A Hawkish Pause – If That

- As was widely expected, the FOMC raised their federal funds rate target a quarter percentage point to between 5% and 5.25%.

- The Fed dropped the sentence in its policy statement noting “additional policy firming may be appropriate” and replaced it with a slightly less dovish statement that leaves them room leave rates unchanged in June or raise them if conditions warrant.

- The flexibility written into the policy statement is purposeful, as employment and inflation may both surprise to the upside between now and the June 13-14 FOMC meeting.

- The Fed noted the “U.S. Banking system is sound and resilient”, a point reiterated at the start of Powell’s press conference.

- Powell also stressed that price stability is the key policy objective for the Fed right now, particularly given the ongoing strength of the labor market. The prominent placing of this statement is likely a response to the unusually public criticism of the Fed from elected officials.

As was widely expected, the Federal Reserve raised its federal funds rate target by a quarter percentage point to between 5% and 5 1/4%. The policy statement released following the meeting was a bit more hawkish than the markets had expected. We see the likelihood of another quarter point hike in mid-June at just slightly better than 50%.

Market participants had expected the Fed to announce it would take a break from hiking interest rates following the May FOMC meeting. While the Fed may still pause in June, the policy statement left them plenty of wiggle room to push forward with hiking rates further in mid-June. The Fed may very well need that wiggle room if the employment data continue to come in strong and the recent moderation in inflation slows or possibly even reverse a bit. The Fed will see two more employment reports and two more CPI reports before their June 13-14 meeting.

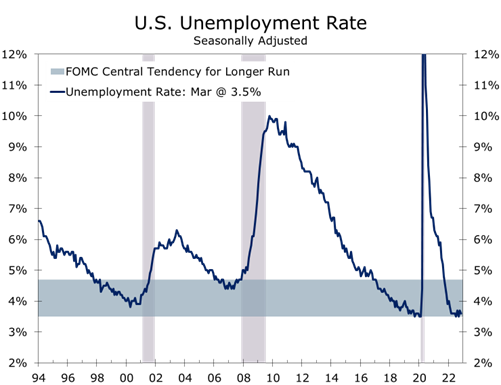

Employment conditions still remain too strong for the Fed to end their policy tightening.

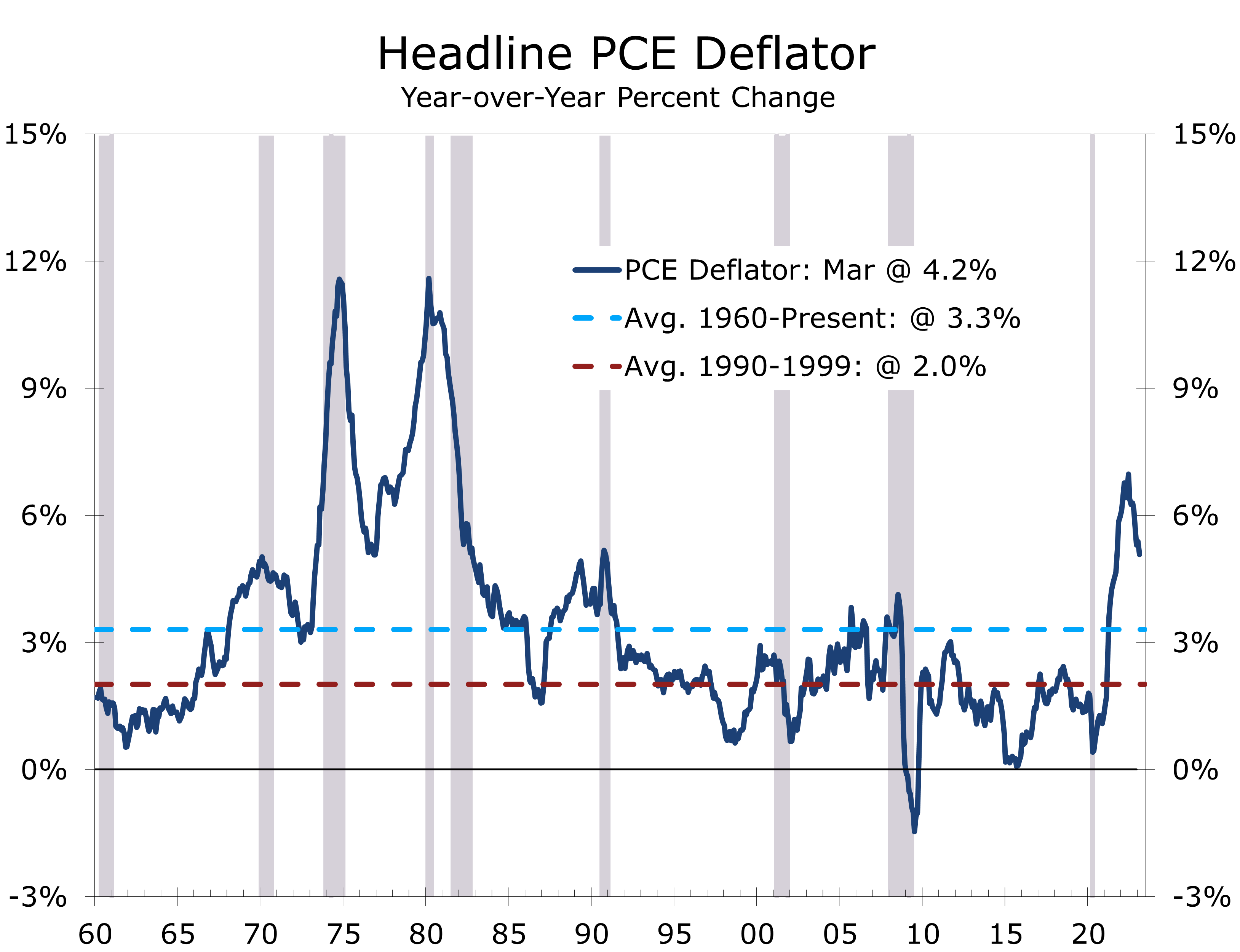

The Fed is aware of the pointed criticism it is seeing from elected officials, academics, and private prognosticators. The Fed also has a rich history to draw upon which shows the best way to meet their dual mandate over the long-term is to maintain price stability and to make certain long-term inflation expectations remain anchored around their 2% target. Employment conditions are currently at the lower bound of the Fed’s long-run target, while inflation is running more than 2 times higher than target.

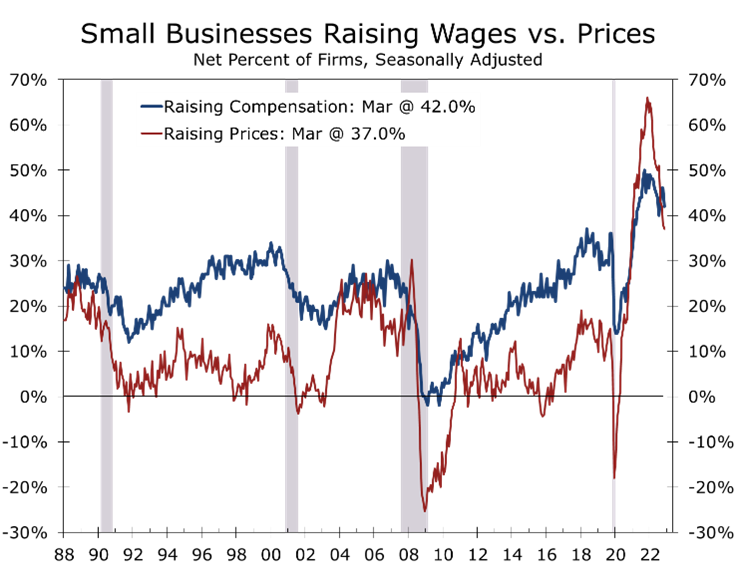

We expected the Fed to keep its options open for its June FOMC meeting after hiking rates in May. Recent evidence on wages suggest bringing inflation back to the Fed’s 2% target will take longer and be more difficult. The Employment Cost Index for the first quarter came in above expectations and survey data on wages show wage growth will likely remain well above levels consistent with bringing inflation back down to 2%.

Strategically, it is too early for the Fed to commit to a pause. The financial markets are already on edge due to the failure of Silicon Valley Bank, Signature Bank and First Republic, as well as continued struggles at some West Coast regional banks and specialty lenders. If the FOMC had signaled a pause and then had to reverse course because the jobs and inflation data came in much hotter than expected, then the volatility that would then be unleased would risk further damage to both the economy and banking system.

Powell cited the recent troubles in the banking system at the start of his press conference and noted conditions in the banking system had improved since the resolution of recent bank failures. He then shifted into a forceful explanation of the Fed’s dual mandate. The tone of Powell’s comments and the bulk of recent economic data suggest it is still too early for the Fed to declare victory.

The change to the policy statement receiving the most attention was the shift in the FOMC’s view on how they will determine what to do next. The statement “The Committee anticipates that some addition policy firming may be appropriate” was changed to “In determining the extent to which additional policy firming may be appropriate” This clearly implies the Fed is keeping their options open.

The Fed also dropped language in the second part of that sentence (following the word appropriate) “… in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.” This change raises the possibility the federal funds rate is now at a neutral level and is critical because if the Fed does pause in June, they do not want to raise concerns they are pulling in their horns too soon.

We expect the upcoming jobs and inflation data to be consistent with another quarter point hike.

We have consistently been more concerned about inflation and continue to believe the Fed has more work to do. We expect the jobs and inflation data to be consistent with another quarter point rate hike in June and expect the recent banking turmoil to subside.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.