Wages Pressure is Proving Persistent

- Wage and benefit costs continue to rise at a highly elevated pace, making the Fed’s job of reining in inflation more difficult.

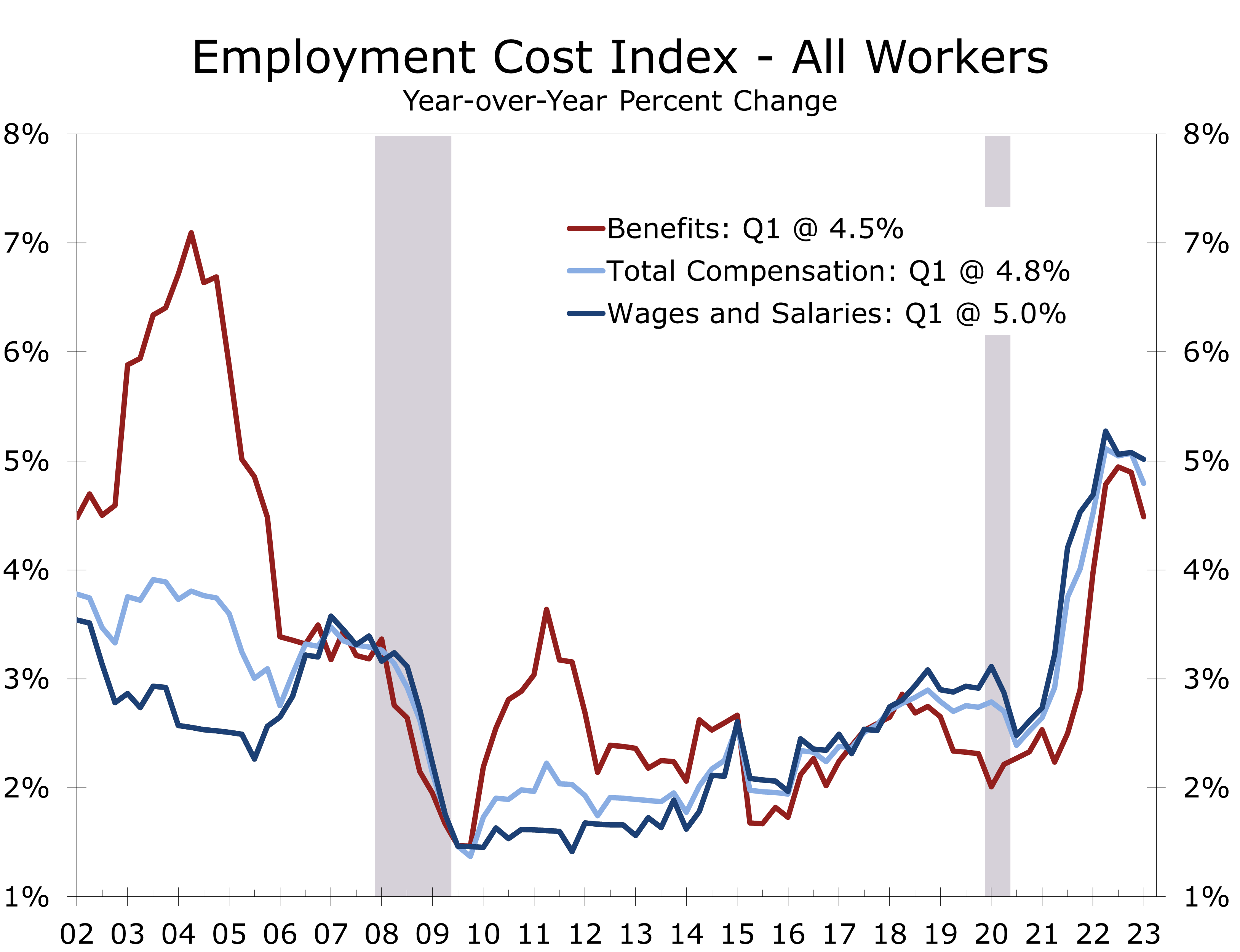

- The Employment Cost Index rose 1.2% in Q1, following a 1.1% rise the previous quarter.

- While the ECI eased slightly on a year-to-year basis, falling from 5.1% in Q4 to 5.0% in Q1, it remains too high. The ECI need to fall to 3.5% or less to bring inflation down to 2%.

- Wages rose 1.2%, the same pace as the prior quarter, while benefit cost ramped up to 1.2% from 1% in Q4.

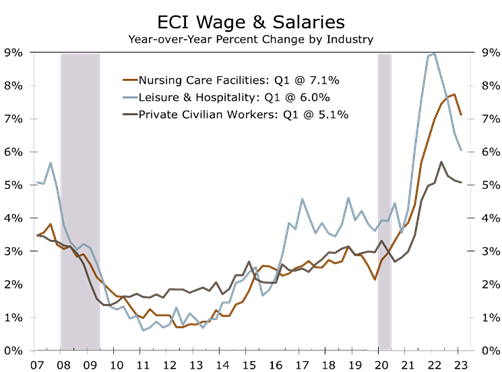

- While wages are up across the board, the sharpest increases continue to come from industries striving to staff back up from the pandemic, namely leisure & travel (+6.0%) and nursing care facilities (+7.1%).

- Wages are rising faster for nonunion workers (+5.1%) than for union workers (4.2%).

- The South Atlantic region posted the largest wage gains over the past year (+6.3%), following the West Coast and Mountain regions, where wages rose 5.6%.

The costs of providing wages and benefits to workers continues to rise at a pace that is inconsistent with the Fed’s mission to bring inflation back down to its 2% target. The Employment Cost Index rose 1.2% in Q1, which was above consensus expectations, and shows wage and benefit costs remain persistent across nearly every industry. Moreover, wages are rising the fastest in industries still striving to rehire workers lost during the pandemic, such as restaurants and bars, nursing homes and childcare centers.

Those latter industries accounted for the bulk of job growth during the first quarter. All are also relatively low paying industries, which is likely why they are the only major industries that have not regained their pre-pandemic employment levels. Since employers in these industries still need to add staff, we doubt wage pressures will fall off all that much in coming quarters.

Wages are rising fastest in industries still striving to restaff to their pre-pandemic levels.

On a year-to-year basis, overall compensation costs for all workers decelerated slightly, falling from 5.1% in Q4 to 5% in Q1. Compensation costs rose slightly in the goods sector, climbing from 5% to 5.1%, and declined slightly in the services sector, falling from 5.1% to 4.9%.

Wages and salaries in the private sector have risen 5.1% from March 2022, which was the same year-to-year pace as in Q4. Wages and salaries rose 5% from March 2021 to March 2022.

Wages and salaries are rising the fastest in industries striving to restaff their operations to pre-pandemic levels. Restaurants, bars, and hotels are one of the more notable examples. Wage gains in the leisure and hospitality sector peaked about a year ago at 9% but still climbed 6% year-to-year in the latest quarter, or nearly a percentage point more than for the private sector in general. Wages and salaries are up more dramatically at nursing care facilities, which saw staffing levels plummet during the pandemic.

Another area where wage gains could prove problematic is union workers. Union contracts tend to lag unanticipated swings in inflation. Pay for nonunion workers has risen 5.1% over the past year, easily outpacing pay for union workers (4.2%). The gap is even larger in the goods-producing sector, where wages for nonunion workers rose 2 full percentage points faster this past year (5.5%) than they did for union workers (3.5%). We suspect unions will attempt close this wage gap in future union negations, which will continue to put pressure on wage and benefit costs.

Union contracts tend to lag unanticipated swings in inflation and will catch up.

Wages rose fastest in regions of the country experiencing the strongest employment and population growth. Wages in the South Atlantic states, which includes Florida, Georgia, the Carolinas, and Virginia rose 6.3% over the past year. The Mountain region and West Coast both saw wages increase 5.6% over the past year, while wages in the Midwest (4.6%) and Northeast (4.4%) rose more modestly.

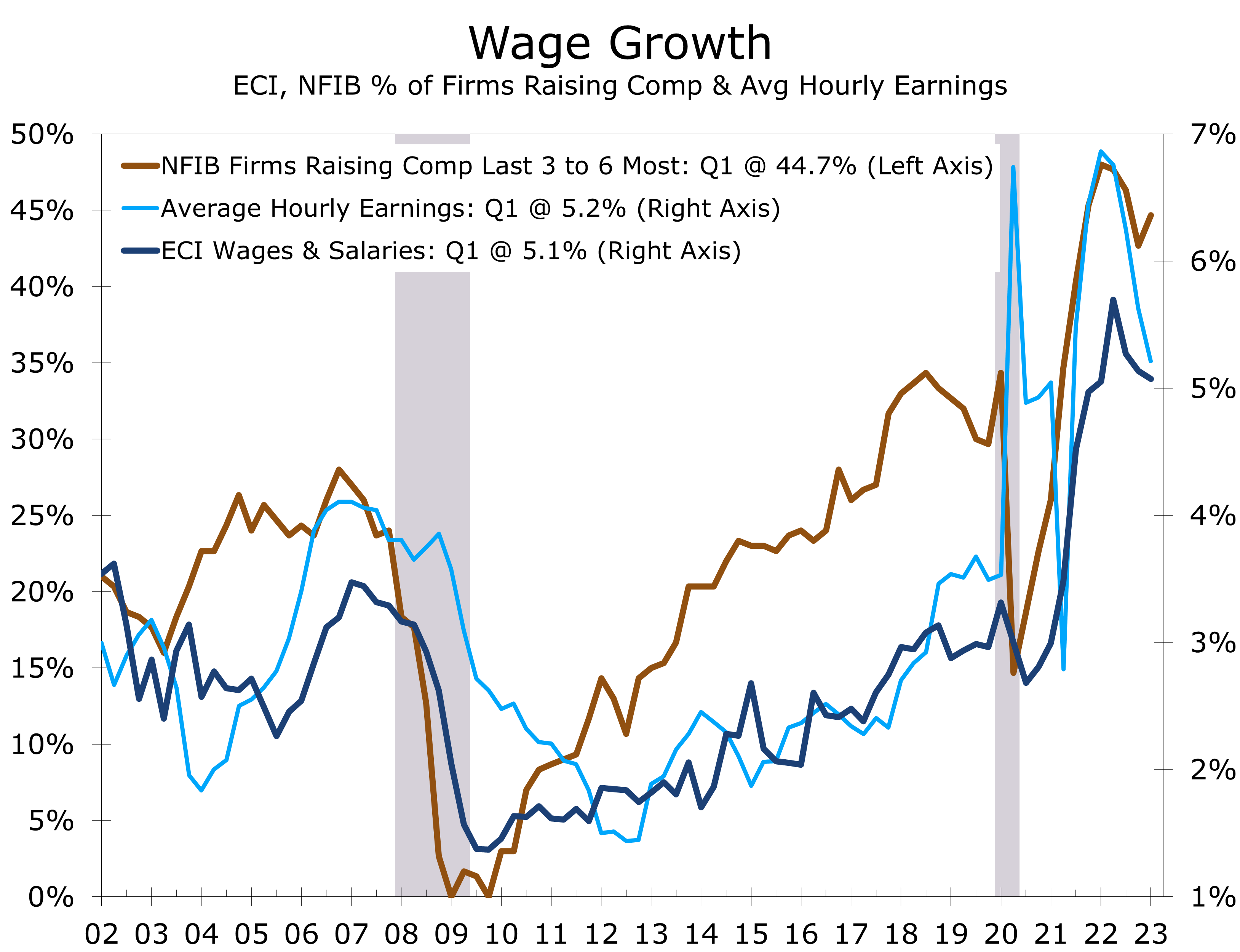

The persistent strength in wage gains will make the Fed’s job more difficult. Assuming productivity growth returns to its typical 1.5%, the Employment Cost Index would need to slow to around a 3.5% pace to be consistent with a 2% inflation rate. That appears to be a tall order right now. The latest NFIB survey of small businesses shows the share of firms raising compensation during the past 3 to 6 months ticked up during the first quarter and remains near historic highs.

The ECI needs to return to around a 3.5% pace to be consistent with the Fed’s 2% inflation target.

Absent a dramatic deterioration in the banking system this weekend or a plunge in Monday’s ISM report, we expect the Fed to hike the funds rate another quarter point at next week’s FOMC meeting. The wording of the policy statement and Powell’s press conference will likely suggest policymakers are keeping their options open for the June meeting and reemphasize that any cut in interest rates is a long way off.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.