Job Growth is Not So Hot After All

- June nonfarm payrolls rose 209,000 and job growth for the prior two months was revised lower by a total of 110,000 jobs.

- The softer employment print largely alleviates fears stoked by yesterday’s hyper-strong ADP report that hiring had accelerated.

- Job growth remains broad based but continues to be led by industries that have struggled to replace pandemic job losses.

- Government added 60,000 jobs in June, with all the gain coming at local governments (32K) and state governments (27K).

- Health care and social assistance (65.5K) is another area still striving to get back to their pre-pandemic trend.

- Manufacturers added 7,000 jobs in June, mostly in the automotive sector. Construction payrolls (23K) also rose solidly, led by continued strength in home building.

- The modest rise in June nonfarm payrolls helps reduce fears hiring had reaccelerated to the point the Fed would have to tighten even more aggressively.

June’s employment report poured cold water on the notion the job market was overheating. Nonfarm payrolls rose by just 209,000 in June and job growth for May and April were revised lower by a combined 110,000 jobs. Hiring remains broad based but shows some signs of softening in the goods sector.

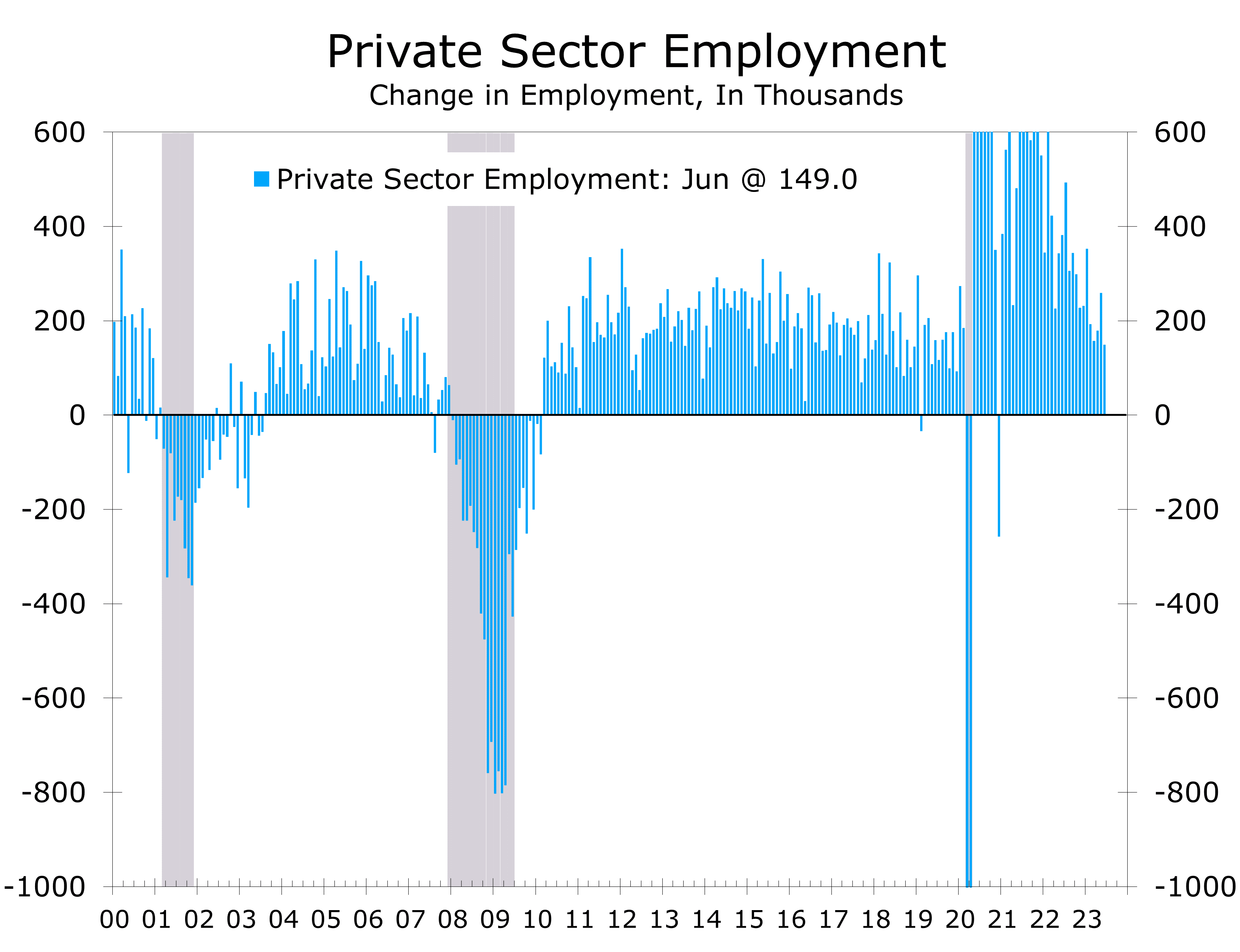

Market expectations had been stoked by yesterday’s blowout ADP employment report, which reported the private sector added 497,000 jobs in June. The ADP report is reasonably accurate over time but often deviates significantly on a month-to-month basis. Private payrolls in today’ BLS report rose by a much more modest 149,000 in June and have decelerated to a 1.8% annual rate over the past three months.

Job growth is now clearly decelerating. Overall payrolls have risen an average of 278,000 per month so far this year, down from 399,000 per month in 2022. Private payrolls have added just 215,000 jobs per month over the past six months (196.5K over the past three months), down from 376,500 in 2022. Moreover, the bulk of job gains continue to come from industries striving to rehire workers lost during the pandemic, particularly state and local governments, leisure and hospitality, and health care and social services.

Governments added 60,000 jobs in June, with the bulk of that gain occurring at state (27K) and local governments (32K). June’s gain was in line with recent months. Governments have added an average of 63,000 jobs a month so far this year, which is more than twice the 23,000 per month added in 2022. Government employment remains 161,000 jobs, or 0.7%, below its February 2020 pre-pandemic level.

Leisure and hospitality added 21,000 jobs in June. This marks the third month of diminished job growth in this sector, where hiring remains 369,000 jobs, or 2.2%, below its pre-pandemic level. Employment in retail trade (-11K), wholesale trade (-4K) and transportation and warehousing (-7K) was also noticeably soft. The weakness likely reflects less than usual summer hiring and some weakness in nondurable goods spending.

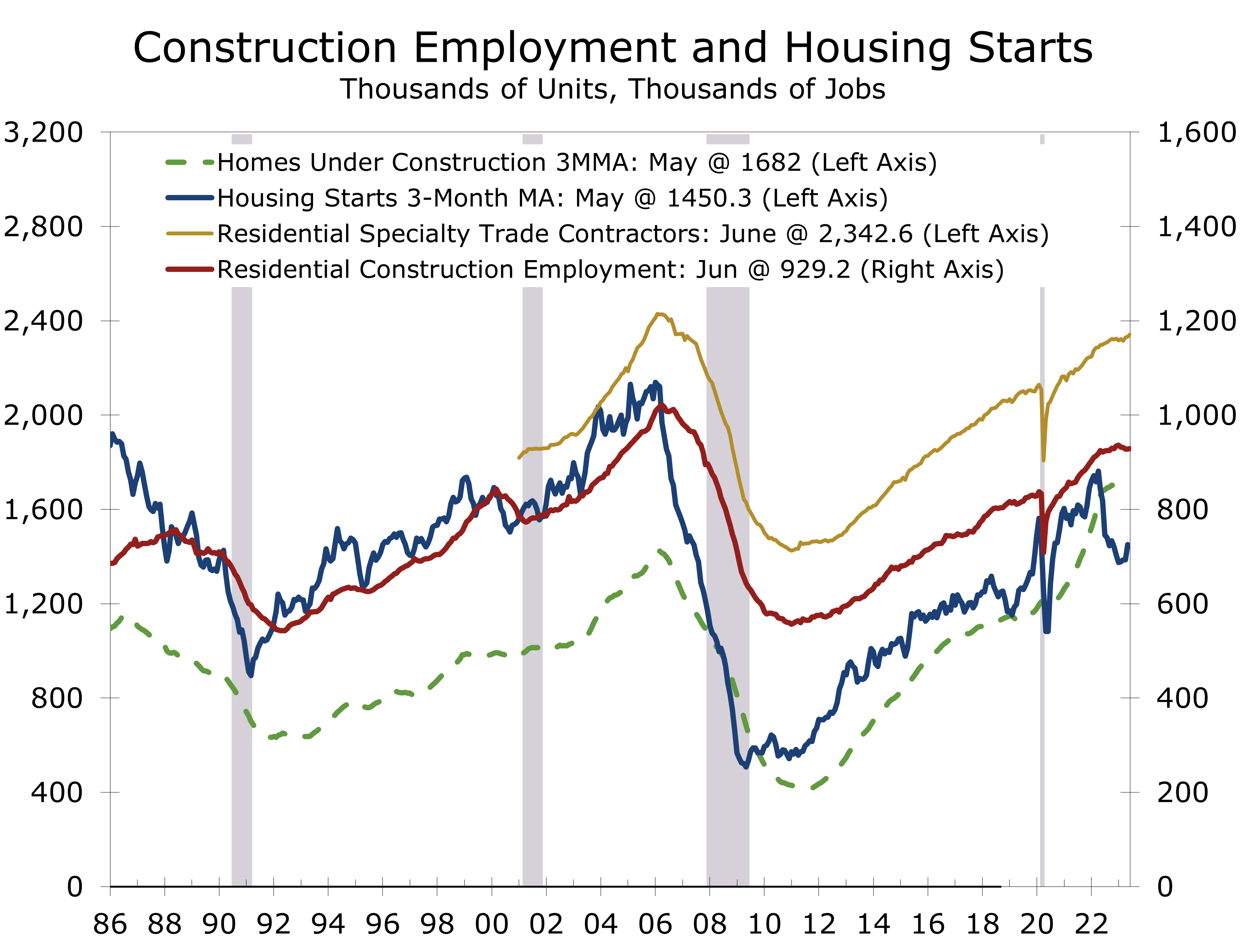

Manufacturing and construction employment held up reasonably well in June.

Manufacturing and construction employment, which is typically the most cyclical part of nonfarm employment, held up reasonably well in June. Manufacturers added 7,000 jobs and the factory workweek was unchanged at 40.1 hours. Durable goods producers added 15,000 jobs, with producers of transportation equipment accounting for nearly half of that gain. Nondurable goods producers cut 8 jobs.

Construction firms added 23,000 jobs in June. Much of that strength was in home building, with residential specialty trade contractors adding 10,000 jobs. The strength in specialty trade contractors is likely due to the unusually large number of homes that remain under construction. Housing starts have pulled back in recent months and are beginning to slow hiring in residential building construction.

Average hourly earnings for all employees on private payrolls rose 0.4% to $33.58. Average hourly earnings are up 4.4% over the past 12 months. Our income proxy shows wages and salaries rising a solid 0.55% in June and at a 4.4% annual rate in the second quarter.

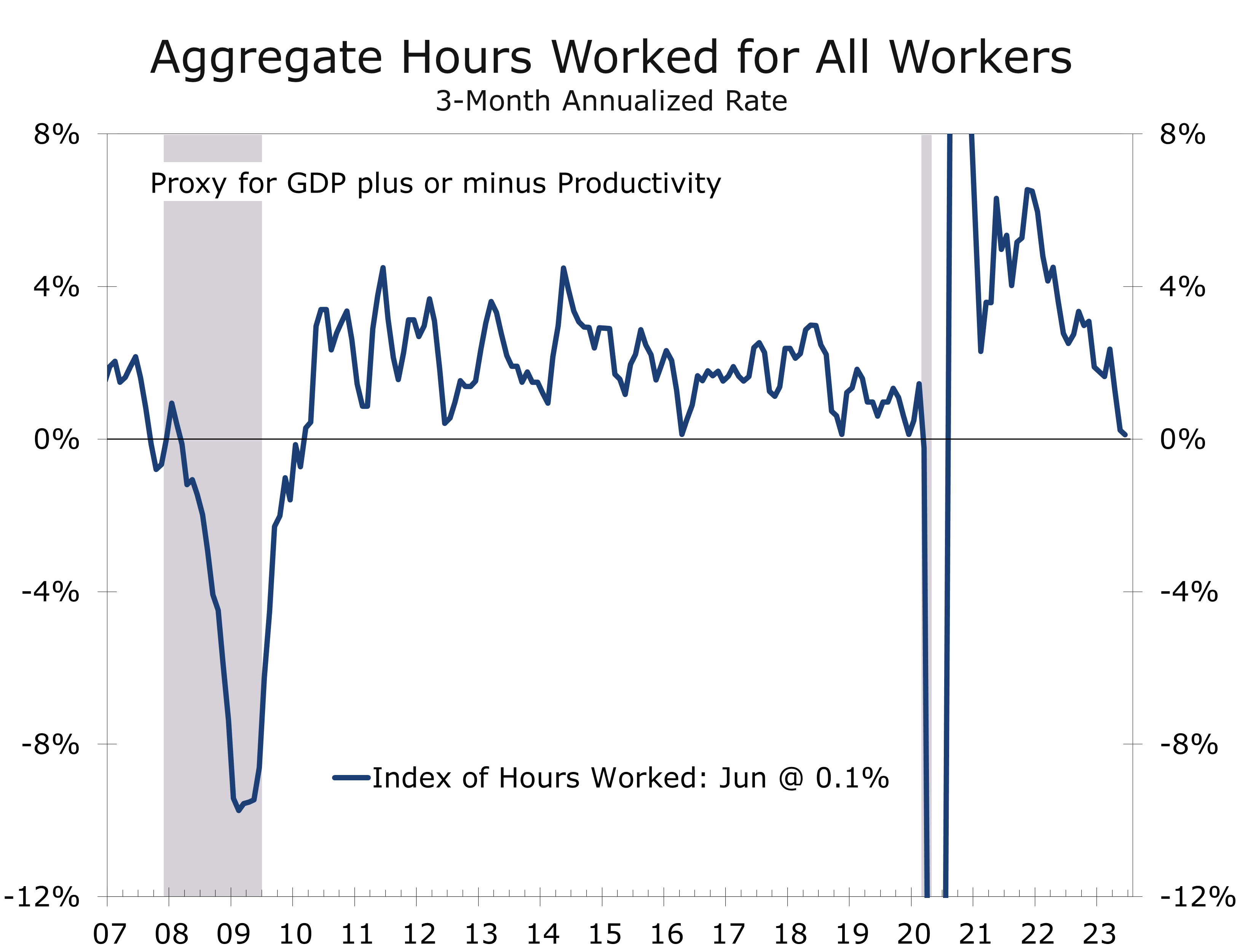

Hours worked improved substantially in June, with the average workweek for all employees edging 0.1 higher to 34.4 hours. Aggregate hours worked, which combines job growth and average weekly hours and is a good proxy for GDP growth, rebounded 0.4% in June, following a 0.1% drop the prior month. For the second quarter, however, aggregate hours worked rose at just a 0.1% annual rate. This means Q2 real GDP likely grew at the lower end of expectations (around 1.5% to 2%).

The unemployment rate inched 0.1 percentage point lower to 3.6%, as a rebound in self-employment helped lift household employment by 273,000, easily outpacing a 133,000 rise in the civilian labor force.

The June employment data are consistent with the Fed hiking its federal funds rate target by a quarter point at the July 26 FOMC meeting. Fears the Fed would have to do much more than that were overblown and will likely diminish further following next week’s CPI report. We look for the Fed to be on hold after July.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.