Consumer Spending Outpaces Income in August

- Personal income rose 0.2% in July. Wages and salaries rose a more solid 0.4%. Proprietors’ income and rental income both rose solidly as well. Transfer receipts fell 0.6%.

- Consumer spending remained strong, however, climbing 0.8%, with solid broad-based gains.

- With spending outpacing income, the saving rate fell an eye-popping 0.8 percentage points to 3.5%.

- Both the PCE price index and core PCE deflator rose 0.2% in July.

- The overall PCE deflator is now up 3.3% over the past year, while the core is up 4.2%.

- Core services prices excluding housing rose 0.5% in July and remain up 4.7% over the past year, which is down only marginally from its peak of 7.9% hit in November 2021.

- After adjusting for inflation, consumer spending grew 0.6% in July, which gets the third quarter off to a strong start. Slower income growth, diminishing savings and sticky inflation point to a correction later this year.

July’s personal income and spending report ties together a number of loose ends from other economic indicators released earlier this month. The report is consistent with the soft landing narrative, as income growth continues to moderate. Headline inflation is also improving, but there are also signs that inflation remains sticky in many core categories.

Personal income rose just 0.2% in July, which was below expectations. The miss was largely due to a continuing slowdown in government transfer payments, which fell 0.6%. Most of that drop was in receipts of Medicaid benefits and ‘other’ benefits. Unemployment benefits also declined slightly, falling for the third consecutive month, while most other benefits categories, including Social Security and Veterans’ benefits posted modest gains.

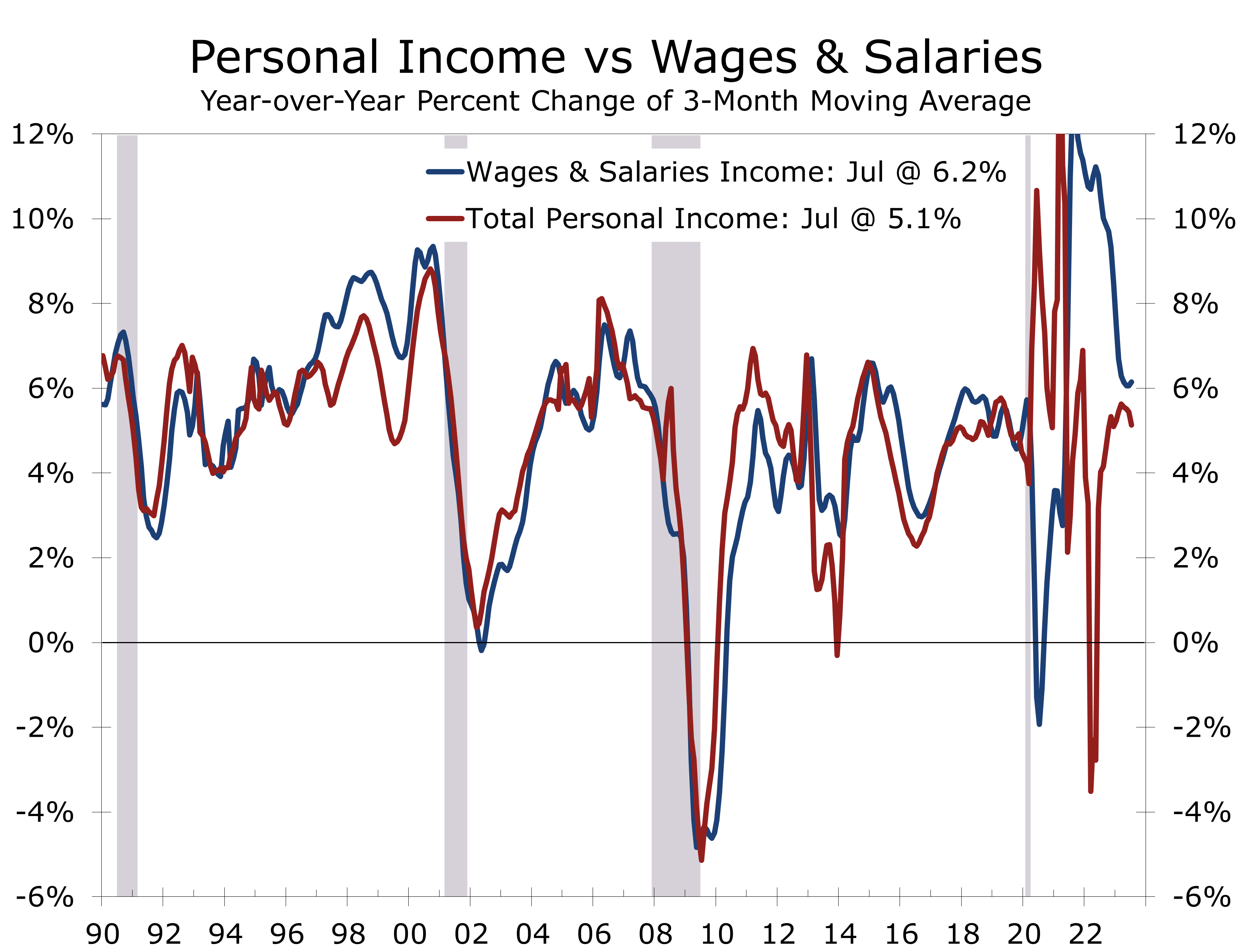

Wages and salaries rose 0.4%, which is in line with more modest job gains in recent months. Wages and salaries are growing fastest in the services sector and government. Manufacturing and transportation are seeing more modest gains, reflecting slower growth in the goods sector.

Over the long run, wages and salaries set the trend for consumer spending. Consumers have been making up for lost time in recent months, spending freely for travel and entertainment. That spending spree has helped drive the saving rate back down to 3.5%.

With much of consumers’ pandemic-era savings drawn down, spending will now more closely track wages and salaries, which remain up a respectable 6.2% over the past year. Even factoring in 4% inflation, real consumption should remain solidly positive, providing some cushion against a likely slowdown in job growth.

Nominal consumer spending rose 0.8% in July and growth for the prior month was revised 0.1 pp higher to 0.6%. After adjusting for inflation, real consumer spending rose 0.6% and has risen at a 2.8% annual rate over the past three months. Spending rose broadly, with outlays on durable goods rising 1.4% and outlays on nondurables climbing 0.7%. Services outlays rose 0.4%, the largest gain since March.

The strength in spending and the upward revision to the June data get the third quarter off to a strong start. With the increase, consumer spending is 0.9% above its second quarter average, which means real personal consumption, which accounts for more than two-thirds of GDP, would rise at a 3.6% pace if spending was unchanged through the rest of the quarter.

With July’s strong growth in consumer spending, the third quarter is off to a strong start.

We might see some payback in August. Spending in July was bolstered by record Amazon Prime Day sales and efforts by brick and mortar retailers to compete with them. Spending on travel and entertainment also saw exceptionally strong growth, with concerts and blockbuster movie weekends bolstering services outlays. Several retailers have noted softer back-to-school sales in August, which might produce an outsized impact after seasonal adjustment.

Even if there is some payback in August, the third quarter looks to be quite solid. We are now looking for consumer spending to rise at a 4% annual rate in the third quarter and see real GDP rising at around a 3.5% pace. Output and employment may also get a boost from ramped up auto production ahead of a possible strike this fall.

Strong third quarter GDP growth slightly lifts the odds the Fed will hike the federal funds rate another quarter percentage point but does not change the Fed’s narrative or timetable, which has them hiking rates at least one more time this year.

Disposable income, or after-tax income was unchanged in July. Tax payments rose 1.3%, nullifying the 0.2% in personal income. The difference between disposable income and consumer spending yields personal saving, which fell sharply in July, pulling the saving rate back down to 3.5%.

Consumers have likely exhausted much of their extra savings built up during the pandemic. This means spending will more closely track wage and salary growth, which will slow along with nonfarm employment growth later this year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.