Job Growth Continues to Baffle Wall Street

- Employers added 339,000 jobs in May, easily outpacing the consensus forecast of 190,000. The whisper number was even lower.

- Job growth for the prior two months was also revised higher by a combined 93,000 jobs.

- Job gains were broad based, with nearly every key industry adding jobs in May.

- Health care and social assistance was the top gainer, adding 74,600 jobs.

- Business and professional services added 64,000 jobs, with particularly strong gains in professional, scientific, and technical services.

- Construction added 25,000 jobs, while manufacturing lost 2,000.

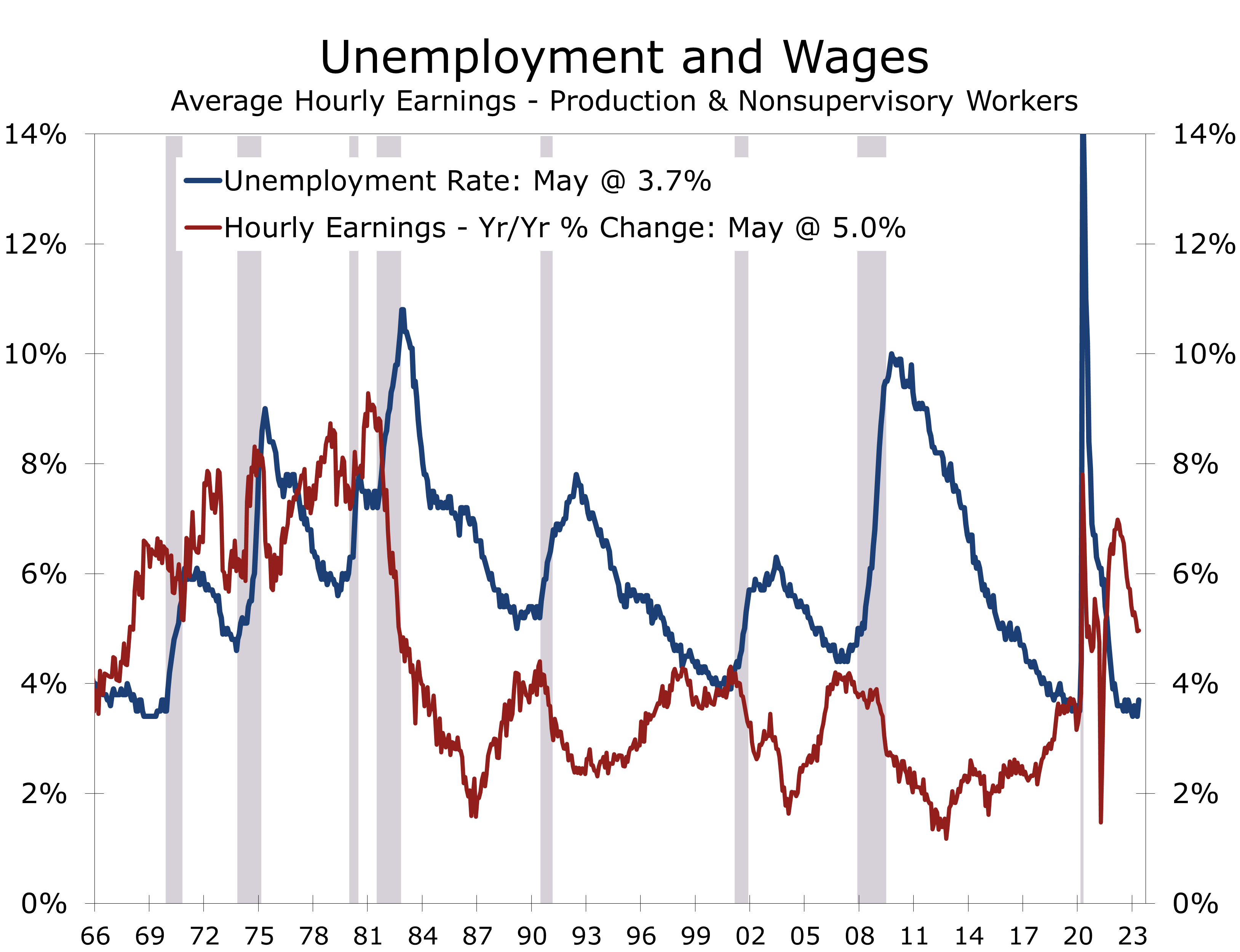

- The unemployment rate jumped 0.3 percentage points to 3.7%, as the household employment measure fell by 310,000 jobs.

- Bottom line: Job growth is still way too strong for the Fed to end its tightening regimen. While a pause is likely, May’s outsized job gains and upward revisions to prior data puts a quarter-point hike in June back on the table.

Employers added 339,000 jobs to nonfarm payrolls in May, easily blowing past the consensus estimate of 190,000 jobs. Gains for the prior two months were revised up by a combined 93,000 jobs, which weakens the argument that growth had cooled off enough for the Fed to either take a break from rate hikes in June or end them entirely. The more volatile household data were weak, however, with the number of employed declining by 310,000 in May. Reconciling the data to make them consistent with the nonfarm data, however, yields an even larger gain of 394,000 jobs in May.

While the net number of jobs added was stronger than expected, hours and earnings were soft. Average weekly hours fell 0.1 to 34.3 hours. Average hourly earnings rose just 0.3% and average weekly earnings were essentially flat. The factory workweek was unchanged at 40.1 hours, although overtime rose 0.1 to 3.0 hours. Hours and earnings for production and non-supervisory workers was a touch stronger, however, so industrial production and wages and salaries should remain modestly positive.

GDP growth will likely continue to lag job growth, reflecting sluggish productivity gains.

While the jobs figures throw more cold water on the notion the economy is on the precipice of recession, second quarter GDP growth still looks to be fairly sluggish. Aggregate hours worked have fallen in 2 of the past 3 months and are rising at just a 1.2% pace from their first quarter average.

After adjusting the household employment data so they are consistent with the nonfarm data, both show remarkably strong gains in May and the past 3 months.

Not only was job growth stronger than expected in May but gains continue to be exceptionally broad based. The largest gains continue to come from industries that have had the most trouble staffing back up following the pandemic. Health care and social assistance added 74,600 jobs in May, with strong gains at doctors’ and dentists’ offices and hospitals. The gains reflect some catchup with patients that had put off visits to the doctor during the pandemic. Nursing homes and childcare centers also continue to restaff, adding back a combined 12,500 jobs.

Leisure and hospitality continue to add jobs back at a rapid clip. Restaurants, bars, and hotels added 34,400 jobs in May and arts, sports and entertainment venues added 13,700 jobs. Even after May’s gains, leisure and hospitality employment remains 2.1%, or 349,000 jobs below its pre-pandemic level.

One of the bigger surprises this month was the outsized gains in professional and business services, which added 64,000 jobs in May, following a similar sized gain the prior month. Professional, scientific and technical services added 43,000 jobs with accounting firms and technology consultants posting strong gains.

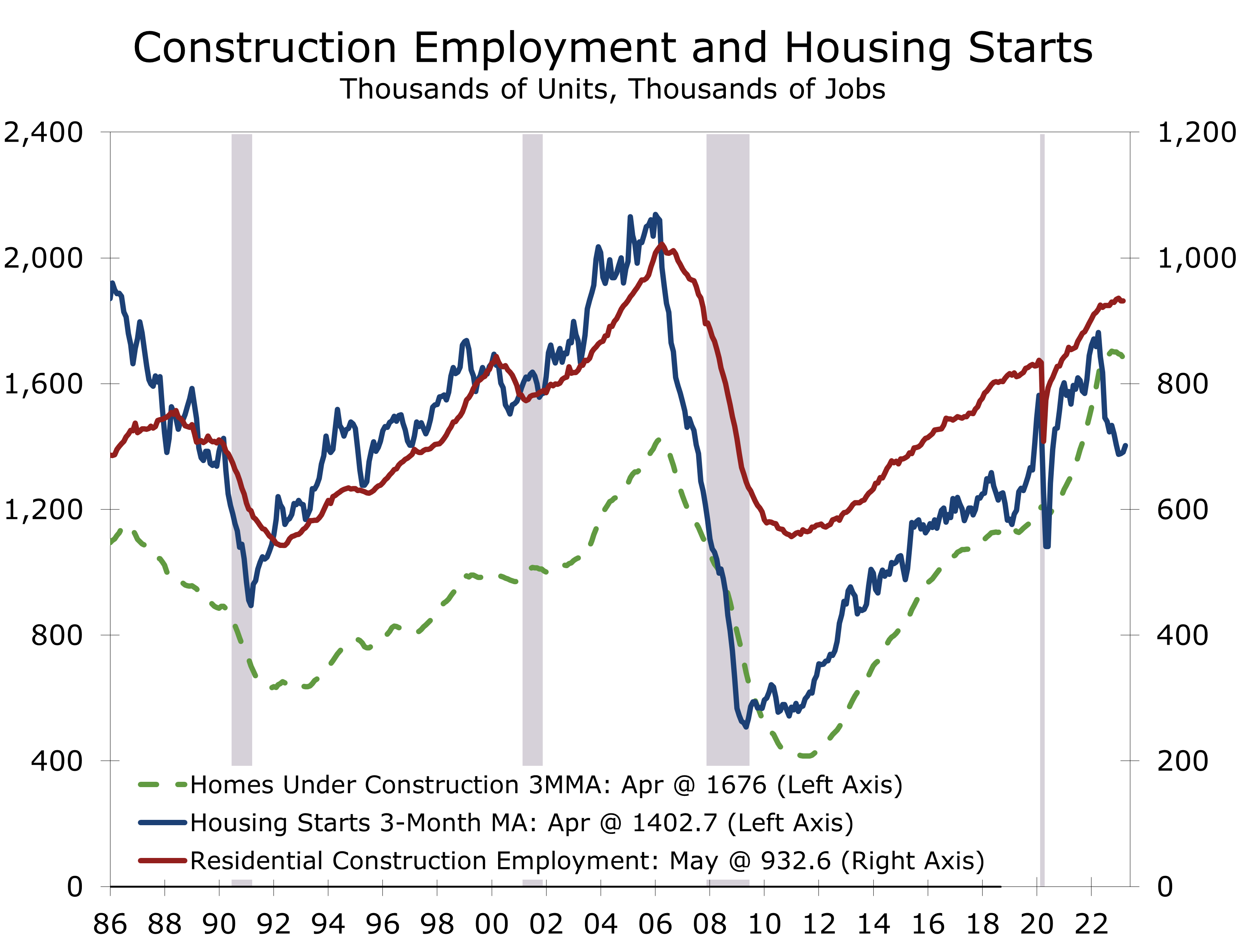

Construction remains a bright spot, with a net 25,000 jobs added in May. The growth reflects the unusually large number of homes and apartments currently under construction. Industry payrolls will likely soften a bit later this year, as more homes are completed.

The divergence between the strong employment gains and weak hours data is a red flag that something may be amiss in the employment data. Average weekly hours are usually a leading indicator for job growth and the recent weakness suggests hiring will slow or may be overstated. One area where we could see some payback is private and public education. The May and June data often see wide swings in such jobs due to the timing of the end of the school year, which varies from year to year. Private education added 22,300 jobs in May, while public schools added 24,300 jobs.

Of course, the other red flag is the 0.3 percentage point rise in the unemployment rate to 3.7%. The rise results from a 310,000 drop in household employment and a 130,000-person rise in the labor force. As noted earlier, however, household employment rose 394,000 after adjusting the data to be consistent with the nonfarm employment measure, with a suspiciously large drop in self-employment accounting for the difference.

The rise in the unemployment rate is due to a sharp, and dubious, drop in self-employment.

A 0.3 percentage point rise in the unemployment rate is still significant, however, and is consistent with the deterioration noted earlier this week in the job outlook components of the Consumer Confidence survey.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.