Existing Home Sales Fall Further in September

- Existing home sales fell 2.0% in September to a 3.96-million-unit pace, a new cycle low.

- Sales have fallen 15.4% over the past year, while inventories are down 8.1%. Inventories remain tight at just a 3.4-month supply.

- Sales of existing single-family homes fell 1.9% in September, while sales of condominiums and co-ops fell 2.3%.

- Homes are taking slightly longer to sell, remaining on the market for 21 days, up from 20 days in August and 19 a year ago.

- The median price of an existing homes fell 2.4% in September, marking the third consecutive monthly drop. Prices remain up 2.8% year-to-year, however. Prices for single-family homes have risen 2.5% over the past year to $399,200, while prices for condos and co-ops rose 6.8% to $353,800.

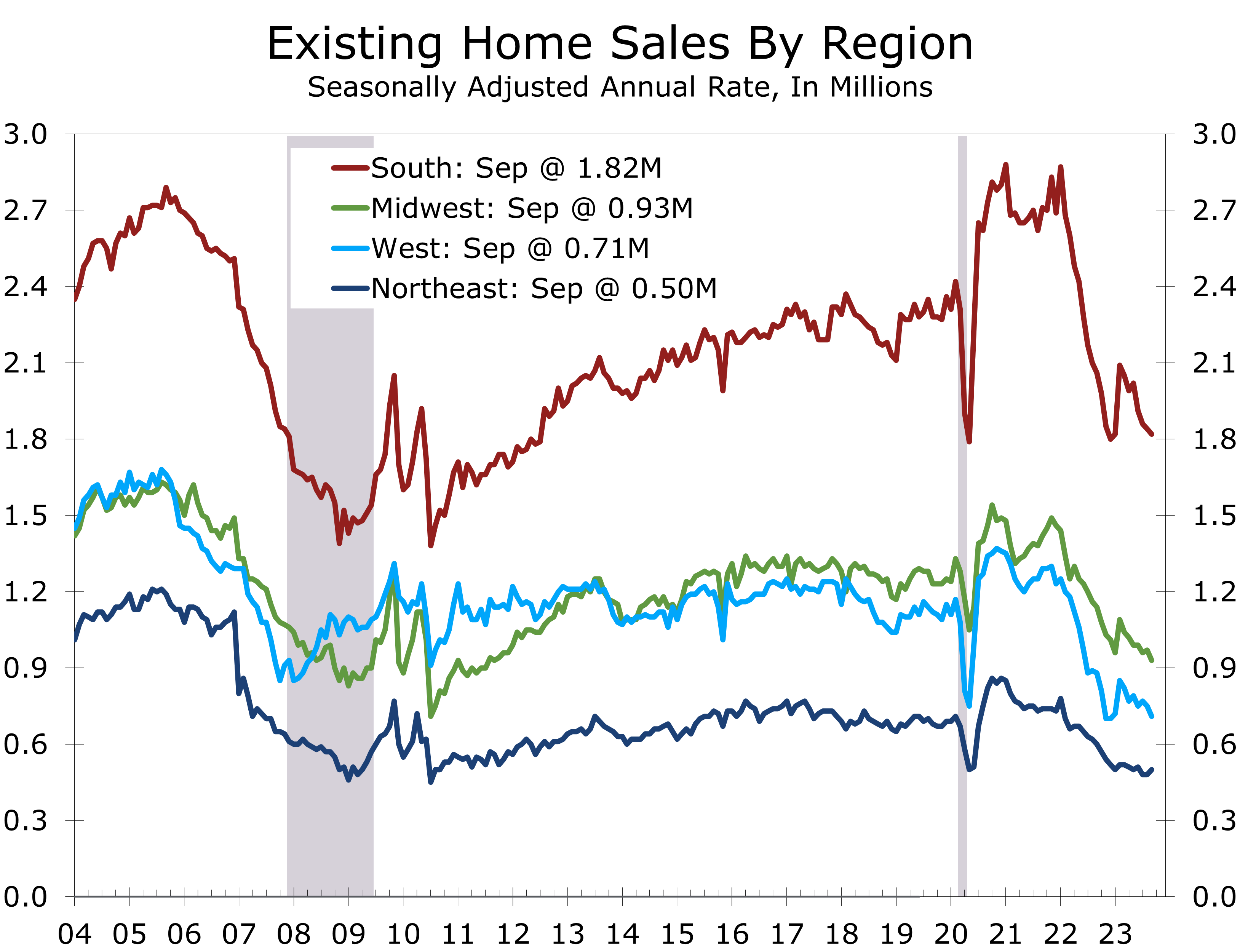

- Sales fell in every region but the Northeast, falling 5.3% in the West, 4.1% in the Midwest, and 1.1% in the South.

- The housing market remains the primary transmission mechanism for the Fed’s interest rate hikes. Sales of existing homes have now fallen to a new cycle low, which will have meaningful knock-on effects in 2024.

The housing market is one area where the Fed’s tightening monetary policy is making an impact. Sales of existing homes have fallen in 19 of the past 22 months, including a 2.0% drop in September. Sales are now running at their slowest pace since October 2010 and are 3.2% below their pandemic-era low hit when the economy was largely shut down.

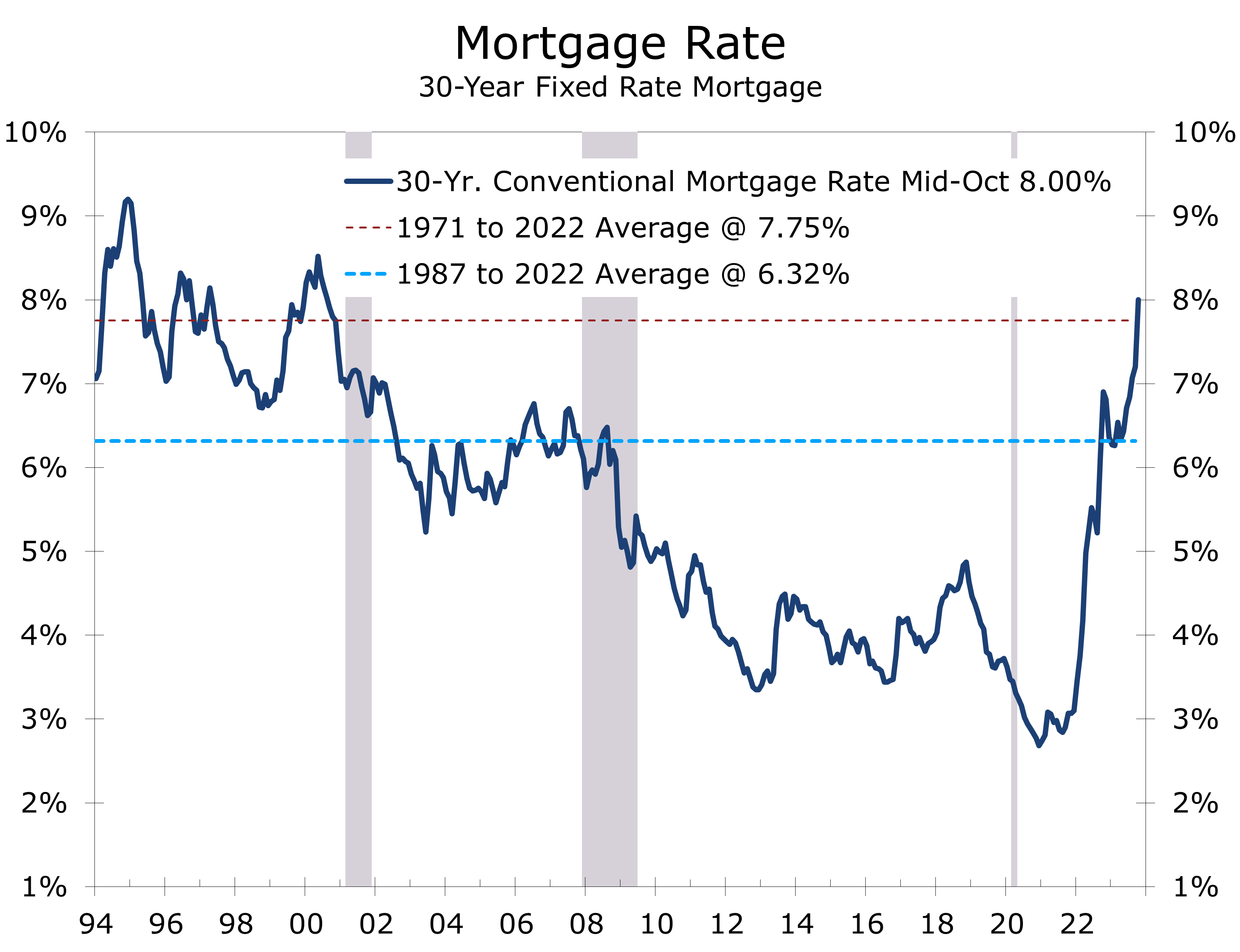

Existing home sales are being impacted by a myriad of headwinds. The most obvious is higher mortgage rates, which topped 8% this morning. The combination of higher interest rates and higher home prices have made housing much less affordable. As of August, a family earning the median income that purchased a home at the median price with a 20% down payment would need to devote a record 27.3% of their gross income to make the $2,234 monthly principal and interest payment. The long-term average is around 19%, or about $675 a month less.

Rising interest rates and higher home prices continue to sap housing affordability.

Ordinarily rising interest rates would set off a correction, with declining home sales slowing home price appreciation and leading to a broader economic deceleration. But with so many homeowners either owning their home outright (42% of homeowners) or having locked in generationally low mortgage rates (more than 80% of mortgages are fixed at less than 5%, and more than 60% or below 4%), homeowners are less impacted by rising interest rates than in the past.

At 8%, mortgage rates are now above their average for the past 50 years. If rates remain at this level, they will meaningfully cut further into existing home sales. Existing home sales reflect closings on contracts signed 1 to 2 months prior, which means homes closed in September were likely put under contract in July and August, when mortgage rates were closer to 7%.

Pending homes, which track purchase contracts, plunged 7.1% in August and are running 18.9% below their year ago level. The decline in pending home sales suggests existing home sales have further to fall. We expect existing home sales to fall 4.3% in the fourth quarter to a 3.8-million-unit pace and likely fall even further during the first half of 2024.

Housing is one of the primary transmission mechanisms for monetary policy to influence the broader economy. Falling home sales not only cut into commission income for realtors and mortgage lenders but also reduce knock-on effects from spending on home improvements, furniture, and home furnishings.

Further declines in home sales will have an impact but they will not be devastating by any means. Spending on home improvements and furniture have both weakened along with existing home sales and will likely slow even further in coming months. Home prices, however, are likely to remain resilient as even fewer homeowners are likely to put their homes up for sale.

The median price of an existing home fell 2.4% in September, marking the third consecutive monthly decline on a non-seasonally adjusted basis. The price of a single-family home fell 2.7%, while the price for condominiums and co-ops fell 0.1%. The recent declines are not unusual, as home prices usually decline in late summer and fall. Prices remain up 2.8% year-to-year and will likely remain up through the end of this year. Prices may dip slightly for a short period of time in 2024 but are unlikely to decline significantly as the supply of homes for sale will remain tight.

The National Association of Realtors also noted that the share of all-cash purchases rose to 29% of transactions in September, up from 27% in August and 22% in September 2022. Individual investors and second-home buyers, which typically account for the bulk of all-cash sales, accounted for 18% of home purchases in September, up from 16% in August and 15% last September.

The rise in all-cash purchases likely reflects the ongoing migration of home buyers from high cost housing markets in the West and Northeast to lower-price housing markets in the South and Midwest. Investors appear to be shying away from home purchases.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.