But Hiring Is Softer Than the Headline Suggests

- Employers added 216,000 jobs in December, surpassing the consensus forecast of 165,000.

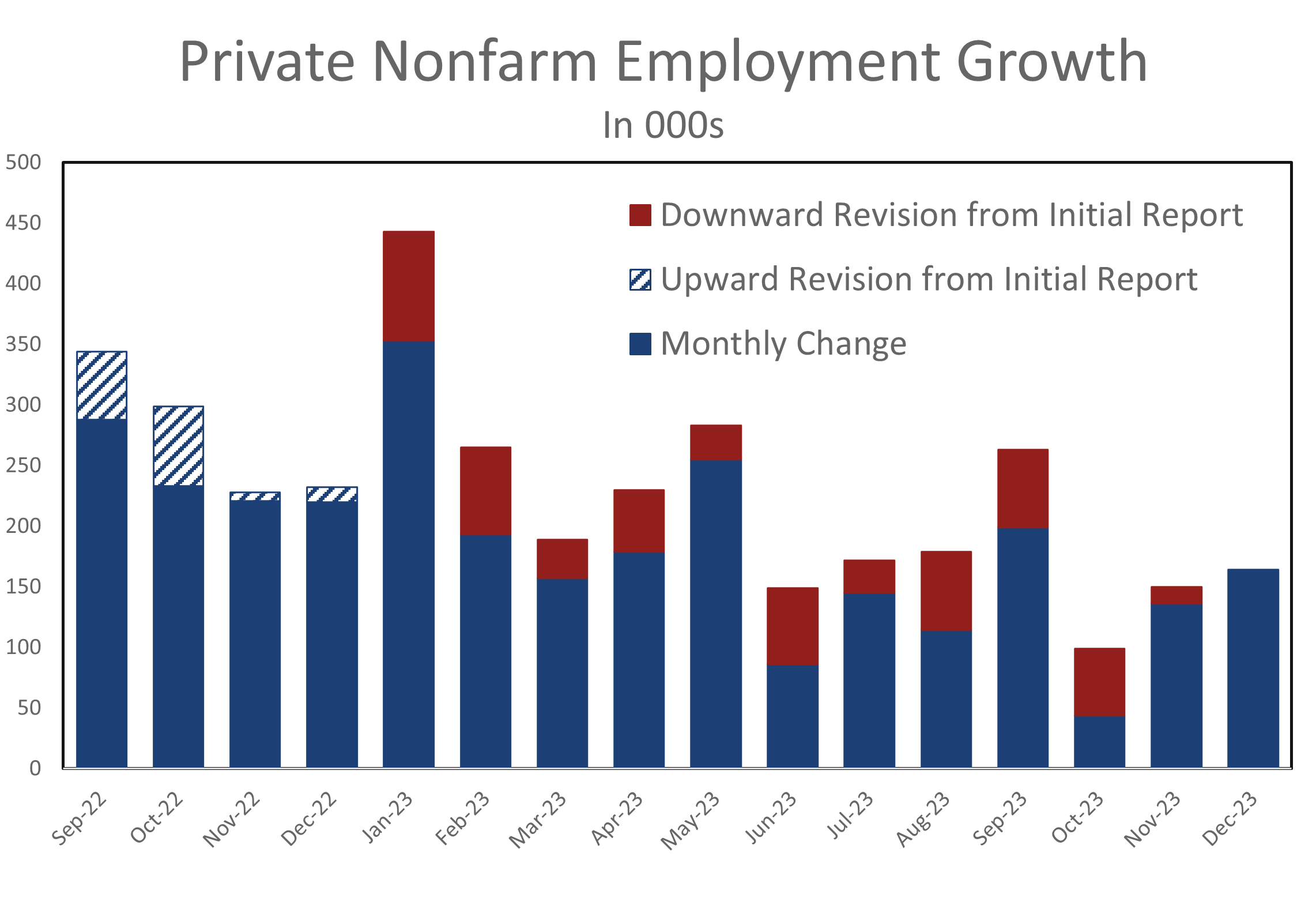

- Hiring was not as strong as the headline suggests, as payrolls were revised lower for the preceding two months.

- Fewer industries are hiring aggressively, with the majority of job growth now coming from government (+52K), leisure and hospitality (+40K) and health care (37.7K).

- Hiring is strongest in lower-paying occupations where rehiring workers laid off during the pandemic has proved challenging.

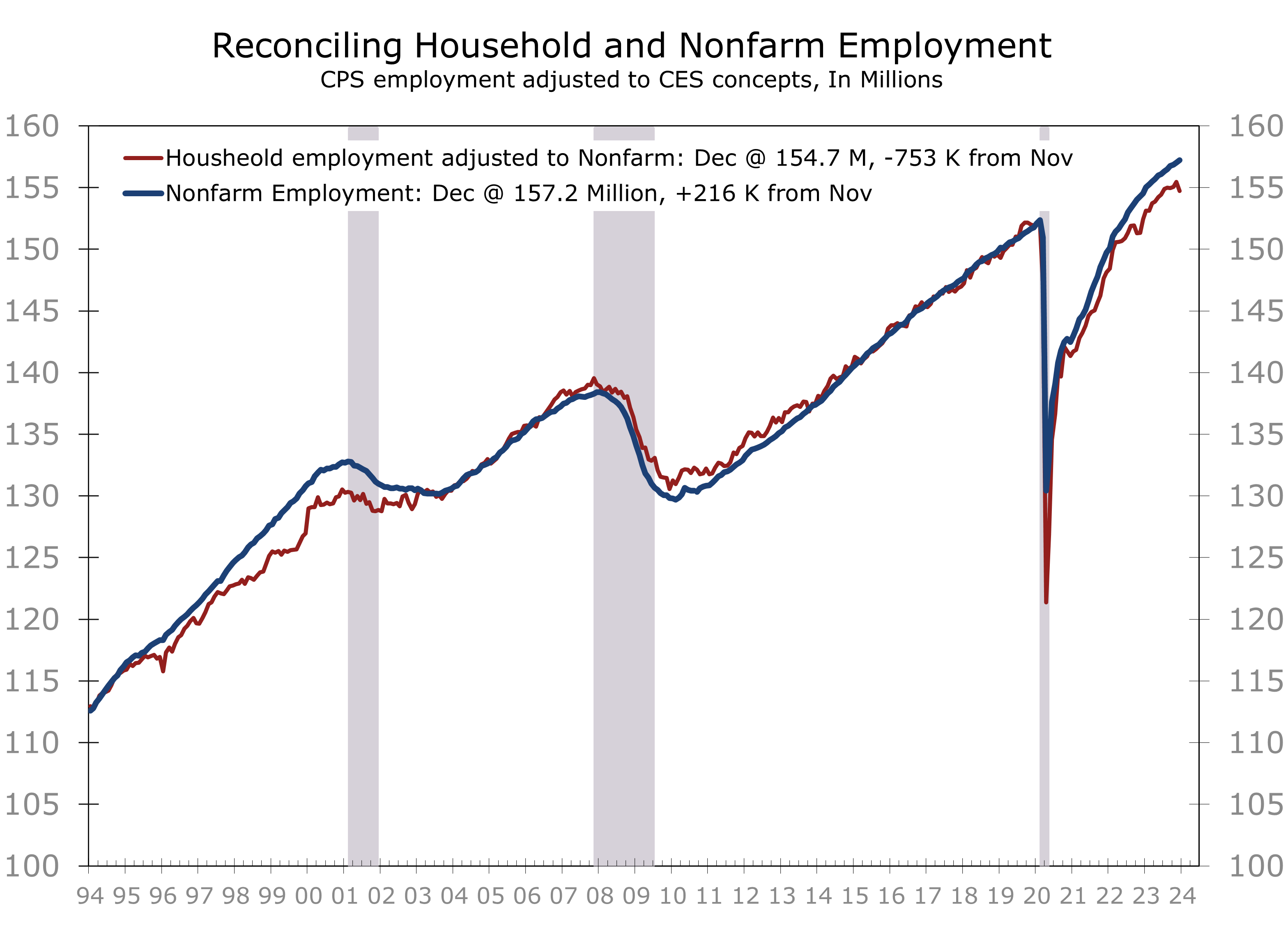

- The unemployment rate remained unchanged at 3.7%, as both the labor force and household employment falling by roughly the same proportion.

- Average hourly earnings rose a larger-than-expected 0.44% in December and are up 4.1% from last December.

- Job growth remains solid but is concentrated in a handful of industries, with weak hiring in the goods sector and a slowdown in certain parts of the services sector. Revisions to previous months’ data reinforce the decelerating trend. We anticipate three quarter-point interest rate cuts this year, which is half of the current consensus.

There is much to digest from the December employment data. Although the overall gain of 216,000 jobs exceeded expectations by 41,000 jobs, downward revisions to the previous two months’ data tempered the positive headline number. Job growth was also concentrated in just a few sectors, with government payrolls (+52k) and health care and social assistance (+58.9k) contributing to over half of December’s increase.

Warmer-than-usual weather likely boosted job gains, particularly in leisure hospitality (adding 40,000 jobs), and retail trade and construction (both adding 17,000 jobs). Hiring in most other sectors was less robust. Manufacturers added 6,000 jobs, financial services added 2,000 jobs (primarily in property management), and information services added 14,000 jobs, mainly in motion pictures, indicating a sustained recovery from the recent writers and screen actors’ strikes.

Temporary staffing jobs continues to decline, possibly presaging weaker overall job growth.

The AI boom appears to be bolstering hiring in the tech sector. IT services added 4,400 jobs in December, and professional, scientific, and technical services saw a gain of 25,300 job. Overall job growth in professional services, however, continues to be hindered by declines in temporary staffing jobs (-33.3k).

The unusually wide gap between temporary jobs and nonfarm employment is primarily due to increased hiring in the public sector. Government payrolls have surged by 2.9% this past year, with the bulk of the increase occurring at the state and local levels. Hiring has accelerated in various line positions that were challenging to fill following the pandemic lockdowns, such as bus drivers, sanitation workers, and within public school systems and other public works.

Outside of government hiring is losing momentum., Private sector rose just 1.5% over the past year and at a 1.0% annual rate over the last three months. Furthermore, the initial estimate for private sector payrolls has been consistently revised lower in each subsequent month throughout the year.

Private sector payrolls have consistently been revised downward each month this year.

The BLS will provide a comprehensive employment update next month when they releases their annual revisions along with the January employment data. The BLS noted earlier these revisions are expected to reduce job growth by about 0.2% points lower than previously reported and private-sector payrolls will be 0.3% lower. The benchmark revisions reflect hard data through March 2023 but should also incorporate improved estimates for months since then, which should further reduce previously reported job growth.

Average hourly earnings rose a larger than expected 0.44% in December and finished the year 4.1% higher than in December 2022. Wages for production and supervisory workers rose 0.34% but are up an even larger 4.3% over the past year. Aggregate hours worked fell 0.2% in December and rose at just an 0.8% annual rate during Q4, which is consistent with our expectation for Q4 real GDP to rise at a 2% annual rate.

Nonfarm payrolls will likely be revised lower and more closely follow the household series.

The unemployment rate held steady at 3.7%, but the underlying data were unequivocally weak. Household employment dropped by 683k, offset by a 676k decline in the labor force. The labor force participation rate fell to 62.5%, reflecting declines in both men and women. Employment adjusted to the nonfarm employment methodology was even weaker, decreasing by 753k.

We expect nonfarm employment to be revised closer to the household series when the annual revisions are released next month. Despite the slower pace of job growth, we continue to believe the Fed will maintain a cautious approach to easing next year. We look for three quarter point cuts, most likely following the June, September, and December FOMC meetings.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.