Sounder Footing on a Weakening Foundation

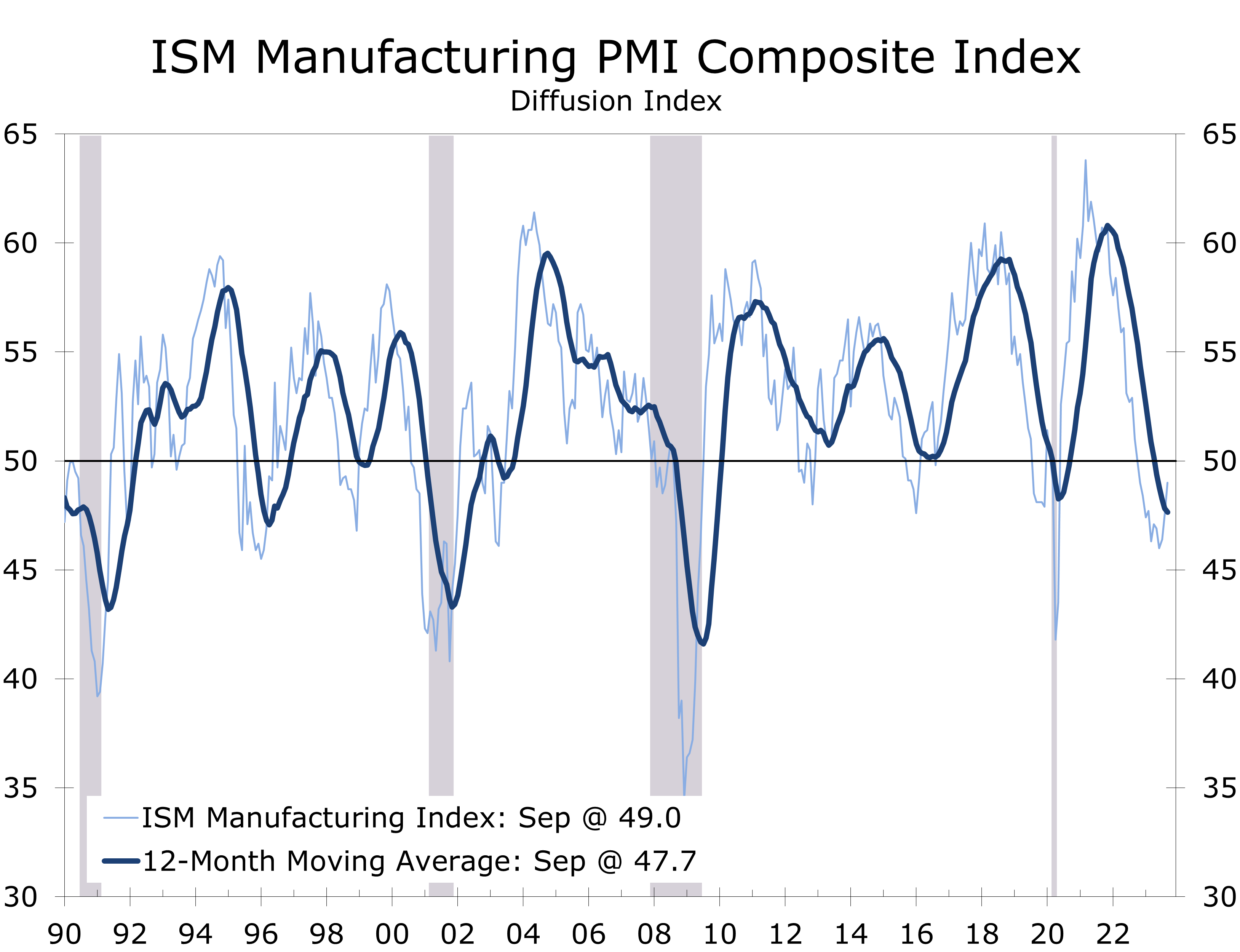

- The ISM Manufacturing Index rose 1.4 points in September to 49.0, marking the 11th consecutive month in contraction territory.

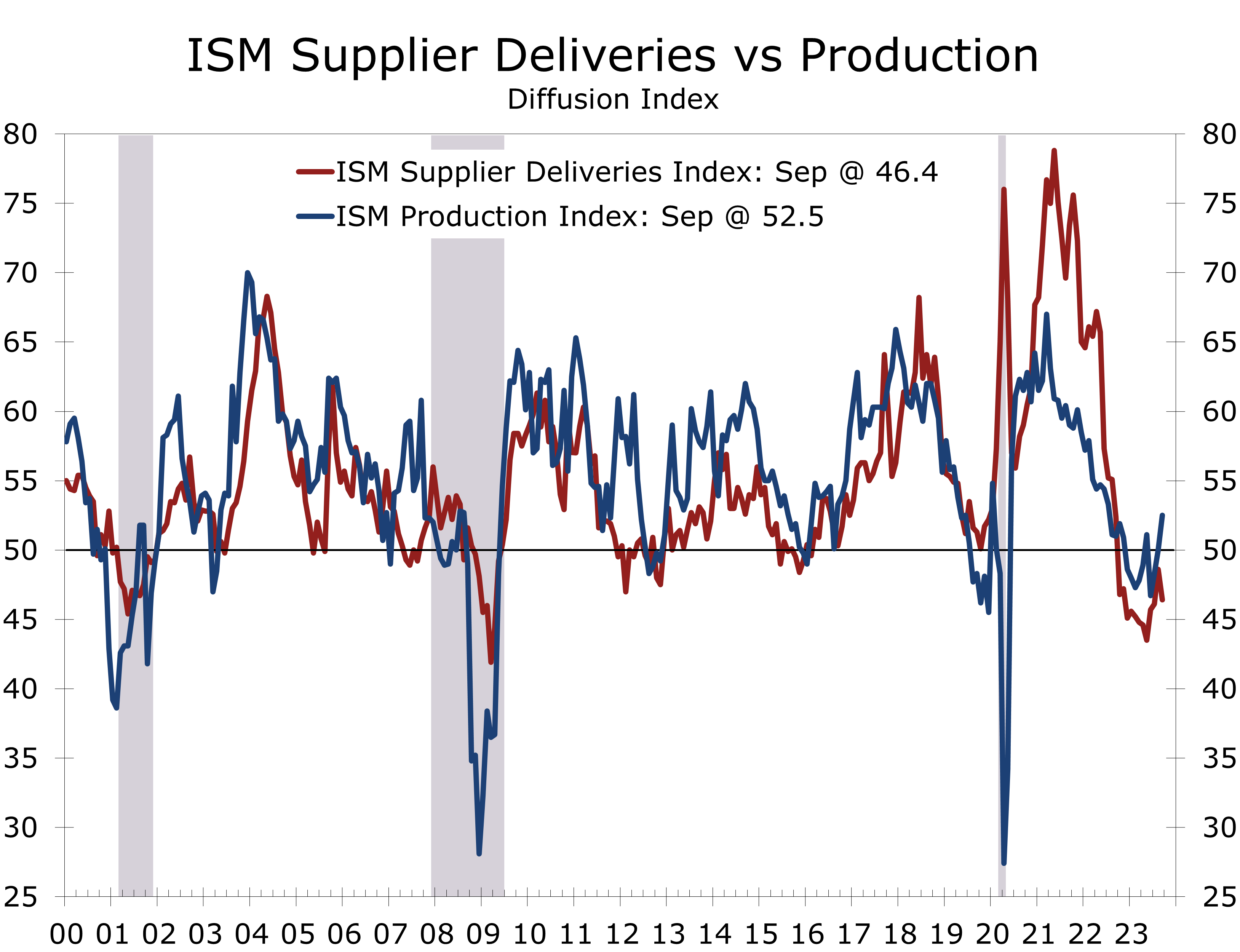

- Employment (+2.7 points), Production (+2.5) and New Orders (+2.4) all rose solidly in September, while Supplier Deliveries (-2.2) and Prices Paid (-4.6) fell sharply.

- With this past month’s increases, the Employment (51.2) and Production (52.5) series moved back into expansion territory.

- The sharp decline in the Prices paid index is surprising given the recent spike in oil prices and suggests inflationary pressures in goods are moderating.

- Customer inventories fell 1.6 points to 47.1, which is relatively low and might provide a near-term boost to orders and output.

- Export orders rose 0.9 points higher to 47.4, while Import orders crept 0.2 points higher to 48.2.

- September’s strong ISM report likely overstates the strength in the factory sector. While the manufacturing PMI rose, it remained below the 50 break-even level, which means the slowdown in the factory sector merely moderated, it did not reverse.

The ISM Manufacturing report is one of the key pieces of economic data released each month because it provides insight into the breadth of strength or weakness in the most cyclical part of the economy. The latest reading suggests the economy continues to expand, despite growing headwinds from rising interest rates, higher inflation, and labor unrest.

The Manufacturing PMI is derived from a survey of manufacturing purchasing and logistics managers that ask them about the state of their business. The index is derived from the net difference in the number of responses stating key aspects of their business are improving or weaking. A reading above 50 means more managers see conditions improving than seeing them weakening.

The Manufacturing PMI rose 1.4 points in September to 49.0, marking the 11th consecutive month the PMI has been below the key 50 breakeven level, signaling another month of contraction in the factory sector. This past month’s rise in the index means the pace at which manufacturing activity contracted at moderated in September.

September’s rise in the PMI means the contraction in manufacturing moderated.

With the latest increase, the monthly PMI is now back above its trailing 12-month average, which has typically signaled a turning point for the factory sector. The 12-month average peaked 22 months ago, as the economy came roaring back after the pandemic.

On the surface, the September ISM report is encouraging. Four of the 5 components that directly factor into computing the PMI improved in September, and two components rose back into positive territory. The Employment index rose 2.7 points to 51.2, reaching its highest level since May, while the Production index rose 2.5 points to 52.5.

The New Orders index rose 2.4 points but remained in contraction territory at 49.2, while the Inventories index rose 1.8 points to 45.8. The Supplier Deliveries index fell 2.2 points to 46.4. Taken together, these data suggest businesses have reduced inventories in order to conserve cash, which is what typically happens when short-term interest rates increase. The rise in orders also suggests output might see some additional improvement.

Businesses have reduced inventories in order to conserve cash as interest rates have risen.

We doubt September marks a major turn for the factory sector, however, as the improvement still remains fairly narrowly based. Only 5 industries reported improving conditions in September (Nonmetallic Mineral Products; Food, Beverage & Tobacco Products; Textile Mills; Primary Metals; and Petroleum and Coal Products), while 11 industries reported conditions continued to deteriorate.

We suspect some of the recent improvement in production and employment is coming from a further lessening of supply chain disruptions. The Supplier Deliveries and Production indices typically move together. The extreme difficulty in bringing supply chains back up following the pandemic caused delivery times to lengthen considerably and pulled the supplier delivery index to all-time highs. With supply chains less of a headwind, production is getting a slight boost.

The improvement in production and employment may not have much staying power. The unfilled orders index fell 1.7 points and remains exceptionally low at 42.4 on a monthly basis and the 12-month moving average is a smidgen below that at 42.3. The unfilled orders series is strongly correlated with employment, and the most recent reading suggest manufacturers will be paring payrolls in 2024.

The Prices Paid series tumbled 4.6 points in September to 43.8, despite sharp increases in energy prices. The list of products where prices are falling grew longer, led by aluminum, caustic soda, corrugated boxes, and ocean shipping rates. The list of commodities in short supply also grew shorter and continues to be led by electrical components and equipment.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.