Manufacturing Continues to Show Resilience

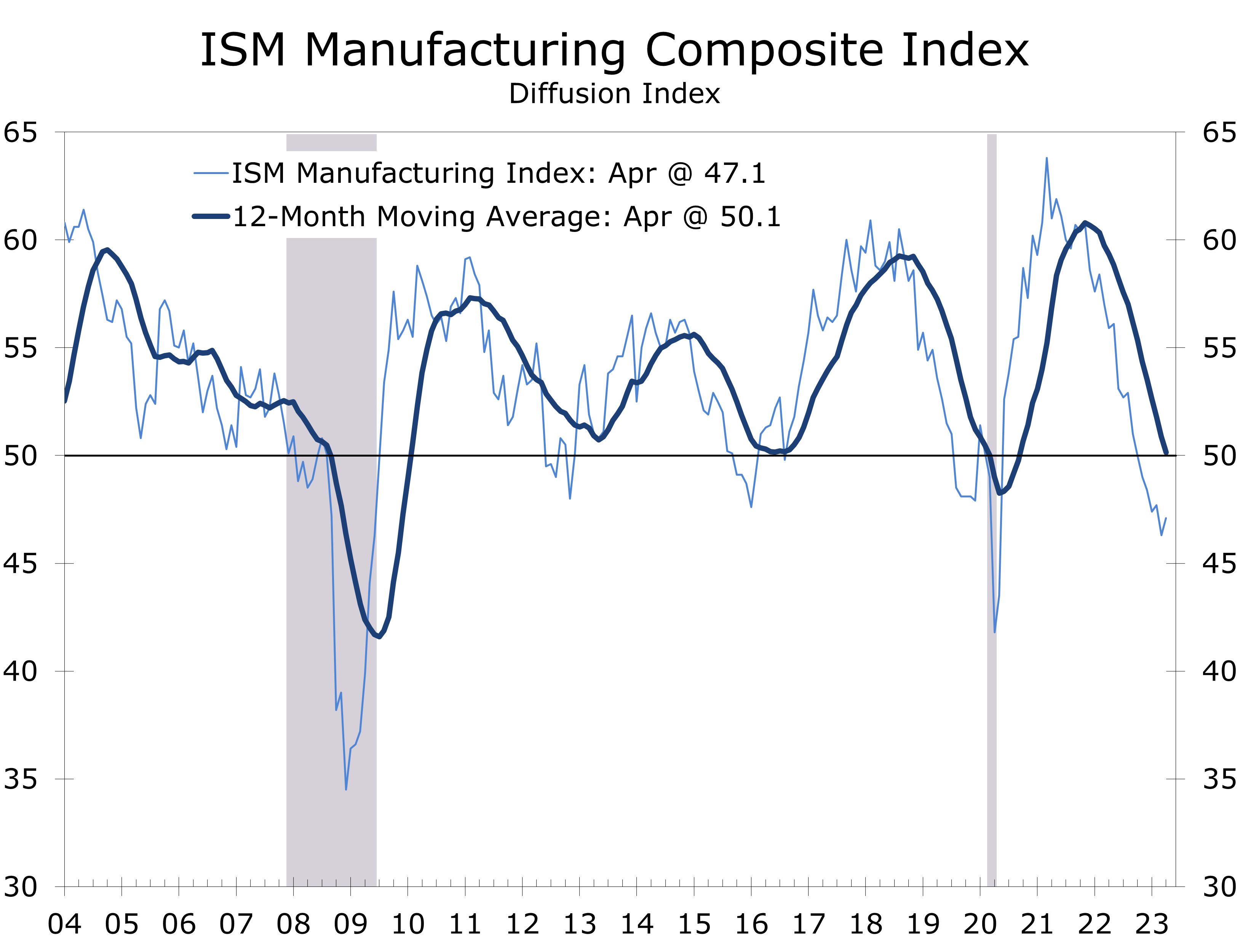

- The ISM Manufacturing index rose 0.8 points in April to 47.1, as the slowdown in the manufacturing sector moderated somewhat.

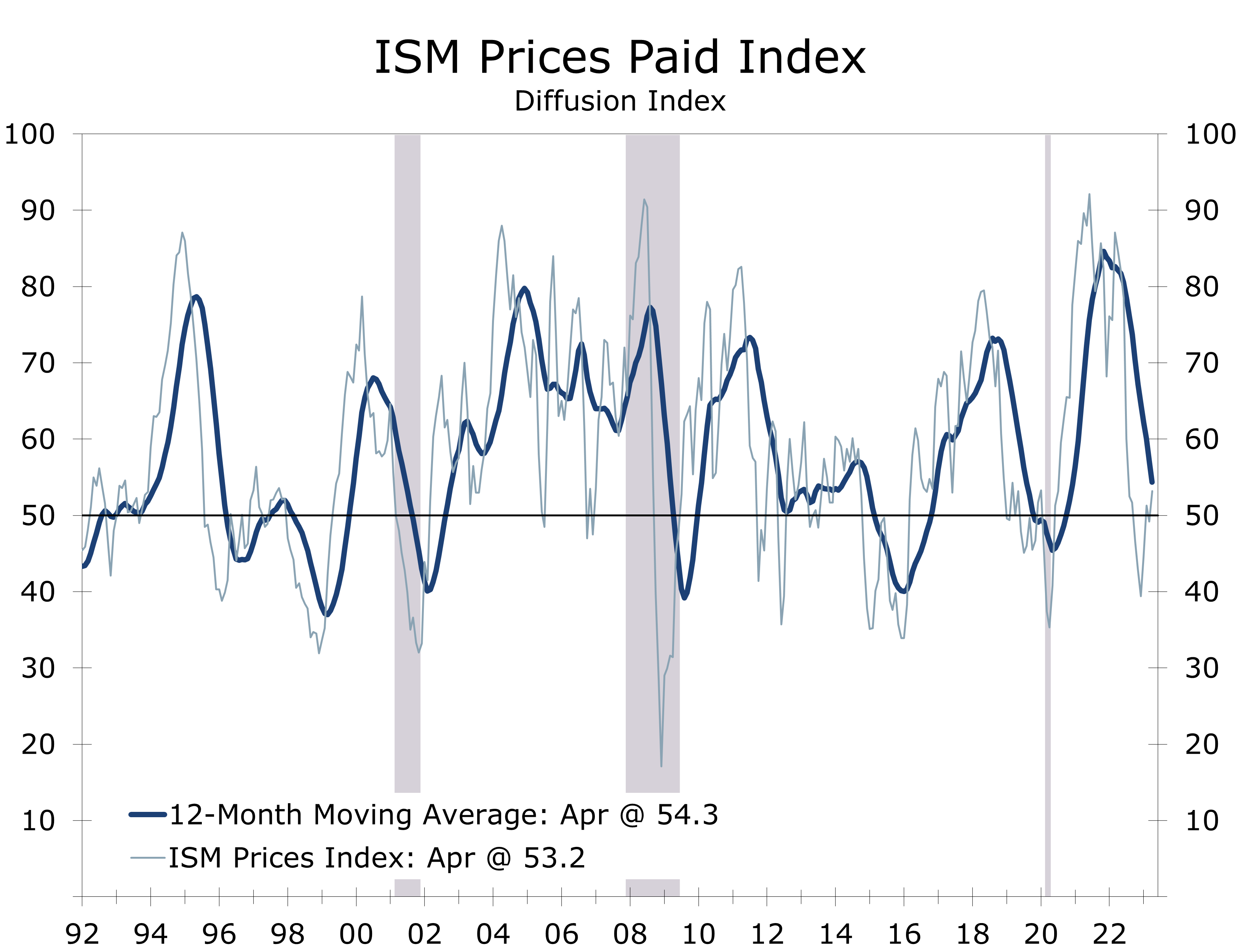

- While the index remained in contraction territory for a sixth consecutive month, the composition of April’s increase was quite strong. Seven of the ISM’s 10 components rose, with the prices paid series jumping 4 points to 53.2.

- The employment index also rose solidly, climbing 3.2 points to 50.2. Manufacturers cut 1,000 jobs in both February and March.

- Customer inventories rose 2.4 points to 51.3, and now look a bit high. Inventories have been falling at manufacturers and wholesalers, however.

- Manufacturers are working down their order backlogs and drawing down inventories to generate cash. The inventories index fell 1.2 points to 46.3, while order backlogs fell 0.8 points to 43.1.

Manufacturing activity improved slightly in April, with the ISM manufacturing survey rising 0.8 points to 47.1. The ISM survey is a diffusion index and provides insight into the breadth of strength or weakness within the factory sector. A reading above 50 means more manufacturers see conditions in their business improving than deteriorating.

April marks the sixth consecutive month the index has been below the key 50 break-even level, signaling a contraction in the manufacturing sector. Furthermore, the Institute for Supply Management notes any reading below 48.7 is generally consistent with a decline in overall economic activity, and the index has been below that level for the past five months.

Manufacturing has been unusually volatile in the wake of the Pandemic. Supply shortages had greatly extended delivery times, which helped pull the index to extraordinary heights as the economy reopened. Supply chains have normalized across many industries and the decline in the delivery times has tended to exaggerate the slide in the index to the downside.

Producers are actively working down their backlogs and reducing inventories to generate cash.

While manufacturing is showing a great deal of resilience, producers are actively working down their order backlogs and reducing inventories to generate cash. The shift may reflect some caution on the part of manufacturers in lieu of the troubles in the banking sector. There was no mention of credit conditions in the ISM report, however, and the reduction in backlogs might simply reflect normalizing supply chains.

Order backlogs surged following the pandemic, as demand recovered much faster than production. The order backlog index peaked about a year ago and has tumbled more than 20 points since. The latest data show the backlog index at just 43.1, a level that has typically been associated with manufacturing job loss.

Manufacturing activity is still being impacted by echoes from the pandemic, however. One of the reasons backlogs have slowed so rapidly is that deliveries of key raw materials and inputs are now much timelier and there are fewer shortages. One thing that remains in short supply, however, is labor and manufacturers appear to be in no hurry to reduce staff that has been so hard to hire and retain.

Backlogs are likely to continue to contract this year. While the advance first quarter GDP data noted a decline in inventories, all that drop occurred at manufacturers and wholesalers. Retailers saw inventories increase in the first quarter. That inventory build may be carrying over in the spring. Customers’ inventories rose 2.4 points in April to 51.3, which means more manufacturers report their customer inventories were too high than were too low, likely presaging a further pullback in orders.

On the plus side, export demand may be reviving. The export order index rose 2.2 points in April to 49.8. China’s reopening might possibly be boosting exports.

The 4-point rise in the prices paid component is one of the more notable swings in the April ISM report. The prices paid series had trended down sharply over the past year, as supply chains normalized and there were fewer bottlenecks and shortages. April’s reversal marks a break with this trend and might signal there is less price relief remaining in the pipeline. The Institute for Supply Management noted price increases for foundational purchased materials like steel, copper, plastics, and diesel fuel continue to put upward pressure on material costs.

The 4-point rise in the Prices Paid series signals there is less price relief left in the pipeline.

The ISM survey is one of the last pieces of data the Fed will see before they make their decision on interest rates this week. The FOMC is likely to take note of April’s 4-point rise in the prices paid component, as well as the resilience of manufacturing payrolls. We expect the Federal Reserve to hike the federal funds rate another quarter percentage point and look for the language in the policy statement and Chair’s press conference to suggest the interest rate decision at the June meeting remains an open question.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.