Manufacturing Activity Falls Again in June

- The ISM Manufacturing Index fell 0.9 percentage points to 46.0 in June, marking the 8th consecutive month of ‘contraction’.

- New orders were one of the few bright spots in June, rising 3 points to 45.6.

- Weakness in the factory sector appears to be broadening, however, with the 12-month moving average for every component now below the key 50 breakeven level.

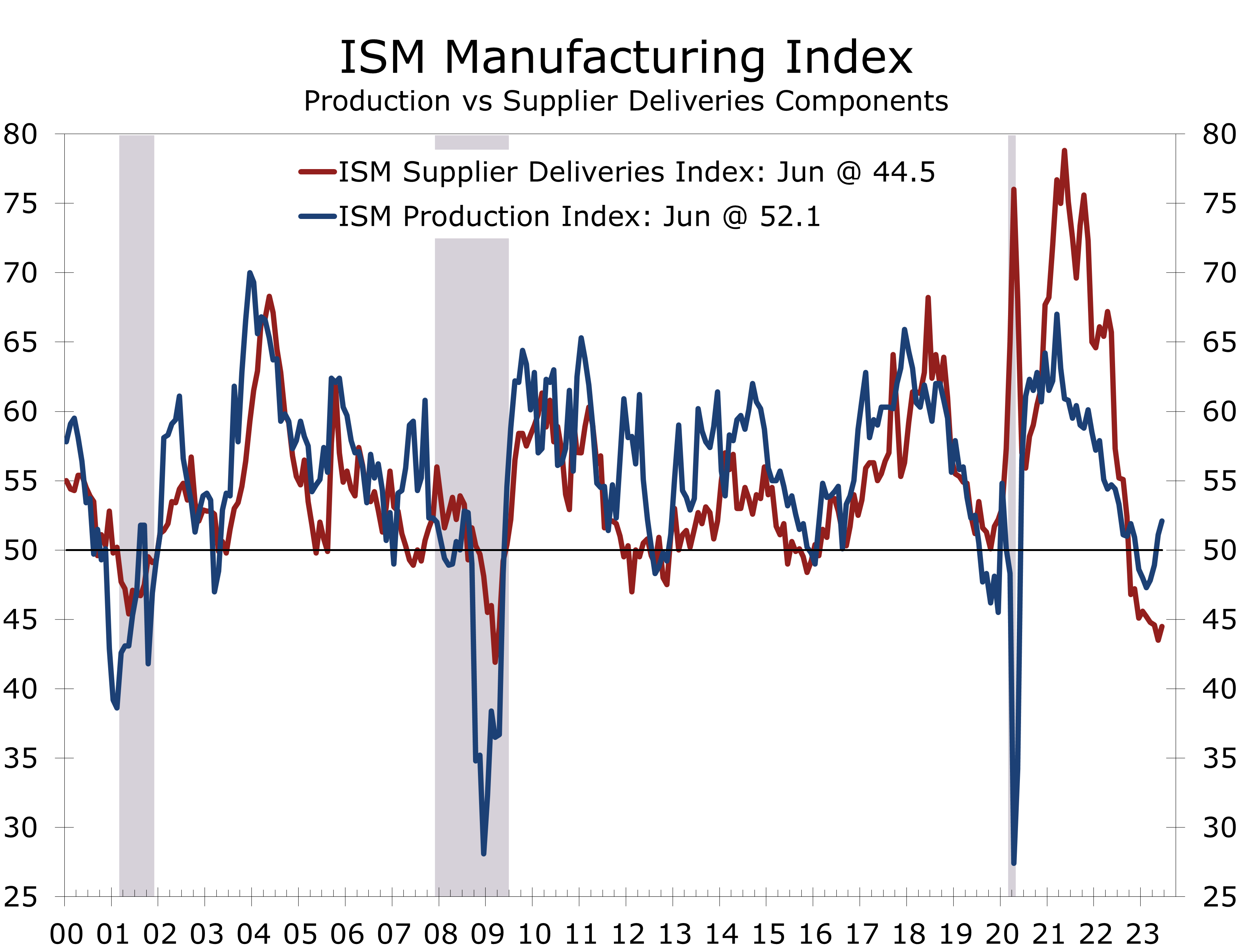

- Supply chains continue to normalize, with more manufacturers reporting quicker deliveries and fewer reporting shortages.

- Demand appears to be flagging, however, particularly overseas. The new export orders index fell 2.7 points to 47.3.

- The ongoing normalization of supply chains has likely exaggerated the slowdown in the ISM manufacturing index. Supplier deliveries have swung back from extreme highs, which has weighed on the overall index. With fewer shortages, production and employment have been bolstered.

The Institute for Supply Management (ISM) manufacturing index fell 0.9 points to 46.0 in June. The underlying composition was mixed, with new orders rising 3.0 points to 45.6, but the production index falling 4.4 points to 46.7. The employment index also fell sharply, declining 3.3 points to 48.1.

The ISM report is a diffusion index that reports on the breadth of the strength or weakness in the factory sector. A reading below 50 means more manufacturers report deteriorating conditions as opposed to improving conditions. The June reading marks the 8th consecutive month the overall index has been below the key 50 breakeven level, signaling contraction.

All 5 of the subindices that directly factor into the ISM Manufacturing index are now in contraction territory and many have been for quite some time. The latest 12-month moving average for the overall index is now at 48.8, marking its second month below 50. The 12-month moving average for the new orders index, which is the most leading element of the report, has been below 50 for the past 5 months, although it did rise 3 points in June to 45.6. The 12-month moving average for the backlog of unfilled orders series has also been below 50 for the past 5 months, while the 12-month moving average for the employment index has been below 50 for the past 4 months.

While manufacturing represents a smaller portion of the economy today, the factory sector still provides the bulk of the cyclical impulse to the broader economy and largely drives the ups and downs of the business cycle. According to the ISM, June’s 46.0 level is consistent with a 1.0% decline in real GDP.

The demarcation line between recession and growth is more complicated today due to the ongoing return to pre-pandemic norms. Supply shortages, most notably for microchips, slowed production of light vehicles and certain other durables as the economy reopened.

The return to pre-pandemic norm supply chains has exaggerated the swing in the ISM index.

Shortages have greatly diminished this past year, as can be seen by the long slide in the supplier delivery component. With fewer shortages, production has been surprisingly resilient. The June data show a bit of a reversal from that trend, with the production index tumbling 4.4 points after rising 2.2 points in May. With the drop, the 12-month moving average for the production index dipped into contraction territory for the first time since September 2020.

Supply chains are still normalizing. The supplier delivery index rose slightly in June, climbing 2.2 points to 45.7. While the index rose, more manufacturers are still reporting faster delivery times, which suggests there are fewer shortages and supply-chain bottlenecks. The lead time for production materials edged lower by 1 day in June to 83 days. That is still relatively high, however. The lead time for production materials averaged 64 days just prior to the pandemic and just 51 days back to the series start in 1988.

The normalization of supply chains should help curb inflation. The ISM prices paid index fell 2.4 points in June to 41.8, indicating more firms report paying lower prices for key inputs. Lower prices for oil and natural gas are playing a big role in delivering price relief, both directly through lower fuel costs and indirectly through lower prices for plastics, resins, and shipping.

The closely watched ISM employment index fell 3.3 points in June to 48.1, returning to contraction territory after two months of being above 50. Only 6 of the 18 manufacturing industries surveyed boosted hiring in June, led by printing, furniture, fabricated metals, and transportation equipment.

The ISM noted employer sentiment has shifted such that layoffs are now more prominent. That shift is apparent in the data. The 12-month moving average for the employment index has dipped to 49.9, which is consistent with a decline in manufacturing payrolls.

We expect the factory sector to lose momentum in the second half of this year. Production of transportation equipment and building materials will provide some much needed buoyancy, however, as demand for other consumer goods and exports sags a bit further.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.