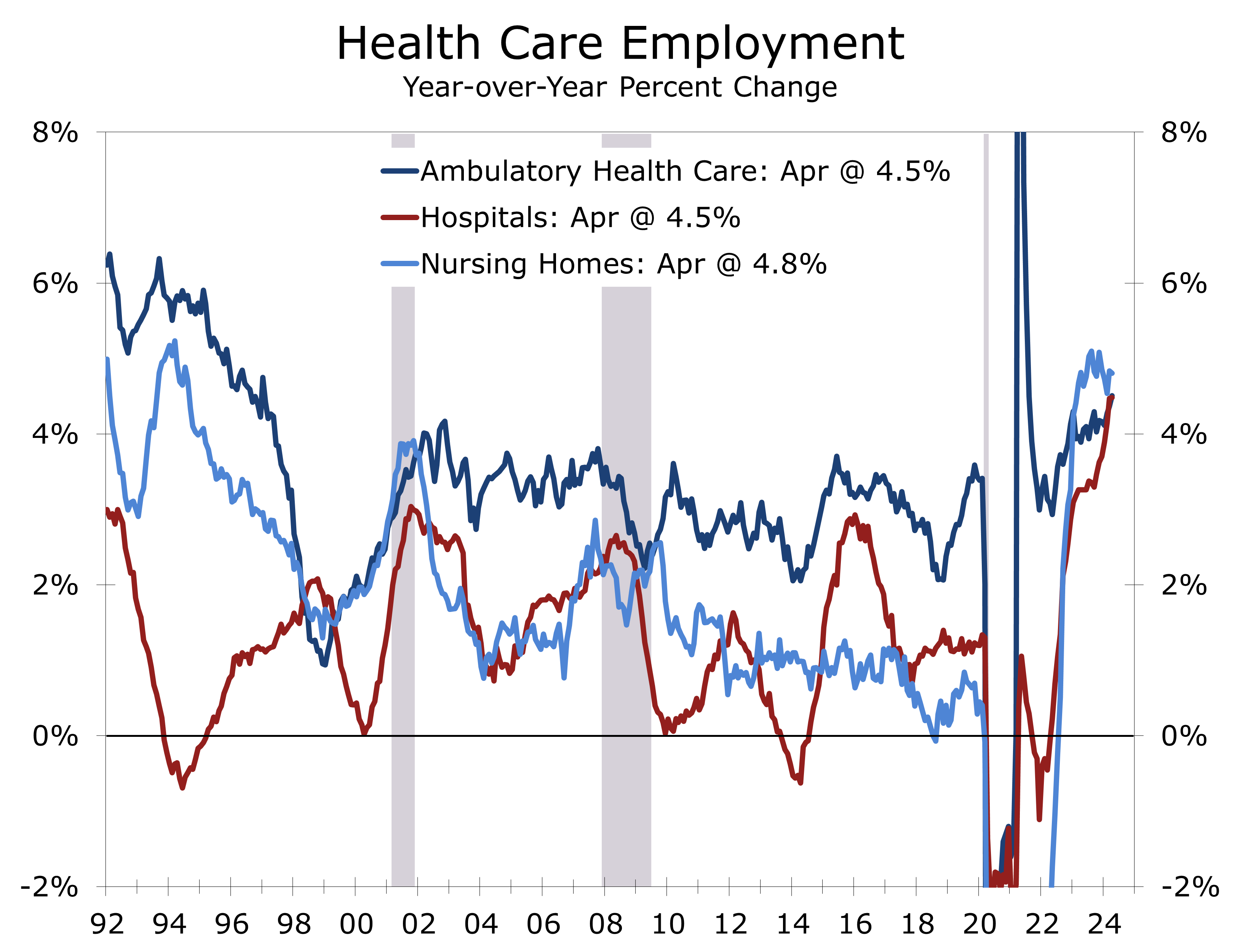

Job gains remain fairly broad based. The diffusion index, which measures the net share of private industries adding staff, rose from 59.6 to 60.4 in April. The bulk of job gains, however, were added in health care and social assistance, which added 87,000 jobs in April, or just under half of all net new jobs.

Health care providers added 56,200 jobs in April. The sector has been striving to rehire workers let go during the pandemic, particularly now that demand for health care has bounced back from folks that had put off visits and procedures during the pandemic. The bulk of job gains are in ambulatory care, a category that includes doctors and dentist offices and home health care. Hiring is also rising at hospitals and nursing homes.

Social services added 30,800 jobs in April, with the bulk of the increase coming from individual and family services. Childcare also continues to add staff.

Health care providers added close to half of all jobs created in April and 26.5% this past year.

Health care and social services have been one of the fastest growing sectors this past year, adding an average of 85,000 jobs a month. By contrast, hiring in two other rapidly growing sectors – leisure and hospitality and government – slowed abruptly, adding just 5,000 and 8,000 jobs in April, versus an average gain of 32,000 and 53,000 jobs a month this past year.

Hiring rose more modestly elsewhere. Transportation and warehousing added 21,800 jobs in April, led by couriers and warehousing. Retailers added 20,000 jobs, while hiring in construction (+9k), manufacturing (+8k) and financial services (6k) eked out minimal gains. Employment declined in information (-8k), professional services (-4k), and mining (-3.5k).

Average weekly hours declined 0.1 to 34.3 hours, and the factory workweek and overtime hours were unchanged at 40 and 2.9 hours, respectively. The drop in aggregate hours means personal income will likely barely eke out a 0.1% gain in April. Industrial production also looks like it started Q2 on a soft note.

Average hourly earnings rose a smaller than expected 0.2% in April, pulling down the year-to-year rise to 3.9%. The slide aligns with other wage measures, such as the Atlanta Fed Wage Tracker, and coincides with the continuing slide in the Quits rate, reported in the JOLTS data earlier this week. Job openings also fell.

The April employment data affirm much of what Jay Powell covered in his press conference, when he noted the economy is moving into better balance. We are looking for two quarter-point rate cuts this year, with the first in September and a second in December.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 3, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000