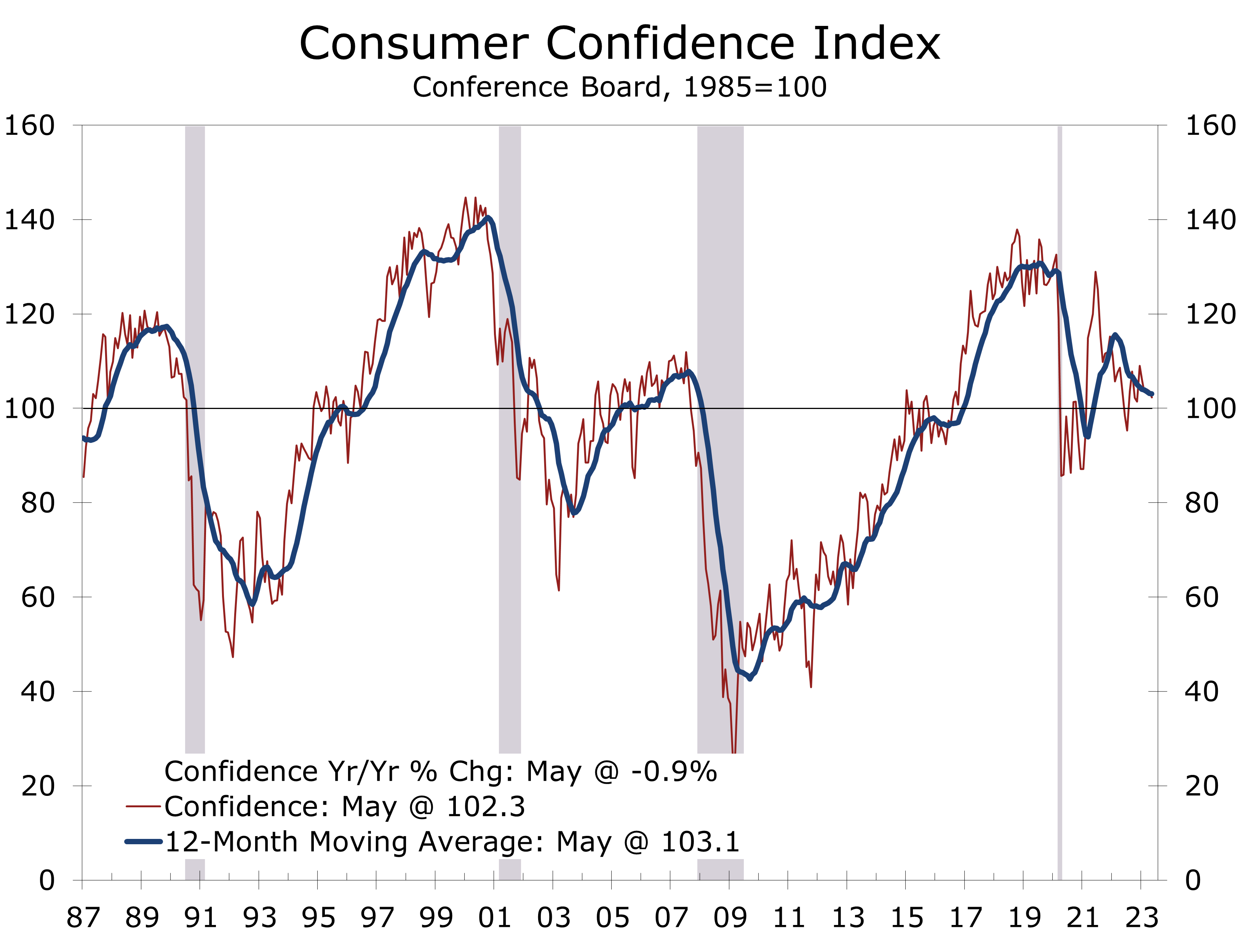

Consumer Confidence Remains at Levels Consistent with Continued Economic Gains

- The Consumer Confidence Index fell 1.4 points in May to 102.3. Data for April were revised higher, so the Index still came in higher than expected despite the drop.

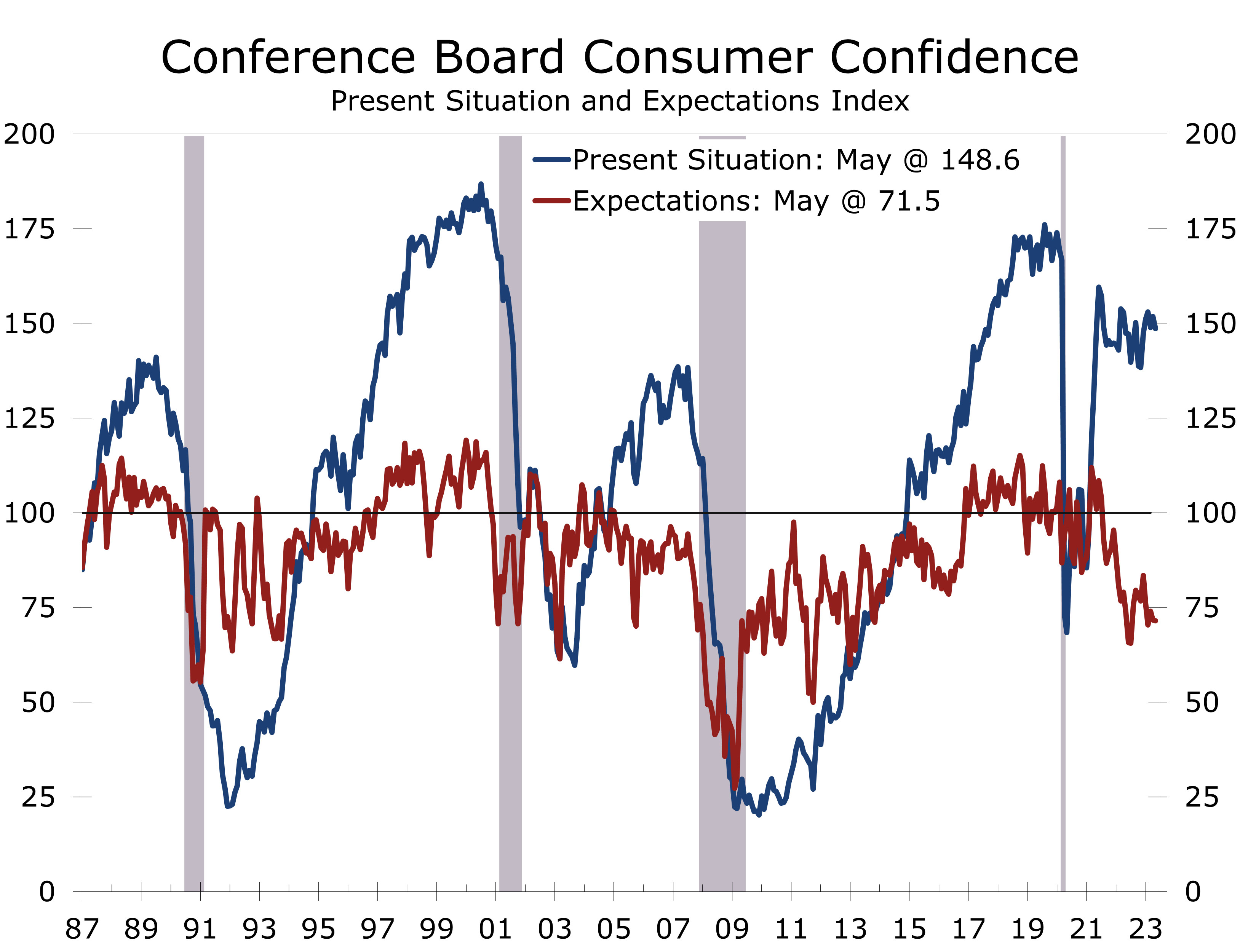

- The present situation series fell 3.2 points to 148.6 but remains consistent with strong economic growth.

- The expectations index fell 0.2 points to 71.5 and remains at levels consistent with a recession beginning within the next year.

- The share of consumers reporting jobs were plentiful fell 4 points in May to 43.5%, while the share stating jobs were hard to get rose 1.9 points to 12.5%.

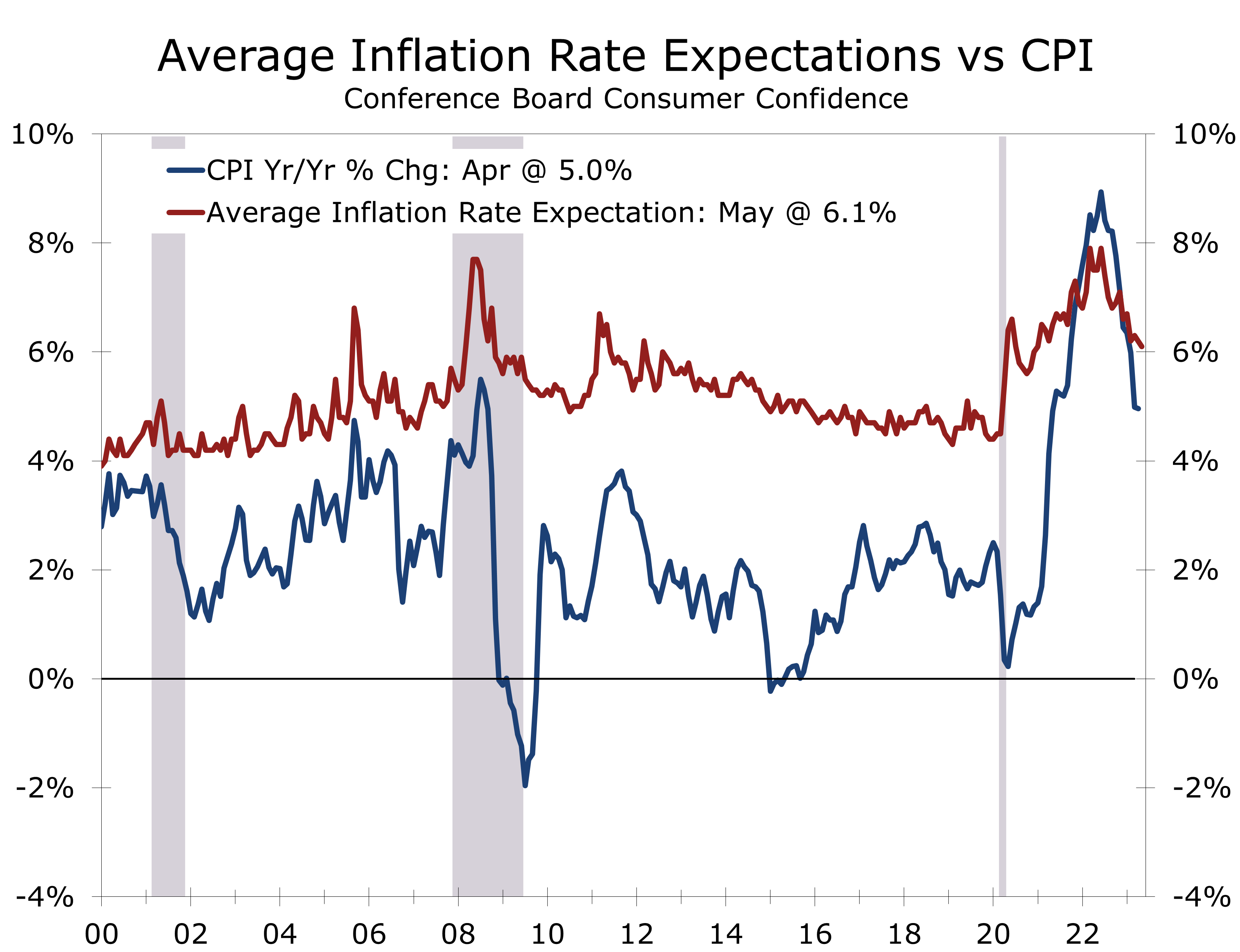

- Consumers expect inflation to average 6.1% over the next year, down slightly from 6.2%.

- Plans to buy major appliances edged higher in May, while plans to buy a home remained unchanged.

The Consumer Confidence Index fell 1.4 points in May to 102.3, marking the fourth drop in the past five months. Data for the prior month were revised higher, so Consumer Confidence remains at a relatively high level even at the latest drop.

As with many other economic indicators, Consumer Confidence provides widely divergent views on the state of the economy. The overall index remains slightly above its 1985 base year average and is consistent with solid economic growth. The present situation index fell 3.2 points to 148.6 and remains at a relatively high level. The expectations index, however, fell 0.2 points to 71.5 and has been below 80 every month since February 2022, except December. A reading below 80 has typically presaged a recession beginning within the next year.

The deterioration in expectations closely follows the period when the Fed began raising short-term interest rates. That period has been associated with heightened stock market volatility and a moderation in job growth and job openings. The unemployment rate has fallen slightly over this period, however, declining to 3.4% in April, slightly below its pre-pandemic low.

Consumer Confidence closely tracks employment conditions, which have so far remained resilient.

The Conference Board’s Consumer Confidence Index is much higher than the University of Michigan’s Consumer Sentiment Index, which has been at recession levels for much of the past year. The Conference Board survey puts more weight on still buoyant employment conditions, while the Michigan survey more closely tracks consumer finances and the financial markets, which have both been under stress.

Consumers’ assessment of current economic conditions weakened somewhat in May. The drop appears to have been tied to softening labor market conditions. The share of consumers stating ‘jobs were plentiful’ tumbled 4 points in May to 43.5%, marking the largest 1-month drop since October of last year. The jobs plentiful series peaked in March of last year at 56.7% and has fallen a cumulative 13.5 points since then, which is when the Fed began hiking rates.

The share of consumers stating ‘jobs were hard to get’ rose 1.9 points in May to 12.5%. This series bottomed out in March of last year at 9.5%. The labor market differential takes the difference of these two series and fell 5.9 points to 31, which is the lowest it has been since April 2021. This series has been a good predictor of changes in the unemployment rates. The deterioration in the labor market differential by itself is consistent with a 0.2 rise in the unemployment rate.

Consumers’ assessment of current conditions might have been influenced by the run-up in concerns about the nation’s debt ceiling. The survey was completed 3 days prior to the apparent agreement. Even with May’s 3.2-point drop, the present situation index remains above its 12-month average. The share of consumers’ rating current business conditions as “good” rose 0.6 points to 19.6% in May, and the share rating current conditions “bad” falling 1.1 points to 17% – lower than at any time since before the pandemic.

The expectations series is clearly the more problematic subset of consumer confidence. Expectations have averaged 74.9 since February 2022, consistent with a recession beginning in the next year. The series is derived from questions about business conditions, employment, and income six months from now.

The share of consumers expecting business conditions to improve over the next 6 months fell 1.2 points in May to 12.9%, but the share expecting condition to worsen also fell 0.8-points to 20.6%. Views about the availability of jobs six months out saw similar declines, with the share expecting more jobs to be available falling 0.7-points to 13.6% and the share expecting fewer jobs to be created falling 0.9-points to 20.2%.

Expectations for the labor market and inflation are moderating.

The moderation in expectations for the job market and inflation is exactly what the Fed is looking for. The question is whether it is enough to justify a pause in rate hikes? The Fed will need to see solid evidence that the pullback in expectations is matched by a further moderation in hiring and inflation, which they should have a better idea of before their mid-June meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.